Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.8 Billion |

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Compound Feed Market Analysis by Mordor Intelligence

The Vietnam compound feed market size was valued at USD 1.80 billion in 2025 and estimated to grow from USD 1.86 billion in 2026 to reach USD 2.23 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031). Volume expansion is steady rather than spectacular because integrated farming groups now favor precise rations over blanket tonnage gains. Ingredient cost swings, stricter biosecurity norms, and a consumer pivot toward documented food safety continue to reshape formulation choices inside the Vietnam compound feed market. Domestic soybean-crushing capacity cushions mills from currency volatility, while insect protein pilots illustrate a near-term route toward circular sourcing that appeals to export buyers. Simultaneously, regulations that limit antimicrobial growth promoters lift demand for organic acids, essential oils, and probiotics, raising formulation costs yet opening a premium niche in the Vietnam compound feed market.

Key Report Takeaways

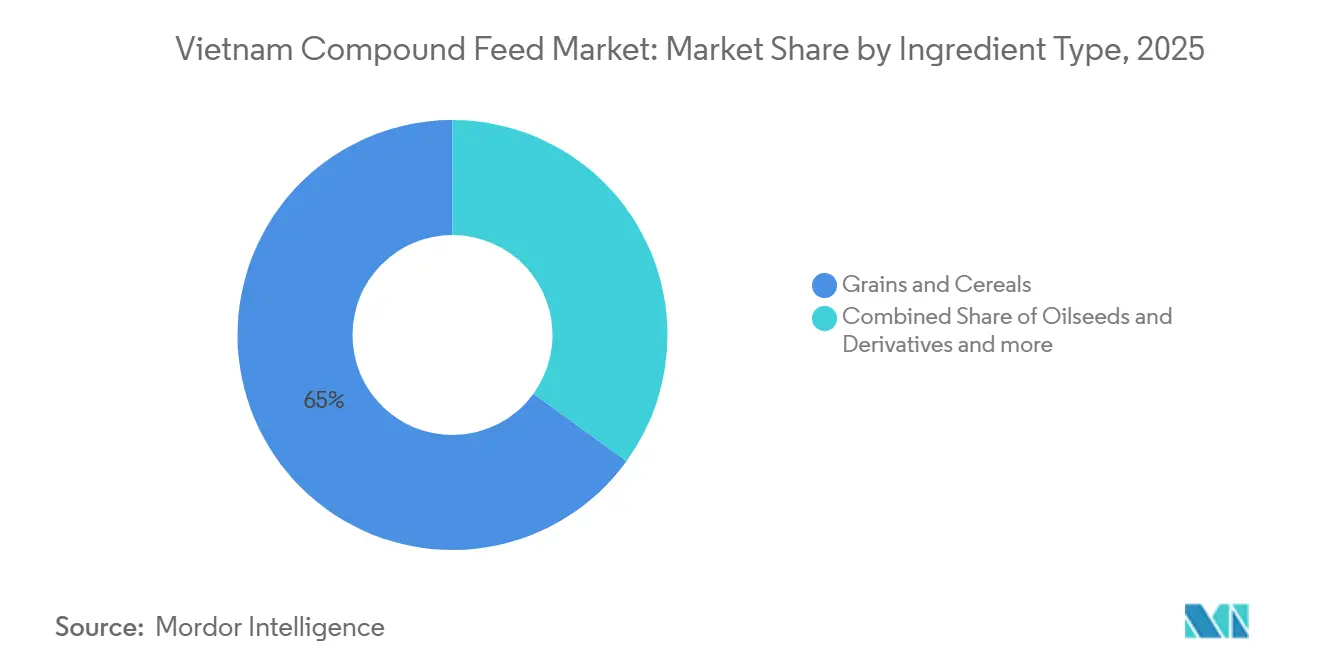

- By ingredient type, grains and cereals accounted for 65% of the Vietnam compound feed market size in 2025, while novel insect proteins are projected to expand at a 13.2% CAGR to 2031.

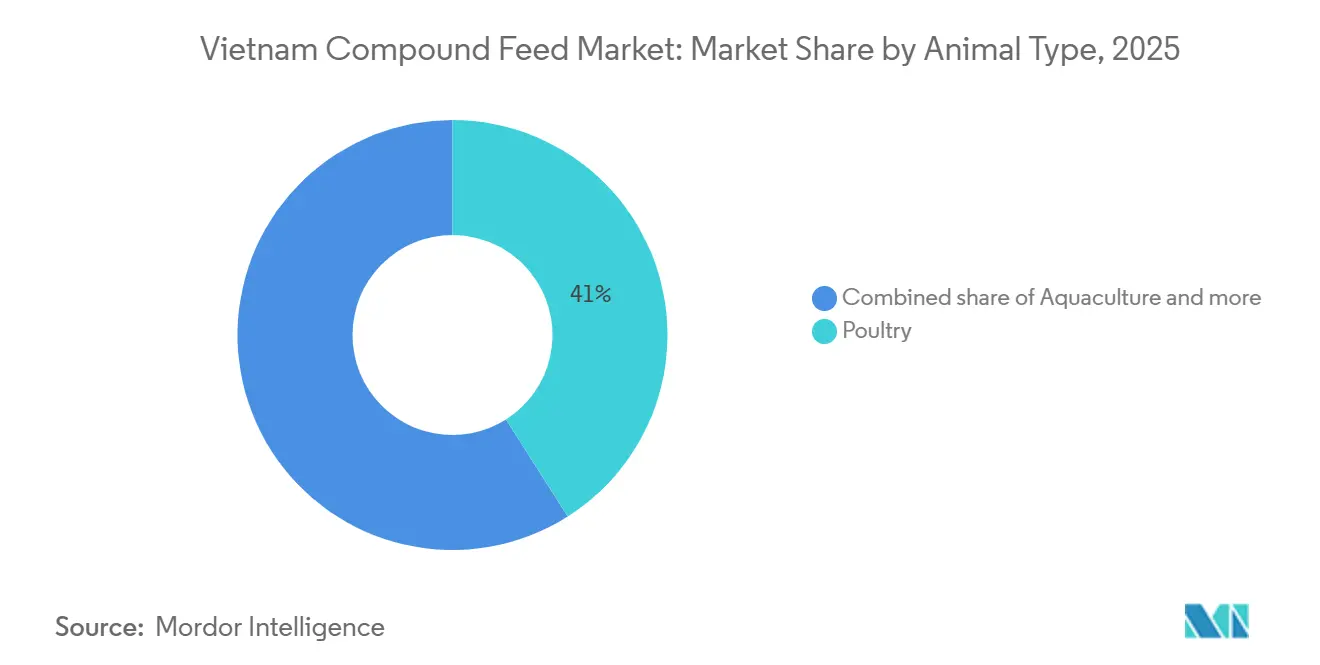

- By animal type, poultry held 41% of the Vietnam compound feed market share in 2025, while aquaculture feed is advancing at an 8.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Compound Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising meat and seafood consumption | +2.1% | National, stronger in urban centers | Medium term (2-4 years) |

| Emphasis on animal health and functional nutrition | +1.8% | National, commercial farming regions | Long term (≥ 4 years) |

| Expansion of integrated mega-farms and contract farming models | +1.5% | Mekong Delta, Red River Delta, and Central Coast | Medium term (2-4 years) |

| Growth of Vietnam aquaculture export corridor | +1.4% | Mekong Delta, and Central Coast | Short term (≤ 2 years) |

| Adoption of insect meal and other novel proteins | +0.9% | National, early aquaculture uptake | Long term (≥ 4 years) |

| Digital feed-formulation platforms improving farm ROI | +0.6% | National, tech-forward operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Meat and Seafood Consumption

Vietnam's per capita meat consumption reached 39 kilograms in 2025 after strong wage gains and urban migration drove consumers toward animal protein[1]Source: USDA Foreign Agricultural Service, “Vietnam: Livestock and Products Annual 2025,” USDA.gov. Poultry leads the volume increase because chilled broiler cuts now populate modern retail chains that require consistent sizing and traceability. Pork demand is rebounding as farms rebuild post-African swine fever with higher-health genetics and precision starter feeds that contain immunoglobulins and organic acids. Seafood consumption is also expanding, supported by affordable farmed shrimp and pangasius that fit household budgets and nutritional goals. Together, these trends underpin a dependable baseline for the Vietnam animal feed market, insulating mills from cyclical swings in any single species segment.

Emphasis on Animal Health and Functional Nutrition

Integrated enterprises now benchmark ratios on immune modulation and gut integrity, pushing mills toward organic acids, essential oils, and direct-fed microbials. In 2023, on-farm trials led by Cargill technicians showed a 4% improvement in feed conversion ratio when yeast-derived beta-glucans replaced synthetic growth promoters. Documented performance gains justify premium formulas and foster long-term supply contracts inside the Vietnam compound feed market. As digital scales and sensor data become mainstream, proof of efficacy will move functional nutrition from niche to baseline practice.

Expansion of Integrated Mega-Farms and Contract Farming Models

Charoen Pokphand, Masan, and Japfa increasingly manage the full chain from genetics to processing, securing captive consumption for in-house mills. Contract growers receive chicks or piglets plus proprietary feed at fixed prices, reducing working-capital strain and guaranteeing offtake. Predictable throughput boosts mill utilization and lowers per-unit overhead, consolidating power among the largest players in the Vietnam compound feed market. Independent mills respond by targeting specialty segments such as organic or antibiotic-free rations where flexibility beats scale.

Growth of Vietnam Aquaculture Export Corridor

Vietnam exported USD 11.3 billion worth of seafood in 2025, a 12.4% increase from 2024, as per the Vietnam Association of Seafood Exporters and Producers (VASEP), and premium buyers in the European Union, the United States, and Japan required Aquaculture Stewardship Council and Best Aquaculture Practices certifications. Certified farms rely on high-digestibility pellets featuring soy protein concentrate and insect meal to reduce fishmeal load. The export premium feeds straight into higher average selling prices, deepening profit pools in the Vietnam compound feed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of corn, soybean, and fishmeal | -1.9% | National, import-dependent mills | Short term (≤ 2 years) |

| Tighter limits on antimicrobial growth promoters | -1.2% | National, intensive zones | Medium term (2-4 years) |

| Recurring livestock epidemics | -0.8% | National, cyclical outbreaks | Short term (≤ 2 years) |

| Stricter environmental and wastewater compliance for mills | -0.7% | National, small mills | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Corn, Soybean, and Fishmeal

Ingredients account for 70% of finished-feed costs, so spot spikes quickly compress gross margins. Drought in grain-origin countries raised corn prices in early 2024, while fishmeal jumped 20-25% in 2025 after El Niño curtailed Peruvian anchovy harvests. With limited access to futures hedging, many Vietnamese mills pass costs to farmers after a lag, but smallholders often resist higher prices, weakening demand. Persistent volatility thus dampens growth momentum in the Vietnam compound feed market.

Tighter Limits on Antimicrobial Growth Promoters

Regulations enacted in 2024 capped copper sulfate and banned high-dose zinc oxide in piglet feeds, aligning with European standards. Reformulating a finisher diet adds roughly 3-5% to material cost because mills must substitute probiotics, organic acids, or essential oils. Large multinationals absorb the burden through global purchasing power, but stand-alone mills face working-capital strain. Compliance pressure, therefore, accelerates consolidation within the Vietnam compound feed market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Grains Anchor Formulations While Novel Proteins Capture Innovation Spend

Grains and cereals maintained 65% of the Vietnam compound feed market share in 2025, reflecting Vietnam's traditional reliance on corn and rice-based feed formulations, while the segment maintains steady growth aligned with overall market expansion. Wheat and sorghum served as alternatives when corn prices increased, although their lower energy density required adjustments in rations. Soybean meal contributed significantly to the inclusion tonnage, with the establishment of new local crushers reducing logistical costs. Supplements, including enzymes and organic acids, represented a small portion of the volume but contributed notably to the value, highlighting the ongoing functional shift in the Vietnam compound feed market. The regulatory environment increasingly favors sustainable and traceable ingredients, positioning domestic alternative protein producers for accelerated market penetration as environmental compliance requirements tighten across the value chain.

Novel ingredients, such as insect meal and fermented protein, are growing rapidly at a fastest CAGR of 13.2% from 2026-2031, as aquaculture exporters replace fishmeal in diets to meet sustainability requirements. The share of fishmeal in aquafeed has declined, replaced by soy protein concentrate and poultry by-product meal. Additives like phytase and xylanase help reduce phosphorus excretion, aligning with wastewater regulations[2]Source: Ministry of Natural Resources and Environment, “Regulation on Livestock Wastewater Management,” Monre.gov.vn. This diversification of ingredients mitigates risks and supports the development of value-added products within the Vietnam compound feed market.

By Animal Type: Poultry Leads Volume While Aquaculture Commands Premium Pricing

Poultry feeds led the Vietnam compound feed market size in 2025 at 41% share, supported by Vietnam's position as Southeast Asia's second-largest poultry producer and consistent domestic consumption growth. Technical innovation in aquafeed formulations, particularly for shrimp and pangasius, creates opportunities for premium pricing and margin expansion as farmers prioritize feed conversion efficiency and disease resistance over cost minimization.

Aquaculture feeds are projected to grow at the fastest-growing 8.4% CAGR from 2026-2031, the fastest among all animal types, on the back of export-linked shrimp and pangasius farms. Specialty additives such as krill hydrolysate and yeast beta-glucans raise cost but improve early survival syndrome resistance, supporting feed conversion ratios below 1.5 for pangasius. With stricter certifications, aquaculture is anticipated to remain a key area of innovation within the structure of Vietnam's compound feed market share.

Geography Analysis

Southern Vietnam accounted for a significant share of compound feed usage, driven by the concentration of poultry integrators and pangasius farming in areas such as Dong Nai, Long An, and the Mekong Delta. The presence of deep-water ports and cold-chain infrastructure facilitates the seamless export of chilled meats and frozen fillets. Additionally, expressway expansions have reduced door-to-door delivery times, enabling feed mills to maintain lean inventories and reduce working capital requirements. These factors position Southern Vietnam as a key region in the Vietnam compound feed market.

Northern provinces, including Hai Duong and Hung Yen, recovered more quickly from the African swine fever outbreak due to government-led vaccine programs. The cooler winters in this region allow for higher energy densities in feed rations, reducing the relative inclusion cost per kilogram of weight gain. Proximity to urban areas has increased scrutiny on environmental factors such as odor and dust, prompting mills to install odor scrubbers and enclosed load-out chutes. While these measures raise fixed costs, they also improve pellet quality and consistency. Consequently, the northern region focuses on quality-sensitive niches within the Vietnam compound feed market.

The Central Highlands provinces of Gia Lai and Dak Lak are emerging as hubs for dairy and beef feed production. This growth is supported by the availability of coffee pulp and husk by-products, which serve as cost-effective fiber sources. Smaller mills in the region leverage local co-products to create economical feed rations, which are transported to Ho Chi Minh City processors. Infrastructure improvements made bulk deliveries more feasible, fostering the development of a small but rapidly growing regional node. This diversification reduces geographic concentration risks within the Vietnam compound feed market.

Regulatory Landscape

Vietnam's compound feed sector is regulated primarily by the Ministry of Agriculture and Rural Development (MARD) under the Law on Animal Husbandry (Law No. 32/2018/QH14), which has governed feed production, trade, imports, and quality inspection since it took effect in 2020. Under MARD administration, complete compound feed and concentrated feed for commercial circulation must be self-declared via the ministry's electronic portal before entering the market, with dossiers documenting conformity to applicable national standards (TCVN) and technical regulations (QCVN).

Feed safety and contaminant control are central enforcement themes, including limits and testing expectations related to mycotoxins, heavy metals, and microbiological criteria under national technical regulations such as QCVN 01-183:2016/BNNPTNT and subsequent consolidated updates. MARD circulars periodically update lists of prohibited substances and restricted inputs, while imported feeds or feed ingredients not previously approved in Vietnam may require dossier appraisal and/or testing for authorization, which increases compliance burden for smaller mills and import-reliant formulations.

Competitive Landscape

The Vietnam compound feed market is moderately concentrated, with a few key players such as Charoen Pokphand Group Co., Ltd, Cargill, Incorporated, De Heus Animal Nutrition B.V., GreenFeed Group JSC, and Tongwei Co., Ltd. collectively controlling the majority of revenue in 2025. Charoen Pokphand Group Co., Ltd operates mills equipped with technology to ensure precise nutrient specifications. Cargill Incorporated focuses on field support, deploying veterinarians and nutritionists to foster customer loyalty through measurable performance improvements[3]Source: Cargill Incorporated, “Animal Nutrition Solutions,” Cargill.com. De Heus Animal Nutrition B.V. is expanding its market share through acquisitions, increasing capacity, and leveraging an established dealer network.

GreenFeed Group JSC operates mills strategically located across all regions, enabling timely delivery to maintain pellet freshness in tropical conditions. The company also offers a fintech credit program that provides competitively priced working capital to contract growers, utilizing digital solutions to enhance customer loyalty. Nutreco’s Trouw Nutrition is testing predictive ration software that adjusts amino-acid profiles daily based on farm sensor data, reducing feed costs without compromising weight gain.

Vietnam’s feed regulations now require regular laboratory testing for mycotoxins, heavy metals, and banned antibiotics, as well as digital registration of feed formulations. Large mills benefit from economies of scale to manage testing costs, while smaller mills either pass these costs on to customers or exit the market. Additionally, environmental, social, and governance pressures from foreign retailers favor suppliers capable of certifying low-carbon inputs and providing blockchain-based traceability. As a result, data management and compliance capabilities are becoming as critical as physical production capacity in shaping leadership within the Vietnam compound feed market.

Vietnam Compound Feed Industry Leaders

Charoen Pokphand Group Co., Ltd

Cargill Incorporated

GreenFeed Group JSC

CJ CheilJedang Corp

De Heus Animal Nutrition B.V.,

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large, modern capacity additions and automation upgrades are creating room for premium compound feed and higher-value nutrition solutions (premixes, functional additives, and biosecure programs). In 2026, GREENFEED initiated an expansion and upgrade of its Binh Dinh factory to a designed capacity of 700,000 tons per year, while Haid Group brought online a 200,000-tonne-per-year feed facility in Phu Tho Province and Japfa Comfeed Vietnam inaugurated a new feed mill in Binh Phuoc with an initial capacity of 240,000 tonnes per year. These projects increase addressable volume for poultry, swine, and aquaculture rations, while also raising competitive pressure on smaller mills that have limited capital for environmental controls, laboratory testing, and digital monitoring.

The direction on regulatory compliance and export readiness also supports demand for formulations that reduce reliance on antimicrobial growth promoters and improve traceability for integrated supply chains. MARD's updated 2026 self-declaration guidance via the ministry portal reinforces product registration and labeling discipline, which aligns with integrator procurement and third-party certification needs in export-linked aquaculture. Cost-management initiatives are further shaping formulation strategies, including Decree 73/2025/ND-CP tax exemptions and reductions for corn and soybean meal imports, alongside greater use of local by-products and novel proteins in response to fishmeal price volatility and sustainability requirements in seafood export corridors.

Recent Industry Developments

- June 2026: Charoen Pokphand (C.P.) Vietnam partnered with FPT Corporation to launch six AI transformation initiatives across its integrated Feed-Farm-Food value chain, including digital feed-mixing prescription management and image-based raw material quality inspection. The program tightens quality control and standardizes formulations at scale, raising the benchmark for data-driven manufacturing and traceability in Vietnam's compound feed ecosystem.

- October 2025: De Heus Animal Nutrition B.V. acquired 100% of CJ Feed & Care's operations across Vietnam and several Asian markets, encompassing 17 feed mills. The deal strengthens De Heus' regional footprint and procurement leverage, increasing competitive intensity for domestic producers while accelerating consolidation around players that can fund compliance and advanced nutrition capabilities.

- November 2024: Aboitiz Foods invested USD 45 million in a new feed manufacturing facility in Long An province with 300,000 metric tons annual capacity, targeting swine recovery and poultry growth. The plant's environmental controls and digital monitoring systems support alignment with tighter industrial compliance expectations, reinforcing the shift toward larger, more automated mills in Vietnam.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of compound feed sold in Vietnam, meaning factory-formulated feed rations made by mixing multiple ingredients into a ready-to-use feed for farm animals.

Scope exclusions: We exclude raw feed ingredients traded as commodities and on-farm feed mixes that are not sold as compound feed.

Segmentation Overview

- By Ingredient Type

- Grains and Cereals

- Oilseeds and Derivatives

- Fish Meal and Fish Oil

- Supplements

- Other Ingredient Types

- By Animal Type

- Ruminants

- Swine

- Poultry

- Aquaculture

- Other Animal Types

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context for Vietnam feed by animal population, production output, and trade dependence for key inputs. We leaned on public sources such as the General Statistics Office of Vietnam, the Ministry of Agriculture and Rural Development, FAOSTAT, USDA FAS country reports, and UN Comtrade to cross-check livestock and aquaculture activity with feed ingredient flows.

In parallel, company annual reports, investor presentations, and association websites were reviewed to understand capacity additions, product mix shifts, and pricing direction. Where available, we also used paid subscriptions focused on company financials and news intelligence, and an import and export shipment-level database to sanity check ingredient import momentum. The sources listed here are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating feed demand drivers, pricing behavior, and mix changes by animal type, especially where public data is reported with time lags. We spoke with stakeholders across feed manufacturing, ingredient distribution, and downstream livestock and aquaculture farming, and then used their inputs to confirm conversion ratios, realistic utilization levels, and near-term risk factors across Vietnam.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 39% | |

| Smaller Players: 20% | Managers: 47% |

Market-Sizing & Forecasting

Sizing started with a top-down demand pool build-up, where livestock and aquaculture production signals in Vietnam were translated into feed needs using species-level feed intensity and commercial feed penetration assumptions. Those totals were then adjusted through checks on ingredient availability and price movement, because compound feed economics in Vietnam are closely tied to grains and oilseed meal imports.

To keep the model practical, a few inputs were treated as key levers, including animal population and output trends, commercial feed share versus on-farm mixing, average feed conversion indicators by species, capacity utilization direction at feed mills, and average selling price movement by feed type. The final totals were corroborated with selective bottom-up approximations, such as sampled price per ton times estimated sales volumes for a set of producers, plus channel checks on distributor throughput. Where there were gaps, we used conservative ranges first, then narrowed them after follow-up calls.

For forecasting, scenario analysis was used so near-term shocks, such as disease cycles, input price swings, or export demand changes for seafood, could be reflected without forcing a single straight-line outcome. Expert feedback was used to set the expected path for penetration, feed efficiency, and pricing, and then the demand-led projections were converted into market value in USD.

Data Validation & Update Cycle

Validation was done by triangulating the modeled value against independent signals, including Vietnam livestock and aquaculture output direction, ingredient trade patterns, and observed price ranges for key feed categories. When a number moved outside expected bands, the inputs were rechecked, assumptions were stress-tested, and a second analyst review was completed before sign-off.

The report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major policy shifts, large capacity additions, or sudden changes in input costs. Before delivery, we do a final pass to confirm the latest data points and remove any inconsistencies created by newer disclosures or revised public statistics.

Mordor Intelligence's Vietnam Compound Feed Market Size Versus Other Published Estimates

Published numbers for Vietnam compound feed do not always match because each publisher makes different choices on what qualifies as compound feed, which years and currency timing are used, and how price per ton is built into the value model.

The main gap comes from whether premixes, concentrates, and broader nutrition products are rolled into the same total. In the approach used here, Mordor Intelligence counts only formulated compound feed sold as a ready ration and keeps raw ingredient value outside the market number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.80 B (2025) | |

| Industry Publisher A | USD 2.45 B (2025) | Uses a wider definition that can lift the value base through different inclusion choices across product types and through a higher implied average selling price progression. |

| Market Publisher B | USD 8.71 B (2024) | Appears to capture a broader upstream or adjacent spend pool beyond compound feed, which inflates totals when manufacturing and distribution layers are valued differently and when year and currency timing are not aligned. |

The spread in the table is mainly explained by scope choices and how value per ton is constructed from price assumptions. By tying the estimate to a clear demand pool, using realistic penetration and feed intensity inputs, and then cross-checking the result with trade and pricing signals, the final number stays easier to replicate and interpret year over year.

Key Questions Answered in the Report

What is the current value of the Vietnam compound feed market?

It reached USD 1.86 billion in 2026 and is projected to climb to USD 2.23 billion by 2031.

Which ingredient group dominates feed formulations in Vietnam?

Grains and cereals account for 65% of Vietnam compound feed value in 2025, reflecting heavy reliance on corn and broken rice blends.

Why is aquaculture feed growing faster than terrestrial segments?

Export shrimp and pangasius farmers need certified, high-specification rations that support an 8.4% CAGR through 2031.

How do new regulations affect formulation costs?

Limits on antimicrobial growth promoters require mills to incorporate pricier organic acids, essential oils, and probiotics, adding 3-5% to material cost.

Who leads the Vietnam compound feed market?

Charoen Pokphand Group Co., Ltd, Cargill, Incorporated, De Heus Animal Nutrition B.V., GreenFeed Group JSC, and Tongwei Co., Ltd. leads the Vietnam compound feed market 2025.

Page last updated on: