Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 2.68 Billion liters |

| Market Volume (2030) | 3.18 Billion liters |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

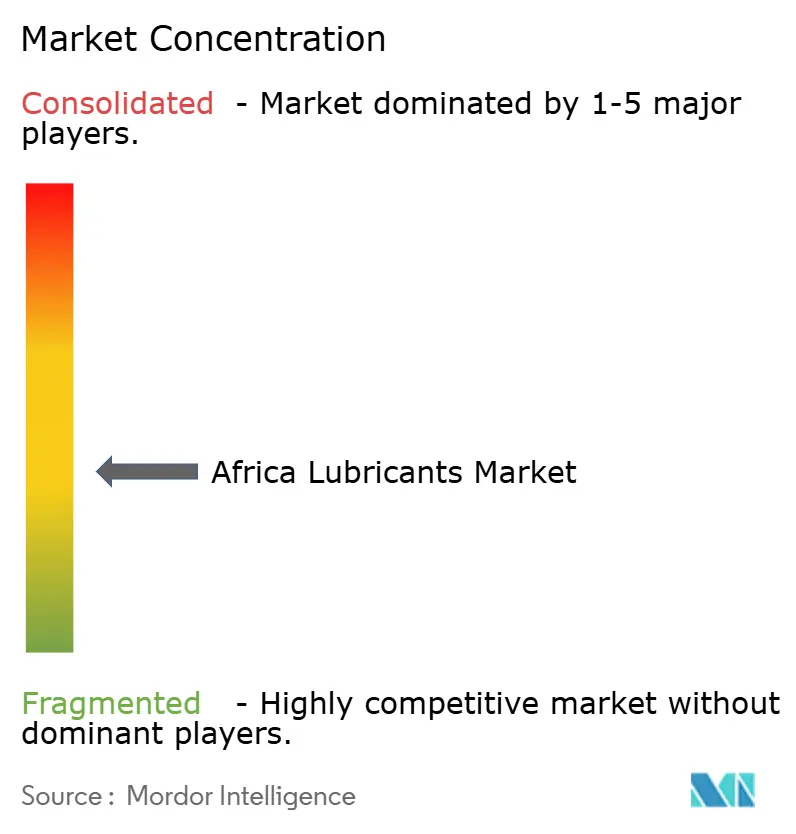

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Lubricants Market Analysis by Mordor Intelligence

The Africa Lubricants Market size is estimated at 2.68 billion liters in 2025, and is expected to reach 3.18 billion liters by 2030, at a CAGR of 3.52% during the forecast period (2025-2030). Robust infrastructure programs, accelerating mining output, and the rapid expansion of regional vehicle fleets underpin this volume growth. Public and private investments in road, rail, and energy assets continue to drive higher demand for construction machinery lubricants, while rising motorization rates in cities, from Cairo to Lagos, support sustained consumption of automotive engine oils. Local refinery upgrades, notably the base-oil streams emerging from new Nigerian capacity, strengthen regional supply resilience and temper import dependence. OEM mandates for extended drain intervals are nudging buyers toward synthetic grades, especially in markets now enforcing Euro 4 and Euro 5 emission norms, and this transition is most evident in Egypt, South Africa, and Morocco. Competitive intensity remains moderate; international majors leverage brand equity and technical know-how, yet regionally rooted suppliers gain ground by offering flexible pack sizes, price-competitive mineral formulations, and on-site equipment services.

Key Report Takeaways

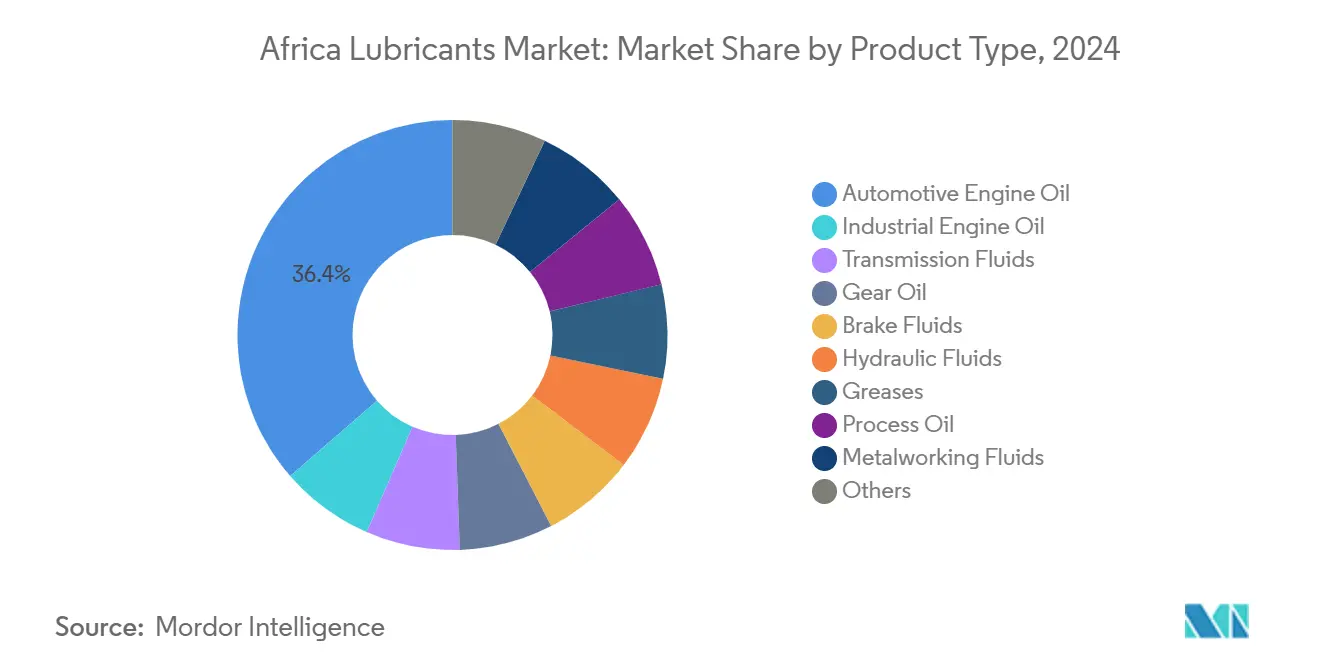

- By product type, automotive engine oil led with a 36.41% share of Africa's lubricants market in 2024, while process oils are expected to expand at a 4.42% CAGR through 2030.

- By end-user, the automotive segment held a 45.28% share of the African lubricants market size in 2024, whereas industrial applications are projected to advance at a 4.09% CAGR through 2030.

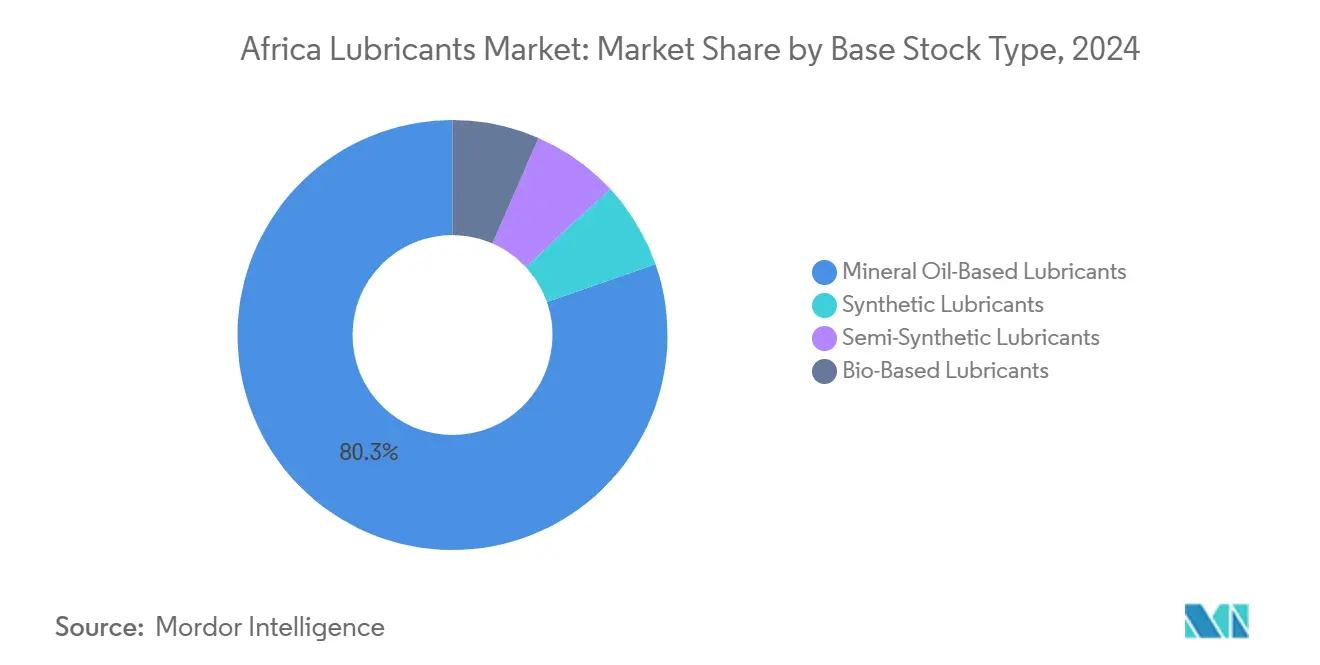

- By base stock, mineral oils accounted for 80.34% of the Africa lubricants market size in 2024, and synthetic lubricants are forecast to progress at a 4.14% CAGR over the outlook period.

- By geography, Egypt commanded 23.21% of Africa's lubricants market share in 2024, and Morocco is poised for the fastest growth at a 4.03% CAGR through 2030.

Africa Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid motorization driving automotive demand | +1.2% | Egypt, Nigeria, South Africa, Morocco | Medium term (2-4 years) |

| Infrastructure-led mining and construction | +0.8% | South Africa, Nigeria, Algeria, Rest of Africa | Long term (≥ 4 years) |

| Local refinery upgrades boosting base oils | +0.6% | Nigeria, Egypt, Algeria | Medium term (2-4 years) |

| OEM drain-interval extensions favoring synthetics | +0.4% | South Africa, Egypt | Long term (≥ 4 years) |

| Fast-growing e-commerce fleet demand | +0.3% | Nigeria, Egypt, South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Motorization Driving Automotive Lubricant Demand

Vehicle ownership is rising faster than population growth in major urban centers, creating a steady pull for engine oils, transmission fluids, and brake fluids. Commercial truck fleets in Lagos and Johannesburg experience arduous duty cycles, which shorten oil change intervals and increase consumption. National assembly plants across North Africa now require factory-fill volumes and consistent aftermarket supply, with local content regulations encouraging in-country blending. Motorists are gradually shifting from monograde to multigrade formulations as modern engines become more prevalent, and the preference for smaller pack sizes aligns with the purchasing power of individual car owners. OEM service networks champion licensed products that meet Euro 5 emission requirements, thereby accelerating the uptake of mid-SAPs synthetic blends.

Infrastructure-Led Mining and Construction Boom

Copper, phosphate, and critical mineral projects are expanding in South Africa, Zambia, and Morocco, each utilizing heavy mechanical loaders and conveyors that require premium hydraulic fluids and EP gear oils capable of withstanding dust and high loads. Concurrent road, port, and rail upgrades across Egypt and Nigeria sustain demand for greases and turbine oils used in large earth-moving equipment and power generation sets. Suppliers able to deliver bulk volumes to remote sites win contracts, while those offering oil analysis and condition monitoring services secure long-term relationships that lock in product offtake. The predictable operating schedules of construction consortia create baseline orders that stabilize blender capacity utilization even during seasonal dips in passenger car consumption.

Local Refinery Upgrades Boosting Base-Oil Availability

The start-up of advanced refining units in Nigeria, as well as revamps in Egypt and Algeria, adds Group I and Group II base-oil streams to the regional supply. Local blenders benefit from reduced freight costs and shorter lead times, which enable more competitive pricing and a faster response to tenders. Consistent quality improves batch blending efficiency, lowering rework and waste. Refinery supply agreements also mitigate currency-related cost spikes linked to imported feedstocks. Over time, the expanded slate of higher viscosity-index base oils supports a broader synthetic blend portfolio, widening the product mix available to high-performance industrial equipment operators.

OEM Drain-Interval Extensions Favoring Synthetics

Truck manufacturers now recommend drain intervals of 40,000-60,000 km when suitable low-ash synthetic oils are used, encouraging fleet owners to weigh the total cost of ownership against the upfront price. Field trials in South Africa have demonstrated improvements in fuel economy when synthetic 5W-30 oil is used in place of conventional 15W-40 oil in long-haul tractors[1]American Petroleum Institute, “Engine Oil Licensing and Certification System, 22nd Edition,” api.org. The longer service life lowers lubricant disposal volumes, aligning with corporate sustainability policies. Industrial equipment OEMs echo the trend; modern compressors specified for LNG trains in Algeria require PAG-based oils that can withstand elevated discharge temperatures. The extension of oil change intervals frees maintenance crews for other tasks, improving overall asset productivity.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent fuel-subsidy volatility | -0.7% | Nigeria, Egypt, Algeria | Short term (≤ 2 years) |

| Dominance of low-grade Group I imports | -0.4% | Nigeria, Rest of Africa | Medium term (2-4 years) |

| Informal counterfeit-oil networks | -0.3% | Nigeria, Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Fuel-Subsidy Volatility Distorting Prices

Abrupt subsidy removals or reinstatements shift pump prices and indirectly influence lubricant demand, as transporters recalibrate mileage and maintenance budgets. Sudden cost spikes prompt operators to stretch drain intervals or down-trade to cheaper monograde oils, eroding premium segment volumes. Importers struggle to forecast landed costs when exchange rates and subsidy levels change in tandem, complicating inventory decisions. Policy uncertainty discourages heavy capital investment in blending plants and storage, prolonging reliance on toll blending and third-party logistics.

Dominance of Low-Grade Group I Imports

Price-sensitive buyers in many African markets view lubricants as commodities, opting for base-level monogrades sold from bulk drums rather than higher-specification packs. Traders import oversupplied Group I base oils from the Middle East and Asia, blending them locally into low SAPS formulations that meet only minimal API standards. The resulting price differential, often lower than that of synthetic blends, constrains the supplier's ability to upsell. This dynamic also keeps average selling prices subdued, dampening overall market value growth relative to volume gains.

Segment Analysis

By Product Type: Engine Oils Remain the Anchor of Demand

Automotive engine oil held 36.41% of Africa's lubricants market share in 2024, supported by a continent-wide vehicle fleet that continues to age under challenging operating conditions. Commercial trucks account for a sizable portion of sump volumes, and frequent oil changes increase the total liters consumed each year. Process oils, serving rubber, textile, and petrochemical plants, are forecast to grow at a 4.42% CAGR, the fastest among all product lines, thanks to industrial diversification programs in Egypt and Nigeria. Gear oils cater to underground mining machines that operate under extreme shock loads, while transmission fluids gain prominence as automatic gearboxes become more prevalent in commercial fleets. Hydraulic fluids experience steady demand from backhoes and cranes operating on large construction sites throughout West and North Africa. Metalworking fluids track the evolution of domestic component manufacturing, particularly the brake pad and filter plants that have recently been established in Morocco.

Demand for greases is rising in surface mining and marine thrusters, with lithium-complex products preferred for their water resistance. Brake fluids show linear growth in line with new vehicle assemblies, though the shift toward electric cars may curb long-term expansion. Turbine oils secure slots in combined-cycle gas plants commissioned under national electrification agendas, and transformer oils benefit from grid reinforcement projects feeding rapidly urbanizing regions. Collectively, the diversified product slate anchors the resilience of the Africa lubricants market, balancing cyclical softness in any single end-use with momentum in others.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Automotive Leads, Industry Builds Momentum

The automotive domain captured 45.28% of the 2024 volume, reflecting the prevalence of passenger cars, buses, and two-wheelers across the continent. Light-duty passenger vehicles dominate in North Africa, while heavy trucks rule corridors connecting inland mines to port gateways in Southern Africa. Industrial users, encompassing manufacturing, energy, and mining, will expand at a 4.09% CAGR through 2030 as governments push downstream processing and localized value creation. Power plants commission new gas and renewable energy capacity, increasing the consumption of turbine and compressor oils. Mining houses adopt centralized lubrication systems that meter greases precisely, reducing wastage while ensuring consistent replenishment contracts.

Marine lubricants gain traction as container traffic through the Suez Canal and West African deep-water terminals rises. Aerospace fluids, though niche, benefit from aircraft fleet renewals among regional carriers. Agricultural mechanization relies on off-highway engine oils and hydraulic fluids, particularly in Ethiopia and Kenya. Across user segments, digital oil analysis services become a competitive differentiator, providing predictive data that underpins supply contracts and cements brand loyalty.

By Base Stock Type: Mineral Dominance Continues, Synthetic Uptake Accelerates

Mineral formulations accounted for 80.34% of the 2024 volume, underscoring entrenched buyer price sensitivity and existing blending infrastructure that is calibrated for Group I feedstock. At the same time, synthetics are expected to register a 4.14% CAGR through 2030 as OEMs mandate higher viscosity indices and improved oxidation stability. Semi-synthetic blends serve as a compromise, offering performance gains for a modest premium, particularly appealing to commercial fleets that prioritize uptime. Bio-based lubricants remain a niche market; however, research on local feedstocks, such as castor and jatropha, demonstrates promising tribological properties when modified with nano-additives[2]Nagarajan T. et al., “Enhanced Tribological Properties of Diesel-Based Engine Oil Through Synergistic MoS₂-Graphene Nanohybrid Additive,” nature.com .

The cost gap between mineral and synthetic oils narrows whenever import freight surges or exchange rates weaken local currencies, which happens frequently in Africa’s floating-rate economies. This dynamic occasionally triggers temporary swings toward higher specification products. National standards bodies are increasingly harmonizing with API and ACEA frameworks, paving the way for a broader shift to synthetics. Over the forecast period, OEM factory fills and long-haul truck segmentation will be the two principal accelerators of synthetic substitution.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Egypt, with 23.21% of the 2024 volume, benefits from a diversified economic base that spans automotive assembly, petrochemical processing, and maritime trade. Lubricant sales are split between passenger car oils and industrial oils servicing fertilizer, steel, and textile plants. Morocco’s lubricants growth is expected to average a 4.03% CAGR, supported by robust auto exports, phosphate extraction, and targeted e-mobility incentives. South Africa’s mature aftermarket values premium formulations that ensure warranty compliance on high-end vehicle brands, while its mining sector continues to absorb heavy-duty gear oils.

Nigeria’s sheer population drives scale, but supply chain bottlenecks and currency swings add volatility to demand cycles. Algeria leverages substantial hydrocarbon revenue to fund refinery upgrades, which improve its base-oil self-sufficiency. The rest of Africa presents a patchwork of opportunities; East African Community states focus on agriculture and small-engine oils, whereas Central African mining enclaves prioritize bulk mineral hydraulic fluids. Regional trade agreements accelerate cross-border flows, yet local standards sometimes limit product interchangeability, compelling suppliers to maintain country-specific variants.

Competitive Landscape

The African Lubricants Market is moderately fragmented. The market is contested by a mix of global majors, including TotalEnergies, Shell, ExxonMobil, and Chevron, alongside regionally entrenched producers such as FUCHS, Engen, and Afriquia. Regional independents sharpen competitiveness through plant automation, smaller batch flexibility, and tailored pack sizes. Chevron introduced NEXBASE 4 XP Group III+ base oil into European tank farms with onward shipping into Morocco and South Africa, enabling local blenders to formulate low-viscosity OW-20 and OW-16 grades for late-model cars. FUCHS’ South-African hub now offers digitally controlled blending lines and rooftop solar arrays targeting net-zero site emissions by 2040.

Africa Lubricants Industry Leaders

-

Shell plc

-

TotalEnergies

-

Exxon Mobil Corporation

-

BP plc

-

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Engen Petroleum (PTY) LTD relaunched its Xtreme 2.0 lubricant range in South Africa, featuring anti-counterfeit QR seals and packs containing post-consumer recycled plastics.

- February 2025: FUCHS opened an expanded South-African plant after a ZAR 218 million investment, doubling automated blending capacity and adding photovoltaic power generation.

Africa Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By Geography

| Nigeria |

| South Africa |

| Egypt |

| Algeria |

| Morocco |

| Rest of Africa |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Geography | Nigeria | |

| South Africa | ||

| Egypt | ||

| Algeria | ||

| Morocco | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Africa lubricants market in 2025?

The Africa lubricants market size stood at 2.68 billion liters in 2025 and is projected to reach 3.18 billion liters by 2030 at a 3.52% CAGR.

Which product segment dominates lubricant demand in Africa?

Automotive engine oil leads with 36.41% of 2024 volume, reflecting widespread vehicle ownership and frequent oil changes.

Which country consumes the most lubricants in Africa?

Egypt currently holds the largest single-country share at 23.21% of 2024 volume.

What is driving synthetic lubricant adoption in Africa?

OEM-mandated longer drain intervals and stricter emission standards are prompting fleet owners to opt for synthetic and semi-synthetic grades.

How will local refinery projects affect lubricant supply?

New Nigerian and upgraded North African refineries are adding Group II base-oil capacity, reducing import dependence and supporting competitive pricing.

Page last updated on: