Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

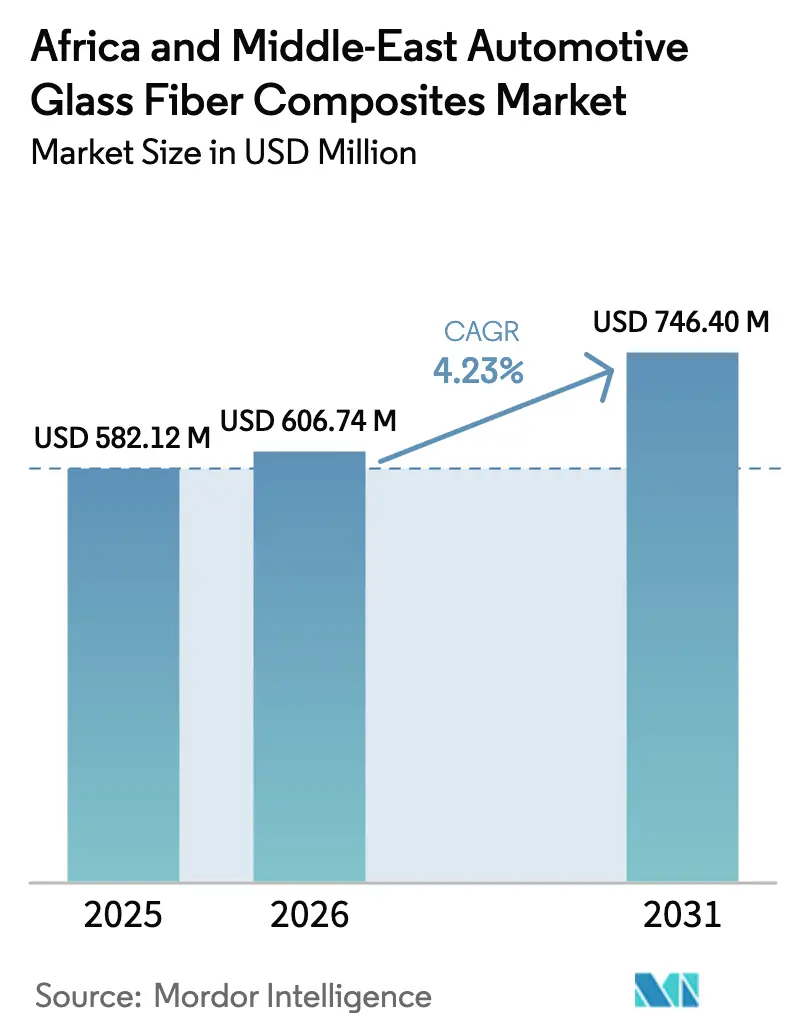

| Base Year Market Size (2025) | USD 582.12 Million |

| Market Size (2026) | USD 606.74 Million |

| Market Size (2031) | USD 746.40 Million |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

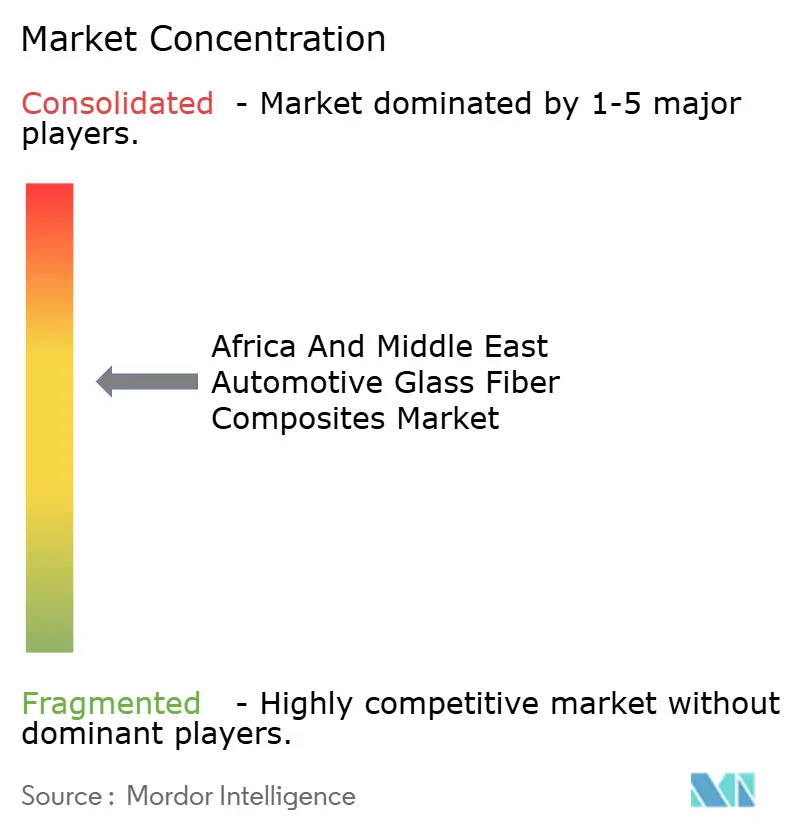

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa And Middle-East Automotive Glass Fiber Composites Market Analysis by Mordor Intelligence

The Africa And Middle-East Automotive Glass Fiber Composites Market size is projected to be USD 582.12 million in 2025, USD 606.74 million in 2026, and reach USD 746.40 million by 2031, growing at a CAGR of 4.23% from 2026 to 2031. A shift in policy toward downstream processing in the Gulf, coupled with domestic-content mandates in key African assembly hubs, is driving investment away from basic hydrocarbon exports toward value-added composite molding. Saudi Arabia’s allocation of USD 987 million from the Public Investment Fund to CEER suppliers in February 2026 highlights this transition, as the program supports tooling for glass-fiber door modules and battery trays. GCC lightweighting regulations and UAE tax incentives are reducing entry barriers for European molders, although logistical challenges through the Red Sea continue to increase the cost of imported roving. African CKD plants are replacing stamped steel with hand-laid composites to meet localization requirements, despite technician shortages in South Africa and Egypt leading to quality rejections under ISO 527 tensile tests.

Key Report Takeaways

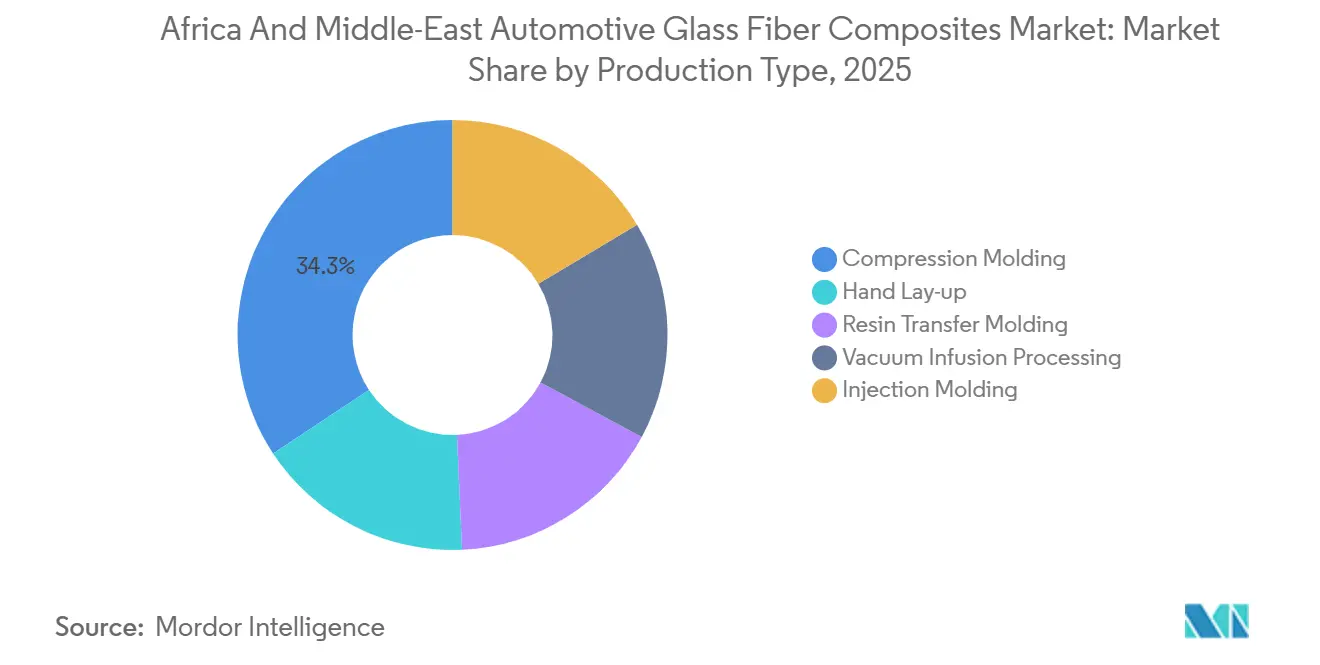

- By production type, compression molding led with 34.28% of the Africa and Middle-east automotive glass fiber composites market share in 2025, while vacuum infusion processing is forecast to post the fastest 4.47% CAGR through 2031.

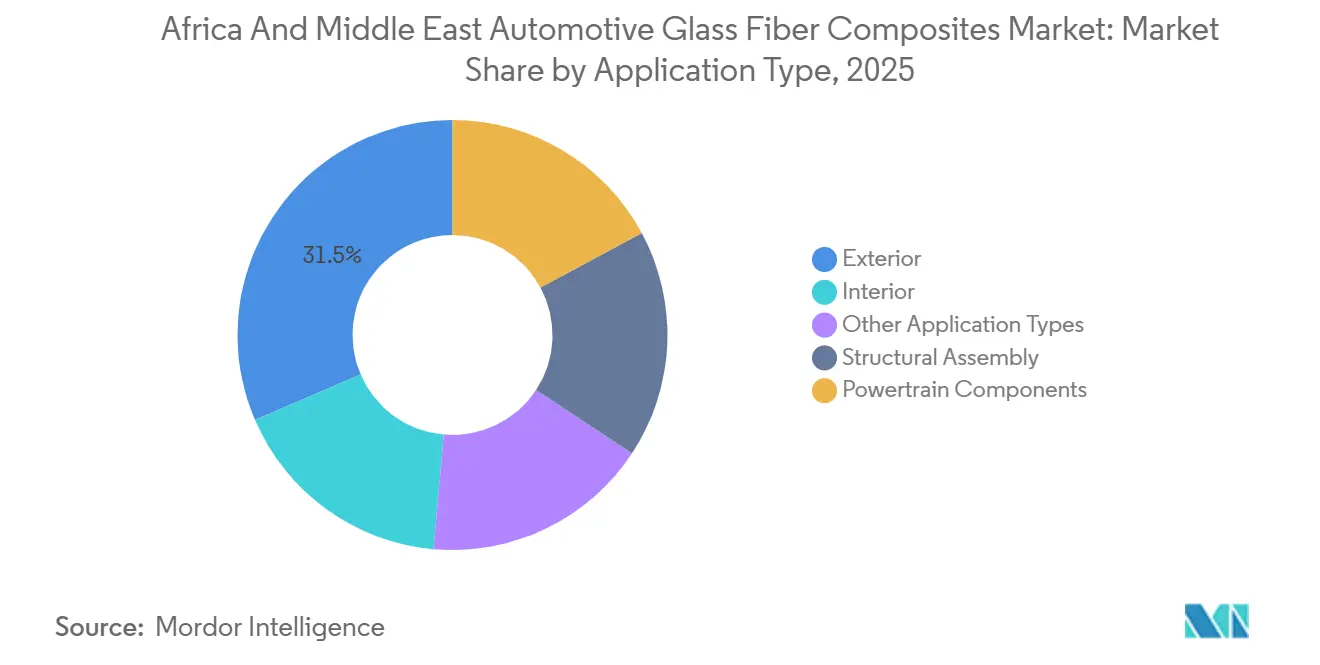

- By application type, exterior captured 31.46% of the Africa and Middle-east automotive glass fiber composites market share in 2025, whereas structural assembly is expected to advance at a 4.87% CAGR through 2031.

- By geography, Saudi Arabia held 27.38% of of the Africa and Middle-east automotive glass fiber composites market share in 2025, while the United Arab Emirates is projected to expand at a 4.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa And Middle-East Automotive Glass Fiber Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for fuel-efficient lightweighting | +1.2% | Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| Shift to battery-electric powertrains raises glass-fiber demand for EV enclosures | +0.9% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Localisation incentives in Saudi and UAE Tier-1 supply chains | +0.8% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Surge in CKD/IKD assembly plants across Africa adopting low-CAPEX hand lay-up parts | +0.7% | Egypt, Algeria, Kenya, Rest of MEA | Medium term (2-4 years) |

| Growing demand for corrosion-resistant composites in desert climates (fleets/buses) | +0.6% | Saudi Arabia, UAE, Egypt, Rest of MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Fuel-Efficient Lightweighting

Saudi Arabia’s SASO 2864:2019 standard lowers fleet consumption to 5.8 L/100 km by 2028, forcing automakers to remove 80-120 kg per vehicle through material substitution. Glass-fiber panels deliver 25-30% weight savings versus mild steel and remain cost-competitive against carbon fiber. The UAE starts EURO 6B in January 2026 and moves to EURO 6D by 2030, increasing pressure on OEMs to amortize lightweight components across GCC runs[1]Emirates Standardization and Metrology Authority, “EURO 6B implementation circular,” esma.gov.ae. While the rules accelerate composite uptake, end-of-life recycling gaps persist because thermoset glass fiber cannot be remelted, raising the prospect of landfill surcharges after 2028.

Shift to Battery-Electric Powertrains Raises Glass-Fiber Demand for EV Enclosures

SGL Carbon’s glass-fiber battery enclosure for BMW’s iX trims pack weight by 15% compared with aluminum housing. CEER’s prototype sedan mirrors this approach with a glass-fiber lower tray that offsets its 600 kg battery. Resin-transfer molding offers complex geometries without the capital intensity of aluminum presses, a key benefit for African plants with tight budgets. Egypt’s Dr. Greiche will open a USD 16.2 million infusion line in Q4 2026 to supply EV underbody shields, underscoring the cross-over between traditional glazing firms and composite components.

Localisation Incentives in Saudi and UAE Tier-1 Supply Chains

Stellantis and Petromin signed an MoU in November 2025 prioritizing glass-fiber door modules and IP substrates for Peugeot and Fiat lines. The UAE’s Make it in the Emirates program grants a 10-year tax holiday and 50% duty waiver on imported machinery, slashing setup costs for European composite specialists. Syensqo and Saudi Aramco’s December 2025 JV at Jubail will supply specialty resins from 2027, shortening lead times and trimming feedstock costs.

Surge in CKD/IKD Assembly Plants Across Africa Adopting Low-CAPEX Hand Lay-Up Parts

KG Mobility opened a 10,000-unit CKD plant in Algeria in November 2025, choosing hand lay-up roof panels and cargo liners to avoid multi-million-dollar tooling bills. Mahindra’s February 2025 feasibility study with South Africa’s IDC shows hand-laid composites stay cost-competitive below 15,000 units when amortization is counted. El Nasr Automotive, revived in November 2024, follows the same path to meet a 63.5% local-content target without forex exposure for imported stampings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile glass-fiber import prices due to Red Sea freight premiums | -0.5% | Egypt, Kenya, South Africa | Short term (≤ 2 years) |

| Shortage of certified composite technicians causing OEM quality rejections | -0.4% | South Africa, Egypt, Rest of MEA | Medium term (2-4 years) |

| Limited regional Tier-2 resin formulators inflating composite costs | -0.3% | Egypt, South Africa, Kenya, Rest of MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Glass-Fiber Import Prices Due to Red Sea Freight Premiums

Houthi attacks in 2024 caused 28% of Asia-to-Europe cargo to be rerouted via the Cape of Good Hope, leading to a 150-200% increase in freight rates. This raised the landed cost of Chinese and Indian rovings by 12-18% for Egyptian and Kenyan molders without hedging tools. Even after the conflict subsides, insurers have added an 8-10% surcharge to premiums, expected to remain through 2027, embedding structural volatility into the Africa and Middle-East automotive glass fiber composites market.

Shortage of Certified Composite Technicians Causing OEM Quality Rejections

NAACAM’s 2024 survey found that 70% of component manufacturers face critical artisan shortages, particularly in composite lay-up processes[2]NAACAM, “Skills survey 2024,” naacam.org.za. Rejection rates exceeding 15% undermine the theoretical labor-cost benefits of African sourcing. Although the South African Qualifications Authority has established standards, training centers are predominantly located in Gauteng and Western Cape, leaving coastal assembly corridors underserved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Type: Compression Molding Anchors Revenue, Vacuum Infusion Gains Share

Compression molding accounted for 34.28% of revenue in 2025, remaining a key production method in the Africa and Middle-East automotive glass fiber composites market. Advanced Fibreform’s 12 presses produce over 3,000 parts weekly for Toyota and Isuzu pickups. Vacuum infusion processing is projected to grow at a 4.47% CAGR through 2031, driven by demand for complex, void-free laminates in EV battery trays and underbody shields. Johns Manville’s USD 55 million Ohio line expansion aims to meet this demand, with output designated for GCC importers.

Hand lay-up continues to be utilized in CKD operations producing fewer than 15,000 units, offering a cost-effective solution to meet local-content regulations in Algeria, Egypt, and Kenya. Resin-transfer molding is used for niche structural components like seat frames, where fiber architecture is critical. Injection-molded short-fiber compounds are employed for high-volume interior brackets.

By Application Type: Exterior Leads, Structural Assembly Accelerates

Exterior applications accounted for 31.46% of 2025 revenue, primarily due to hoods, tailgates, and pickup beds that achieve 25-30% mass savings. Structural assembly is expected to grow at the fastest rate, with a 4.87% CAGR through 2031, as GCC crash regulations align with UN R137, requiring predictable deformation. BMW’s Life Module success with composite subframes has inspired regional OEMs to adopt similar approaches.

Powertrain components such as covers, transmission pans, and oil sumps leverage glass fiber’s damping and thermal stability but face slower growth due to stringent re-qualification requirements. Interior substrates and door panels benefit from fast-cycle compression molding using low VOC resins like Hexcel’s HexMC, which comply with GCC cabin-air standards.

Geography Analysis

Saudi Arabia generated 27.38% of 2025 demand, supported by Vision 2030 local-content initiatives and the USD 987 million CEER supply-chain fund. The Syensqo-Aramco joint venture will begin supplying specialty resins in 2027, reducing reliance on European imports. SASO 2864:2019 emphasizes lightweighting, while corrosion issues in the public bus fleet are prompting a shift toward composite bodies.

The United Arab Emirates is projected to grow at a 4.35% CAGR through 2031, driven by "Make it in the Emirates" tax incentives that attract European press shops. The adoption of EURO 6B standards from 2026 further supports composite usage. The UAE’s automotive glass fiber composites market is expanding rapidly as Dubai targets 50% localized component content by 2030.

Egypt is undergoing a manufacturing resurgence, with El Nasr Automotive’s relaunch targeting 63.5% local content and Dr. Greiche’s USD 16.2 million resin-infusion line supporting growth. However, currency fluctuations remain a challenge, prompting molders to hedge euro-based resin purchases. South Africa continues to anchor the continent’s production volume with Toyota, Isuzu, and VW plants, though NAACAM reports a shortage of skilled artisans. Advanced Fibreform’s weekly output of 3,000 parts demonstrates that local molders can meet OEM quality standards once supply chains stabilize.

Kenya, Algeria, Morocco, and Tunisia contribute to the region’s growth. KG Mobility’s Algerian plant targets 10,000 units annually using hand lay-up, showcasing a low-capex approach to import substitution. Moroccan molders remain dependent on Spanish rovings, exposing them to euro-dirham exchange rate volatility.

Competitive Landscape

The competitive landscape is moderately concentrated, with the top five players accounting for 51% of the market share in 2025. Saint-Gobain’s European plants offer 7-10 day lead times to GCC ports, but the absence of a Middle-East facility allows Syensqo-Aramco to undercut costs once its Jubail facility becomes operational in 2027. Owens Corning is investing in automated fiber placement through its 2024 partnership with Orbital Composites, providing GCC OEMs access to aerospace-grade structural parts.

Regional players focus on hand lay-up and bus body production. Advanced Fibreform supplies South African pickup plants, while Egyptian startups target aftermarket hoods and fenders. Vacuum-infusion capacity remains limited, with fewer than a dozen African molders owning autoclaves, creating opportunities for European toll molders to supply kits. Technician shortages in South Africa and Egypt impact output quality, giving companies that offer bundled training a competitive advantage.

As freight surcharges decrease, the next phase of competition will center on upstream integration. GCC petrochemical companies control resin feedstock, and by 2028, at least two plan to establish in-house compounding lines, challenging small European formulators currently enjoying a 25-35% premium. Mold tooling vendors from Germany and Italy are exploring Riyadh and Abu Dhabi free-trade zones to reduce delivery times.

Africa And Middle-East Automotive Glass Fiber Composites Industry Leaders

BASF

3B - the fibreglass company

Base Materials Ltd.

Gurit Holding AG

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Saudi Arabia's CEER, the Kingdom’s first electric vehicle (EV) brand, signed 16 commercial agreements valued at over SAR 3.7 billion (USD 987 million) with Tier-1 suppliers during the 4th PIF Private Sector Forum. These agreements focused on components such as glass fiber door modules and battery enclosures, supporting the strategy to localize 45% of vehicle components by 2034.

- May 2024: BASF integrated sustainable glass fibers into its Ultramid A and B portfolio to lower Scope 3.1 emissions. This effort reduced the product's carbon footprint by approximately 10%, saving around 5,000 tons annually and improving the sustainability of durable, reinforced automotive components.

Africa And Middle-East Automotive Glass Fiber Composites Market Report Scope

Automotive glass fiber is a lightweight, high-strength reinforcing material designed to replace metal, enhance fuel efficiency, and reduce emissions. It is commonly utilized in exterior panels, structural components, and EV battery enclosures due to its durability, corrosion resistance, and thermal stability.

The Africa and Middle-East Automotive Glass Fiber Composites Market is segmented by production type, application type, and geography. By production type, the market is segmented into compression molding, hand lay-up, resin transfer molding, vacuum infusion processing, and injection molding. By application type, the market is segmented into exterior, structural assembly, powertrain components, interior, and other application types. The report also covers the market size and forecasts for automotive glass fiber composites in 4 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Production Type

| Compression Molding |

| Hand Lay-up |

| Resin Transfer Molding |

| Vacuum Infusion Processing |

| Injection Molding |

By Application Type

| Exterior |

| Structural Assembly |

| Powertrain Components |

| Interior |

| Other Application Types |

By Geography

| South Africa |

| Egypt |

| United Arab Emirates |

| Saudi Arabia |

| Rest of Middle-East and Africa |

| By Production Type | Compression Molding |

| Hand Lay-up | |

| Resin Transfer Molding | |

| Vacuum Infusion Processing | |

| Injection Molding | |

| By Application Type | Exterior |

| Structural Assembly | |

| Powertrain Components | |

| Interior | |

| Other Application Types | |

| By Geography | South Africa |

| Egypt | |

| United Arab Emirates | |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the size of the Africa and Middle-East automotive glass fiber composites market?

The Africa and Middle-East automotive glass fiber composites market stands at USD 606.74 million in 2026 and is projected to reach USD 746.40 million by 2031.

Which production type is growing the fastest through 2031?

Vacuum infusion processing is set to grow at a 4.47% CAGR through 2031, driven by demand for complex EV battery trays.

How are Red Sea freight issues affecting composite costs?

Rerouting around the Cape has added permanent 8-10% freight surcharges, lifting imported glass-fiber prices by 12-18%.

Which application type will expand most rapidly through 2031?

Structural assembly is forecast to advance at a 4.87% CAGR through 2031 has UN R137 crash rules spur adoption of composite subframes.

Page last updated on: