Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

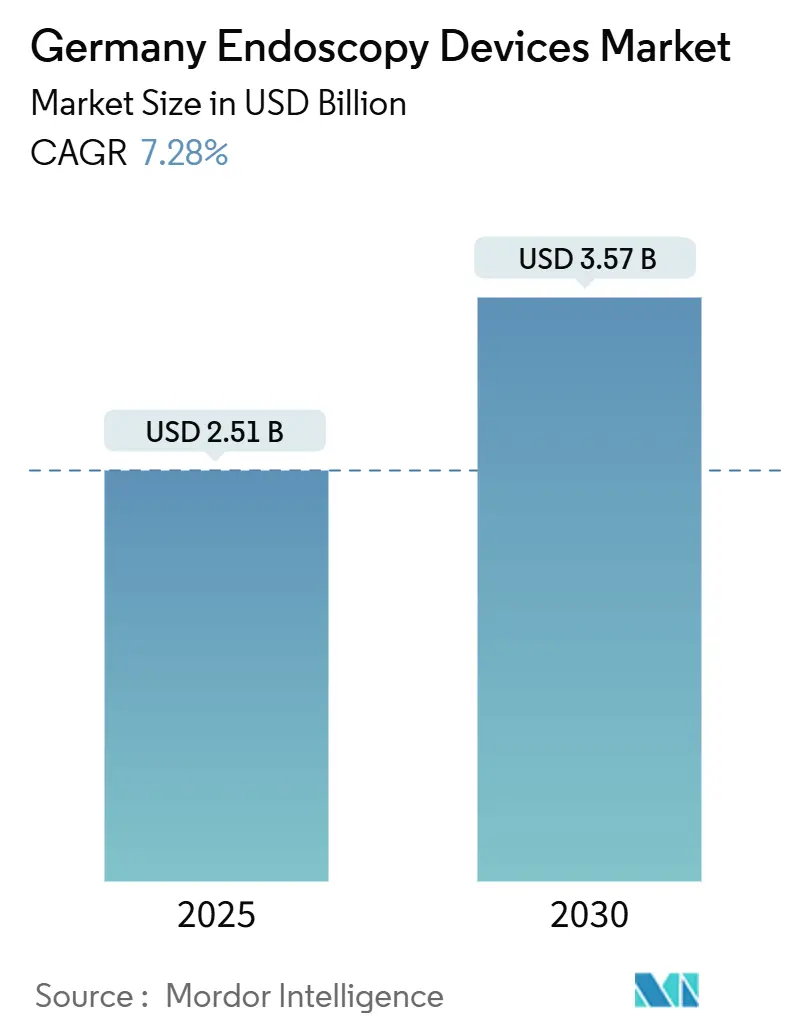

| Market Size (2025) | USD 2.51 Billion |

| Market Size (2030) | USD 3.57 Billion |

| Growth Rate (2025 - 2030) | 7.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Endoscopy Devices Market Analysis by Mordor Intelligence

Germany endoscopy devices market size is valued at USD 2.51 billion in 2025 and is set to reach USD 3.57 billion by 2030, reflecting a 7.28% CAGR during the period. Demographic pressures from an aging population, rapid AI-assisted visualization upgrades, and centralized procurement under the Hospital Reform 2025 are the primary forces behind this trajectory. Hospitals are focusing on 4K and AI imaging to curb adenoma miss rates that stand at 34% under white-light colonoscopy, while outpatient tele-endoscopy networks unlock procedure volumes in metropolitan hubs. The reform’s Leistungsgruppen framework pools purchasing power, enabling volume-based contracts that compress unit prices and standardize quality benchmarks, which in turn accelerates equipment refresh cycles. Meanwhile, pending EU PFAS restrictions are prompting supply-chain overhauls for fluoropolymer substitutes, sharpening vendor competition around sustainable components. These combined trends keep the Germany endoscopy devices market on a clear upswing through 2030.

Key Report Takeaways

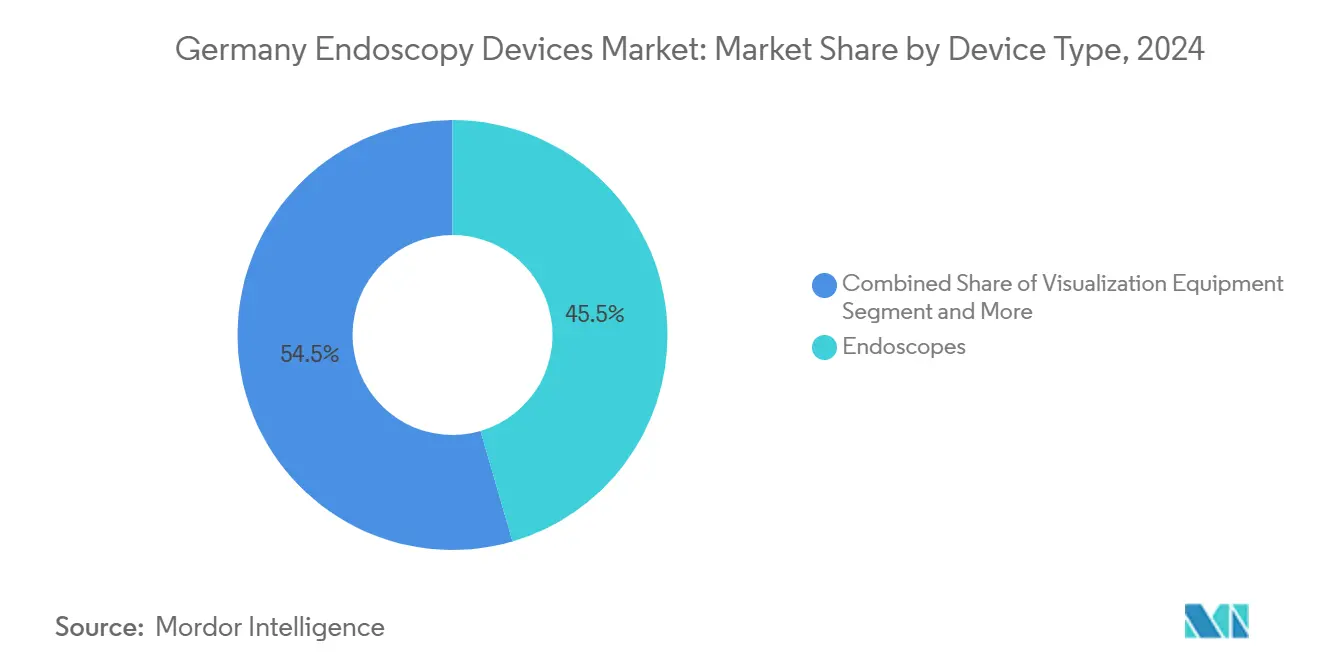

- By device type, endoscopes led with 45.55% of Germany endoscopy devices market share in 2024, while visualization equipment is projected to expand at an 11.25% CAGR to 2030.

- By application, gastroenterology occupied 48.53% of Germany endoscopy devices market size in 2024, and cardiology is advancing at a 9.85% CAGR through 2030.

- By end user, hospitals accounted for 69.63% share of the Germany endoscopy devices market in 2024, whereas ambulatory surgery centers are forecast to grow at 9.87% CAGR to 2030.

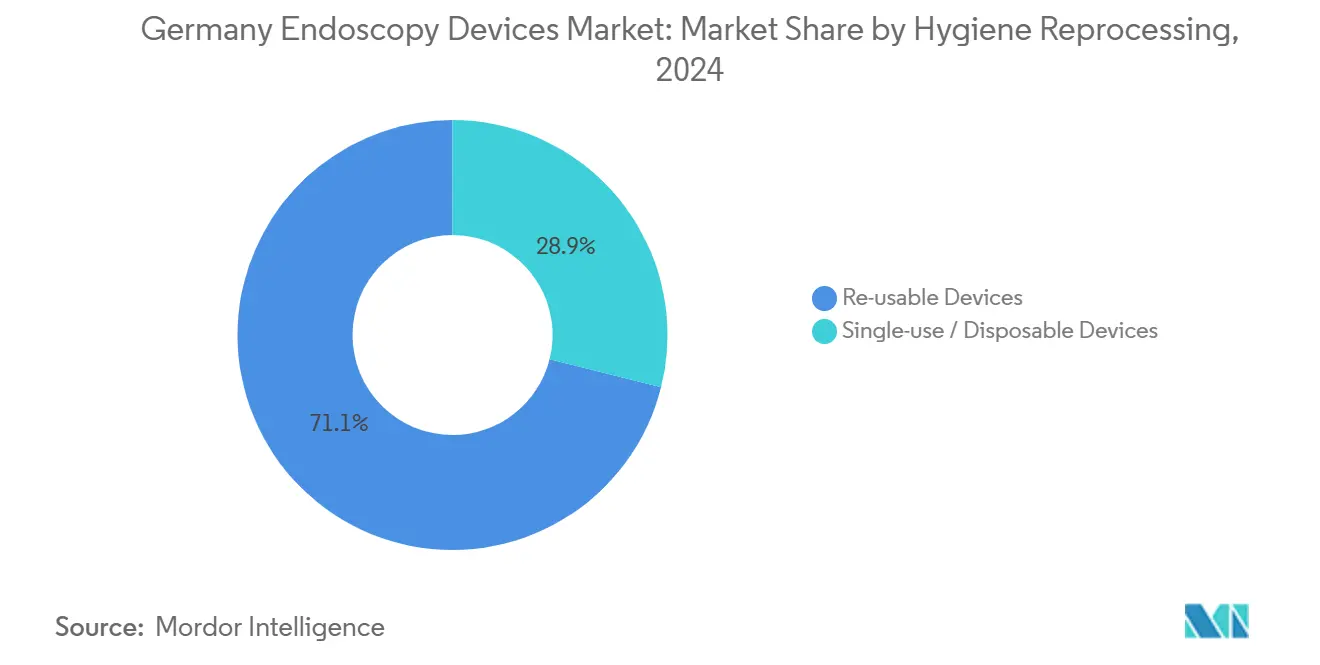

- By hygiene practice, reusable platforms retained 71.13% share in 2024, yet single-use systems are set to accelerate at 12.7% CAGR to 2030.

Germany Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements enabling AI-assisted imaging | +1.8% | National university hospitals | Medium term (2-4 years) |

| Growing preference for minimally invasive surgeries | +1.5% | Urban medical centers | Long term (≥ 4 years) |

| Aging population & rising GI disorder prevalence | +2.1% | Eastern states | Long term (≥ 4 years) |

| German Hospital Reform 2025 centralizing procurement | +1.2% | Public hospitals | Short term (≤ 2 years) |

| EU MDR-driven replacement of aging endoscopes | +0.9% | All regions | Medium term (2-4 years) |

| Surge in outpatient tele-endoscopy networks | +0.8% | Metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements Enabling AI-Assisted Imaging

AI platforms are steadily transforming the Germany endoscopy devices market. Olympus launched its cloud-based ENDO-AID suite, CADDIE, CADU, and SMARTIBD, in Q1 2025 to tackle high adenoma miss rates that reach 34% under conventional white-light screening. Government-funded GI-Insight research at the University of Würzburg adds local algorithm refinement, while MHz-OCT projects in Schleswig-Holstein bring real-time 3D tissue mapping into routine workflows. EVIS X1 upgrade kits let hospitals embed AI without replacing entire towers, a cost advantage under the Leistungsgruppen budget ceilings. Regulatory amendments to the Medical Devices Operator Ordinance effective February 2025 mandate robust cybersecurity, giving established vendors with secure cloud infrastructure a clear competitive edge in the Germany endoscopy devices market.

Growing Preference for Minimally Invasive Surgeries

Hospitals are embracing laparoscopic and endoluminal techniques that shorten stays and cut DRG expenditures, fueling the Germany endoscopy devices market. Uptake of 4K scopes, Narrow Band Imaging, and Texture and Color Enhancement Imaging supports complex interventions such as endoscopic submucosal dissection, documented in more than 1,000 German cases with favorable outcomes[1]Ulrike Denzer, “Neue Endoskopische Verfahren,” Thieme, thieme-connect.de. Demand for multi-energy devices like THUNDERBEAT grows as surgeons value single-instrument vessel sealing up to 7 mm. Interventional cardiology mirrors this shift; transesophageal and structural procedures propel a 9.85% CAGR in cardiology applications, broadening equipment portfolios and contributing to sustained equipment renewals in the Germany endoscopy devices market.

Aging Population & Rising GI Disorder Prevalence

Older demographics guarantee a high procedure baseline. Individuals aged 65 and older reached 22% of the population in 2024 and will exceed 25% by 2050, sustaining Germany endoscopy devices market demand. Claims data covering 25 million insured persons show 80% of women and 69% of men aged 55-64 underwent colorectal exams within a decade. Organized screening raises colonoscopy volumes while therapeutic endoscopy manages detected lesions, ensuring recurring equipment cycles and consistent utilization rates across the Germany endoscopy devices market.

German Hospital Reform 2025 Centralizing Procurement

The Krankenhausversorgungsverbesserungsgesetz pools purchasing decisions into Leistungsgruppen, increasing leverage over vendors and compressing price points in the Germany endoscopy devices market. The Transformationsfonds finances digital systems that integrate with advanced endoscopic platforms, while Vorhaltevergütung compensates hospitals for maintaining complex services, lowering investment risk. Coordinated tenders now favor suppliers offering nationwide service capabilities, accelerating market consolidation and reinforcing technology standardization.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled endoscopy technicians | -1.4% | Rural hospitals | Long term (≥ 4 years) |

| High capital cost of advanced equipment | -1.1% | Smaller hospitals | Medium term (2-4 years) |

| EU PFAS restrictions on fluoropolymer components | -0.7% | National manufacturers | Medium term (2-4 years) |

| MDR recertification backlog & temporary shortages | -0.5% | All regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Endoscopy Technicians

Germany faces a workforce shortfall that limits utilization despite adequate hardware. Part-time trends, constrained training slots, and migration to urban centers leave rural facilities understaffed. Advanced therapeutic procedures require specialized skills, delaying deployment of AI-enabled systems and dampening near-term growth in the Germany endoscopy devices market. Service consolidation into larger centers partially offsets this gap but raises patient-travel barriers.

High Capital Cost of Advanced Equipment

4K towers and AI modules carry steep price tags. Hospitals operating under DRG margins delay purchases and rely on NUB financing, yet approval uncertainty complicates multi-year planning. Ambulatory centers feel the pinch most, as volume thresholds for cost recovery remain high. Bundled-service contracts and pay-per-use models emerge but adoption is gradual, restraining speed of technology penetration in the Germany endoscopy devices market.

Segment Analysis

By Device Type: AI Integration Drives Visualization Growth

Visualization equipment recorded the fastest 11.25% CAGR from 2025 to 2030, while endoscopes still anchor 45.55% of the 2024 Germany endoscopy devices market. Hospitals increasingly direct capital to 4K processors, OLED monitors, and AI overlay modules that raise mucosal detection accuracy without necessitating full tower replacements. Flexible scopes dominate the endoscope subset thanks to broad GI and pulmonary reach, whereas rigid systems cater to ENT and orthopedic niches. Capsule endoscopes, though reimbursed sparingly, offer non-invasive small-bowel views and keep incremental sales alive.

Adoption of single-use bronchoscopes and ureteroscopes accelerates as infection-control protocols tighten post-pandemic. EU MDR traceability favors disposable form factors, pushing vendors to refine biodegradable materials. Meanwhile, multi-energy hand instruments supporting advanced therapeutic procedures remain indispensable, ensuring balanced growth across the Germany endoscopy devices market. Enhanced imaging and AI analytics together re-shape hospital wish lists, firmly positioning visualization equipment at the investment forefront.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Cardiology Interventions Accelerate Growth

Gastroenterology held 48.53% of Germany endoscopy devices market size in 2024, sustained by nationwide colonoscopy programs and rising therapeutic ESD volumes. Cardiology, though smaller, posts the highest 9.85% CAGR as endoscopic ultrasound converges with structural heart interventions, creating hybrid workflows that rely on high-resolution probes. Pulmonology keeps steady momentum with AI-assisted nodule detection, while orthopedics and gynecology enlarge scope portfolios through minimally invasive arthroscopy and hysteroscopic procedures.

Cross-disciplinary innovation blurs boundaries: Olympus Aplio i800 EUS system extends from hepato-pancreato-biliary to cardiac imaging, illustrating platform convergence[2]Olympus Corporation, “Olympus to Begin Sales Activities of Aplio i800 EUS in Europe,” olympus-global.com. Procedure complexity elevates demand for multi-modal devices and real-time analytics, which in turn solidify long-term procurement pipelines across clinical departments of the Germany endoscopy devices industry.

By End User: Ambulatory Centers Drive Outpatient Shift

Hospitals captured 69.63% of Germany endoscopy devices market share in 2024 due to concentration of complex therapeutic interventions. Ambulatory surgery centers, benefiting from the AOP reimbursement expansion, post a 9.87% CAGR on the back of cost-efficient, high-throughput colonoscopy programs. Office-based practices leverage mobile towers and tele-consult links, widening screening access in suburban belts.

Hospitals retain dominance for advanced interventions requiring anesthesia back-up and immediate surgical conversion pathways. However, portable visualization stacks tailored for ambulatory centers, and soon integrating AI SaaS modules, lower entry barriers, redistributing capital budgets within the Germany endoscopy devices market. Vendor service models now segment between 24/7 in-hospital support and lean field coverage for office clinics, ensuring target-specific value propositions.

By Hygiene & Reprocessing: Single-Use Adoption Accelerates

Reusable platforms accounted for 71.13% of 2024 sales, yet single-use scopes pace ahead at 12.7% CAGR through 2030. MDR traceability demands, stricter BfArM reprocessing rules, and residual infection risk collectively favor disposables. Comparative cost models reveal near-parity when factoring labor, detergent, sterilizer depreciation, and unplanned downtime[3]Christoph Werner et al., “Healing of gastrointestinal ulceration using Hemospray,” Scientific Reports, nature.com. Vendors counter environmental critiques by piloting plant-based polymers and closed-loop recycling programs.

Hospitals hedge risk by combining reusable high-definition colonoscopes for routine screening with single-use duodenoscopes for high-contamination ERCPs. This blended fleet approach balances cost and safety, ensuring sustained growth across both product lines in the Germany endoscopy devices market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Southern states, Bavaria, Baden-Württemberg, and North Rhine-Westphalia, anchor equipment demand due to dense networks of university hospitals and med-tech manufacturers. These regions adopt AI modules early, leveraging local vendor support and research partnerships that shorten validation cycles. Munich’s cluster of academic centers and start-ups acts as a living laboratory, accelerating clinical deployment and feedback loops.

Eastern states such as Saxony and Brandenburg display lower baseline utilization yet exhibit above-average growth rates as modernization grants target infrastructure gaps. Colonoscopy uptake in Saxony reached only 18%, compared with 23% in southern counterparts, highlighting untapped potential. Federal funding under the Hospital Future Act directs digital and imaging upgrades into these underserved areas, thereby lifting long-term prospects for the Germany endoscopy devices market.

Metropolitan hubs, Berlin, Hamburg, Frankfurt, pioneer tele-endoscopy networks that link suburban clinics with urban specialists. Portable towers shipped to satellite sites feed live video back to central reading centers, broadening access. Logistics proximity to manufacturing plants in Tuttlingen and Hamburg ensures rapid maintenance turnaround, which further cements vendor relationships in these high-volume locales. Regional procurement consortia under Leistungsgruppen unify specifications, thereby leveling purchase terms across Germany.

Competitive Landscape

The Germany endoscopy devices market is moderately concentrated, with Olympus and KARL STORZ holding leading positions through broad product portfolios and embedded service networks. Olympus capitalizes on ENDO-AID cloud analytics launched in 2025, offering subscription models that bundle software updates with hardware leasing. KARL STORZ reinforced its supply chain by acquiring medi-G in February 2025, rebuilding the Meßkirch site with advanced assembly lines that secure laparoscopic component availability.

AI competency is the new competitive frontier. Start-ups partnering with university hospitals aim to inject niche algorithms into legacy towers, yet MDR certification hurdles impede rapid scaling. Established vendors leverage internal regulatory teams and existing notified-body relationships to fast-track approvals, maintaining their edge in the Germany endoscopy devices market. Collaboration with cloud-security providers ensures compliance with the Medical Devices Operator Ordinance, a differentiator for hospital CIOs under the Hospital Future Act mandates.

Opportunity whitespace lies in portable visualization solutions for ambulatory centers and single-use scope ecosystems. Multinational suppliers co-develop environmental recycling pathways with regional waste processors, addressing sustainability directives and bolstering brand equity. Outcome-based contracting gains traction as hospitals tie payments to adenoma detection or readmission reductions, altering traditional capex discussions. Vendors offering data analytics dashboards that prove quality gains strengthen their negotiating stance within centralized tenders.

Germany Endoscopy Devices Industry Leaders

-

B. Braun Melsungen AG

-

Stryker Corporation

-

Boston Scientific Corporation

-

KARL STORZ SE & Co. KG

-

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: KARL STORZ completed the business transfer of medi-G, rebuilding the Meßkirch factory with smart machinery to stabilize component supply for laparoscopy, ENT, and pediatric endoscopy.

- September 2024: Olympus introduced the CH-S700-08-LB 4K camera head for urological endoscopy in Europe, integrating true 4K sensors and Narrow Band Imaging to enhance mucosal visualization.

Germany Endoscopy Devices Market Report Scope

As per the scope of the report, endoscope devices are the minimally-invasive and can be inserted into the body to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries. The Germany Endoscopy Devices Market is segmented by Type of Devices ( Endoscopes, Endoscopic Operative Devices, Visualization Equipment ) and Application (Gastroenterology, Pulmonology, Orthopedics, Cardiology, Gynecology, and Urology, Other Applications). The report offers the value (in USD million) for the above segments.

By Device Type

| Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | |

| Capsule Endoscopes | |

| Disposable/Single-use Endoscopes | |

| Endoscopic Operative Devices | |

| Visualization Equipment |

By Application

| Gastroenterology |

| Pulmonology |

| Orthopaedic Surgery |

| Cardiology |

| Gynaecology & Urology |

| Other Clinical Applications |

By End User

| Hospitals |

| Ambulatory Surgery Centres |

| Office-based / Out-patient Clinics |

By Hygiene & Reprocessing

| Re-usable Devices |

| Single-use / Disposable Devices |

| By Device Type | Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | ||

| Capsule Endoscopes | ||

| Disposable/Single-use Endoscopes | ||

| Endoscopic Operative Devices | ||

| Visualization Equipment | ||

| By Application | Gastroenterology | |

| Pulmonology | ||

| Orthopaedic Surgery | ||

| Cardiology | ||

| Gynaecology & Urology | ||

| Other Clinical Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Office-based / Out-patient Clinics | ||

| By Hygiene & Reprocessing | Re-usable Devices | |

| Single-use / Disposable Devices |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Germany endoscopy devices market in 2025?

The market stands at USD 2.51 billion in 2025 and is forecast to reach USD 3.57 billion by 2030, expanding at a 7.28% CAGR.

Which device segment is growing fastest?

Visualization equipment, driven by AI integration and 4K resolution, is rising at an 11.25% CAGR through 2030.

What is driving single-use scope adoption?

Infection-control priorities, MDR traceability, and PFAS material restrictions push hospitals toward disposable endoscopes growing at 12.7% CAGR.

Why are ambulatory centers important for growth?

Reimbursements under the AOP framework favor outpatient procedures, enabling ambulatory surgery centers to grow at 9.87% CAGR.

How does the Hospital Reform 2025 affect purchasing?

The Leistungsgruppen structure centralizes procurement, securing volume discounts and standardizing quality benchmarks nationwide.

Which regions offer the most untapped potential?

Eastern states such as Saxony and Brandenburg, where colonoscopy utilization rates lag the national average, present higher growth opportunities.

Page last updated on: