Market Overview

| Study Period | 2019 - 2030 |

|---|---|

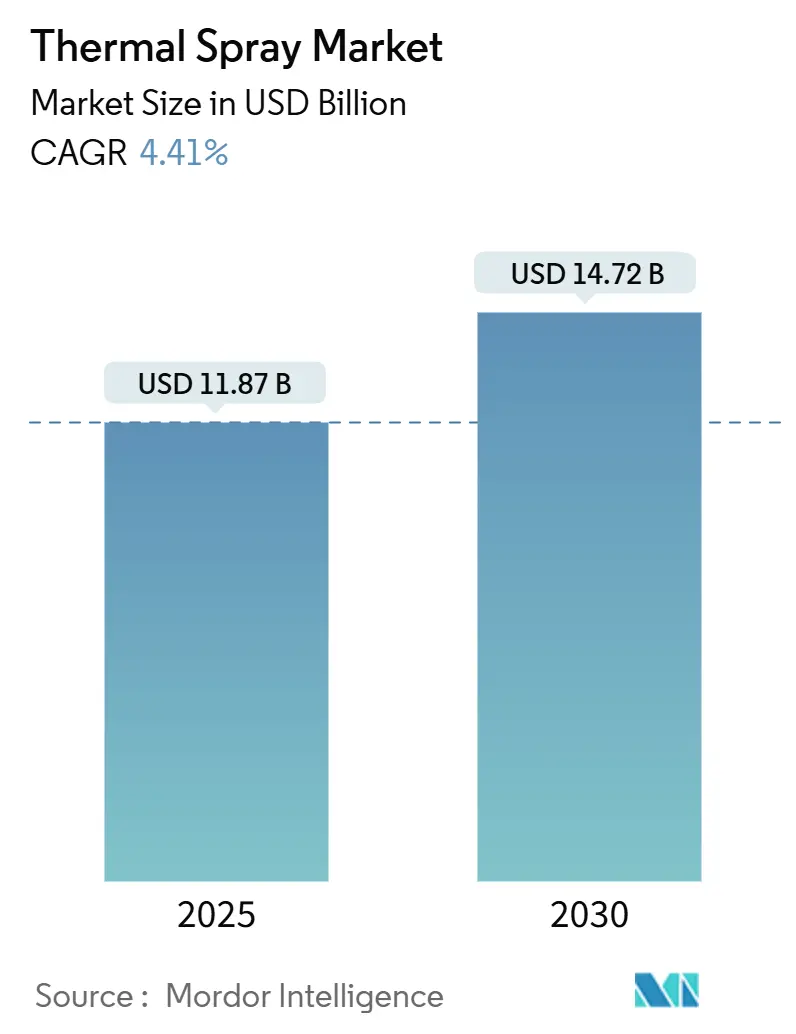

| Market Size (2025) | USD 11.87 Billion |

| Market Size (2030) | USD 14.72 Billion |

| Growth Rate (2025 - 2030) | 4.41% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

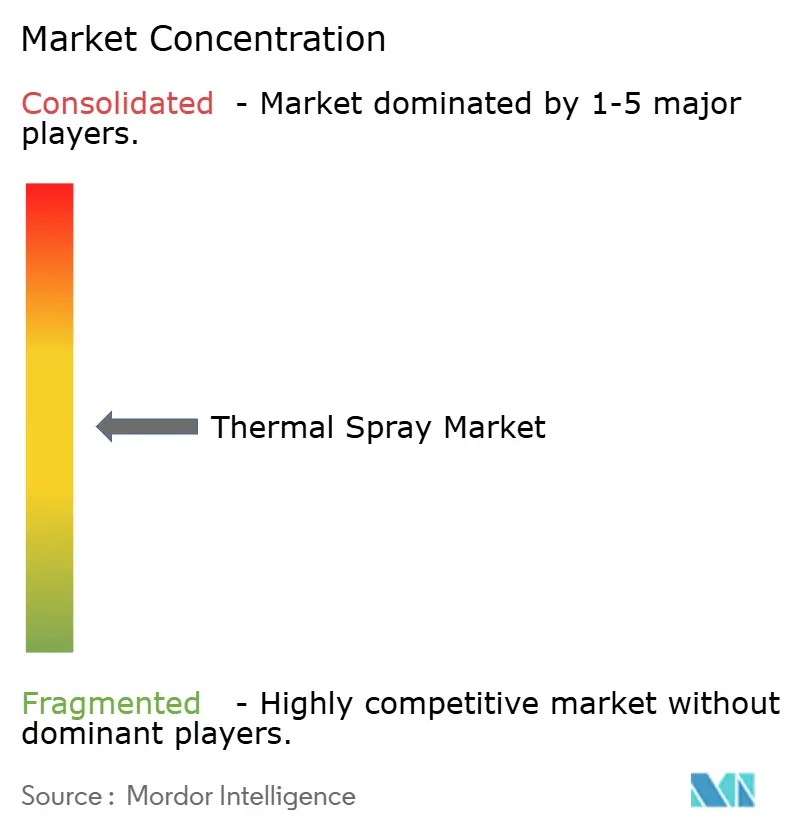

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thermal Spray Market Analysis by Mordor Intelligence

The Thermal Spray Market size is estimated at USD 11.87 billion in 2025, and is expected to reach USD 14.72 billion by 2030, at a CAGR of 4.41% during the forecast period (2025-2030). Demand is rising as aerospace, medical-device, and next-generation automotive manufacturers replace legacy surface treatments with high-performance coatings that extend part life and improve thermal management. Investments in automated equipment and real-time process monitoring continue to ease skilled-labor constraints, while the shift to electric energy spray techniques aligns with tightening environmental regulations. The Asia-Pacific manufacturing base is expanding rapidly, driving regional consumption of both coating materials and turnkey spray cells aimed at electronics and e-powertrain components.

Key Report Takeaways

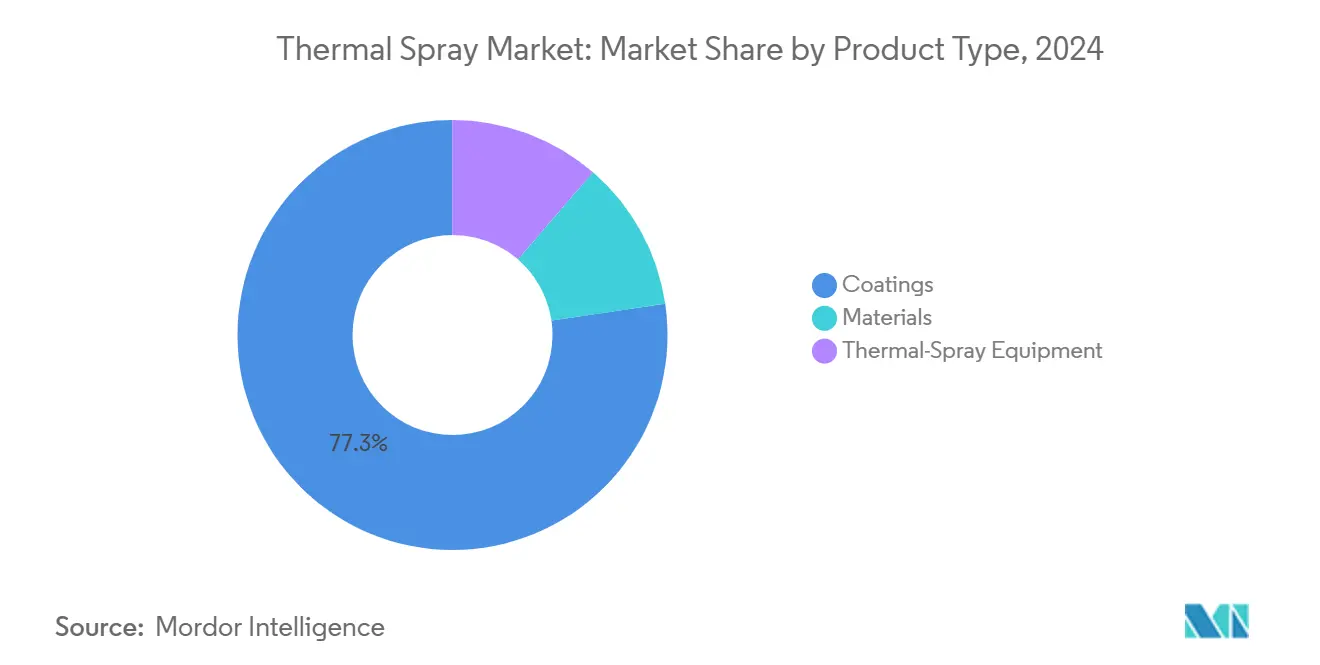

- By product type, coatings dominated with 77.31% of thermal spray market share in 2024, while equipment is forecast to post the fastest 6.31% CAGR through 2030.

- By coating technology, combustion processes held 45.91% of the thermal spray market size in 2024, whereas electric energy methods are expected to expand at a 4.60% CAGR over the same period.

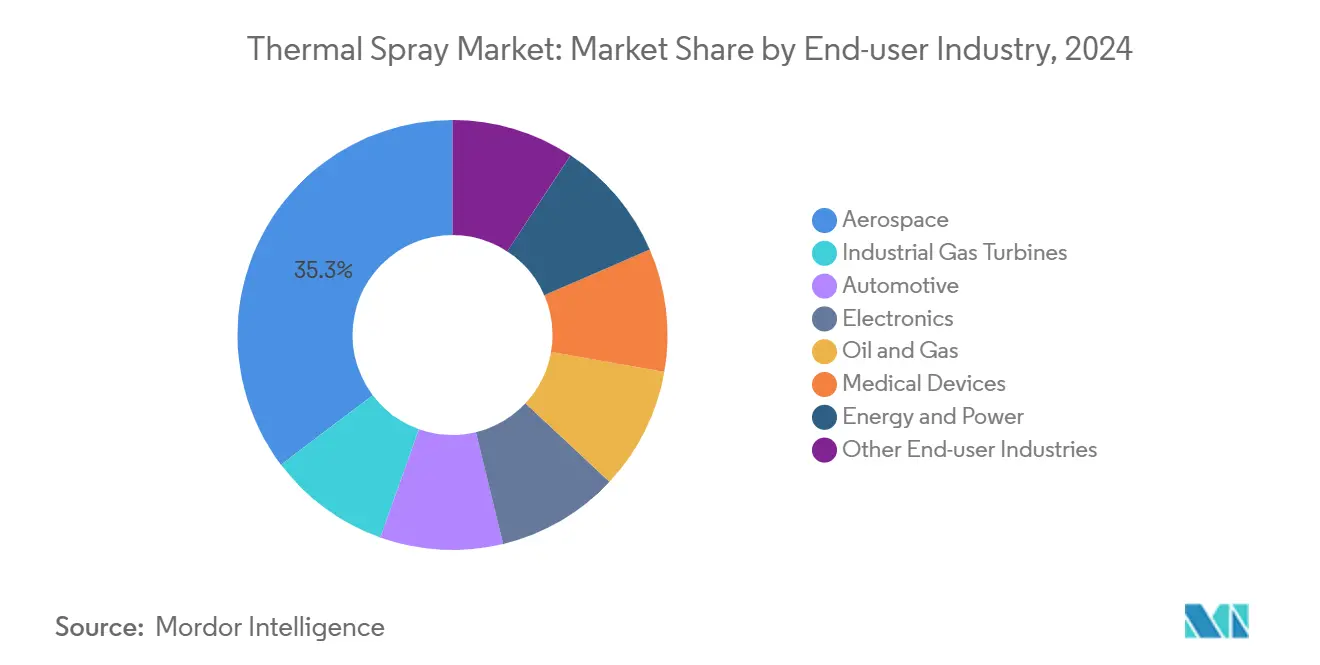

- By end-user industry, aerospace led with 35.30% revenue share in 2024; electronics is projected to register the highest 6.25% CAGR to 2030.

- By geography, Asia-Pacific accounted for 33.91% of global sales in 2024 and is advancing at the quickest 5.15% CAGR through 2030.

Global Thermal Spray Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermally-sprayed hydroxyapatite coatings in orthopedic and dental implants | +1.2% | North America, Europe, Global | Medium term (2-4 years) |

| Hard-chrome replacement in rotating equipment and hydraulic rods | +0.9% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Lightweight, high-temperature alloys in next-gen narrow-body aircraft engines | +1.1% | North America, Europe | Long term (≥ 4 years) |

| Hydrogen ICE and e-powertrains needing wear-resistant cylinder coatings | +0.8% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| High-entropy alloy coatings for geothermal and space assets | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Use of Thermally-Sprayed Hydroxyapatite Coatings in Orthopedic and Dental Implants

Thermally-sprayed hydroxyapatite coatings significantly improve bone ingrowth and reduce rejection rates, making them the preferred surface finish for load-bearing orthopedic screws, hip stems, and dental fixtures. Process control enables tailored porosity that matches cancellous bone morphology, accelerating osseointegration and shortening rehabilitation periods. Regulatory acceptance under U.S. FDA class II devices and CE marking frameworks supports rapid adoption among global implant makers. Growing geriatric populations in the United States, Germany, and Japan keep procedural volumes expanding, sustaining raw-material demand for calcium-phosphate powders. Equipment suppliers now bundle closed-loop robots and inline thickness gauges that assure repeatability, addressing surgeon concerns regarding coating delamination. As hospitals track infection metrics more closely, the bioactive nature of hydroxyapatite surfaces provides an additional clinical advantage that keeps the thermal spray market on a steady upswing.

Replacement of Hard-Chrome Plating in Rotating Equipment and Hydraulic Rods

Tightening REACH and OSHA rules on hexavalent chromium have forced OEMs to seek alternatives, positioning high-velocity oxygen fuel (HVOF) coatings as the sustainable successor. HVOF layers routinely exceed 60 HRC hardness while slashing porosity below 1%, more than doubling component lifetimes for hydraulic shafts and compressor impellers. Reduced maintenance translates into lower down-time costs for process industries, bolstering the total cost-of-ownership argument in favor of thermal spray market adoption. Automated boom manipulators now apply HVOF inside hard-to-reach bores, extending the addressable part universe. Early conversion programs in North American oil-and-gas drill fleets demonstrated payback periods under 18 months, spurring wider replication in Asian foundries. As ESG auditors tighten supply-chain scorecards, the switch from chrome baths to solvent-free spray booths provides an immediate emissions win.

Demand for High-Temperature Lightweight Alloys in Next-Gen Narrow-Body Aircraft Engines

Engine OEMs require blades and combustors to survive steady-state gas temperatures near 1 600 °C, a threshold that only advanced thermal barrier coatings can meet[1]MTU Aero Engines staff, “Digitalization in Aerospace: Oerlikon and MTU Aero Engines Initiate Establishment of a Smart Thermal Spray Factory,” mtu.de . Air plasma spray and electron-beam physical-vapor-deposition systems lay down yttria-stabilized zirconia layers with columnar microstructures that tolerate thermomechanical shock. When combined with bond coats containing rare-earth dopants, the stack increases turbine entry temperature by 100 °C, yielding 1-2 percentage-point fuel-burn gains. The thermal spray market benefits from long certification cycles that lock in specification adherence for an engine platform’s 20-year lifespan. Smart cells launched by Oerlikon Metco integrate digital twins that monitor plume velocity, ensuring uniformity across thousands of serialized blades. These aerospace commitments anchor capital-equipment orders and create a halo effect that validates thermal spray for mid-tier industrial gas turbines.

Automotive Shift Toward Hydrogen ICE and E-Powertrains Requiring Wear-Resistant Cylinder Coatings

Hydrogen combustion generates higher flame speeds and more water vapor, accelerating liner wear unless cylinder walls are protected with chromium-rich HVOF or arc-wire overlays. The same OEMs also demand high-conductivity coatings on electric-motor housings to dissipate heat away from permanent magnets, boosting inverter efficiency and range. Asia-Pacific assemblers deploy cold-spray robots for aluminum battery enclosures because the solid-state process avoids heat-affected zones and preserves mechanical strength[2]The Indian Thermal Spray Association staff, “What Is Cold Spray,” indtsa.org . Pilot lines in Korea confirm a 20% reduction in reject rates versus weld-on fin approaches. As zero-tailpipe policies advance in Europe and California, new drivetrain programs allocate greater budget shares to surface-engineering, expanding the thermal spray market footprint across the broader automotive supply chain.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of hard trivalent chrome coatings with lower CAPEX | -0.7% | Global | Short term (≤ 2 years) |

| Process repeatability and skilled-operator shortage in Asia and LATAM job-shops | -0.5% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Volatile pricing and supply risk for WC-Co and rare-earth oxide feedstocks | -0.6% | Global, China-dependent materials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emergence of Hard Trivalent Chrome Coatings with Lower CAPEX

Next-generation trivalent chrome baths provide 50 HRC hardness at investment levels one-third those of an entry-level HVOF cell, a value proposition that appeals to small hydraulic-rod refurbishers in cost-sensitive markets. Suppliers emphasize drop-in compatibility with existing fixtures, eliminating the need for new ventilation or dust-collection systems. Early field results confirm acceptable corrosion resistance for gear shafts operating below 200 °C, blunting near-term replacements by the thermal spray market in those niches. However, trivalent chrome struggles at higher thicknesses and cannot serve components exposed to combustion gases, which preserves the advantage for thermal barrier and wear-resistant overlays in aerospace as well as oil-and-gas pumps. The technology therefore acts as a selective restraint rather than a universal threat.

Process Repeatability and Skilled-Operator Shortage in Asia and Latin America Job-Shops

Coating uniformity hinges on correct traverse speed, standoff, and gas-flow balance, skills that take years to master. Many regional job-shops rely on manual guns without closed-loop feedback, leading to variation that fails automotive or defense audits. OEMs in Mexico and Vietnam report 8% scrap rates when sourcing locally versus 2% in European service centers. Equipment integrators now bundle vision systems and AI-based plume analytics that cut operator input by half, yet up-front capital and maintenance complexity slow deployment in emerging clusters. Unless training partnerships scale quickly, throughput bottlenecks may cap regional contribution to the global thermal spray market over the medium horizon.

Segment Analysis

By Product Type: Equipment Automation Drives Market Evolution

The equipment category is projected to expand at a 6.31% CAGR through 2030, surpassing consumables in growth momentum even though coatings retained a 77.31% share of the overall thermal spray market in 2024. Automated cells equipped with six-axis robots and closed-loop mass-flow control reduce coat-to-coat variance below 2 µm, a requirement set by turbine OEMs aiming for zero unplanned downtime.

Recurring revenues from powders and wires remain pivotal, as every kilogram deposited creates a pull-through effect for replacement nozzles and plasma electrodes. Tungsten carbide-cobalt powders continue to dominate wear-protection formulas, but scarcity and price volatility have sparked process recipes that extend tip life or recycle overspray. Suppliers now promote modular feeder units that switch between fine and coarse fractions in under 10 minutes, enhancing shop flexibility. Noise-attenuating booths and cyclone-based dust collectors clock double-digit growth rates, an ancillary but lucrative niche aligned with factory-safety mandates in Germany and South Korea.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Thermal Spray Coatings and Finishes: Electric Energy Processes Gain Momentum

Electric energy methods, spearheaded by plasma spray and twin-wire arc, are forecast to advance at 4.60% CAGR, steadily eroding the 45.91% share still held by combustion techniques in 2024. Semiconductor fabs rely on ultra-clean plasma chambers that demand less than 5 ppm contamination, a specification achievable only with closed-loop gas controls and high-purity argon used in electric-arc systems.

Combustion-based HVOF remains indispensable for oversized mining drills and steel-rolling equipment that require thick layers at rapid deposition rates. Still, hybrid gun designs now offer on-the-fly switching between kerosene and hydrogen fuels, improving versatility while cutting CO₂ output by 20%. Europe’s Fit-for-55 package is projected to levy higher carbon prices on propane-based flame cells, gradually tipping procurement toward electrically heated plasma torches. This progressive mix shift underscores how sustainability agendas intersect with performance-driven purchasing, reshaping supplier playbooks in the thermal spray market.

By End-User Industry: Electronics Sector Drives Innovation

Electronics is projected to register a 6.25% CAGR to 2030, the fastest among end-users, even though aerospace commanded 35.30% of 2024 revenue. Chip-fabrication plants deploy yttria and alumina coatings on etch chambers to shield silicon wafers from particle contamination that would otherwise force costly rework. Volume expansions underway in Taiwan and the United States multiply repeat orders for high-purity powders, tilting raw-material flows toward white-ceramic lines rather than metallic blends.

Aerospace maintains leadership through entrenched engine overhauls and strict certification that favor incumbents with longstanding airworthiness approvals. More-electric aircraft architectures bring lightweight aluminum housings that must be cold-sprayed with copper alloys to manage stray currents, giving rise to incremental coating SKUs. Industrial gas turbines, automotive, and medical devices each contribute mid-single-digit growth, underpinned by grid upgrades, hydrogen pilot lines, and an aging demographic that spurs joint replacements. Oil-and-gas applications remain lumpy, tied to rig counts and price cycles, but deep-water subsea pumps still rely on cermet overlays, providing a dependable service revenue stream for the thermal spray market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific contributed 33.91% of the thermal spray market in 2024 and is forecast to climb at a 5.15% CAGR, reflecting aggressive onshoring of semiconductor fabs in China and advanced battery plants in Japan. Regional governments channel subsidies into smart-machinery imports, lowering payback barriers for automated spray booths. Still, the skilled-labor gap persists, pushing OEMs to partner with vocational institutes in India and Malaysia that offer operator certification under ISO 14924 standards.

North America and Europe are underpinned by legacy aerospace fleets and strict occupational safety guidelines favoring chrome-free overlays. The United States remains the largest single-country buyer of tungsten carbide powders, while Germany leads in plasma-torch exports. Both regions invest in research and development focused on hydrogen-compatible coatings.

South America and the Middle East and Africa trail in absolute revenues but post steady double-digit equipment orders linked to petrochemical plant upgrades and mining conveyor refurbishments. Each geography therefore plays to distinct end-market triggers, yet converges on a common trajectory of digitalized and environmentally compliant surface-engineering solutions within the global thermal spray market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market shows moderate fragmentation. Bodycote invests in HIP-plus-spray packages that combine densification with wear coatings, delivering turnkey post-processing for additive parts. Linde PLC focuses on high-purity gas delivery skids, bundling them with plasma controllers to lock in consumables pull-through. Midsize players pursue regional niches. Praxair Surface Technologies licenses a cold-spray cell to Mexican gearbox rebuilders, while Wall Colmonoy pitches nickel-base rods tailored for sugar-mill shredder refurbishment in Brazil. Start-ups such as Keronite develop plasma-electrolytic oxidation hybrids that blur the boundary between spray and anodizing, challenging incumbents on light metals. Across tiers, software-driven quality control and predictive maintenance emerge as key differentiators, rewarding vendors that integrate sensors and cloud analytics into their equipment portfolios.

Thermal Spray Industry Leaders

-

BODYCOTE

-

Linde PLC

-

OC Oerlikon Management AG

-

Castolin Eutectic

-

Kennametal Inc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: Oerlikon and MTU Aero Engines began building a smart thermal spray factory to digitalize aerospace coating, integrating inline analytics for traceability.

- June 2024: Oerlikon Group opened an Advanced Coating Technology Center for turbine components, expanding research and development capacity.

Global Thermal Spray Market Report Scope

Thermal spraying is an industrial coating process where a consumable is applied as a spray of finely divided semi-molten or molten droplets to produce coatings and then deposit them onto a surface. It is a technology that improves or restores the surface of a solid material. Thermal spraying aids in applying coatings to various materials and components to resist wear, corrosion, cavitation, abrasion, or heat.

The thermal spray market is segmented by product type, thermal spray coatings and finishes, end-user industry, and geography. By product type, the market is segmented into coatings, materials, and thermal spray equipment. By thermal spray coatings and finishes, the market is segmented into combustion and electric energy. By end-user industry, the market is segmented into aerospace, industrial gas turbines, automotive, electronics, oil and gas, medical devices, energy and power, steel making, textile, and printing and paper. The report also covers the market sizes and forecasts for the thermal spray market in 27 countries across major regions. For each segment, the market size and forecast are provided based on revenue (USD).

By Product Type

| Coatings | |||

| Materials | Coating Materials | Powders | Ceramics |

| Metals | |||

| Polymers and Other Powders | |||

| Wires/Rods | |||

| Other Coating Materials | |||

| Supplementary Materials (Auxiliary Material) | |||

| Thermal-Spray Equipment | Thermal Spray Coating Systems | ||

| Dust Collection Equipment | |||

| Spray Guns and Nozzles | |||

| Feeder Equipment | |||

| Spare Parts | |||

| Noise-reducing Enclosures | |||

| Other Thermal Spray Equipment | |||

By Thermal Spray Coatings and Finishes

| Combustion |

| Electric Energy |

By End-user Industry

| Aerospace |

| Industrial Gas Turbines |

| Automotive |

| Electronics |

| Oil and Gas |

| Medical Devices |

| Energy and Power |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Coatings | |||

| Materials | Coating Materials | Powders | Ceramics | |

| Metals | ||||

| Polymers and Other Powders | ||||

| Wires/Rods | ||||

| Other Coating Materials | ||||

| Supplementary Materials (Auxiliary Material) | ||||

| Thermal-Spray Equipment | Thermal Spray Coating Systems | |||

| Dust Collection Equipment | ||||

| Spray Guns and Nozzles | ||||

| Feeder Equipment | ||||

| Spare Parts | ||||

| Noise-reducing Enclosures | ||||

| Other Thermal Spray Equipment | ||||

| By Thermal Spray Coatings and Finishes | Combustion | |||

| Electric Energy | ||||

| By End-user Industry | Aerospace | |||

| Industrial Gas Turbines | ||||

| Automotive | ||||

| Electronics | ||||

| Oil and Gas | ||||

| Medical Devices | ||||

| Energy and Power | ||||

| Other End-user Industries | ||||

| By Geography | Asia-Pacific | China | ||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Malaysia | ||||

| Thailand | ||||

| Indonesia | ||||

| Vietnam | ||||

| Rest of Asia-Pacific | ||||

| North America | United States | |||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| NORDIC Countries | ||||

| Turkey | ||||

| Russia | ||||

| Rest of Europe | ||||

| South America | Brazil | |||

| Argentina | ||||

| Colombia | ||||

| Rest of South America | ||||

| Middle-East and Africa | Saudi Arabia | |||

| Qatar | ||||

| United Arab Emirates | ||||

| Nigeria | ||||

| Egypt | ||||

| South Africa | ||||

| Rest of Middle-East and Africa | ||||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What was the global thermal spray market value in 2025?

The market reached USD 11.87 billion in 2025.

Which end-user segment is expanding fastest?

Electronics is projected to grow at a 6.25% CAGR through 2030 thanks to semiconductor thermal-management needs.

Why are electric-energy spray methods gaining share?

Plasma and electric-arc systems provide tighter contamination control and lower emissions, aligning with environmental regulations.

Which region leads in market growth?

Asia-Pacific combines a 33.91% revenue share with a 5.15% CAGR, driven by electronics and battery manufacturing expansion.

How are regulations affecting chrome plating alternatives?

REACH and OSHA restrictions on hexavalent chromium are pushing industry toward HVOF and other thermal spray coatings.

What competitive factor is most critical for suppliers today?

Integrated automation, digital monitoring and predictive maintenance capabilities have become decisive differentiators.

Page last updated on: