Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

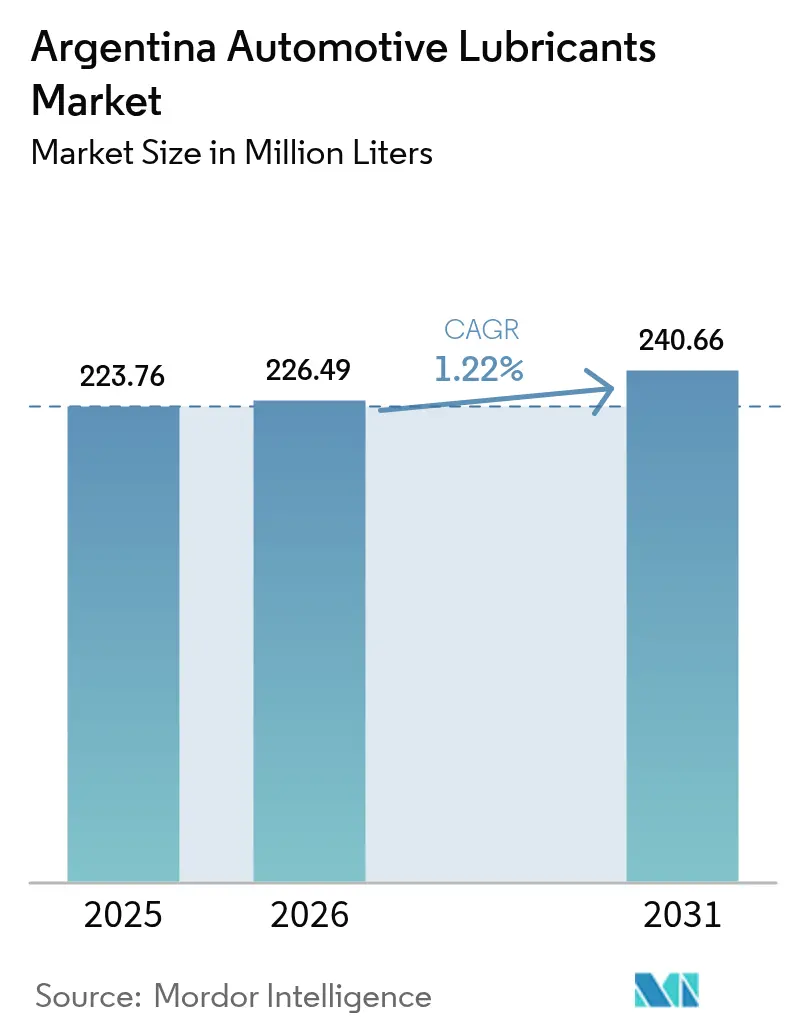

| Base Year Market Size (2025) | 223.76 Million Liters |

| Market Volume (2026) | 226.49 Million Liters |

| Market Volume (2031) | 240.66 Million Liters |

| Growth Rate (2026 - 2031) | 1.22% CAGR |

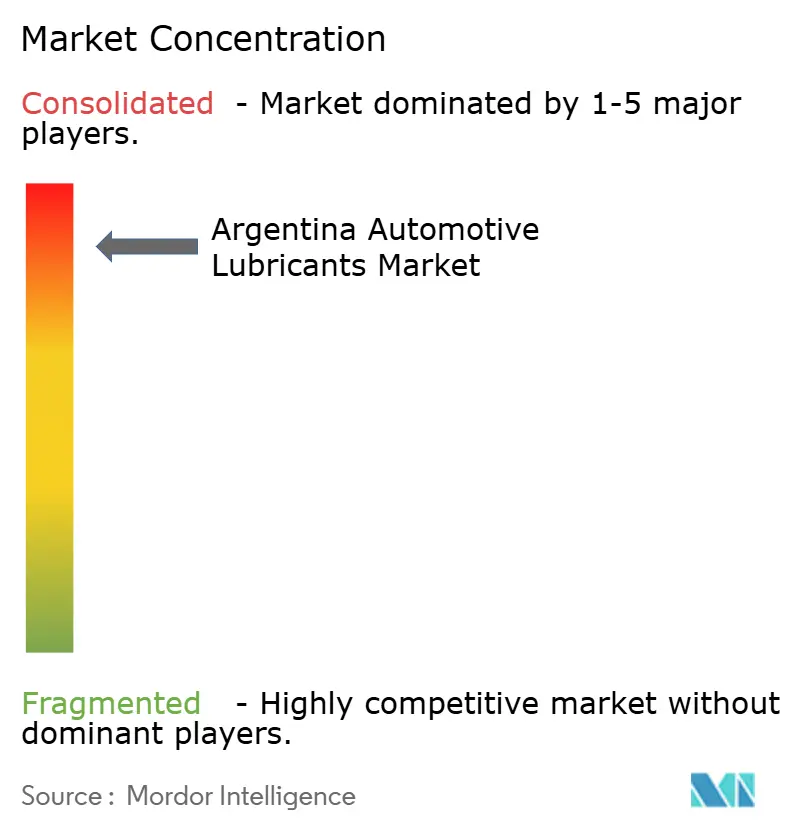

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Automotive Lubricants Market Analysis by Mordor Intelligence

The Argentina Automotive Lubricants Market size in 2026 is estimated at 226.49 million liters, growing from 2025 value of 223.76 million liters with 2031 projections showing 240.66 million liters, growing at 1.22% CAGR over 2026-2031. The Argentina automotive lubricants market continues to expand even as extended drain intervals, currency volatility, and the early adoption of electric vehicles temper volumetric growth. OEM‐approved synthetic grades that deliver fuel economy gains command higher margins, while an upswing in used-car imports, recovering domestic vehicle production, and a larger commercial vehicle fleet that services Vaca Muerta shale operations provide steady opportunities. The independent aftermarket’s share reinforces price sensitivity, yet local producers leverage national content incentives to market premium low-viscosity products. At the same time, ongoing consolidation among downstream assets positions integrated firms to optimize supply chains and widen distribution reach.

Key Report Takeaways

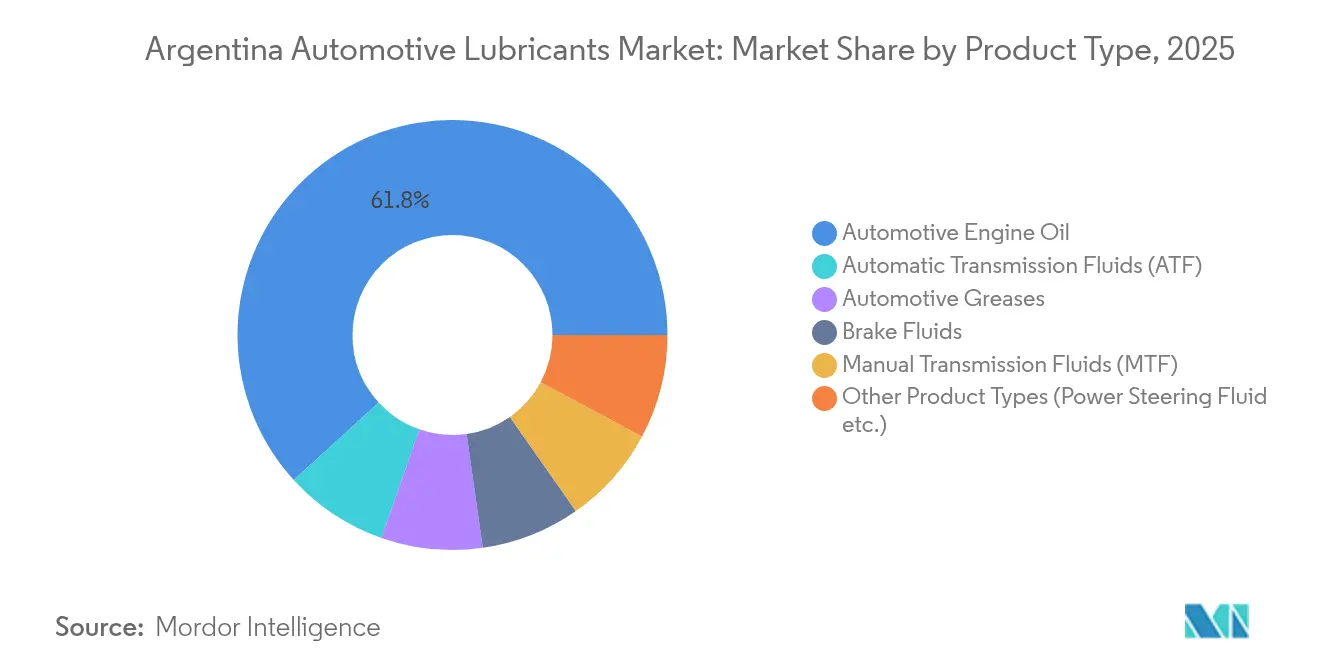

- By product type, automotive engine oil led with 61.78% revenue share of the Argentina automotive lubricants market in 2025. Automatic transmission fluids recorded the fastest projected CAGR at 1.9% through 2031.

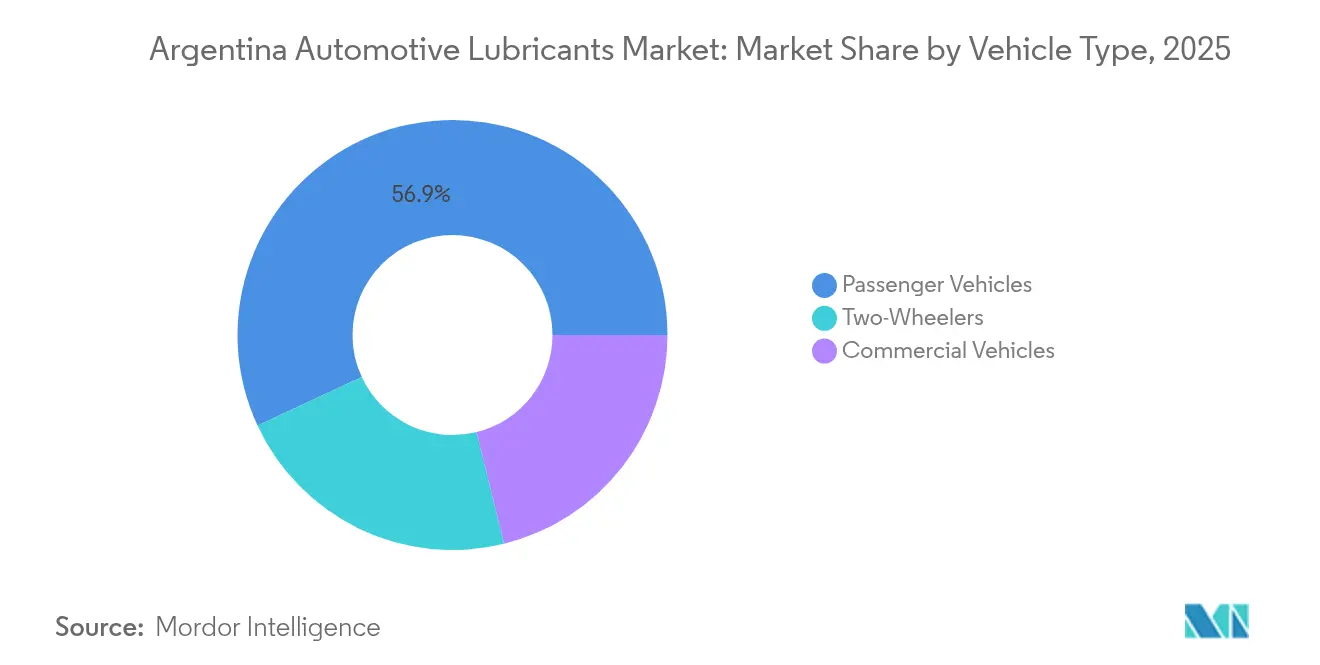

- By vehicle type, passenger cars held 56.92% of the Argentina automotive lubricants market share in 2025, while two-wheelers posted the highest forecast CAGR at 1.69% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated shift to low-viscosity, fuel-economy lubricants | +0.30% | National, with early adoption in Buenos Aires metropolitan area | Medium term (2-4 years) |

| Resurgence of used-car imports boosting service fill demand | +0.20% | National, concentrated in border regions and major urban centers | Short term (≤ 2 years) |

| OEM factory-fill contracts linked to local content rules | +0.20% | National, with manufacturing hubs in Córdoba and Buenos Aires | Long term (≥ 4 years) |

| Growing penetration of synthetic blends in motorcycle segment | +0.10% | National, with higher adoption in urban motorcycle-dense areas | Medium term (2-4 years) |

| Expansion of Vaca Muerta drilling logistics fleet (diesel CVs) | +0.10% | Neuquén province and Patagonia region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Low-Viscosity Fuel-Economy Lubricants

Argentina’s shift toward 0W-XX and 5W-XX grades intensifies as OEMs, led by Japanese and European brands, extend recommended service intervals to 10,000–12,000 km[1]TotalEnergies Argentina, “Marketing & Services,” totalenergies.com.ar . Domestic supplier YPF responds with TEC-based formulations that meet newer ACEA and API specifications, illustrating how national content rules stimulate local innovation. As automatic transmissions account for roughly 35% of new-car registrations, specialized low-viscosity ATF demand rises, giving blend plants reason to expand synthetic capacity. Although longer drain intervals lower refill frequency, the higher price points of premium synthetics lift revenue per liter, partially offsetting volume erosion. Over the medium term, the Argentina automotive lubricants market benefits from stronger brand differentiation predicated on performance credentials.

Resurgence of Used-Car Imports Boosting Service-Fill Demand

Eased import rules and dollar-denominated payment windows have triggered a surge in used vehicles that require immediate oil, filter, and coolant changes to adapt to local fuel quality. With the average fleet age now 12 years, service centers in border provinces and metropolitan hubs see higher volumes of high-mileage engines that favor thicker base stocks and additive packages targeting wear control. Independent retailers emphasize multi-grade mineral and semi-synthetic offerings that balance price and protection, capturing budget-conscious drivers affected by lingering inflation. Distributors such as LAC have segmented their four-zone network to ensure timely product availability across Santiago del Estero, Tucumán, and Entre Ríos, underscoring the logistical complexity of meeting dispersed demand. As import volumes stabilize, the Argentina automotive lubricants market absorbs incremental service-fill consumption despite slower growth in new-car sales.

OEM Factory-Fill Contracts Linked to Local Content Rules

Argentina’s local content law mandates progressively higher domestic value added in passenger-car assembly, prompting OEMs to source lubricants from in-country plants. TotalEnergies Argentina supplies roughly one-third of factory fills through contracts with Peugeot-Citroën, Hino, and multiple motorcycle brands. YPF leverages its 244,000 m³ per year base-oil capacity to bundle feedstock and finished lubricants, lowering OEM procurement risk. Automakers reward such integration by granting multi-year agreements that assure volume offtake and joint R&D. Long-duration warranties—Toyota’s “Toyota 10” extends to 200,000 km—anchor post-sale demand, yet also formalize extended drain intervals, forcing suppliers to engineer higher-performance fluids that sustain additive strength over more miles.

Growing Penetration of Synthetic Blends in Motorcycle Segment

Two-wheeler registrations climb as commuters seek fuel-efficient transport amid high gasoline prices, pushing motorcycle lubricant sales ahead of overall market growth. YPF’s RÖD line, rolled out in August 2025, covers 2-stroke and 4-stroke engines with viscosity grades tuned to Argentina’s broad climate zones. Urban riders gravitate toward semi-synthetics that moderate cost yet deliver temperature stability in stop-and-go traffic, while long-distance enthusiasts adopt full synthetics for extended touring intervals. Regulatory exemptions that allowed nearly 27,600 motorcycles lacking combined-brake systems into the 2025 market sustain fleet expansion. Together, these factors create a steady revenue pocket even as passenger-car lubricant volumes plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-driven price volatility hurting consumer upgrade intent | -0.40% | National, with higher impact in lower-income regions | Short term (≤ 2 years) |

| Extended oil-change intervals mandated by OEM warranty terms | -0.20% | National, concentrated in newer vehicle segments | Long term (≥ 4 years) |

| Rising EV adoption in urban passenger-car parc | -0.10% | Buenos Aires, Córdoba, and major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency-Driven Price Volatility Hurting Consumer Upgrade Intent

Peso devaluation multiplied by triple-digit inflation through 2024 compressed disposable income and pushed more than half the population below the poverty line. Drivers cut mileage by 10%, delaying oil changes and prioritizing mineral products over costlier synthetics. Blend plants that import base oil in USD grapple with unstable input costs, often alternating between Group I and Group II stocks to protect margins. Although inflation cooled to below 3% monthly in mid-2025, consumers remain price sensitive, slowing premium product uptake. As long as purchasing power lags wage growth, the Argentina automotive lubricants market endures a deflationary tilt toward volume retention strategies.

Extended Oil-Change Intervals Mandated by OEM Warranty Terms

Automakers lengthen service schedules to reduce ownership costs and align with cleaner engine technologies. BMW’s digital service records and Toyota’s ten-year warranty both stipulate higher-tier lubricants capable of enduring 10,000 km drains[2]BMW Argentina, “Garantía y Mantenimiento Total BMW,” bmw.com.ar. Each extension removes at least one workshop visit across a typical ownership cycle, shaving aggregate lubricant demand even as per-liter revenue rises. Dealers capture the remaining factory-approved business, narrowing aftermarket share for independent garages that usually depend on more frequent oil changes. Over the long term, the Argentina automotive lubricants market must shift emphasis from refill volumes to value-added services such as in-field oil analytics and predictive maintenance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Dominance with ATF Upside

Engine oil generated 61.78% of 2025 volume, underscoring its central role in the Argentina automotive lubricants market. The segment benefits from an 11 million-unit light-vehicle fleet—now averaging 12 years—that relies on regular top-ups to manage wear. YPF’s Elaion and Extravida product families cover monograde mineral through 0W-16 full synthetics, enabling shelf-presence across service channels. Conventional multi-grade 15W-40 still serves older diesel pickups that frequent Patagonia’s harsh routes, while lower-viscosity 5W-30 grades win share among newer turbocharged gasoline engines. On the upside, automatic transmission fluids advance at a 1.9% CAGR, reflecting an eight-fold rise in automatic-gearbox penetration over the past decade. Lubricant blenders have introduced multi-vehicle synthetic ATFs that simplify inventory for workshops, especially in provincial cities where service bays handle mixed fleets. Manual-transmission and gear oils remain relevant for Argentina’s enduring stick-shift parc, but the growth curve bends toward automatic systems as urban congestion triggers consumer preference for clutch-free driving.

Greases, brake fluids, and specialty power-steering fluids form the market’s long-tail. Disc-brake upgrades across economy hatchbacks sustain DOT-4 brake-fluid replacements at two-year intervals, while lithium-complex greases support hub and chassis lubrication in heavy trucks servicing Vaca Muerta rigs. As OEMs migrate to electric power-steering systems, demand for hydraulic steering fluid levels off, but remains steady in light commercial vans. Product-mix evolution thus mirrors Argentina’s diverging fleet demographics: aging vehicles that require mineral and semi-synthetic upkeep coexist with modern platforms demanding premium synthetics. Local content incentives further encourage Argentine formulators to integrate additive packages at domestic blend plants, embedding resilience against foreign-exchange gyrations and tightening control of the Argentina automotive lubricants market supply chain.

By Vehicle Type: Passenger-Car Core and Two-Wheeler Momentum

Passenger cars absorbed 56.92% of 2025 demand thanks to their numerical weight in registrations and routine service patterns that favor 4-to-6-quart sump capacities. Independent garages capture the majority of these oil changes, aligning product offerings with household budgets. That dynamic explains why semi-synthetic 10W-40 remains ubiquitous even as OEMs advocate 5W-30 full synthetics for late-model turbo engines. Commercial vehicles account for roughly one-third of volumes and are pivotal to lubricants’ heavy-duty grade mix. Diesel-powered trucks that shuttle equipment to and from Neuquén’s shale wells require high-TBN blends to combat soot and fuel-dilution challenges, while city buses use low-ash formulations compatible with selective catalytic reduction systems. Output of heavy vehicles grew in the first four months of 2025 as logistics operators expanded fleets to serve energy exports and rising intra-Mercosur trade.

Two-wheelers, though a distant third in sheer liters, hold the fastest 1.69% CAGR through 2031. Affordability, maneuverability in gridlock, and low fuel consumption drive their appeal, particularly in Córdoba and Greater Buenos Aires. The segment’s lubricant needs vary from mineral SAE 40 for 2-stroke mopeds to cutting-edge 0W-20 full synthetics for performance 4-stroke models. Regulatory leniency that allowed tens of thousands of non-ABS units onto roads in 2025 inadvertently broadened the installed base and thus aftermarket consumption. Lubricant marketers tailor small-pack SKUs—1 liter to 1.2 liter bottles—for this customer set, often bundling free fuel-additive sachets to encourage brand loyalty. Consequently, as urban mobility trends intersect with economic austerity, the Argentina automotive lubricants market secures a sustainable two-wheeler growth vector, even as passenger-car volumes plateau and drain-interval extensions take hold.

Geography Analysis

Buenos Aires province anchors the majority of the Argentina automotive lubricants market, combining the country’s densest vehicle parc, its largest port complex, and multiple blend facilities. YPF’s La Plata refinery integrates Group I base-oil output with lube-oil blending, enabling cost-efficient supply to 380-plus YPF Boxes service centers spread across the metropolitan grid. Proximity to the Dock Sud and Zárate terminals further streamlines additive imports and finished-lube exports into neighboring Uruguay and Paraguay. Automakers in the Pilar-Escobar corridor secure just-in-time deliveries of factory-fill lubricants, reinforcing the province’s strategic role in OEM supply chains.

Neuquén province shows notable regional growth as an outlet, propelled by Vaca Muerta shale development. Crude exports reached USD 1.801 billion in H1 2025, magnifying demand for diesel engine oils, hydraulic fluids, and greases used in drilling-rig maintenance. YPF’s Directo Añelo distribution hub holds tailored inventories of CI-4+ and CK-4 lubricants alongside field-laboratory capability for used-oil analysis. Service contractors operating 24/7 under extreme dust and temperature fluctuations rely on extended-life synthetics to reduce downtime, thereby swelling per-truck lube consumption. Supply resilience in Patagonia also benefits from improved logistics via National Route 22, shortening lead times from blend plants in Luján de Cuyo.

Córdoba maintains its historical relevance through automotive assembly and expansive soy and corn agriculture. OEM agreements with lubricant producers often stipulate dual-channel delivery—factory fill and dealer network—creating steady throughput for the province’s parts distribution centers. Agro-machinery fleets consume monograde SAE 30 hydrauli-trans oils during planting and harvest seasons, producing predictable seasonal spikes. Meanwhile, northern border provinces such as Formosa and Misiones capture new demand linked to imported used cars channeled through Paraguay. Dispersed demand patterns oblige distributors to maintain mixed modal transport—road tanker, ISO container, and railcar—highlighting the geographic diversity that characterizes the Argentina automotive lubricants market.

Competitive Landscape

The Argentina automotive lubricants market exhibits high concentration as vertically integrated YPF remains the clear leader. Its 244,000 m³ per year base-oil capacity, eight blend plants, and branded service network underpin cost advantages and nationwide reach. The firm’s USD 327 million acquisition of Mobil Argentina in February 2025 secured additional upstream acreage and eliminated a formidable competitor. YPF has since rationalized overlapping SKUs and funneled premium base stocks into its TEC-enhanced Elaion range to protect margins across supermarket and e-commerce channels.

TotalEnergies Argentina holds a significant position but differentiates through OEM alliances. Supplying roughly 30% of domestic factory fills gives the French major a technical edge: every homologation cycle transfers new formulation know-how into its Quartz and Hi-Perf aftermarket lines. The company is also trialing field sensors that monitor oil oxidation in ride-share fleets, bundling analytics with bulk-oil purchases to lock in long-term workshop contracts. In parallel, Raízen’s acquisition of Shell’s downstream assets adds 665 filling stations and a Luján blend plant, yet the Brazilian joint venture has signaled intent to divest, creating uncertainty that rivals aim to exploit.

Regional challengers leverage M&A to build scale. Trafigura’s Puma Energy network mobilizes 400 sites and a newly expanded Avellaneda lube plant devoted to Group II derivatives. Vibra’s Brazilian base-oil exports target Argentina’s small and mid-size blenders, injecting competitive feedstock alternatives. Still, barriers to entry remain high; local content mandates, technical homologation fees, and retail shelf-space constraints collectively shield incumbents. Against this backdrop, competition increasingly centers on service models—used-oil analytics, drain-interval optimization, and mobile quick-lube vans—that deepen customer ties beyond commodity supply.

Argentina Automotive Lubricants Industry Leaders

BP PLC (Castrol)

ExxonMobil Corporation

Shell Plc

TotalEnergies

YPF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Chevron Products Company, a division of Chevron U.S.A. Inc. has partnered with YPF, appointing it as the exclusive distributor of NEXBASE base oils in Argentina. This collaboration is set to enhance the supply chain and boost the availability of premium base oils, driving growth in the country's automotive lubricants market.

- January 2025: YPF acquired Mobil Argentina from ExxonMobil and QatarEnergy for USD 327 million, gaining a 54% stake in the Sierra Chata concession in Vaca Muerta. The rebranding of Mobil Argentina to SC Gas under YPF's ownership is expected to strengthen its position in the Argentine automotive lubricants market by enhancing supply chain capabilities and market reach.

Argentina Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is the Argentina automotive lubricants market in 2026?

The market totals 226.49 million liters in 2026 and is forecast to reach 240.66 million liters by 2031, posting a 1.22% CAGR.

What is the largest product category in Argentine lubricants?

Engine oil dominates with 61.78% of 2025 volume, while automatic transmission fluids are the fastest-growing sub-segment.

Which region shows the fastest demand growth?

Neuquén province leads growth due to Vaca Muerta shale activity that boosts heavy-duty diesel lubricant consumption.

How is currency volatility affecting lubricant sales?

Devaluation and inflation have pushed consumers toward lower-priced mineral grades, moderating premium-product uptake in the near term.

What impact do extended OEM warranties have on lubricant volumes?

Longer drain intervals reduce annual oil-change frequency, shifting market focus from volume to higher-margin, long-life synthetics.

Page last updated on: