Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.91 Billion |

| Market Size (2031) | USD 21.25 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amines Market Analysis by Mordor Intelligence

Amines market size in 2026 is estimated at USD 16.91 billion, growing from 2025 value of USD 16.15 billion with 2031 projections showing USD 21.25 billion, growing at 4.69% CAGR over 2026-2031. This sustained expansion is supported by resilient industrial demand, stricter environmental regulations that favor cleaner chemistries and a growing pipeline of high-value applications such as carbon-capture solvents. Rising investments in semiconductor fabrication, large-scale agricultural modernization and widespread adoption of bio-based personal-care surfactants are expanding both volume and value opportunities in the amines market. Producers are improving energy efficiency and integrating renewable feedstocks to manage volatile ammonia and ethylene prices while complying with emerging volatile organic compound limits across major economies. Leading suppliers are also channeling capital toward ultra-pure electronics-grade capacities to meet the stringent metal specifications required by next-generation chips, highlighting a visible shift from commodity production toward specialized solutions that offer superior margin potential.

Key Report Takeaways

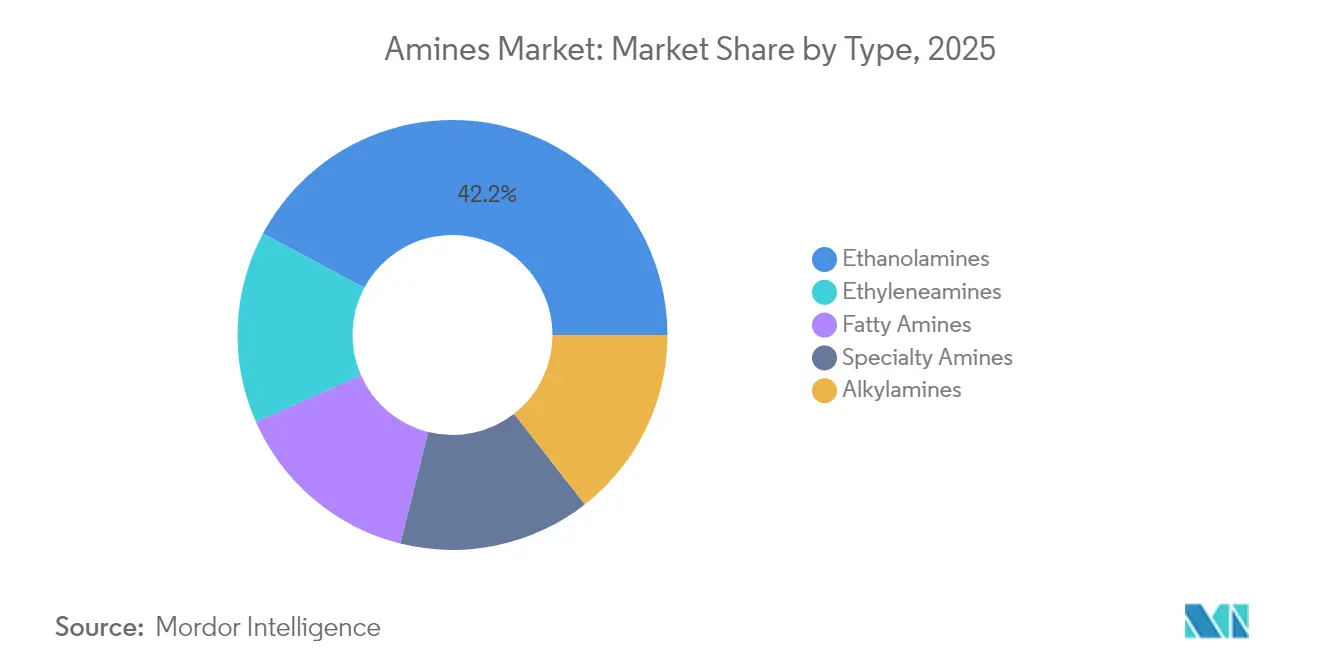

- By type, ethanolamines led with 42.18% amines market share in 2025, whereas specialty amines are projected to post the fastest 4.84% CAGR through 2031.

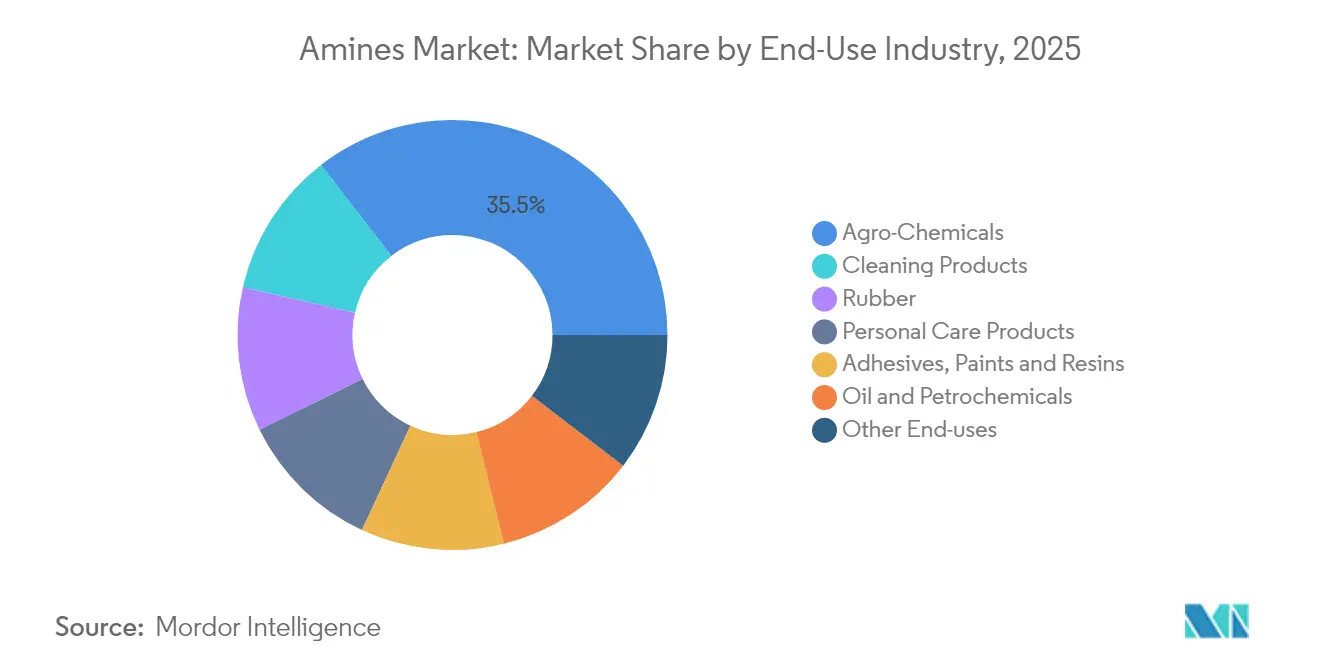

- By end-use industry, agro chemicals commanded 35.12% share of the amines market size in 2025; cleaning products is expected to accelerate at a 5.31% CAGR to 2031.

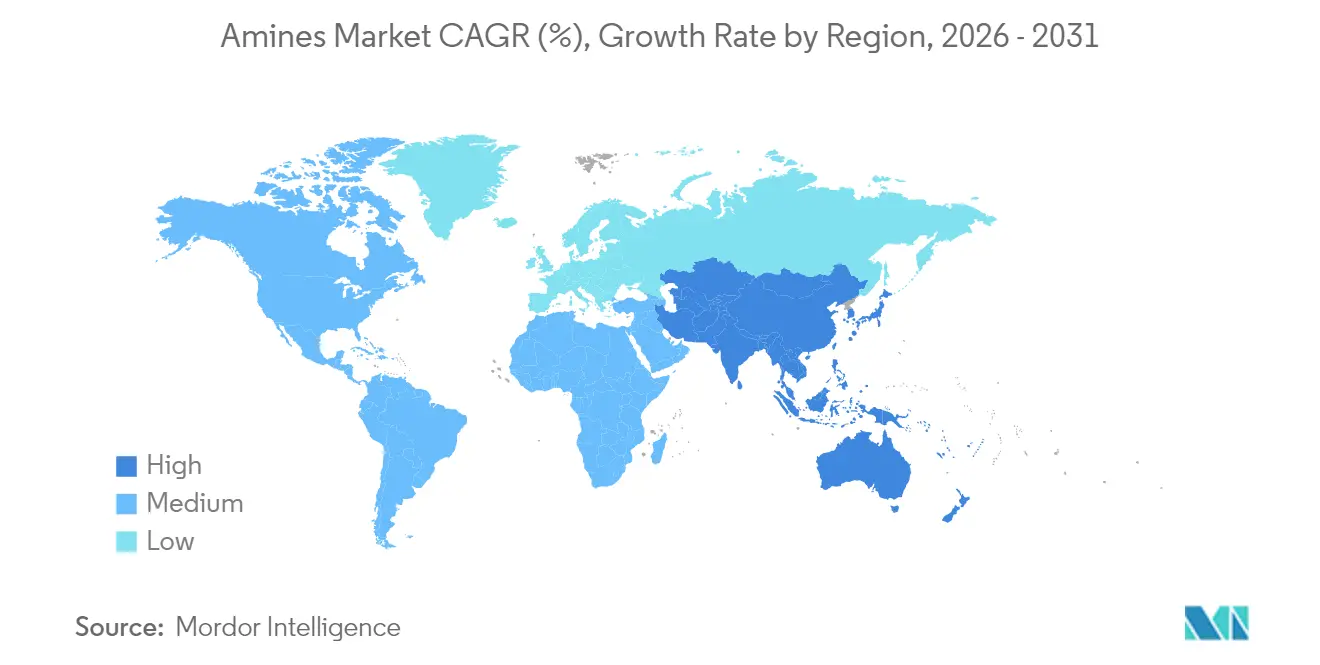

- By geography, Asia Pacific accounted for 38.55% revenue in 2025 in the amines market and is forecast to grow at the highest 5.64% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Amines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from Asian personal-care formulators | +0.80% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Rapid pesticide adoption in emerging agriculture hubs | +1.20% | Asia Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Infrastructure boom spurring construction chemicals | +0.60% | Global, with concentration in Asia Pacific and Middle East | Medium term (2-4 years) |

| Electronics-grade amines for advanced semiconductor fabs | +0.90% | Asia Pacific, North America | Short term (≤ 2 years) |

| On-site green-hydrogen-derived amines pilots | +0.40% | North America, Europe, with selective Asia Pacific deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Asian Personal-Care Formulators

Amino acid-based surfactants have outpaced traditional sulfate systems, recording 18% average annual growth since 2010. Asian formulators are mainstreaming glutamate and alaninate derivatives that offer low irritation and high biodegradability, forcing amine suppliers to expand bio-based lines with International Sustainability and Carbon Certification (ISCC-PLUS) credentials. Nouryon’s certified production of green ethylene oxide and ethanolamines illustrates how plant operators are realigning portfolios toward clean-label formulations[1]Nouryon, “ISCC-PLUS certification at Stenungsund site,” nouryon.com . In tandem, multifunctional amine oxides are gaining ground in shampoo, body-wash and household categories as manufacturers pursue high-foaming yet mild profiles. With middle-class consumers gravitating toward products boasting a natural-origin index approaching 100%, the amines market is set to deepen its role as a pivotal enabler of Asia’s fast-growing clean-beauty ecosystem.

Rapid Pesticide Adoption in Emerging Agriculture Hubs

Modern farming practices in Asia Pacific and South America require precision chemical inputs, lifting demand for amine-based pesticide salts and emulsifiers, supporting growth in the amines market. Novel decentralized ammonia plants powered by renewable electricity are lowering logistics costs and improving regional supply security, notably in Brazil and India. CF Industries and POET’s pilot of low-carbon ammonia fertilizer demonstrates the agronomic and sustainability pay-off of integrating green hydrogen pathways. Such developments bolster long-term offtake for ethanolamines, alkylamines, and fatty amines used in herbicides, insecticides, and seed-treatment agents.

Infrastructure Boom Spurring Construction Chemicals

Large-scale urbanization projects across Asia and the Middle East continue to elevate demand for epoxy systems, concrete plasticizers and corrosion inhibitors that rely on polyamines or amidoamines as curing agents. Evonik’s Ancamine series allows structural adhesives to set at 70 °C, enabling faster project cycles. Green-building mandates in China, India and the Gulf Cooperation Council markets are also driving interest in bio-based curing agents derived from vegetable oils, while graphene-enhanced rubber composites formulated with specialty amines deliver superior tensile strength for bridge bearings and rail pads used in extreme climates.

Electronics-Grade Amines for Advanced Semiconductor Fabs

The shift toward 3 nm and below process nodes calls for quaternary amines and amine oxides with parts-per-billion metal impurities. Huntsman has upgraded its Conroe, Texas plant to deliver E-GRADE volumes tailored for lithography cleaning and developer baths. Given that Asia hosts over 70% of global leading-edge capacity additions slated through 2028, local procurement of ultra-pure amines is becoming a supply-chain imperative. Short qualification cycles in chip fabs mean that suppliers capable of consistently meeting sub-ppb thresholds are locking in multi-year contracts, magnifying the growth stimulus for the amines market in the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to wood-free paper & digital documentation | -0.30% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Volatile ammonia & ethylene feedstock pricing | -0.70% | Global | Short term (≤ 2 years) |

| Stricter amine VOC/odor regulations | -0.50% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Wood-Free Paper & Digital Documentation

Declining office-paper consumption in developed economies is dampening demand for amine-based pulp bleaching agents and paper coatings. Companies are reallocating volumes toward faster-growing personal-care and construction segments to cushion the long-term drag. BASF’s decision to reconfigure legacy amine assets toward specialty chemicals highlights the industry’s proactive adjustment to this structural shift.

Volatile Ammonia & Ethylene Feedstock Pricing

Natural-gas price swings translate directly into ammonia and ethylene cost variability, compressing producer margins. Anhydrous ammonia prices have tracked gas markets lower in recent quarters, but geopolitical risks—such as potential Strait of Hormuz disruptions impacting global ammonia trade—keep cost projections uncertain. Suppliers are hedging through forward contracts, portfolio diversification and pilot investments in electrolysis-based green-ammonia routes that promise greater cost stability once scaled.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ethanolamines Lead While Specialty Amines Accelerate

Ethanolamines captured 42.18% of the overall amines market in 2025, owing to their indispensable role in gas sweetening, personal-care surfactants and corrosion inhibitors. Steady demand from natural-gas treatment and triethanolamine-based cement additives underpins a robust baseline, even as newer uses in carbon-capture solvents emerge. The segment’s scale gives leading suppliers cost leverage and operational synergies across derivative chains ranging from ethoxylates to morpholine. In contrast, specialty amines are projected to post the fastest 4.84% CAGR through 2031, propelled by niche applications in electronics, pharmaceuticals and advanced composites.

Producers are installing multipurpose reactors capable of quick changeovers between high-purity morpholines, diamines and chiral amine intermediates. Evonik’s expansion in Nanjing exemplifies this pivot toward higher value-added molecules. Concurrently, academic breakthroughs such as ruthenium/triphos catalysts achieving 90% yields on renewable feedstocks promise to widen the sustainable feedstock pool for specialty grades. The interplay of scale in ethanolamines and growth in specialty amines underpins the balanced long-term trajectory of the amines market.

By End-Use Industry: Agriculture Dominance Meets Cleaning Innovation

Agro chemicals accounted for 35.12% of the amines market size in 2025 as global food-security imperatives spurred large-scale adoption of amine-salt herbicides and emulsifiers. Fertilizer producers utilize monoethanolamine scrubbing to eliminate acid gases, safeguarding synthesis catalysts and improving plant uptime. Downstream, pesticide formulators depend on fatty and alkyl amines to reduce spray drift and enhance leaf cuticle penetration, supporting higher crop yields.

Cleaning products, though smaller in absolute terms, are on track to grow 5.31% annually through 2031, driven by sulfate-free personal-care and plant-based household formulations. Syensqo’s naturally derived surfactant line underscores the appeal of mild, eco-labeled ingredients. Parallel regulatory scrutiny of 6PPD antioxidants in the tire industry has prompted a search for alternative amines that maintain ozone resistance without generating harmful transformation products. These shifts emphasize how evolving health and sustainability standards are reshaping demand patterns within the amines market.

Geography Analysis

Asia Pacific retained its dual leadership position, generating 38.55% of global revenue in 2025 and expanding at a 5.64% CAGR through 2031. China’s 45.52 million t ammonia capacity anchors the region’s raw-material advantage. India’s specialty chemicals champions, including Alkyl Amines and Balaji Amines, operate more than 20 plants and export to over 100 countries, leveraging cost-competitive manufacturing. Semiconductor expansions across Taiwan, South Korea and mainland China are pushing demand for electronics-grade amines, while ASEAN nations add incremental growth through pharmaceuticals, agro chemicals and household products. BASF’s planned USD 10 billion Zhanjiang Verbund project, powered entirely by renewable electricity, illustrates how multinationals intend to capture enduring regional upside.

North America represents a mature yet strategically vital cluster, with rising investments in blue ammonia facilities integrated with carbon-capture systems. The United States is expected to quadruple ammonia capacity by 2030. This expansion safeguards domestic fertilizer supply and provides a local feedstock base for ethanolamine and urea derivatives. Meanwhile, Canada’s abundant hydropower positions it as a contender for low-carbon amine production targeting both domestic and export markets.

Europe continues to pursue circular-economy objectives, driving innovations in bio-based intermediates and energy-efficient reactors. Nouryon’s ISCC-PLUS certification for green ethylene oxide supports regional demand for eco-labeled surfactants. The European Commission’s stricter VOC targets are encouraging formulators to substitute conventional volatile amines with higher-flashpoint derivatives that meet performance criteria.

The Middle East and Africa benefit from natural-gas feedstock availability, enabling competitively priced ammonia and downstream amine chains, especially in Saudi Arabia and Oman.

South America’s focus on soybean and corn cultivation assures steady consumption of herbicidal amine salts, with Brazil and Argentina leading uptake.

Competitive Landscape

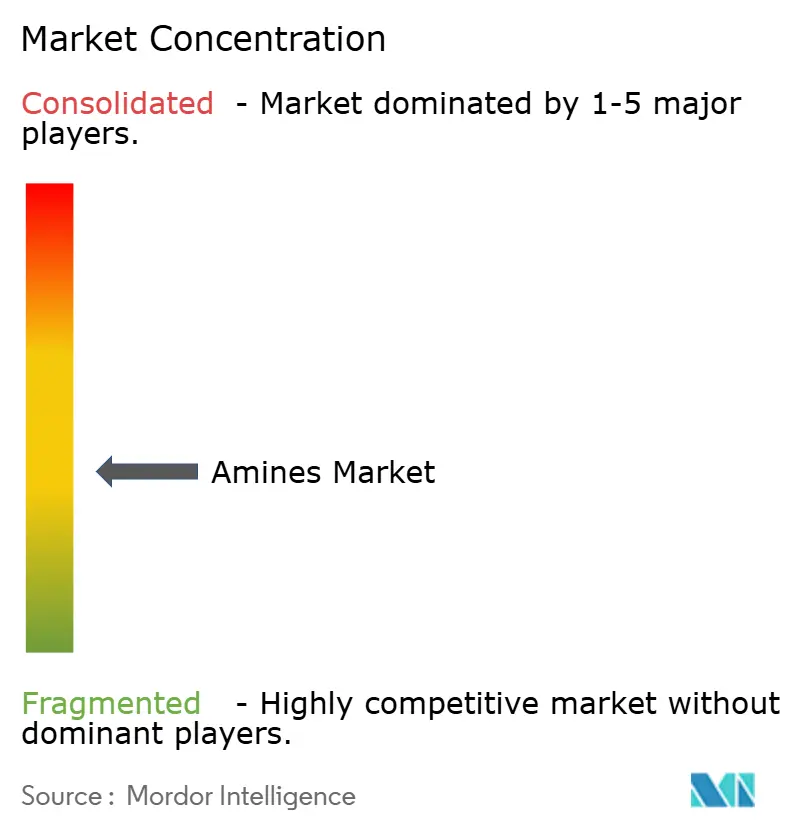

The global amines market is moderately fragmented. BASF, Dow and Huntsman leverage upstream ethylene and ammonia integration to stabilize raw-material costs and guarantee supply continuity. Dow holds the leading position in both ethyleneamines and ethanolamines, underpinned by proprietary Oxirane technology. Huntsman’s E-GRADE platform targets chipmakers that require sub-ppb metal specifications, reinforcing its reputation in high-purity niches. BASF’s 140,000 t/year alkyl ethanolamine plant in Antwerp and the 260,000 t/year hexamethylenediamine unit in Chalampé extend its leadership across intermediates for polyurethanes, nylon 6,6 and specialty surfactants.

Strategic partnerships are central to sustainability progress. Evonik has teamed with BASF to source biomass-balanced ammonia, cutting cradle-to-gate carbon footprints by more than 65%. Similar collaborations are emerging across the value chain, pairing catalytic-process innovators with large-volume operators to accelerate commercialization of low-carbon routes. Niche producers focusing on bespoke amines market opportunities for pharma active ingredients and 3D-printing resins are capturing segments overlooked by commodity incumbents.

Competitive intensity is increasing in emerging applications such as carbon-capture solvents, where traditional monoethanolamine blends are being challenged by proprietary sterically hindered amines that promise lower regeneration energy. ANDRITZ reported 95% CO₂ removal efficiency with liquid amine systems at scale. Suppliers that can combine superior performance with reduced environmental footprint stand to secure early-mover advantage in this rapidly evolving segment of the amines market.

Amines Industry Leaders

Akzo Nobel N.V.

BASF SE

Dow

Huntsman International LLC

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BASF has opened a world-scale hexamethylenediamine (HMD) plant in Chalampé, France, increasing its annual production capacity to 260,000 metric tons. This development is expected to enhance competition and drive growth in the amine market.

- November 2024: Evonik has commenced the expansion of its specialty amines plant in Nanjing, China. This strategic initiative aims to strengthen its amine portfolio, leverage cost-efficient raw materials, and enhance competitiveness by optimizing its production network. The facility is projected to commence commercial-scale production by 2026.

Global Amines Market Report Scope

The amines market report includes:

By Type

| Ethyleneamines |

| Alkylamines |

| Fatty Amines |

| Specialty Amines |

| Ethanolamines |

By End-use Industry

| Rubber |

| Personal Care Products |

| Cleaning Products |

| Adhesives, Paints and Resins |

| Agro-Chemicals |

| Oil and Petrochemicals |

| Other End-uses |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Ethyleneamines | |

| Alkylamines | ||

| Fatty Amines | ||

| Specialty Amines | ||

| Ethanolamines | ||

| By End-use Industry | Rubber | |

| Personal Care Products | ||

| Cleaning Products | ||

| Adhesives, Paints and Resins | ||

| Agro-Chemicals | ||

| Oil and Petrochemicals | ||

| Other End-uses | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the amines market?

The amines market size reached USD 16.91 billion in 2026 and is projected to grow to USD 21.25 billion by 2031.

Which amine type holds the largest share?

Ethanolamines led with 42.18% share of global demand in 2025 due to widespread use in gas sweetening, personal-care and cement additives.

Which region is expanding the fastest in amines market?

Asia Pacific combines the largest consumption base with the highest 5.64% CAGR forecast through 2031, driven by manufacturing scale in China, India and Southeast Asia.

What is the biggest end-use for amines today?

Agro chemicals dominate, accounting for 35.12% of global volume in 2025 as modern farming requires amine-based herbicides, fertilizers and adjuvants.

How are feedstock price swings affecting producers?

Volatile natural-gas and ethylene costs compress margins; leading suppliers are pursuing green hydrogen routes and long-term supply agreements to stabilize input pricing.

Why are electronics-grade amines gaining attention?

Advanced semiconductor fabs need ultra-pure amines with ppb-level metal impurities, prompting investments in specialized purification facilities that command premium pricing.

Page last updated on: