Female Contraceptives Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

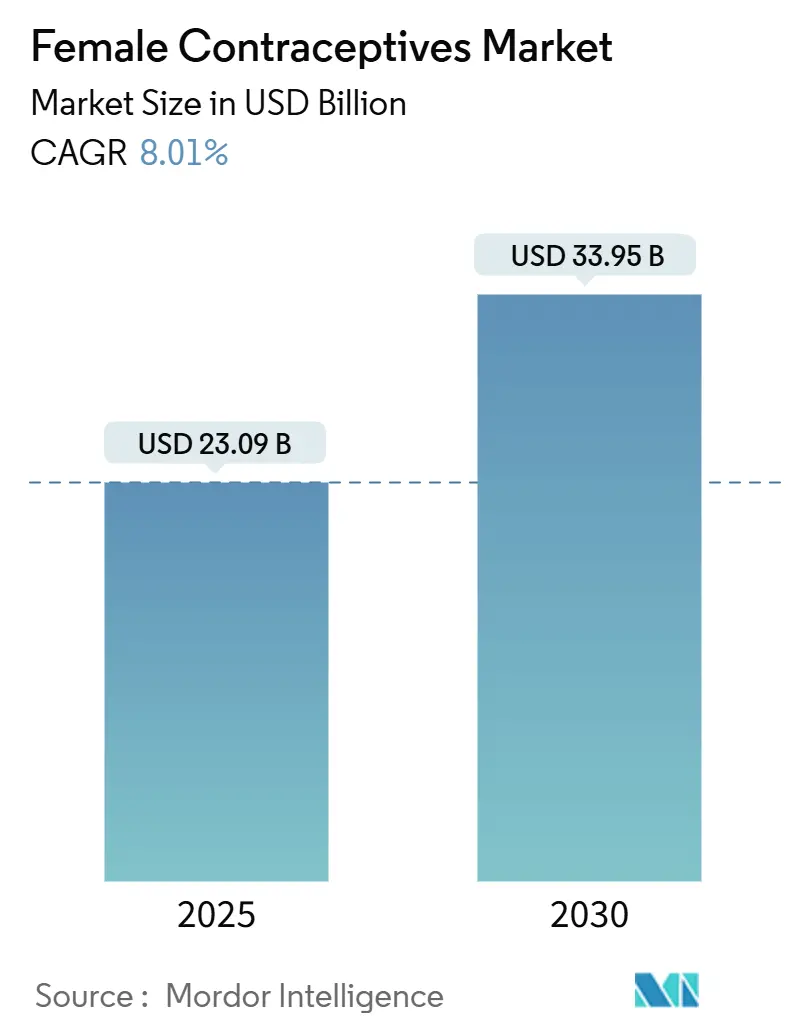

| Market Size (2025) | USD 23.09 Billion |

| Market Size (2030) | USD 33.95 Billion |

| Growth Rate (2025 - 2030) | 8.01% CAGR |

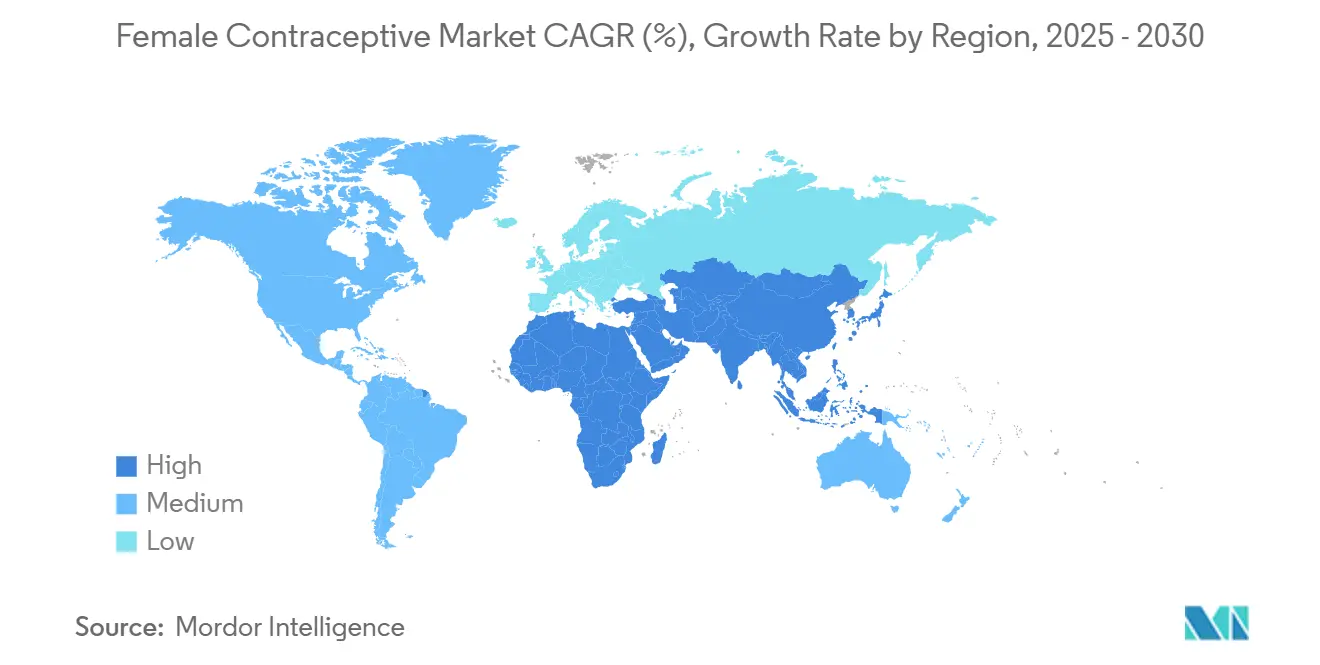

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Female Contraceptives Market Analysis by Mordor Intelligence

The female contraceptive market is valued at USD 23.09 billion in 2025 and is forecast to reach USD 33.95 billion by 2030, posting an 8.01% CAGR. Accelerated demand for non-hormonal methods, rapid digital health uptake, and supportive policy measures are steering expansion. The February 2025 FDA approval of MIUDELLA, the first new copper intrauterine system in four decades, validates commercial momentum for hormone-free options. Simultaneously, direct-to-consumer telehealth platforms are widening access, while legal scrutiny of certain hormonal products is nudging users toward safer profiles. Intensifying R&D in low-cost implants and biodegradable devices is opening new addressable populations, particularly in emerging economies. Together, these forces have created a resilient growth path for the female contraceptive market.

Key Take Aways

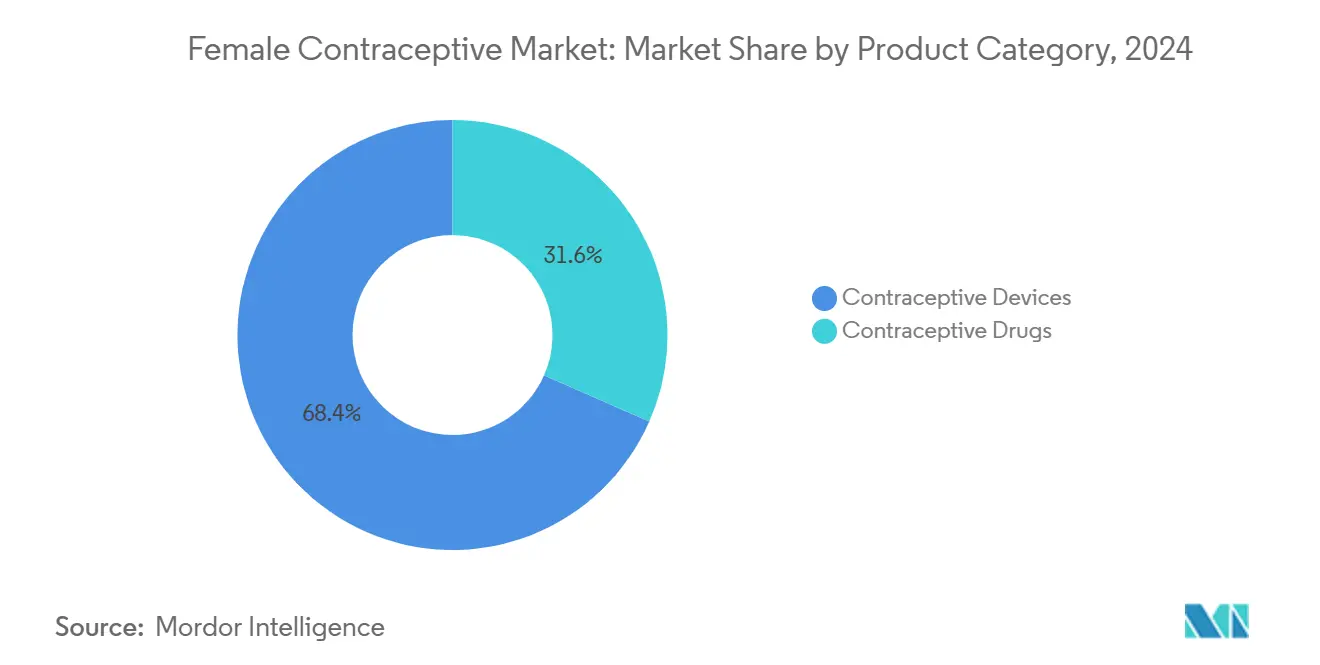

- By product category, devices commanded 68.4% of female contraceptive market share in 2024, whereas drugs are projected to expand at an 8.1% CAGR through 2030.

- By hormone type, combined formulations led with 51.2% revenue share in 2024; progesterone-only products record the fastest CAGR at 8.8% during 2025-2030.

- By duration of action, short-acting methods held 60.1% of the female contraceptive market size in 2024, while long-acting reversible contraceptives grow at an 9.3% CAGR to 2030.

- By age group, women aged 20-29 years accounted for 34.8% share of the female contraceptive market in 2024; the 30-39 years cohort registers a 9.1% CAGR through 2030.

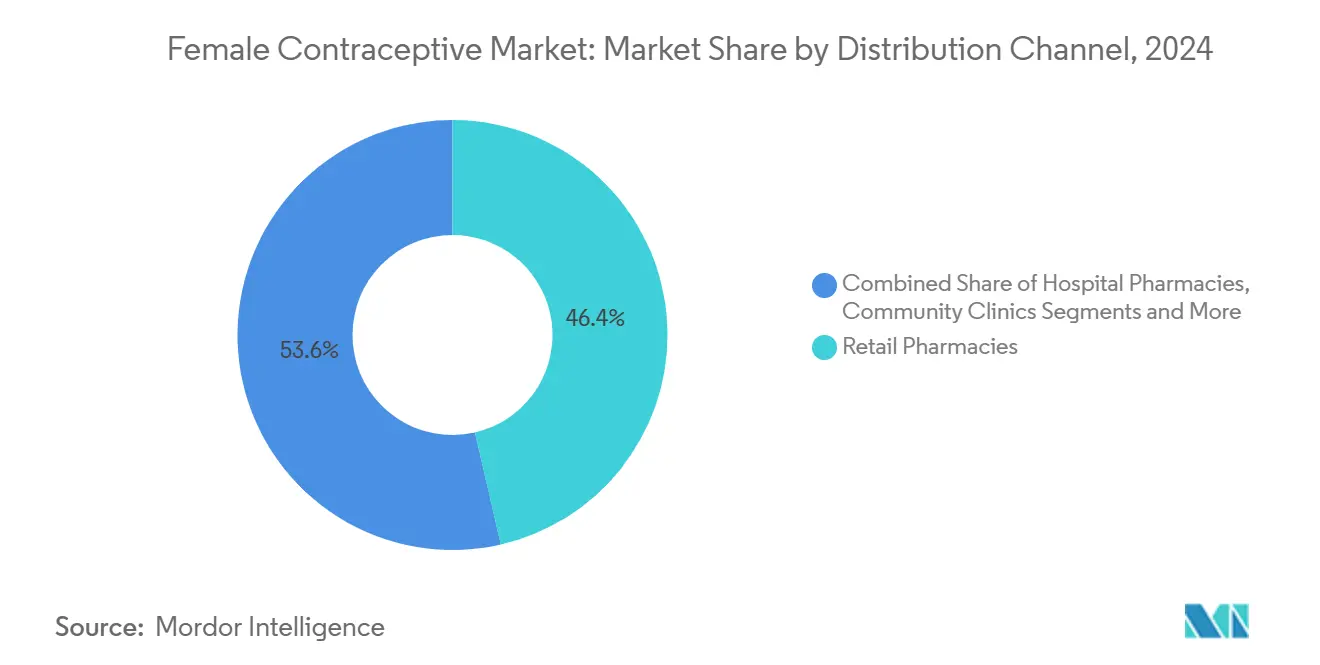

- By distribution channel, retail pharmacies led with 46.4% revenue share in 2024, whereas online/direct-to-consumer platforms deliver an impressive 11.3% CAGR during the same period.

- By end-user setting, home-use products dominated with 68.4% revenue share in 2024, while clinical-use modalities grow at a 9.5% CAGR through 2030.

- By geography, Asia-Pacific led with 32.40% market share in 2024; the Middle East and Africa region posts the highest CAGR of 8.96% over 2025-2030.

Global Female Contraceptives Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for advanced and innovative contraceptives such as hormone-free copper IUDs | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government and market-player initiatives to increase awareness and access of female contraceptives | +1.8% | Global with emphasis on Middle East & Africa | Long term (≥ 4 years) |

| Increasing trend of tele-prescribing and telehealth | +1.5% | North America, Europe, Urban Asia-Pacific | Short term (≤ 2 years) |

| Investment by market players in low-cost implants | +1.2% | Asia-Pacific, Africa, Latin America | Medium term (2-4 years) |

| HPV-linked cancer risk awareness accelerating barrier-method adoption | +0.9% | Global with emphasis on North America & Europe | Medium term (2-4 years) |

| Regulatory green-light for over-the-counter daily oral contraceptive pills | +0.8% | North America, Europe, select emerging markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Growing Preference for Advanced and Innovative Contraceptives

Momentum for hormone-free contraception is accelerating. MIUDELLA received FDA clearance in February 2025, introducing a lower-copper IUD that maintains 99% efficacy while reducing bleeding and pain. Clinical pipelines support the trend, with Ovaprene’s Phase 3 trial read-out expected in 2025, combining barrier action and local drug delivery. R&D is targeting polymer coatings and alloy modifications to ease insertion and limit adverse events. The value proposition resonates with women seeking effective yet endocrine-neutral options, shifting demand away from legacy hormonal products. Device makers are therefore allocating larger capital budgets to copper and polymer-based platforms, signalling sustained expansion for this segment of the female contraceptive market.

Government and Market-Player Initiatives for Awareness and Access

Public-private coalitions are narrowing the contraceptive funding deficit. During the 2024 UN General Assembly, donors pledged USD 350 million toward the global contraceptive financing gap, projected at USD 1.5 billion by 2030.[1]United Nations Population Fund, “Governments and Philanthropies Commit US$350 Million to Family Planning,” unfpa.org The Gates Foundation is contributing USD 280 million annually for innovative technologies and community programs through 2030. Early results are evident in Uganda, where integrated youth reproductive-health campaigns unexpectedly boosted uptake among women aged 25-49 years.[2]Global Health: Science and Practice, “Integrating Adolescent and Youth Sexual Reproductive Health Interventions,” ghspjournal.org Such commitments underpin long-term growth across the female contraceptive market, particularly in resource-limited regions.

Increasing Trend of Tele-Prescribing and Telehealth

Digital channels have redrawn supply chains. Hims & Hers reached 2.2 million subscribers in 2024, earning USD 1.5 billion and guiding to USD 2.4 billion for 2025. Thirty US states now permit pharmacists to prescribe contraceptives, multiplying consumer touchpoints. A 2024 survey reported 49.7% of pill, patch, and ring users obtaining contraceptives from preferred sources, with over half opting for telehealth or OTC channels. Fast fulfilment, privacy, and subscription models are expanding market penetration, consolidating telehealth’s role as a key accelerator of the female contraceptive market.

Investment by Market Players in Low-Cost Implants

Leading companies are channeling resources into affordable long-acting reversible contraceptives. Pfizer and partners aim to supply 320 million doses of Sayana Press to low-income nations, addressing underutilisation of LARCs despite their efficacy. Biodegradable implants in Phase 1 trials may eliminate removal procedures, lowering system costs.[4]Global Health Technologies Coalition, “Six Innovative Contraceptive Technologies on the Horizon,” ghtcoalition.org Adolescents currently show 5-6% LARC adoption, signalling upside once affordability and education barriers are removed. These investments promise to extend the reach of the female contraceptive market in price-sensitive geographies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Religious, social and ethical issues for adoption of various contraceptives such as IUDs | -1.3% | Middle East, Africa, conservative areas of Asia and Latin America | Long term (≥ 4 years) |

| Product liability litigation and risks of side effects such as hormonal pills and implants | -0.9% | North America, Europe | Medium term (2-4 years) |

| Regulatory challenges coupled with limited insurance coverage | -0.7% | Global with emphasis on emerging markets | Medium term (2-4 years) |

| Supply-chain fragility for key hormonal APIs | -0.5% | Global with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

Source: Mordor Intelligence

Religious, Social and Ethical Issues for Contraceptive Adoption

Cultural norms restrict uptake in several regions. The Family Planning Policy Atlas MENA 2023 indicates that 15% of women aged 15-49 in the Middle East and North Africa still have unmet contraceptive needs due to social constraints.[3]European Parliamentary Forum for Sexual and Reproductive Rights, “White Paper MENA 2023,” epfweb.org A 2025 Ethiopian study found rural women 53% less likely to use LARCs than urban peers. In the United States, proposed policy shifts under Project 2025 could curtail free emergency contraception for 48 million users. Such headwinds demand culturally nuanced outreach to sustain the female contraceptive market trajectory.

Product Liability Litigation and Side-Effect Risks

Heightened legal exposure weighs on growth. A multidistrict litigation created in February 2025 to consolidate Depo-Provera tumor claims, with potential settlements exceeding USD 1 million per severe case. CooperSurgical faces over 2,600 suits over alleged Paragard breakage. The threat of costly judgments drives insurers to raise premiums, inflating barriers for new entrants. This environment accelerates the pivot to non-hormonal devices yet tempers overall expansion in the female contraceptive market.

Segment Analysis

By Product Category: Devices Dominate, Drugs Accelerate

Devices held 68.4% of female contraceptive market share in 2024, anchored by intrauterine systems that deliver 99% efficacy alongside low maintenance. MIUDELLA showcases the appetite for innovations that cut copper load yet preserve effectiveness. The segment benefits from sustained investments in polymer coatings that reduce bleeding, broadening acceptance among first-time users. Contraceptive drugs, while smaller, are rising at an 8.1% CAGR through 2030 as formulators refine dosing and extend release profiles. The first OTC progestin pill has expanded retail reach, positioning oral agents for faster gains inside the female contraceptive market size.

Advanced vaginal rings and non-hormonal candidates like Ovaprene are poised to open new sub-segments. Drug developers are leveraging sustained-release matrices to shorten dosing gaps and improve adherence. Together, these innovations are expected to close the convenience gap with devices while retaining pharmacological control. Competitive intensity is therefore increasing as firms straddle both modalities within the female contraceptive market.

Note: Segment shares of all individual segments available upon report purchase

By Hormone Type: Combined Formulations Lead, Progesterone-Only Gains

Combined estrogen–progesterone products accounted for 51.2% revenue in 2024. Their long clinical history and predictable bleeding patterns reinforce physician preference. However, progesterone-only options are expanding at an 8.8% CAGR, driven by safety for women with estrogen contraindications and emerging prolonged-release injectables. Sayana Press distribution partnerships aim to supply 320 million doses to low-income markets. That plan could lift the female contraceptive market size in underserved areas.

Research into non-hormonal pathways continues, propelled by demand for side-effect-free contraception. Early copper-alloy devices and spermicidal barriers represent tangible progress. These alternatives give manufacturers scope to hedge against liability exposure while diversifying offerings in the female contraceptive market.

By Duration of Action: Short-Acting Methods Prevail, LARCs Surge

Short-acting methods controlled 60.1% of 2024 revenue because users appreciate rapid reversibility. Yet LARCs are recording an 9.3% CAGR to 2030 thanks to superior efficacy and minimal user action. Phase 1 trials of biodegradable implants target cost savings by removing removal visits.[4]Global Health Technologies Coalition, “Six Innovative Contraceptive Technologies on the Horizon,” ghtcoalition.org Successful commercialization would reinforce LARC appeal and enlarge the female contraceptive market share for long-duration technologies.

Adolescents remain cautious; uptake sits near 6% due to myths about fertility impact. Targeted counseling can narrow perception gaps, as satisfaction climbs above 80% among informed users. Manufacturers partnering with youth-focused NGOs may therefore accelerate penetration and further diversify the female contraceptive market.

By Age Group: 20-29 Years Lead, 30-39 Years Accelerate

Women aged 20-29 comprised 34.8% of 2024 demand, reflecting high fertility intent management. Meanwhile, the 30-39 cohort is growing 9.1% annually as career and delayed childbirth trends intensify. Studies show women aged 40-49 are 1.87 times more likely to choose LARCs compared with younger peers. This pattern indicates market gaps for age-tailored education.

Integrated adolescent programs in Uganda unexpectedly raised uptake among women 25-49, proving spill-over benefits of cross-generational outreach. Such findings guide marketers toward mixed-age messaging that enhances overall female contraceptive market penetration.

By Distribution Channel: Retail Dominates, Online Platforms Surge

Retail pharmacies delivered 46.4% of 2024 sales owing to on-the-spot availability. They now complement digital channels rather than replace them, as telehealth subscriptions rise 45% year over year. The female contraceptive market size attributed to online platforms is advancing at an 11.3% CAGR through 2030.

Policy is catalyzing the shift; pharmacist prescribing authority in 30 US states boosts convenience. Nonetheless, hospital and fertility clinics retain importance for physician-inserted devices. Hybrid service models are emerging, with brick-and-mortar chains integrating virtual consultations to retain share within the female contraceptive market.

By End-User Setting: Home Use Predominates, Clinical Settings Evolve

Home settings represented 68.4% of 2024 usage as privacy and autonomy resonate strongly. The March 2024 OTC pill approval added further momentum. Microneedle patches and self-injected depot formulations in development could widen the menu of home-compatible solutions.

Clinical settings still matter for professional LARC insertion, driving a 9.5% CAGR for in-clinic procedures through 2030. More comprehensive counseling services and bundled postpartum insertion initiatives tie device placement to existing care pathways. These strategies anchor continued growth of the female contraceptive market across both settings.

Geography Analysis

Asia-Pacific led the female contraceptive market with 31.60% share in 2024. Government-backed family-planning campaigns, falling fertility rates, and the rise of women’s digital health ecosystems underpin leadership. China and India supply scale, while Japan and South Korea broaden uptake of LARCs among late-marrying populations. Telehealth penetration is growing quickly, with the women’s digital health sector forecast to expand at 20.54% CAGR to 2034.

North America ranks second aided by mature insurance coverage and regulatory flexibility. Pharmacist prescribing authority has multiplied access points, benefiting rural users. Contraceptive deserts persist for 19 million US women, but telehealth and OTC options are gradually shrinking gaps in the female contraceptive market. Europe exhibits strong reimbursement yet heterogeneity in preferred methods. Northern markets tend toward LARCs while Southern Europe maintains oral dominance.

The Middle East and Africa region is the fastest-growing with a 9.30% CAGR to 2030. Algeria and Tunisia showcase supportive legal frameworks.[3]European Parliamentary Forum for Sexual and Reproductive Rights, “White Paper MENA 2023,” epfweb.org Merck for Mothers has reached 8.3 million African women through mobile information services. The UAE exemplifies commercial promise as its contraceptive device segment is set to double between 2022 and 2030. Social norms still restrain adoption in conservative areas, yet rising urbanization and education catalyze progressive attitudes that favour female contraceptive market expansion.

Competitive Landscape

The female contraceptive market is moderately concentrated. Bayer AG, Organon & Co., and Pfizer Inc. leverage expansive portfolios and global distribution to maintain leadership. Organon collaborates with Cirqle Biomedical on a non-hormonal gel candidate and licensed Daré Biosciences’ Xaciato to diversify offerings. Sebela Women’s Health secured FDA approval for MIUDELLA, bringing competitive pressure to copper IUD incumbents.

Smaller innovators are gaining visibility. Femasys earned a CE mark for FemBloc, the first non-surgical permanent contraception method, aiming for initial European launches in 2025. Telehealth disruptors Ro and Hims & Hers bypass legacy supply chains, monetising subscription convenience and data analytics to claim share within the female contraceptive market.

Litigation risk shapes strategy. Depo-Provera and Paragard lawsuits highlight the cost of safety lapses, pushing manufacturers toward lower-risk non-hormonal pipelines. Entrants must secure robust post-market surveillance and liability coverage to compete effectively. The resulting environment rewards firms that pair medical innovation with digital engagement and proactive risk management.

Female Contraceptives Industry Leaders

-

Bayer AG

-

Pfizer Inc

-

Teva Pharmaceuticals

-

Organon

-

CooperSurgical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Femasys Inc. received CE mark for its FemBloc delivery system, enabling non-surgical permanent birth control launch in select European states

- February 2025: Sebela Women’s Health gained FDA approval for MIUDELL, a hormone-free copper intrauterine system offering up to three years of protection

- February 2025: The Judicial Panel on Multidistrict Litigation created MDL 3140 consolidating Depo-Provera meningioma lawsuits

- January 2025: Bayer commenced an endometriosis awareness initiative that supports its contraceptive portfolio.

Global Female Contraceptives Market Report Scope

As per the scope of the report, contraception is defined as the intentional prevention of conception through the use of various devices, sexual practices, chemicals, drugs, or surgical procedures to prevent a woman from becoming pregnant. These devices and drugs function by acting as a physical barrier between the sperm and ovum or by changing the mechanism of ovulation. The Female Contraceptive Market is segmented by Contraceptive Drugs (Oral Contraceptives, Topical Contraceptives, Contraceptive Injections, Spermicides), Devices (Female Condoms, Diaphragms and Caps, Vaginal Rings, Contraceptive Sponges, Sub-dermal Contraceptive Implants, Intra-Uterine Contraceptive Devices (IUCDs) and Other Devices), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Product Category | Contraceptive Drugs | Oral Contraceptives | Combined Pills | |

| Progestin-Only Pills | ||||

| Contraceptive Injections | ||||

| Topical Contraceptives | ||||

| Spermicides | ||||

| Contraceptive Devices | Female Condoms | |||

| Diaphragms & Cervical Caps | ||||

| Vaginal Rings | ||||

| Contraceptive Sponges | ||||

| Sub-Dermal Implants | ||||

| Intra-Uterine Devices (IUD) | Copper IUDs | |||

| Hormonal IUDs | ||||

| By Hormone Type | Estrogen-Only | |||

| Progesterone-Only | ||||

| Combined (E+P) | ||||

| By Duration of Action | Short-Acting Methods | |||

| Long-Acting Reversible Contraceptives (LARC) | ||||

| By Age Group | 15-19 Years | |||

| 20-29 Years | ||||

| 30-39 Years | ||||

| 40+ Years | ||||

| By Distribution Channel | Hospital Pharmacies | |||

| Retail Pharmacies | ||||

| Online and DTC Platforms | ||||

| Community / Fertility Clinics | ||||

| By End-User Setting | Home Use | |||

| Clinical Use | ||||

| Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| Australia | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | GCC | |||

| South Africa | ||||

| Rest of Middle East and Africa | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Contraceptive Drugs | Oral Contraceptives | Combined Pills | |

| Progestin-Only Pills | |||

| Contraceptive Injections | |||

| Topical Contraceptives | |||

| Spermicides | |||

| Contraceptive Devices | Female Condoms | ||

| Diaphragms & Cervical Caps | |||

| Vaginal Rings | |||

| Contraceptive Sponges | |||

| Sub-Dermal Implants | |||

| Intra-Uterine Devices (IUD) | Copper IUDs | ||

| Hormonal IUDs | |||

| Estrogen-Only |

| Progesterone-Only |

| Combined (E+P) |

| Short-Acting Methods |

| Long-Acting Reversible Contraceptives (LARC) |

| 15-19 Years |

| 20-29 Years |

| 30-39 Years |

| 40+ Years |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online and DTC Platforms |

| Community / Fertility Clinics |

| Home Use |

| Clinical Use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current Global Female Contraceptive Market size?

The Global Female Contraceptive Market is projected to register a CAGR of 8.5% during the forecast period (2025-2030)

1. What is driving the fastest growth in the female contraceptive market?

The strongest momentum comes from non-hormonal innovations such as MIUDELLA and from telehealth distribution models that remove access barriers

2. Which product type leads the female contraceptive market share today?

Devices remain dominant, holding 68.4% share in 2024 thanks to widespread adoption of intrauterine systems.

3. Why are long-acting reversible contraceptives gaining popularity?

LARCs combine 99% efficacy with convenience, and new biodegradable implants are set to lower follow-up costs, contributing to an 9.3% forecast CAGR.

4. Which region is expanding the fastest in female contraceptives?

The Middle East and Africa region posts the highest projected CAGR at 8.96% between 2025 and 2030 due to shifting societal norms and rising health budgets

5. How is telehealth influencing contraceptive access?

Platforms like Hims & Hers and Ro provide prescription services online, supporting double-digit growth for direct-to-consumer channels.

6. What legal risks affect the female contraceptive industry?

Ongoing lawsuits around products such as Depo-Provera and Paragard IUD highlight liability exposure, prompting manufacturers to prioritize safety and diversify into non-hormonal products.

Page last updated on: June 18, 2025