Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

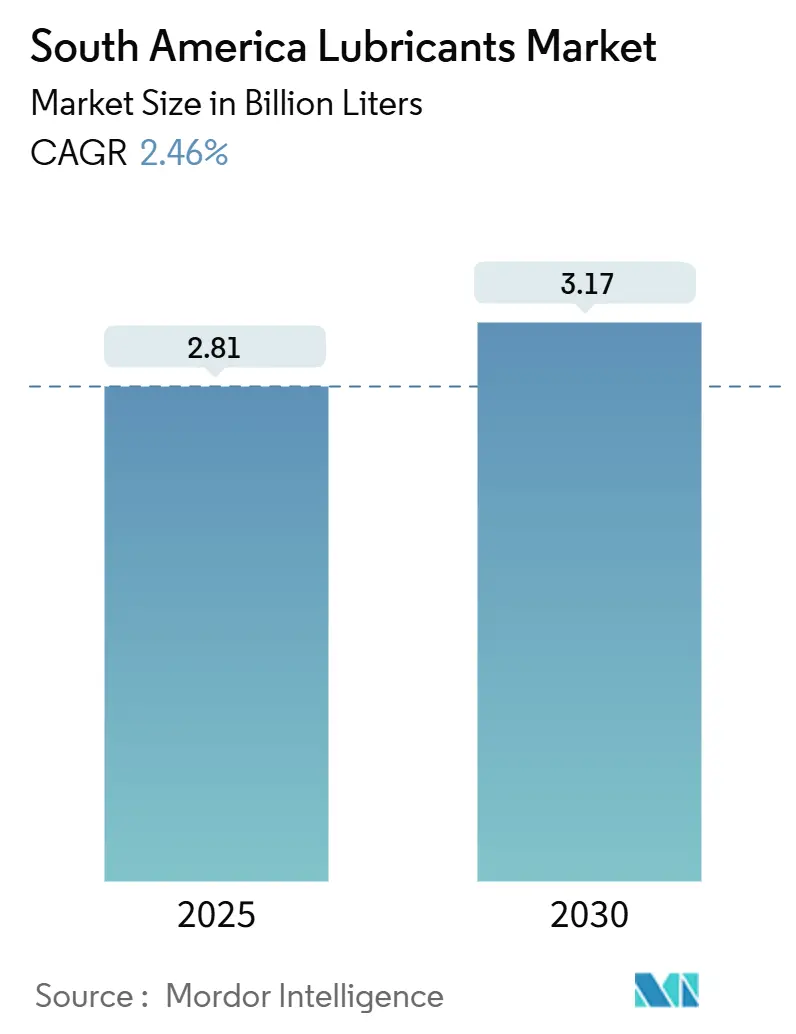

| Market Volume (2025) | 2.81 Billion Liters |

| Market Volume (2030) | 3.17 Billion Liters |

| Growth Rate (2025 - 2030) | 2.46% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Lubricants Market Analysis by Mordor Intelligence

The South America Lubricants Market size is estimated at 2.81 Billion Liters in 2025, and is expected to reach 3.17 Billion Liters by 2030, at a CAGR of 2.46% during the forecast period (2025-2030). Recovering regional freight mileage, expanding offshore oil activity, and ongoing industrial modernization underpin demand, even as currency volatility and policy shifts create pockets of risk. Automotive manufacturing in Brazil, deep-water exploration in Brazil and Guyana, and mining automation in Chile and Peru together secure a broad consumption base. Renewable power additions, led by wind and solar, are introducing new needs for turbine and hydraulic fluids, while stricter emissions standards are accelerating migration toward low-SAPS and synthetic formulations. Competitive intensity remains moderate but rising as multinationals strengthen local supply chains and regional firms seek scale through mergers and distribution alliances.

Key Report Takeaways

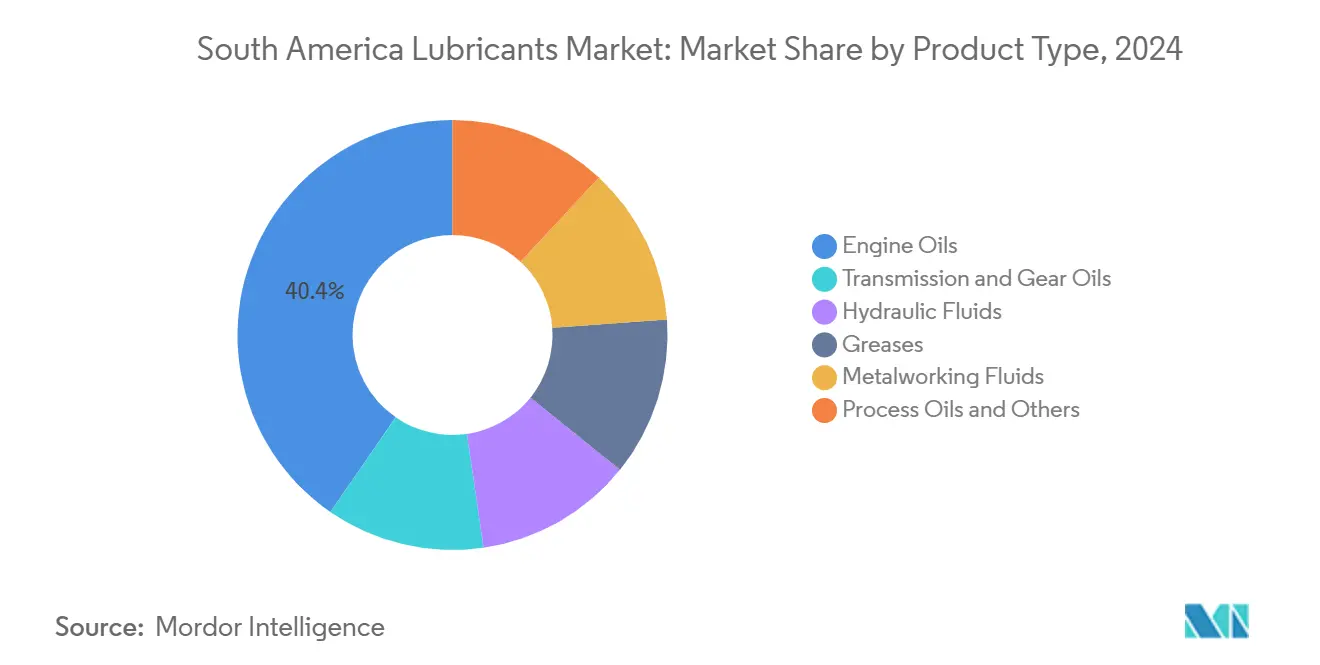

- By product type, engine oils accounted for 40.36% of the South America lubricants market share in 2024; hydraulic fluids are forecast to expand at a 2.78% CAGR through 2030.

- By base oil, mineral oils captured 62.23% of the South America lubricants market size in 2024, whereas bio-based alternatives are projected to post a 3.12% CAGR to 2030.

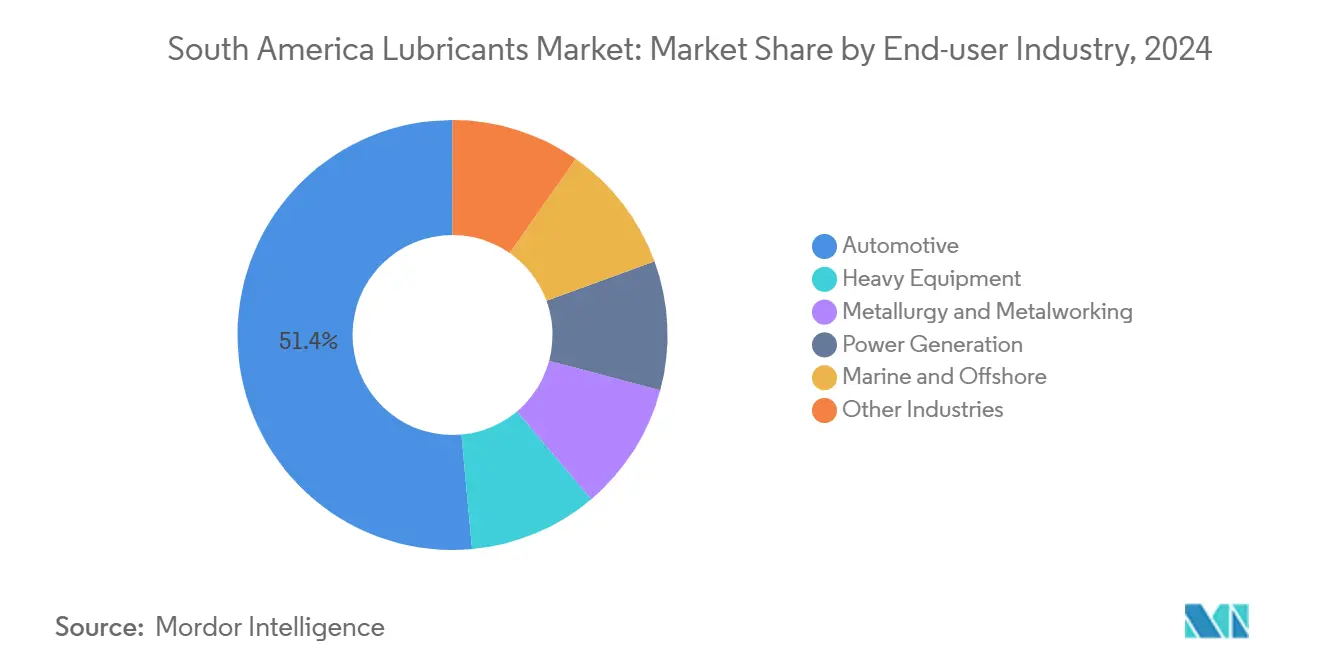

- By end-user, automotive led with a 51.45% share of the South America lubricants market in 2024, while power generation recorded the highest projected 3.01% CAGR to 2030.

- By geography, Brazil commanded 47.12% share in 2024, while Chile is projected to grow the fastest at a 2.95% CAGR through 2030.

South America Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong rebound in on-road freight mileage post-COVID | +0.4% | Brazil, Argentina, Chile core markets | Short term (≤ 2 years) |

| Accelerated deep-water energy and power activity in Brazil and Guyana boosting demand for high-performance drilling fluids | +0.6% | Brazil offshore, Guyana Stabroek Block | Medium term (2-4 years) |

| Mandatory Euro VI-equivalent emissions phase-in (Brazil PROCONVE P-8) driving low-SAPS engine-oil adoption | +0.3% | Brazil national, spillover to MERCOSUR | Medium term (2-4 years) |

| Surge in regional soybean-oil biodiesel blends spurring growth of bio-based hydraulic fluids | +0.5% | Argentina, Brazil agricultural regions | Long term (≥ 4 years) |

| Rapid automation of mining fleets in Chile and Peru requiring long-drain synthetic gear oils | +0.4% | Chile, Peru mining corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Rebound in On-Road Freight Mileage Post-COVID

Freight activity has surpassed pre-pandemic levels as near-shoring shifts and e-commerce intensify long-haul truck movements across Brazil, Argentina, and Chile. Brazil’s trucking sector alone handles more than 60% of domestic cargo and now demands premium engine and transmission oils that enable extended drain intervals and fuel economy gains. Harvest cycles for soy, corn, and copper further lift lubricant volumes during peak logistics seasons, locking in a short-term consumption surge that sustains baseline market growth[1]The World Bank Group, “The Brazil of the Future: Towards Productivity, Inclusion, and Sustainability,” documents1.worldbank.org .

Accelerated Deep-Water Energy and Power Activity in Brazil and Guyana Boosting Demand for High-Performance Drilling Fluids

Brazil’s pre-salt fields and Guyana’s Stabroek Block collectively require synthetic drilling muds, subsea gear oils, and hydraulic fluids capable of withstanding extreme temperatures and 2,000 m water depths. ExxonMobil’s multiplatform program and Petrobras subsea boosting contracts exemplify the specialized service models that command premium pricing and deepen supplier-client technical ties[2]Oil and Gas Innovation, “SLB Awarded Subsea Boosting Contract by Petrobras, Offshore Brazil,” oilandgasinnovation.co.uk.

Mandatory Euro VI-Equivalent Emissions Phase-In (Brazil PROCONVE P-8) Driving Low-SAPS Engine-Oil Adoption

Effective January 2025, PROCONVE L8 lowers NOx+NMOG thresholds for passenger cars and tightens heavy-duty standards, making low-SAPS lubricants essential to protect diesel particulate filters and SCR catalysts. OEM-approved formulations with reduced ash, phosphorus, and sulfur broaden market opportunities for synthetic and semi-synthetic products.

Surge in Regional Soybean-Oil Biodiesel Blends Spurring Growth of Bio-Based Hydraulic Fluids

Argentina’s biodiesel output of 775,366 tonnes in 2024 and Brazil’s ethanol-heavy energy matrix supply abundant fatty-acid feedstocks for advanced biolubricants. Enzymatic synthesis processes now deliver viscosity indices above 100 and oxidation stability competitive with mineral oils, positioning bio-based hydraulics for agriculture and forestry applications.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged fuel-price subsidies in Argentina discouraging premium-lube consumption | -0.3% | Argentina national, border regions | Short term (≤ 2 years) |

| Currency-devaluation risk inflating import costs of PAO and additive packages | -0.4% | Argentina, Brazil, regional importers | Medium term (2-4 years) |

| Rising penetration of EV two-wheelers in urban centers eroding motorcycle-oil volumes | -0.2% | Urban centers across Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Fuel-Price Subsidies in Argentina Discouraging Premium-Lube Consumption

Subsidized pump prices reduce consumer motivation to purchase high-efficiency synthetics, locking many motorists into short-interval mineral oils and capping value growth in passenger-car motor oils. The subsidy system has historically favored volume over value, encouraging frequent oil changes with conventional mineral oils rather than extended-service premium products. This dynamic particularly affects the passenger vehicle segment, where cost-conscious consumers prioritize immediate savings over long-term engine protection and fuel economy benefits.

Currency-Devaluation Risk Inflating Import Costs of PAO and Additive Packages

Most synthetic base oils and high-performance additives are priced in hard currencies; peso and real depreciation widen cost spreads for regional blenders, stressing margins and delaying portfolio upgrades. Brazil's lubricant manufacturers face similar challenges with imported feedstocks, though the country's larger domestic petrochemical base provides some insulation. Currency hedging strategies remain limited for smaller regional players, creating competitive disadvantages against integrated multinationals with global supply chains and natural currency hedges through diversified revenue streams.

Segment Analysis

By Product Type: Engine Oils Hold Sway While Hydraulics Accelerate

Engine oils retained 40.36% of the 2024 South America lubricants market share, but hydraulic fluids are poised for a 2.78% CAGR as automation spreads in mining, agriculture, and renewables. Specialized hydraulics formulated from synthetic or bio-based stocks ensure oxidative stability and temperature resilience demanded by high-pressure systems. Transmission and gear oils gain from fleet modernization programs, whereas greases protect bearings in harsh marine and industrial environments.

Emissions mandates push engine oil upgrades toward Group III and synthetic blends, yet price sensitivity keeps mineral products relevant in older vehicles. Hydraulic-fluid demand benefits from renewable-energy build-outs, where biodegradable formulations are preferred for environmental compliance. Continuous research and development in additive chemistry allows regional blenders to position differentiated offerings in the South America lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Base Oil: Mineral Prevalence with Bio-based Upswing

Mineral base oils accounted for 62.23% of volume in 2024, leveraging local refining capacity at Petrobras and YPF. Bio-based alternatives, however, are projected to register the quickest 3.12% CAGR, buoyed by soybean, palm, and castor feedstock availability and supportive sustainability policies. Synthetic imports, primarily PAO and esters, serve premium industrial and marine niches despite exposure to currency risk.

Regional refiners invest in hydrocracking and hydrotreating to lift output quality toward Group II and Group III, seeking to retain share as OEM specifications tighten. In parallel, enzyme-catalyzed processes upgrade vegetable-oil derivatives into high-VI base stocks that compete on both performance and carbon footprint, reshaping procurement priorities across the South America lubricants market.

By End-User: Automotive Scale Meets Power-Sector Momentum

Automotive applications generated the largest share at 51.45% in 2024, supported by an expanding vehicle parc and strong OEM production in Brazil and Argentina. Fleet operators increasingly shift to low-SAPS and extended-drain formulations that align with new emissions rules, sustaining premiumization in the South America lubricants market. Power generation, although smaller, is projected to grow the fastest at a 3.01% CAGR through 2030 as wind, solar, and gas-fired peaking plants proliferate. Specialized turbine oils, fire-resistant hydraulic fluids, and condition-monitoring services elevate value per liter in this segment.

The automotive customer base remains exposed to electrification; yet, medium-term ICE dominance coupled with growing freight demand anchors volume. Mining and construction fleets add resilience, with autonomous haul trucks and mechanized agriculture consuming high-performance hydraulic and gear oils. Suppliers that bundle product, analytics, and onsite service capture cross-segment synergies, reinforcing competitiveness across the South America lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil commanded a 47.12% share in 2024, anchored by its automotive hub, petrochemical network, and offshore exploration projects. PROCONVE L8 rules and deep-water investment jointly spur demand for advanced lubricants, making Brazil the technology bellwether for the region. Chile is set to outpace others with a 2.95% CAGR through 2030, driven by copper-mining automation that relies on long-drain synthetics and centralized condition monitoring.

Argentina’s fuel subsidies and currency swings restrain premium sales, but the Vaca Muerta shale play and vast agricultural machinery fleet support baseline volume. Peru and Colombia contribute via mining and oil production, respectively, while Guyana’s emerging offshore province opens a new high-margin marine-lubricant frontier. Regional trade blocs facilitate cross-border supply, yet political risk and FX volatility necessitate robust hedge strategies for participants in the South America lubricants market.

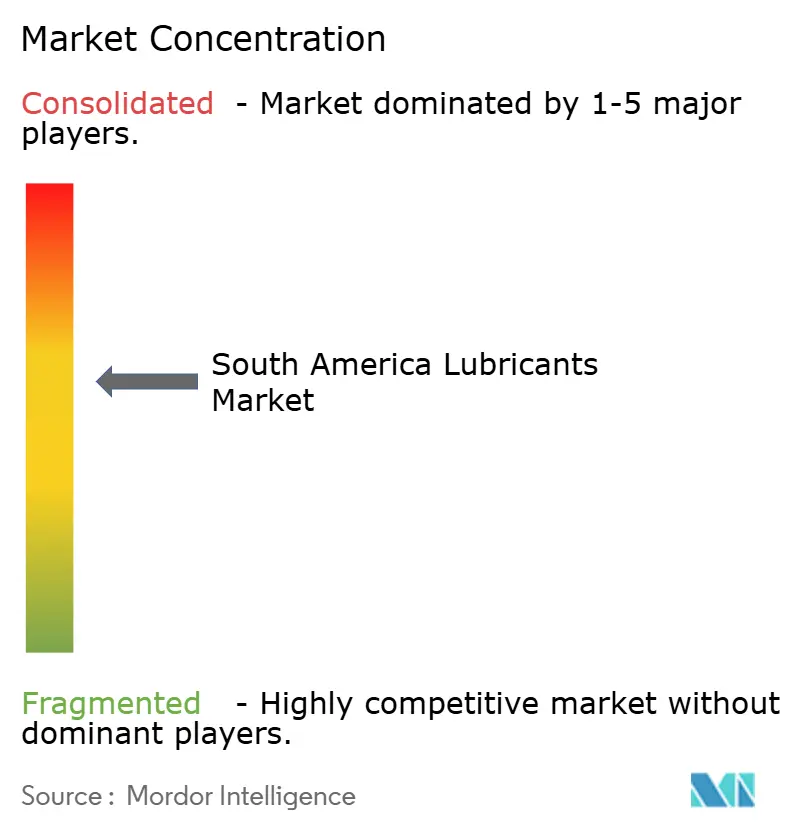

Competitive Landscape

The market features moderate fragmentation with marked country-level contrasts. Digitalization is a key differentiator: leading suppliers deploy IoT sensors for real-time oil-condition data, bundling analytics with product. Bio-based formulation research and development offers white-space entry points, while service contracts in offshore, power, and mining protect margins against commoditization. Mergers and acquisitions activity is likely to intensify as economies of scale in procurement and logistics become decisive within the South America lubricants market.

South America Lubricants Industry Leaders

-

BP plc (Castrol)

-

Exxon Mobil Corporation

-

ICONIC

-

Petrobras

-

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: FUCHS committed BRL 220 million (USD 39 million) to a new production site in Sorocaba, Brazil, targeting doubled local share.

- November 2024: Vibra Energy invested BRL 100 million (USD 17.2 million) to purchase and expand the Lubrax plant in Duque de Caxias, raising capacity by 53.3%.

South America Lubricants Market Report Scope

By Product Type

| Engine Oils |

| Transmission and Gear Oils |

| Hydraulic Fluids |

| Greases |

| Metalworking Fluids |

| Process Oils and Others |

By Base Oil

| Mineral |

| Synthetic (PAO, Esters, PAG) |

| Semi-synthetic |

| Bio-based |

By End-User Industry

| Automotive |

| Heavy Equipment |

| Metallurgy and Metalworking |

| Power Generation |

| Marine and Offshore |

| Other Industries |

By Country

| Argentina |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Engine Oils |

| Transmission and Gear Oils | |

| Hydraulic Fluids | |

| Greases | |

| Metalworking Fluids | |

| Process Oils and Others | |

| By Base Oil | Mineral |

| Synthetic (PAO, Esters, PAG) | |

| Semi-synthetic | |

| Bio-based | |

| By End-User Industry | Automotive |

| Heavy Equipment | |

| Metallurgy and Metalworking | |

| Power Generation | |

| Marine and Offshore | |

| Other Industries | |

| By Country | Argentina |

| Brazil | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the South America lubricants market in 2025?

The market totals 2.81 billion liters in 2025 and is projected to reach 3.17 billion liters by 2030.

Which end-user segment drives volume?

Automotive holds the lead with 51.45% share, backed by Brazil's sizable vehicle fleet.

What is the fastest-growing product category?

Hydraulic fluids are forecast to advance at a 2.78% CAGR through 2030 on rising automation demand.

Why are bio-based lubricants gaining traction?

Abundant soybean and castor feedstocks plus stricter environmental rules propel a 3.12% CAGR for bio-based base oils.

Which country offers the highest growth rate?

Chile is expected to record a 2.95% CAGR to 2030, driven by mining-sector modernization.

How will emissions regulations affect lubricant formulations?

Brazil's PROCONVE L8 and P-8 standards accelerate the shift to low-SAPS and synthetic oils to protect after treatment systems.

Page last updated on: