Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

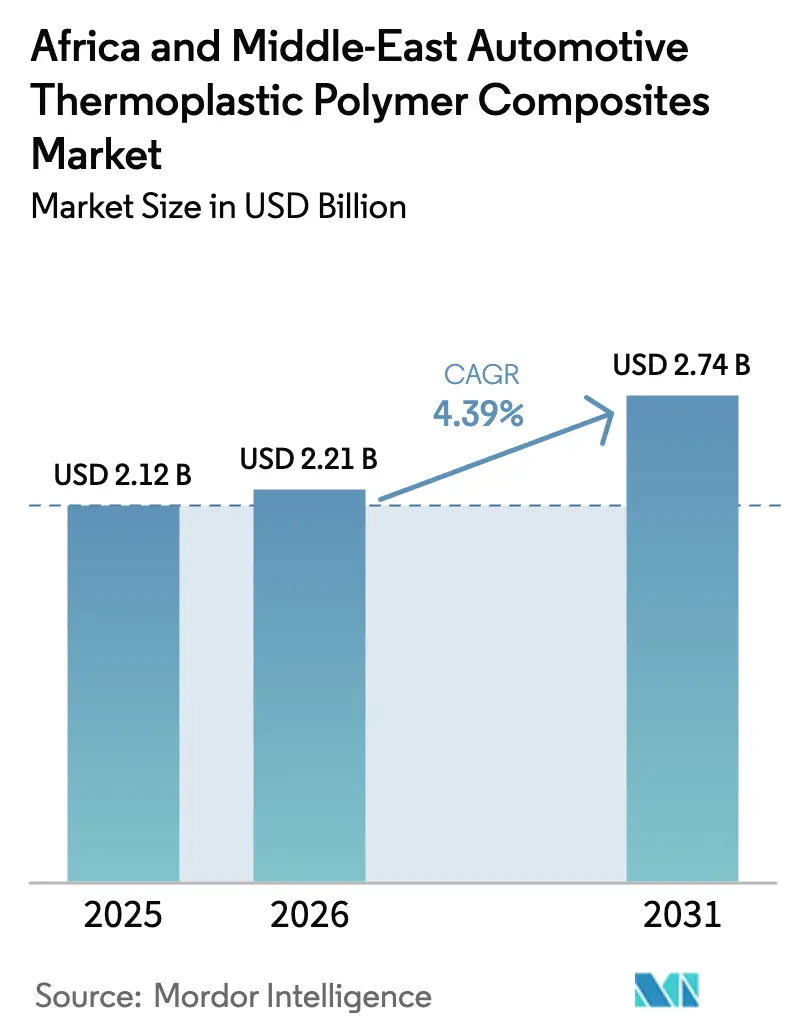

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

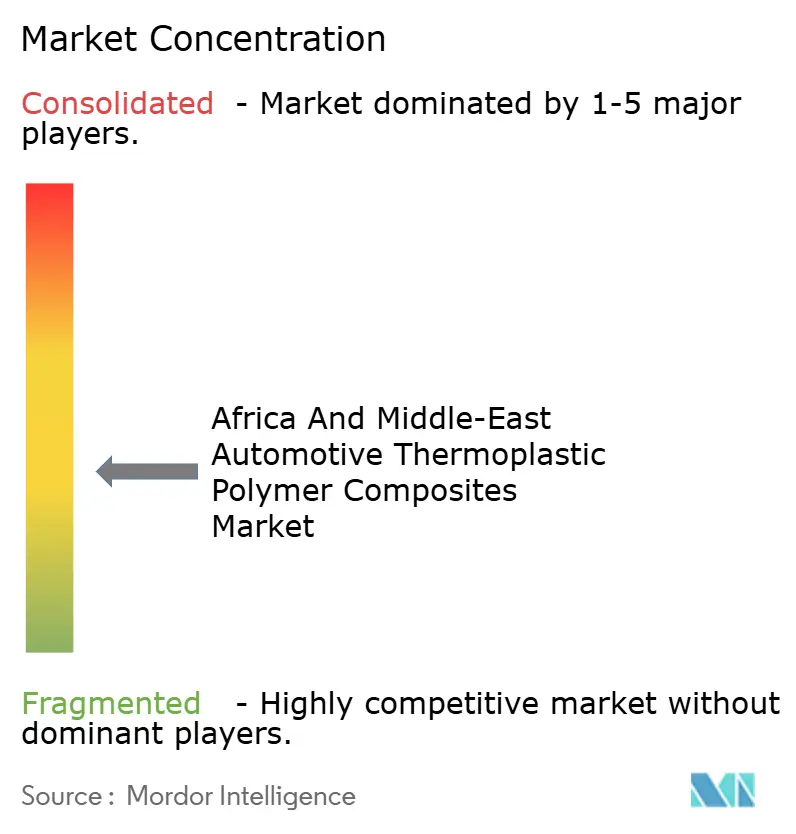

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa And Middle-East Automotive Thermoplastic Polymer Composites Market Analysis by Mordor Intelligence

The Africa And Middle-East Automotive Thermoplastic Polymer Composites Market size is expected to grow from USD 2.12 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 4.39% CAGR over 2026-2031. Light-weighting mandates, localization incentives in Saudi Arabia and the United Arab Emirates, and the growing transition to electric vehicles are driving increased demand for glass- and carbon-fiber-reinforced polypropylene and polyamide components. Injection molding continues to dominate in producing interior trim and small exterior parts due to its high-volume capabilities. However, compression molding is expanding rapidly, supported by the adoption of continuous-fiber organo-sheets, which reduce cycle times to under 90 seconds. Regional carbon-pricing pilots, though currently limited, are providing a clear price signal that benefits OEMs capable of demonstrating lower life-cycle emissions. Consequently, supply chain strategies are shifting toward in-region compounding and multi-year fiber offtake agreements, which help mitigate raw material price volatility and reduce lead times.

Key Report Takeaways

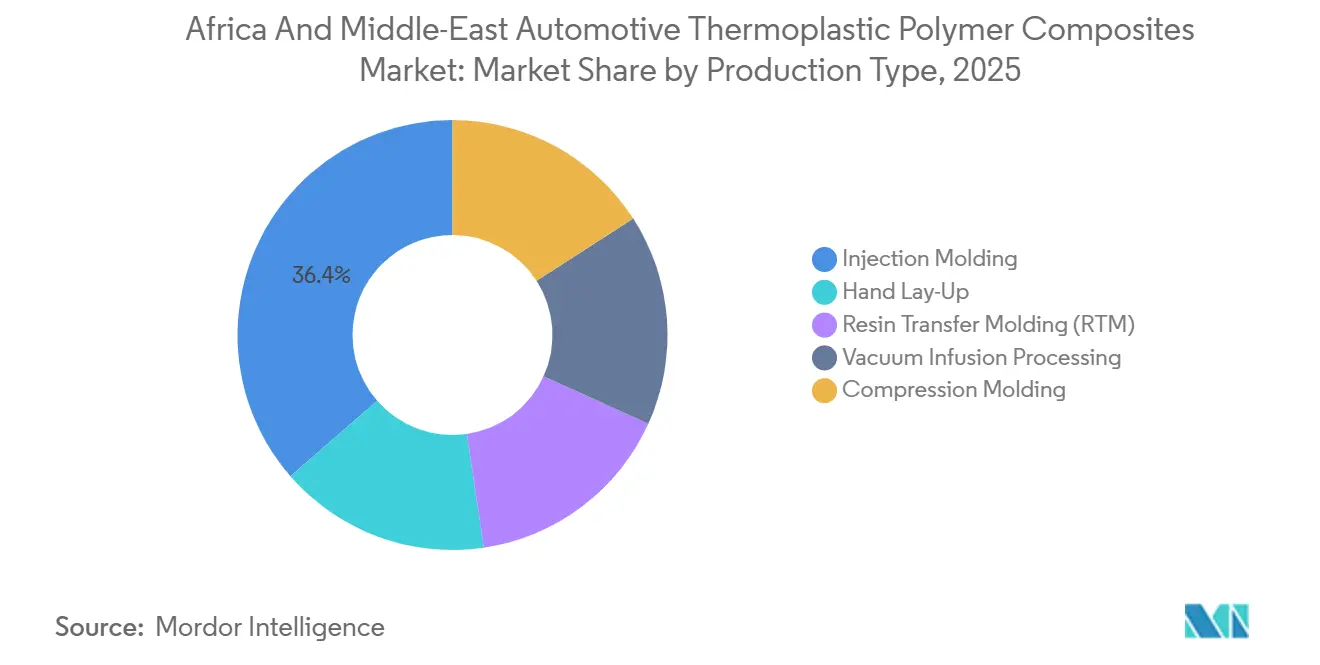

- By production type, injection molding led with 36.42% of the Africa and Middle-east automotive thermoplastic polymer composites market share in 2025, while compression molding is forecast to advance at a 4.78% CAGR through 2031.

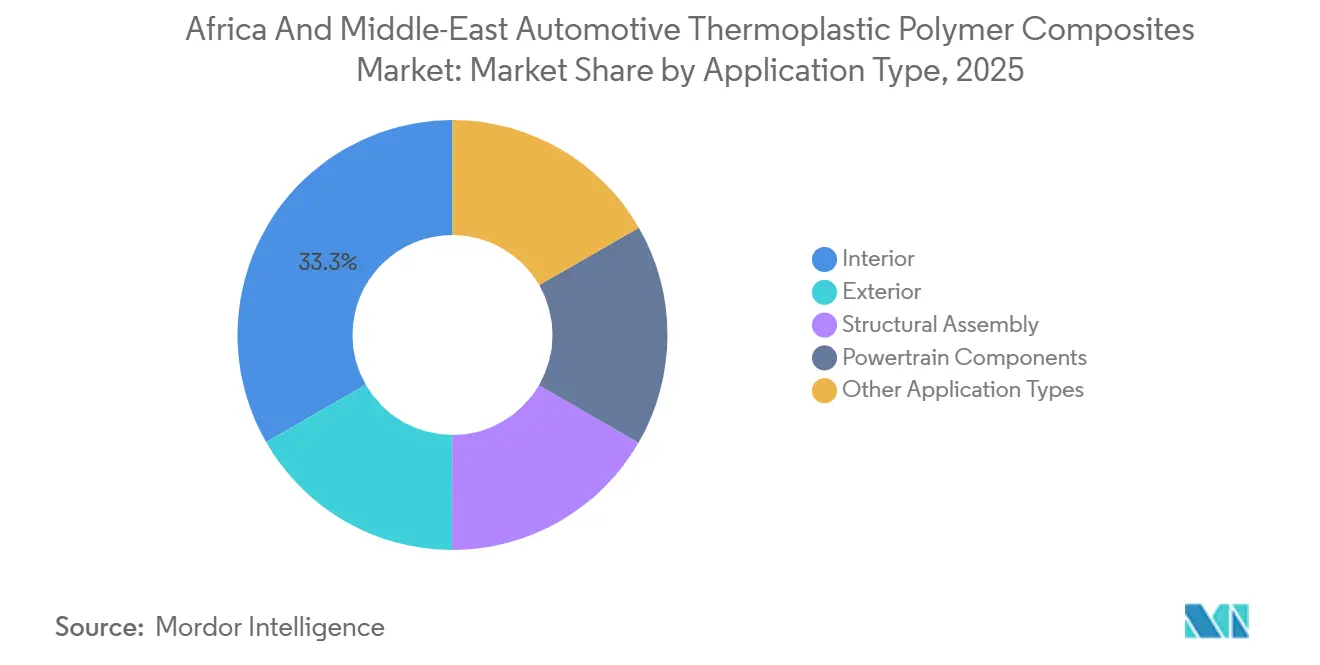

- By application type, interior captured 33.28% of the Africa and Middle-east automotive thermoplastic polymer composites market share in 2025; structural assembly is projected to expand at a 4.66% CAGR through 2031.

- By geography, Saudi Arabia commanded 26.47% of the Africa and Middle-east automotive thermoplastic polymer composites market share in 2025, yet the United Arab Emirates is poised to post the fastest 4.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa And Middle-East Automotive Thermoplastic Polymer Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regional CO₂/CAFÉ-like auto-emission policies | +1.2% | Saudi Arabia, UAE, Egypt | Medium term (2-4 years) |

| OEM localization incentives in Saudi Arabia and UAE free-zones | +0.9% | Saudi Arabia, UAE, with spillover to Egypt | Short term (≤ 2 years) |

| Rapid EV component sourcing shift towards recyclable PP/PA composites | +1.1% | Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| GCC carbon-pricing pilots boosting lightweight material demand | +0.6% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| 3D-printed long-fiber thermoplastic tooling lowering cap-ex | +0.5% | Global, with early adoption in UAE and South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regional CO₂/CAFÉ-Like Auto-Emission Policies

Fleet-average fuel-economy targets planned for Saudi Arabia in 2025 and Egypt's implementation of Euro 5 norms are driving the replacement of steel with long-glass-fiber polyamide in components such as door modules, front-end carriers, and instrument panels. This transition achieves 30%-40% mass savings while meeting crash-performance standards. Additionally, UAE programs aiming for 50% electric or hybrid vehicle sales by 2030 are reinforcing this trend, as battery packs increase vehicle curb weight, heightening the demand for lightweight materials. OEM bid documents increasingly reference ISO 14040 life-cycle assessments, requiring suppliers to measure carbon footprints from polymerization to end-of-life recycling.

OEM Localization Incentives in Saudi Arabia and UAE Free Zones

Ten-year tax holidays, duty-free equipment imports, and subsidized land in King Abdullah Economic City and Abu Dhabi’s KIZAD are motivating tier-1 converters to establish local compounding and molding facilities. For instance, Lucid Motors shifted the production of long-glass-fiber polypropylene interior panels from U.S. plants to a Saudi-based source, reducing logistics costs by 18% and shortening lead times from eight weeks to three. Similar agreements with Chinese material producers are anchoring polyamide-66 and polyphenylene-sulfide extrusion capacities for EV powertrain components.

Rapid EV Component Sourcing Shift Toward Recyclable PP/PA Composites

Continuous-fiber polyamide 6 and polypropylene laminates meet underbody impact and flame-resistance requirements and can be mechanically re-extruded while retaining up to 85% of their mechanical properties[1]Teijin Limited, “EV Composite Solutions Brochure 2025,” teijin.com. Tadweer’s 2025 pilot project confirms the feasibility of closed-loop recycling for post-consumer auto parts, aligning with EU circular-economy standards already applicable to South African exporters.

GCC Carbon-Pricing Pilots Boosting Lightweight Demand

Voluntary carbon credit trading platforms in the UAE and Saudi Arabia, with prices expected at USD 8–12 per ton in 2025, are enabling logistics fleets to monetize fuel-efficient vehicle choices. Consequently, OEMs are revisiting the use of glass-fiber-reinforced polyamide in components such as bumper beams, liftgates, and seat frames to secure economic advantages as carbon prices increase.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-driven raw-material price volatility (glass and carbon fiber) | -0.8% | Regional, with acute impact in Egypt and Sub-Saharan Africa | Short term (≤ 2 years) |

| Deficit of skilled composite technicians across North and Sub-Saharan Africa | -0.6% | Egypt, Morocco, Kenya, Nigeria, South Africa | Medium term (2-4 years) |

| Fragmented recycling streams for mixed thermoplastic laminates | -0.4% | Regional, with infrastructure gaps most severe in Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-Driven Raw-Material Price Volatility (Glass and Carbon Fiber)

Glass and carbon fiber costs experienced fluctuations of 15%–25% during 2024-2025 due to disruptions in Red Sea shipping and increased energy costs at European furnaces. Saudi and UAE OEMs managed to partially mitigate these fluctuations through multi-year contracts. However, smaller converters in Egypt and Kenya faced challenges, as they had to either absorb the cost increases or risk losing fixed-price component agreements. Additionally, currency depreciation, such as 18% for the Egyptian pound in 2024 and 12% for the South African rand in 2025, further increased local-currency fiber prices, putting pressure on converter margins.

Deficit of Skilled Composite Technicians across North and Sub-Saharan Africa

North African and sub-Saharan vocational systems produce fewer than 500 composite-certified technicians annually, compared to the estimated demand of 3,000 workers by 2028[2]International Labour Organization, “Regional Skills Gap Report 2025,” ilo.org. Multinational companies such as Gurit and SGL Carbon have established in-house training academies to address this shortage. However, these initiatives require an additional investment of USD 2–5 million per site, increasing overhead costs and extending production ramp-up timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Type: Organo-Sheets Propel Compression Molding

Compression molding is anticipated to grow at a 4.78% CAGR through 2031. Injection molding maintained 36.42% of 2025 output due to its cost advantages for high-volume applications such as interior trim, under-hood covers, and small exterior skins. Hand lay-up continues to be used for boutique luxury interiors, but its scalability is restricted by inconsistent fiber distribution and high labor costs. Resin transfer molding is gaining acceptance for battery enclosures, with fast-cure polyamide 6 reducing cycle times to 4-6 minutes. Vacuum infusion remains primarily limited to prototype production.

Organo-sheet technology serves as a key enabler for compression molding. Pre-consolidated continuous fibers embedded in a thermoplastic matrix enable cycle times of less than 90 seconds with consistent quality. Ceer’s first electric vehicle model incorporates compression-molded polyamide-6 underbody shields, achieving a 35% weight reduction and a 20% decrease in total cost of ownership over the vehicle's lifecycle. UAE regulations requiring ISO 527 tensile and ISO 14125 flexural data favor automated processes that ensure quality metrics, accelerating the transition away from manual lay-ups.

By Application Type: Structural Assembly Gains on Battery Integration

Structural assembly is expected to grow at a 4.66% CAGR through 2031, the fastest among all applications, driven by battery-electric platforms that integrate composite trays, crash members, and shields requiring high stiffness-to-weight ratios. Interior applications contributed 33.28% of 2025 market value, as components like instrument panels, door cards, and center consoles remain essential across all propulsion types. Exterior parts, including liftgates and bumper beams, are transitioning from steel to glass-fiber-reinforced polypropylene to meet Euro NCAP pedestrian safety standards while reducing vehicle weight. Powertrain applications remain steady, with composites used in engine covers and transmission pans offering advantages in acoustic damping and thermal insulation over die-cast aluminum.

Continuous-fiber polyamide trays meet UL 94 V-0 standards without brominated additives and withstand stone impacts at 80 km/h, outperforming die-cast aluminum in terms of weight and recyclability. UAE regulations under UN ECE R100 mandate dielectric strength above 20 kV/mm, a requirement easily met by polyamide-6 composites. As electric vehicle floorpans flatten, automakers are increasingly adopting composite crash rails and sills to maintain rigidity while reducing weight, further driving demand for organo-sheet compression molding.

Geography Analysis

Saudi Arabia is accounted for 26.47% of 2025 revenue, maintaining its position as the central hub of the automotive thermoplastic polymer composites market as Vision 2030 ties localization incentives to a minimum of 40% local value content. Fuel-efficiency mandates effective since 2025 are pushing manufacturers toward long-glass-fiber polyamide for liftgates, door inners, and front-end carriers. Tier-1 suppliers located within the King Salman Automotive Cluster are shortening supply chains and supporting in-country compounding of polypropylene and polyamide formulations.

The United Arab Emirates is forecast to grow at a 4.81% CAGR through 2031, outpacing other countries. Free-zone duty exemptions, advanced port logistics, and the inclusion of transportation emissions in the carbon-credit market since 2025 are attracting converters serving Saudi, Egyptian, and East African plants on a just-in-time basis. Tadweer’s polypropylene recycling pilot highlights policy support for circular-economy infrastructure, reinforcing OEM commitments to recyclable materials.

South Africa’s export-driven automotive sector supplies 65% of its production to Europe, adopting recyclable continuous-fiber polyamide to comply with EU circular-economy procurement rules. However, currency depreciation has increased fiber import costs, squeezing converter margins. Egypt leverages lower labor costs and EU trade preferences to attract injection-molding programs in the Suez Canal Economic Zone, though skills shortages and currency volatility limit short-term growth. Morocco benefits from its proximity to Europe, with Tangier-based converters producing small-batch vacuum-infused parts for premium brands. Meanwhile, Kenya and Nigeria are in the early stages of development, focusing on building training pipelines under African Continental Free Trade Area agreements.

Competitive Landscape

The automotive thermoplastic polymer composites market exhibits moderate concentration, with five global players, such as BASF, Solvay, 3B - The Fibreglass Company, Gurit Holding AG, and Base Materials Ltd. accounted for a combined 41% market share in 2025. BASF’s Ultramid hubs in Dubai and Johannesburg integrate application engineers into OEM design processes, often securing resin grades before part designs are finalized. Solvay is gaining traction in niche high-heat applications with Ryton PPS, used in turbo housings and e-motor insulation where polyamide 6 is less effective.

Regional molders like Composite Solutions (South Africa) and Advanced Composite Materials (UAE) secure low-volume, high-mix contracts for applications such as battery-enclosure prototypes and aftermarket body kits, where responsiveness outweighs economies of scale. Opportunities exist in closed-loop recycling and bio-based polyamides derived from castor oil, which reduce cradle-to-gate CO₂ emissions by up to 50%. However, their 20%-30% price premium limits adoption to premium segments. Additive manufacturing firms, including Aerosud and Immensa Technology Labs, eliminate tooling requirements for production runs below 5,000 parts, providing electric vehicle start-ups with a cost-effective market entry option. ISO 527 and ISO 178 quality standards ensure that only technically capable suppliers achieve production approval, maintaining moderate entry barriers.

Africa And Middle-East Automotive Thermoplastic Polymer Composites Industry Leaders

BASF

3B - the fibreglass company

Base Materials Ltd.

Solvay

Gurit Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The BENTELER Group completed the construction of its new automotive plant in Kenitra, Morocco. This facility is expected to drive the automotive thermoplastic polymer composite market by increasing production capacity and supporting advanced manufacturing processes.

- January 2025: Celanese Corporation expanded its partnership with Biesterfeld SE to distribute long-fiber reinforced thermoplastics (LFT) across the EMEA (Europe, Middle-East, and Africa) region. This initiative improved local market access.

Africa And Middle-East Automotive Thermoplastic Polymer Composites Market Report Scope

Automotive thermoplastic polymer composites are high-performance, lightweight materials, including reinforced polyamide (PA) and polypropylene (PP), designed to replace metal components. These materials help reduce vehicle weight, enhancing fuel efficiency and lowering emissions. They provide excellent strength-to-weight ratios, enable high-volume production through injection molding, resist corrosion, and offer design flexibility for structural, interior, and exterior applications.

The Africa and Middle-East Automotive Thermoplastic Polymer Composites Market is segmented by production type, application type, and geography. By production type, the market is segmented into injection molding, hand lay-up, resin transfer molding (RTM), vacuum infusion processing, and compression molding. By application type, the market is segmented into interior, exterior, structural assembly, powertrain components, and other application types. The report also covers the market size and forecasts for automotive thermoplastic polymer composites in 4 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Production Type

| Injection Molding |

| Hand Lay-Up |

| Resin Transfer Molding (RTM) |

| Vacuum Infusion Processing |

| Compression Molding |

By Application Type

| Interior |

| Exterior |

| Structural Assembly |

| Powertrain Components |

| Other Application Types |

By Geography

| South Africa |

| Egypt |

| United Arab Emirates |

| Saudi Arabia |

| Rest of Middle-East and Africa |

| By Production Type | Injection Molding |

| Hand Lay-Up | |

| Resin Transfer Molding (RTM) | |

| Vacuum Infusion Processing | |

| Compression Molding | |

| By Application Type | Interior |

| Exterior | |

| Structural Assembly | |

| Powertrain Components | |

| Other Application Types | |

| By Geography | South Africa |

| Egypt | |

| United Arab Emirates | |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the size of the Africa and Middle-East automotive thermoplastic polymer composites market?

The Africa and Middle-East automotive thermoplastic polymer composites market stands at USD 2.21 billion in 2026 and is projected to reach USD 2.74 billion by 2031.

Which production type is growing fastest through 2031?

Compression molding is the fastest-growing process thanks to organo-sheet adoption, registering a 4.78% CAGR through 2031.

Why are structural assemblies growing fastest through 2031?

Battery-electric platforms require lightweight yet stiff trays, shields, and crash members, pushing structural assemblies to a 4.66% CAGR through 2031.

Which country will post the quickest growth through 2031?

The United Arab Emirates leads with a 4.81% CAGR through 2031, driven by duty-free free zones and carbon-credit incentives.

Page last updated on: