Acrylic Acid Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Market Volume (2026) | 8.59 Million tons |

| Market Volume (2031) | 11.01 Million tons |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

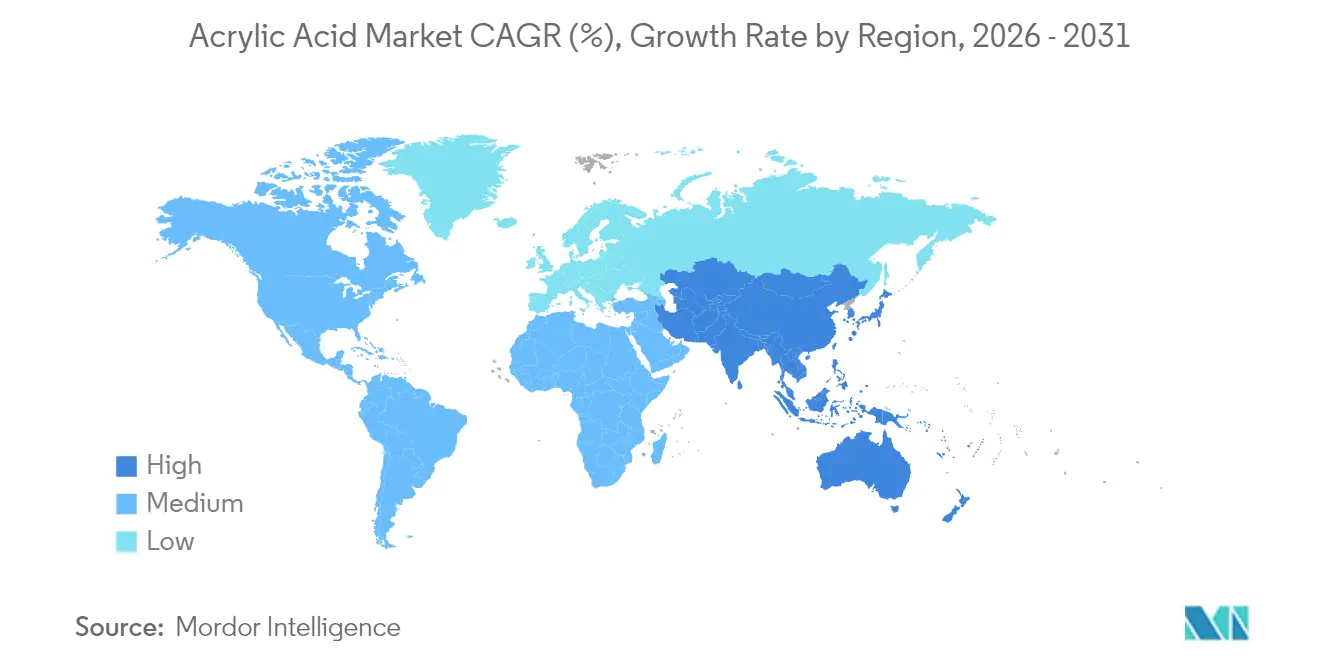

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylic Acid Market Analysis by Mordor Intelligence

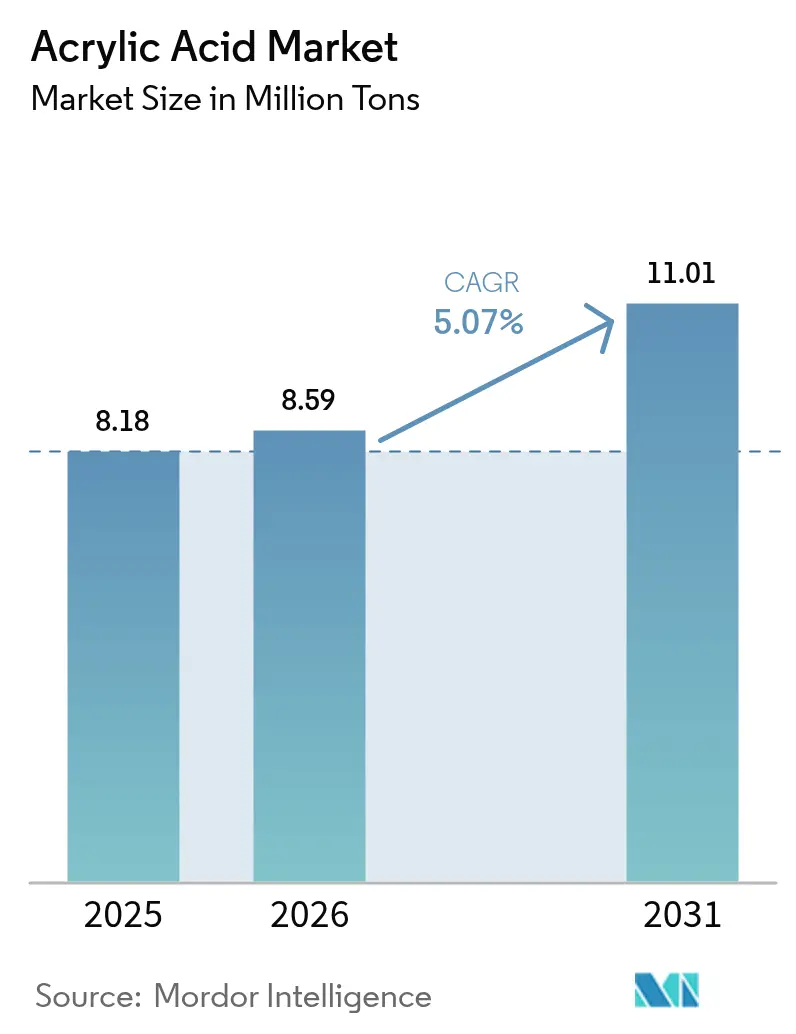

The Acrylic Acid Market size is expected to grow from 8.18 million tons in 2025 to 8.59 million tons in 2026 and is forecast to reach 11.01 million tons by 2031 at 5.07% CAGR over 2026-2031. Sustained demand from super-absorbent polymers, water-borne architectural coatings, and specialty adhesives anchors this growth trajectory. Ongoing substitution of solvent-borne chemistries, demographic shifts toward premium hygiene products, and infrastructure programmes that specify low-VOC coatings all reinforce volume expansion across mature and emerging economies. Feedstock diversification into bio-routes and propane-based technologies mitigates propylene volatility, while vertical integration strategies protect margins. Competitive positioning increasingly hinges on carbon-footprint transparency, certified bio-content, and the ability to supply high-purity grades for electronics and medical applications.

Key Report Takeaways

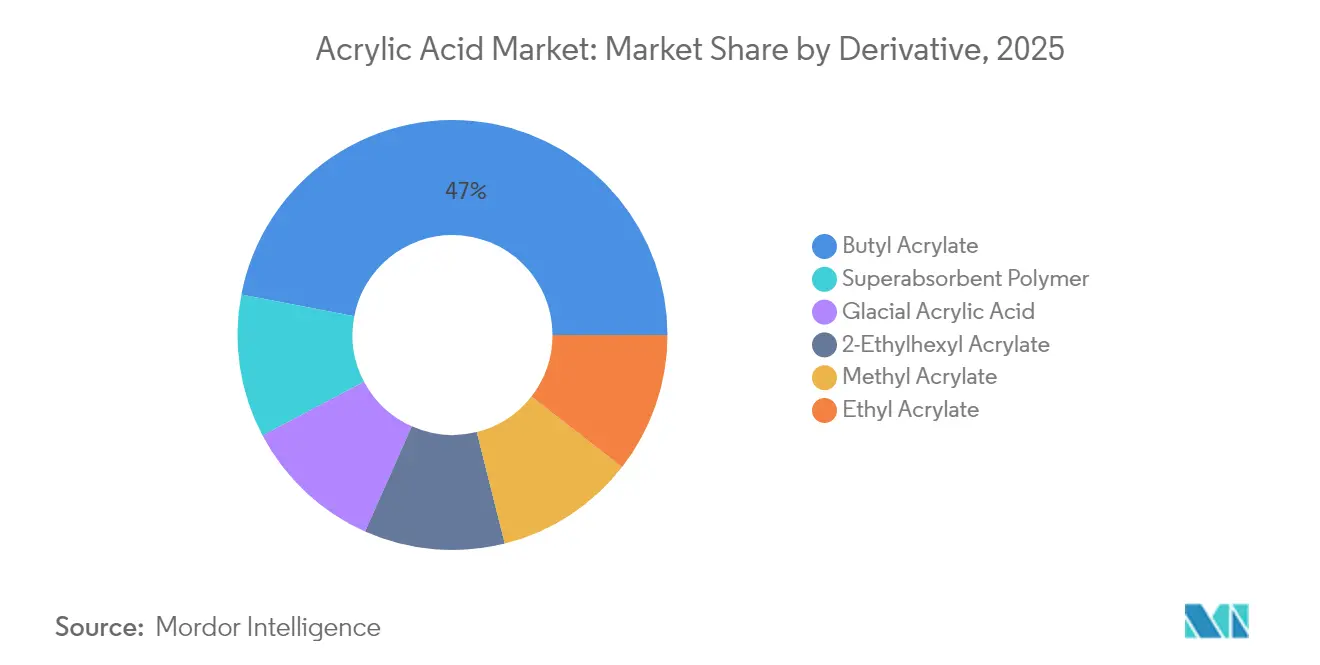

- By derivative, butyl acrylate led with 46.98% of acrylic acid market share in 2025, while Super-absorbent polymers are projected to expand at a 5.53% CAGR through 2031.

- By application, paints and coatings accounted for 35.46% of the acrylic acid market size in 2025, and adhesives and sealants are expected to record the fastest growth at 7.01% CAGR to 2031.

- By purity grade, technical grade held 88.74% volume in 2025, whereas glacial grade advances at a 7.18% CAGR to 2031.

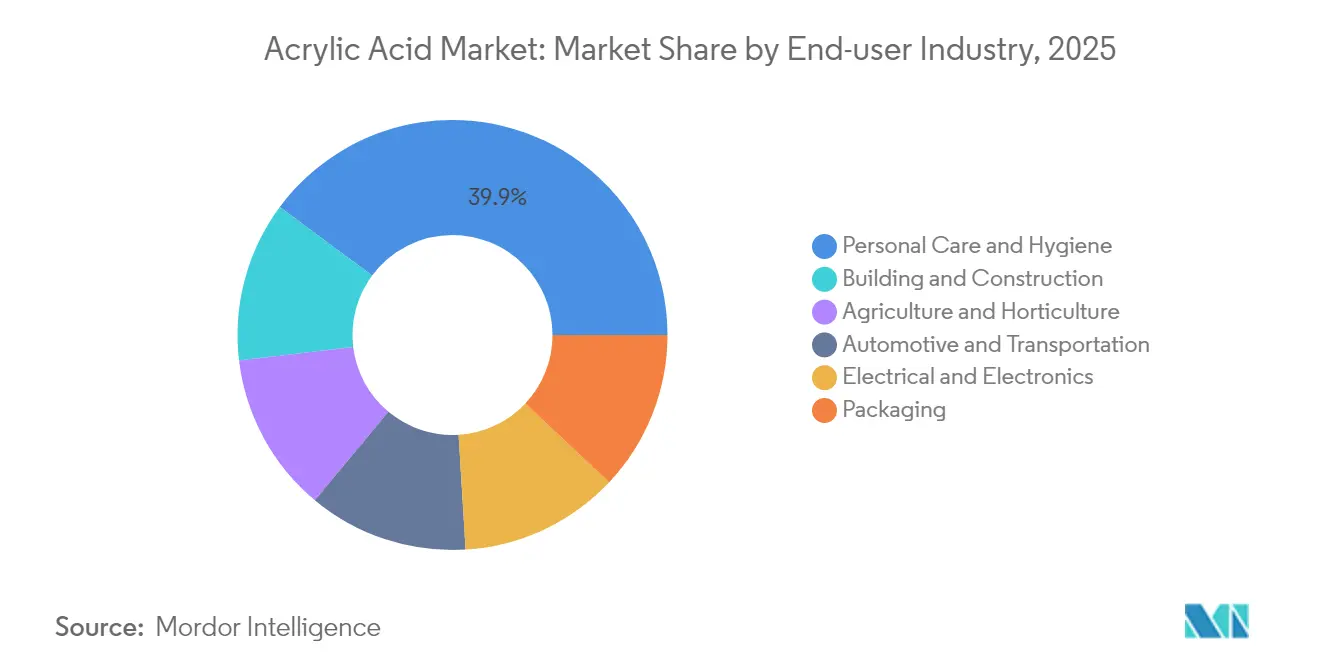

- By end-user industry, personal care and hygiene contributed 39.85% of demand in 2025 and is expected to grow at a 5.48% CAGR to 2031.

- By geography, Asia-Pacific contributed 52.10% of global volume in 2025, expanding at 5.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acrylic Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Super-absorbent polymer demand up-trend | +1.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of waterborne architectural coatings | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Rising hygiene mandates in emerging Asia | +0.8% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Commercialisation of bio-acrylic acid routes | +0.6% | Global, led by North America and EU | Long term (≥ 4 years) |

| Surge in electronics-grade pressure-sensitive adhesives | +0.5% | Global, concentrated in APAC electronics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Super-Absorbent Polymer Demand Up-Trend

Global demographic ageing and rising disposable incomes lift hygiene-product penetration, intensifying consumption of polyacrylate-based super-absorbents. Agricultural adoption broadens the acrylic acid market as growers use the polymers to enhance soil water retention in arid regions. Research into biodegradable cross-linkers lessens end-of-life concerns while preserving absorption capacity. Volume growth remains most pronounced in Asia-Pacific, where infant and adult incontinence products scale rapidly. Leading resin suppliers introduce microwave-based recycling for methyl methacrylate, closing the loop for cast-acrylic waste. Manufacturers also refine catalytic processes to cut energy intensity, underpinning long-term cost competitiveness.

Expansion Of Water-Borne Architectural Coatings

Governmental VOC regulations stimulate a lasting shift from solvent-borne to water-borne systems, cementing acrylic dispersions as the binder of choice. BASF’s new Dutch production line elevates regional capacity without CO₂ increases, signalling a commitment to sustainable scale-up. In the Gulf Co-operation Council states, acrylic resin already commands more than 40% coating formulations, buoyed by large-scale infrastructure builds that require fast-drying, corrosion-resistant finishes. The acrylic acid market benefits as water-borne chemistries need higher binder solids to match legacy performance, materially lifting monomer pull-through. Packaging conversions from plastic to paper substrates further amplify dispersion demand.

Rising Hygiene Mandates in Emerging Asia

Public-health campaigns, halal certification requirements, and supportive e-commerce channels converge to accelerate premium diaper and feminine-care consumption. Indonesian production of biomass-derived acrylic acid demonstrates a local response to faith-based certification as well as feedstock diversification. Governments link sanitation upgrades to measurable reductions in waterborne disease, reinforcing long-run demand for absorbent hygiene products. Rapid urbanisation elevates per-capita spending on personal-care staples, sustaining double-digit growth pockets despite macroeconomic cycles. The acrylic acid market gains additional tailwinds from value-added adult incontinence segments that favour high-performance, ultra-thin cores.

Commercialisation of Bio-Acrylic Acid Routes

LG Chem’s 100 tons/year fully plant-based line validates the commercial feasibility of microbial fermentation pathways. Identical performance enables direct drop-in use, prompting brand owners to specify bio-grades for cosmetics and home-care products. Life-cycle assessment transparency grows in procurement tenders, giving early movers pricing leverage. Technology licensors forecast triple-digit capacity growth over the decade, positioning bio-routes as a structural supply pillar rather than a niche offering. The acrylic acid market thereby decouples part of its raw-material risk from crude-derived propylene.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and toxicity concerns of AA vapours | -0.7% | Global, stricter in North America and the EU | Short term (≤ 2 years) |

| Propylene price volatility | -0.5% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Supply risk from ageing propylene oxide assets | -0.3% | Global, concentrated in North America and EU legacy facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Toxicity Concerns of AA Vapours

Regulatory agencies tighten exposure thresholds, compelling producers to invest in closed-loop loading, advanced scrubbers, and personal protective equipment. The European Commission cites respiratory irritation risks, while NIOSH recommends a 2 ppm TWA[1]National Institute for Occupational Safety and Health, “Acrylic Acid,” cdc.gov. Australia’s National Pollutant Inventory records site emissions to guide licensing limits. WHO and EPA guidance shape multinational policy, adding layers of compliance that elevate fixed costs[2]U.S. Environmental Protection Agency, “Provisional Toxicity Values for Acrylic Acid,” epa.gov. Downstream converters, particularly adhesive plants, must redesign ventilation to meet lowered indoor-air targets. Short-term capacity utilisation can dip as retrofits proceed, tempering acrylic acid market growth in highly regulated regions.

Propylene Price Volatility

Interruptions at ageing propylene oxide assets and refinery rationalisations squeeze monomer margins, prompting firms to accelerate propane dehydrogenation and bio-route investments. Cracker integration or offtake agreements hedge exposure, but spot markets remain prone to double-digit swings that distort quarterly earnings. Producers in Asia-Pacific face amplified risk given the region’s wider import dependency for chemical-grade propylene. Feedstock turbulence encourages customers to seek long-term supply contracts with integrated vendors, consolidating volume with major players. The acrylic acid market thus experiences episodic destocking cycles whenever propylene spikes, particularly across price-sensitive coating derivatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: Versatile Butyl Acrylate Defends Volume Supremacy as SAP Accelerates

Butyl acrylate contributed 46.98% of 2025 shipments on the strength of broad coating, adhesive, and sealant usage. Its balance of flexibility, weatherability, and cost efficiency secures formulation loyalty across the construction and packaging industries. However, demographic trends that lift hygiene standards stoke super-absorbent polymer (SAP) demand, giving SAP derivatives the highest 5.53% CAGR through 2031. SAP producers exploit acrylic acid’s capacity to form highly cross-linked networks that absorb liquids exceeding several hundred times their own weight. Specialty streams such as methyl acrylate enjoy steady niche orders for rapid-cure transmission-coating systems, whereas ethyl acrylate supports textile and leather finishing requiring deep fibre penetration. Two-ethylhexyl acrylate remains the tackifier of choice for pressure-sensitive adhesive labels. Glacial acrylic acid underpins electronics and pharmaceutical intermediates, where 99%+ purity ensures minimal trace metals.

By Application: Performance Adhesives Pull Ahead of Legacy Coatings

Paints and coatings retained 35.46% volume in 2025 thanks to ongoing infrastructure spending, yet adhesives and sealants display a 7.01% CAGR that edges out traditional coating increments. High-clarity, UV-resistant acrylic pressure-sensitive adhesives dominate electronic display lamination and exterior automotive trim, accelerating monomer uptake. Sanitary products leverage advances in cross-link density to reduce core thickness while maintaining absorption metrics, thereby lowering logistics costs. Surfactant applications tap acrylic acid’s amphiphilic property set to improve detergency across concentrated laundry formats. Textile treatments incorporate acrylic derivatives for durable water repellency and anti-soiling finishes that survive multiple wash cycles. Consequently, the acrylic acid market realigns toward high-value bonding solutions that satisfy miniaturisation in electronics and net-zero body-weight targets in automotive.

By Purity Grade: Technical Grade Retains Volume Edge while Glacial Grades Surge

Technical grade (~94% purity) served 88.74% of 2025 demand, largely feeding high-tonnage paints, adhesives, and SAP plants where cost considerations dominate. Nonetheless, glacial grade (more than or equal to 99% purity) advances at a 7.18% CAGR through 2031 as electronics, semiconductor encapsulation, and pharmaceutical actives mandate extremely low ion and metal content. Semiconductor fabs specify ultra-high-purity monomer for photo-resist and underfill formulations, elevating margins significantly over bulk grades. Downstream clients validate supply chains by auditing distillation and ion-exchange polishing trains, tightening entry barriers for new producers.

By End-User Industry: Personal Care Maintains a Rare Balance of Scale and Momentum

Personal care and hygiene dominated 39.85% global offtake in 2025 and will still pace the field with 5.48% CAGR to 2031. Brand owners push thinner, more discreet diaper cores and eco-framed feminine hygiene articles, both of which rely on super-absorbent polymer innovation. Building and construction employ acrylic dispersions in façade coatings that marry crack-bridging flexibility with low VOC compliance.

Automotive and transportation increasingly specify acrylic structural adhesives and thermal-management compounds for electric-vehicle battery packs. Electrical and electronics sectors demand high-purity grades for optically clear adhesive lamination and potting compounds that protect delicate circuitry. Packaging benefits from waterborne acrylic barriers, enabling fibre-based substrates to replace single-use plastics, while agriculture deploys SAP granules to cut irrigation frequency and boost seed germination.

Geography Analysis

Asia-Pacific accounted for 52.10% of global volume in 2025 and is projected to expand at a 5.36% CAGR to 2031. Regional producers capitalise on efficient cracker-to-ester integration, yet downstream consumption rises even faster as urbanisation, hygiene mandates, and infrastructure build intensify. China guides its chemical-industry roadmap toward higher-value chains, encouraging firms such as Wanhua to broaden into acrylic esters under governmental self-sufficiency drives.

North America maintains a resilient supply outlook anchored by integrated Gulf Coast complexes. US producers benefit from shale-advantaged propylene yet face environmental disclosure obligations that spur investment in bio-routes and carbon accounting. Electrical and electronics demand for ultra-high-purity glacial grades supports incremental debottlenecking.

Europe advances sustainability leadership through mandatory scope-3 reporting and circular-economy directives. The Middle East and Africa record the smallest base but witness a pronounced uptick in capacity planning as petrochemical producers capture value through derivative integration. Kuwait Petroleum’s equity entry into Wanhua underscores Gulf entities’ strategy to access Asian demand corridors. Collectively, geographic dynamics elevate the acrylic acid market as a cornerstone feedstock across differentiated economic stages.

Competitive Landscape

Global acrylic acid production remains highly consolidated. LG Chem disrupts through 100% bio-based monomer commercialisation, aligning with consumer-goods companies’ renewable-content pledges. Chinese entrants such as Wanhua employ advantaged propylene supply and state-backed financing to construct world-scale reactors, intensifying rivalry. Strategy centres on feedstock optionality, certified bio-content, and application-specific innovation. Process licensors offer bundled catalyst and evaporative crystallisation packages that shrink energy intensity by double digits. Digital twins optimise reactor uptime, while predictive maintenance reduces unscheduled shutdowns that previously destabilised the acrylic acid market supply.

Acrylic Acid Industry Leaders

Arkema

LG Chem

BASF

Dow

NIPPON SHOKUBAI CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kuwait Petroleum subsidiary acquired a 25% stake in Wanhua Chemical Group, signalling deeper Middle-Eastern integration into China’s downstream value chain.

- February 2025: LG Chem commenced commercial output of 100% plant-based acrylic acid at 100 tons per year scale after achieving USDA bio-preferred certification.

Global Acrylic Acid Market Report Scope

Acrylic acid is a colorless, unsaturated carboxylic acid with the molecular formula C3H4O2, produced through the two-stage catalytic oxidation of propylene. It can be polymerized to form homopolymers and copolymerized with esters and other vinyl monomers. Thus, acrylic acid is mainly used to produce polymers for different plastic products. It can also be used to produce adhesives, sealants, and surfactants.

The acrylic acid market is segmented by derivative, application, and geography. By derivative, the market is segmented into methyl acrylate, butyl acrylate, ethyl acrylate, 2-ethylhexyl acrylate, glacial acrylic acid, and superabsorbent polymer. By application, the market is segmented into paints and coatings, adhesives and sealants, surfactants, sanitary products, textiles, and other applications (consumer goods, etc.) The report also covers the market sizes and forecasts in 15 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons) for all the above segments.

| Methyl Acrylate |

| Butyl Acrylate |

| Ethyl Acrylate |

| 2-Ethylhexyl Acrylate |

| Glacial Acrylic Acid |

| Superabsorbent Polymer |

| Paints and Coatings |

| Adhesives and Sealants |

| Sanitary Products |

| Surfactants |

| Textiles |

| Other Applications |

| Technical Grade (~94 %) |

| Glacial Grade (more than or equal to 99%) |

| Ultra-high Purity (Electronics) |

| Personal Care and Hygiene |

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Packaging |

| Agriculture and Horticulture |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Derivative | Methyl Acrylate | |

| Butyl Acrylate | ||

| Ethyl Acrylate | ||

| 2-Ethylhexyl Acrylate | ||

| Glacial Acrylic Acid | ||

| Superabsorbent Polymer | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Sanitary Products | ||

| Surfactants | ||

| Textiles | ||

| Other Applications | ||

| By Purity Grade | Technical Grade (~94 %) | |

| Glacial Grade (more than or equal to 99%) | ||

| Ultra-high Purity (Electronics) | ||

| By End-user Industry | Personal Care and Hygiene | |

| Building and Construction | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Packaging | ||

| Agriculture and Horticulture | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the acrylic acid market?

The acrylic acid market size is 8.59 million t in 2026 and is projected to reach 11.01 million t by 2031.

Which derivative holds the largest share?

Butyl acrylate leads, representing 46.98% of global volume in 2025.

Which region dominates consumption?

Asia-Pacific accounts for 52.10% of worldwide demand owing to strong hygiene and infrastructure activity.

Why are bio-based grades gaining traction?

Certified bio-content lowers product carbon footprints and meets brand-owner sustainability targets, fostering rapid adoption in Europe and North America.

What is driving the fast growth of adhesives?

Electronics miniaturisation and automotive lightweighting favour acrylic adhesives that combine clarity, UV stability and mechanical strength, producing a 7.01% CAGR through 2031.

Page last updated on: