Urinary Flow Meters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

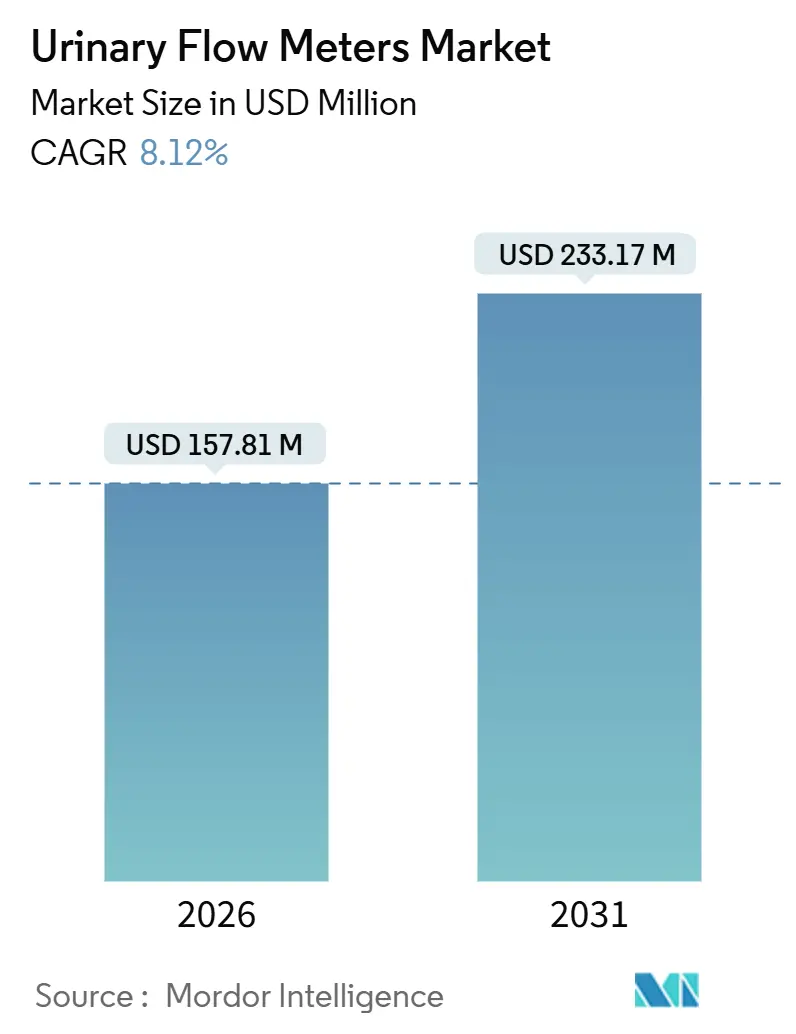

| Market Size (2026) | USD 157.81 Million |

| Market Size (2031) | USD 233.17 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

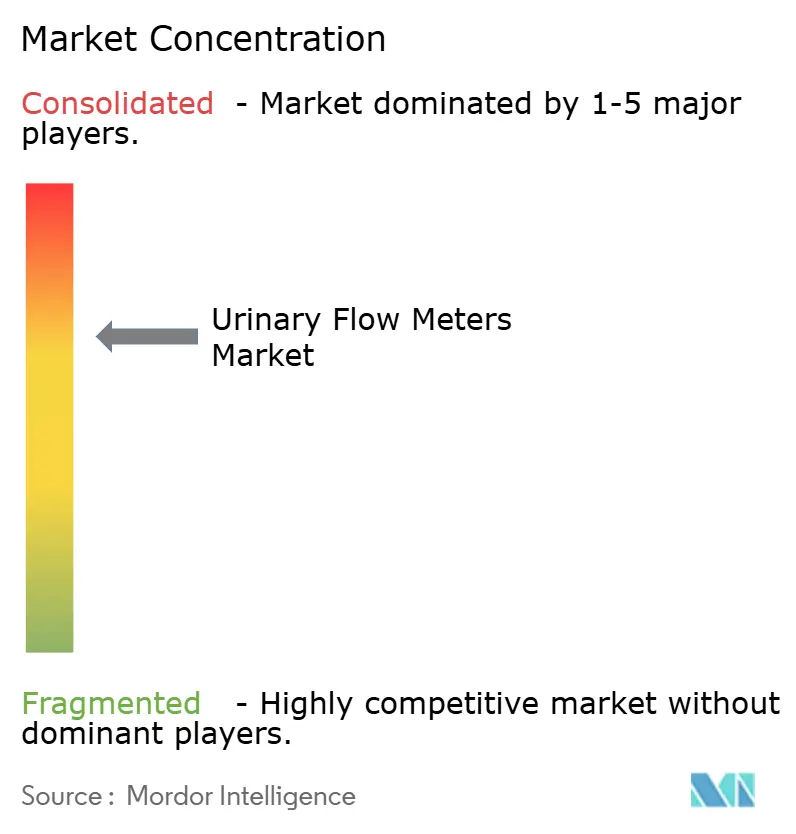

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Flow Meters Market Analysis by Mordor Intelligence

The urinary flow meters market size is estimated at USD 157.81 million in 2026 and is forecasted to reach USD 233.17 million by 2031, advancing at an 8.12% CAGR over the period. Growth momentum is anchored in wireless connectivity, artificial intelligence, and regulatory support for home-based monitoring, which together shift diagnostic activity away from hospital-centric models. Medicare reimbursement for remote uroflowmetry, the FDA’s TEMPO pilot for decentralized trials, and the EU’s streamlined software classification are accelerating commercial launches. Competitive intensity is moderate as Laborie, MMS, and MEDICA consolidate niche assets while start-ups pursue smartphone acoustics and SaaS analytics. Asia-Pacific infrastructure buildout, an aging population, and sub-30% device penetration provide a long runway, whereas cybersecurity mandates and capital constraints weigh on near-term adoption.

Key Report Takeaways

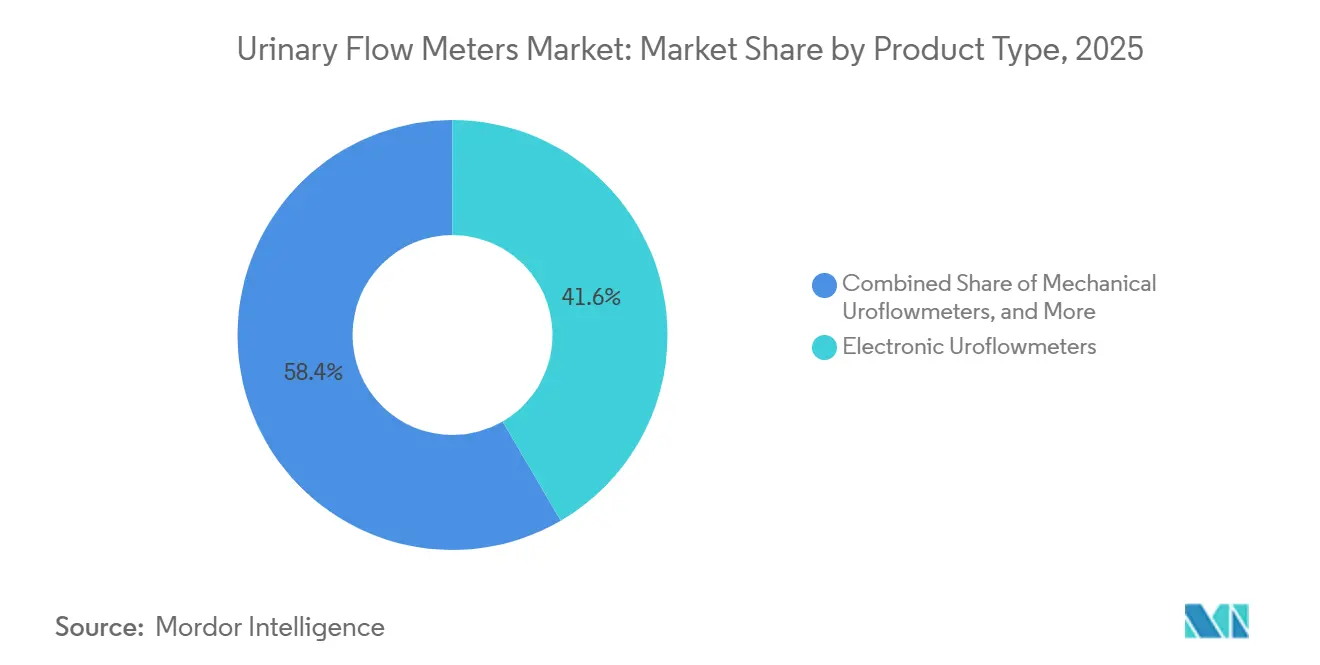

- By product type, electronic uroflowmeters led with 41.55% market share in 2025, while wireless variants are projected to expand at a 9.25% CAGR through 2031.

- By portability, stationary and benchtop systems held 54.53% share of the urinary flow meters market size in 2025; home-use smart devices are poised for a 10.85% CAGR to 2031.

- By application, benign prostatic hyperplasia accounted for 41.23% of the urinary flow meters market size in 2025, whereas pediatric urology is advancing at a 9.55% CAGR across the forecast period.

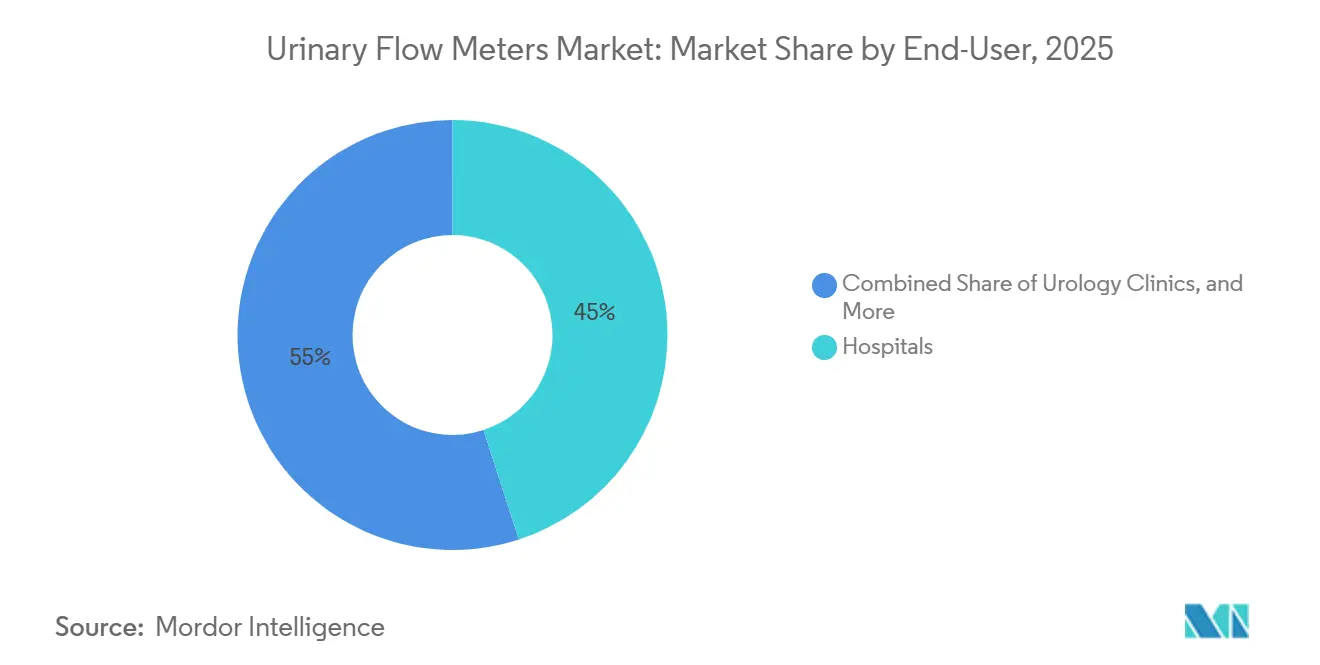

- By end user, hospitals commanded 45.03% urinary flow meters market share in 2025 and home-care settings are set to grow at an 11.11% CAGR through 2031.

- By geography, North America led with 38.13% revenue share in 2025, and Asia-Pacific is forecast to register a 9.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urinary Flow Meters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of BPH & Urinary Incontinence | +2.1% | Global, with concentration in North America, Europe, and aging Asia-Pacific markets | Long term (≥ 4 years) |

| Aging Global Population | +1.8% | Global, particularly Japan, South Korea, Western Europe, and North America | Long term (≥ 4 years) |

| Technological Advances in Wireless & Portable Devices | +1.5% | North America & EU early adoption, APAC scale deployment | Medium term (2-4 years) |

| FDA Endorsement of Home-Based Digital Uroflowmetry | +1.3% | North America, with spillover to EU and APAC regulatory harmonization | Short term (≤ 2 years) |

| AI-Driven Predictive Analytics Creating New Saas Revenue | +1.0% | North America & EU, pilot deployments in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of BPH and Urinary Incontinence

Lower urinary tract symptoms affect more than 50% of men aged 51-60 and over 90% of those aged 80 and older, establishing a stable demand base immune primarily to economic cycles[1]National Institute of Diabetes and Digestive and Kidney Diseases, “Lower Urinary Tract Symptoms in Men,” niddk.nih.gov. Urinary incontinence compounds this pool, with under-diagnosis estimated at 40-60%. Uroflowmetry serves as a first-line, noninvasive screening test that triages patients toward invasive studies or surgery. The shift to outpatient clinics and homes increases measurement frequency, improves diagnostic accuracy, and reduces the number of false-positive surgeries. Expanding reimbursement further supports repeat testing, reinforcing uroflowmetry’s role as a gatekeeper in BPH care pathways.

Aging Global Population

The United Nations projects that the number of people aged 65 or older will reach 1.6 billion by 2050, double the 2022 level. Age-driven detrusor changes and prostate enlargement correlate closely with device demand. Japan, South Korea, and Italy already exceed 28% elderly share, and China and India are entering rapid aging phases. China’s National Health Commission noted an 18% jump in urological consultations in 2024, outpacing overall outpatient growth. Home uroflowmeters align with aging-in-place policies that reduce caregiver burden and hospital readmissions, and reimbursement recognition in Japan and South Korea removes a significant hurdle to adoption.

Technological Advances in Wireless and Portable Devices

Bluetooth Low Energy and Wi-Fi 6 have lowered power draw and component costs, enabling compact devices that stream real-time data to the cloud. A portable system published in IEEE in 2025 achieved 95% correlation with gravimetric standards at weights under 500 g[2]IEEE, “Portable Uroflowmetry System With Integrated Software,” ieeexplore.ieee.org. Smartphone microphones paired with machine learning hit 96% accuracy, hinting at commoditization pressure on dedicated hardware. Lower price points invite penetration in cost-sensitive regions and support direct-to-consumer pathways, shifting capital expenditure from hospitals to patients and payers.

FDA Endorsement of Home-Based Digital Uroflowmetry

The TEMPO pilot, launched in December 2025, places connected urological monitors on an expedited review track[3]U.S. Food and Drug Administration, “TEMPO Pilot Program for Digital Health Technologies,” fda.gov. Bright Uro’s Glean system used this route to secure 510(k) clearance in April 2025, validating wireless performance without the use of catheters. Medicare’s addition of urological parameters to CPT codes 99453, 99454, and 99457 gives providers a billing mechanism and shifts device economics toward covered home use. EU regulators synchronized by classifying SaaS uroflowmetry under Class IIa, lowering evidentiary burdens and compressing launch timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Systems | -1.2% | Global, acute in price-sensitive APAC and South America markets | Short term (≤ 2 years) |

| Need for Skilled Personnel & Inconsistent Patient Compliance | -0.9% | Global, more pronounced in regions with lower healthcare literacy | Medium term (2-4 years) |

| Data-Privacy / Cyber-Security Hurdles Delaying Procurement | -0.7% | North America & EU due to stringent HIPAA and GDPR enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Systems

Hospital-grade units with pressure-flow add-ons are priced between USD 15,000 and USD 40,000, forcing trade-offs with imaging and robotic platforms in capital plans. A 2024 survey found that 38% of U.S. departments deferred replacements due to budget reallocations[4]American Urological Association, “Capital Equipment Trends Survey 2024,” auanet.org. Emerging markets face tighter constraints, with per-capita equipment budgets roughly one-tenth those in North America. Leasing and pay-per-use models can cut cash outlay by 60-70% but remain nascent. Home devices below USD 500 bypass institutional procurement yet often require patient self-funding. Demonstrated episode-of-care savings of USD 1,200 over two years provide a value story but still need payer alignment.

Need for Skilled Personnel and Inconsistent Patient Compliance

A 2024 audit revealed that 31% of hospital tests were technically inadequate due to low voided volume or patient anxiety[5]Journal of Urology, “Technical Adequacy Audit of Uroflowmetry,” jurology.com . Home devices magnify the challenge because patients can misplace sensors or misread instructions. JMIR reported 24% of proudP users needed coaching to capture valid data. Specialist shortages loom; the AUA projects a 30% deficit relative to demand by 2035. Automated quality-control alerts help, but add software complexity and regulatory overhead. Compliance with repeat measurements falls to 60% after three months, blunting longitudinal benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wireless Variants Outpace Legacy Electronic Systems

Electronic units held a 41.55% share of the urinary flow meters market in 2025 and remain embedded in hospital labs for multi-parameter studies. Over the forecast period, wireless devices are projected to log a 9.25% CAGR as Bluetooth Low Energy and Wi-Fi 6 connectivity eliminate cabling and support ambulatory care.

Electronic platforms integrate with HL7 records and command premiums of USD 20,000-35,000, locking in incumbents through replacement cycles. By contrast, modular wireless hubs that couple with flow, pressure, and ultrasound sensors let hospitals add functions without complete system swaps. At the same time, units under USD 1,000 enable small clinics to upgrade rapidly. Academic prototypes such as the i-Flow wearable demonstrated 92% accuracy and <500 g, underscoring the speed of miniaturization.

By Portability: Home-Use Devices Redefine Care Delivery

Stationary systems held 54.53% of the urinary flow meters market share in 2025, favored for precision and multi-parameter integration. Medicare’s 2024 CPT additions converted home-use uroflowmetry from patient-pay to reimbursable, producing a forecast 10.85% CAGR in this segment.

Bright Uro’s Glean system, cleared in April 2025, typifies home-use design with smartphone pairing that streams encrypted data to clinician dashboards. Portable units bridge clinics and ambulatory centers, yet smartphone apps leveraging acoustic signatures could undercut hardware in low-acuity screening. The economic tipping point is a retail price below USD 300, enabling direct-to-consumer channels that shift capital outlays to payers and patients.

By Application: Pediatric Urology Emerges as Growth Frontier

Benign prostatic hyperplasia accounted for 41.23% of the urinary flow meters market size in 2025, as clinicians rely on uroflowmetry before invasive urodynamics. Pediatric urology is forecast to rise at a 9.55% CAGR through 2031, driven by radiation-free diagnostics for congenital anomalies.

A 2024 study showed that flowmetry plus ultrasound achieved 87% sensitivity for detecting vesicoureteral reflux in children, rivalling voiding cystourethrography without catheters. Female incontinence and neurogenic bladder represent untapped niches needing anatomy-specific designs and long-term monitoring. Quarterly surveillance after urethral stricture surgery cements steady demand for high-utilization devices despite lower prevalence.

By End-User: Home Care Settings Disrupt Hospital-Centric Models

Hospitals accounted for 45.03% of the urinary flow meters market share in 2025, reflecting their role as the gateway for benign prostatic hyperplasia diagnosis and pre-surgical evaluation, where uroflowmetry links with pressure-flow studies and cystoscopy. U.S. capital budgets for urology departments range from USD 500,000 to USD 2 million per year, so uroflowmeters compete directly with imaging suites and surgical robots for funding. Despite this institutional dominance, fee-for-service clinics and diagnostic centers still capture complex cases that demand multi-parameter studies, sustaining demand for high-specification instruments even as payer pressure narrows margins. Ambulatory surgical centers, which perform 60% of U.S. transurethral resections, mainly deploy flowmeters for post-operative surveillance, a lower-volume but compliance-driven application that helps keep utilization steady.

Home care settings represent the fastest-growing channel, advancing at an 11.11% CAGR through 2031 as remote monitoring reimbursement and direct-to-consumer sales draw diagnostics outside hospital walls. A December 2025 JMIR study on the proudP mobile app showed that at-home uroflowmetry trimmed clinic visits by 2.3 appointments per patient and saved USD 600-800 per episode of care. This shift forces manufacturers to balance institutional contracts, which bundle service and training, with e-commerce models that favor lower pricing and simplified onboarding. Dual-channel strategies require distinct regulatory labeling, separate technical support pathways, and differentiated pricing to avoid channel conflict. Vendors that harmonize these tracks stand to capture a disproportionate share of the urinary flow meters market as adoption spreads across both professional and consumer settings.

Geography Analysis

North America contributed 38.13% of the urinary flow meters market revenue in 2025, supported by 1.2 million annual procedures and early wireless adoption. Medicare’s remote monitoring codes encourage physician uptake, and Canada trails primarily due to provincial reimbursement variability.

Asia-Pacific is slated for a 9.81% CAGR to 2031, the fastest region, as China and India expand device penetration from under 30% of clinical need. China recorded an 18% rise in urology visits in 2024, while Japan and South Korea classify home devices as reimbursable durable equipment, spurring demand. Local manufacturing in India trims import duties, improving price competitiveness against multinational offerings.

Europe maintains solid uptake through bundled reimbursement in Germany, the United Kingdom, and France. Gulf Cooperation Council investments and private Brazilian clinics foster emerging-region sales, yet reimbursement gaps slow institutional deployments in South America and parts of Africa. Multinationals thus view Asia-Pacific as the primary growth lever for the next five years.

Competitive Landscape

Laborie, MMS, and MEDICA together command a meaningful yet non-dominant share, defining a moderately concentrated urinary flow meters industry. Laborie’s November 2025 acquisition of the JADA System and its 2023 purchase of Urotronic illustrate a bolt-on strategy that links diagnostics with therapeutic devices. Boston Scientific’s USD 3.7 billion Axonics deal shows large strategics knitting diagnostics into broader continence portfolios.

Technology differentiation now centers on AI analytics and connectivity rather than sensor precision, which has plateaued at ±2%. A Nature study found that machine vision outperformed human interpretation, pushing vendors toward SaaS models with recurring fees. Patent activity clusters around acoustic flowmetry, cloud dashboards, and wearable sensors, foreshadowing algorithm-focused intellectual-property disputes.

Regulatory compliance with FDA cybersecurity and EU software standards forms a barrier as smaller firms absorb a 15-20% cost premium for secure coding and penetration testing. Disruptors like proudP and UroMems chase underserved niches in female care and implantable sensors, yet must navigate rising compliance overheads to scale.

Urinary Flow Meters Industry Leaders

Andromeda Medizinische Systeme

Laborie

MEDICA S.p.A

MMS Medical Measurement Systems

NOVAmedtek

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cleveland Clinic implemented the Glean Urodynamics System, marking the first wireless, catheter-free approach to complete urodynamic monitoring.

- April 2025: Bright Uro received FDA 510(k) clearance K243052 for Glean Urodynamics System, a wireless, home-operable device that transmits real-time data to clinicians.

Global Urinary Flow Meters Market Report Scope

As per the report's scope, urinary flow meters (uroflowmeters) are diagnostic medical devices used to measure the rate, volume, and pattern of urine flow during voiding. They help assess lower urinary tract function by identifying abnormalities such as obstruction or weak bladder muscle activity. These devices are commonly used in the evaluation of conditions like benign prostatic hyperplasia (BPH), urinary incontinence, and other voiding disorders.

The urinary flow meters market segmentation includes product type, portability, application, end-user, and geography. By product type, the market is segmented into electronic, mechanical, and wireless/digital uroflowmeters. By portability, the market is segmented into stationary/benchtop systems, portable/handheld systems, and home-use smart devices. By application, the market is segmented into benign prostatic hyperplasia (BPH), urinary incontinence, neurogenic bladder disorders, urethral stricture & obstruction, and pediatric urology. By end-user, the market is segmented into hospitals, urology clinics, diagnostic centers, ambulatory surgical centers, and home care settings. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Electronic Uroflowmeters |

| Mechanical Uroflowmeters |

| Wireless / Digital Uroflowmeters |

| Stationary / Benchtop Systems |

| Portable / Hand-held Systems |

| Home-use Smart Devices |

| Benign Prostatic Hyperplasia (BPH) |

| Urinary Incontinence |

| Neurogenic Bladder Disorders |

| Urethral Stricture & Obstruction |

| Pediatric Urology |

| Hospitals |

| Urology Clinics |

| Diagnostic Centers |

| Ambulatory Surgical Centers |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electronic Uroflowmeters | |

| Mechanical Uroflowmeters | ||

| Wireless / Digital Uroflowmeters | ||

| By Portability | Stationary / Benchtop Systems | |

| Portable / Hand-held Systems | ||

| Home-use Smart Devices | ||

| By Application | Benign Prostatic Hyperplasia (BPH) | |

| Urinary Incontinence | ||

| Neurogenic Bladder Disorders | ||

| Urethral Stricture & Obstruction | ||

| Pediatric Urology | ||

| By End-User | Hospitals | |

| Urology Clinics | ||

| Diagnostic Centers | ||

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the urinary flow meters market in 2031?

The market is forecast to reach USD 233.17 million by 2031.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to post the highest CAGR at 9.81% during the forecast window.

Which product segment leads the market by share today?

Electronic uroflowmeters account for 41.55% of current revenue.

Why are home-use devices gaining popularity?

Reimbursement codes for remote monitoring and FDA support make home devices eligible for coverage, shifting diagnostics out of hospitals.

What is a major restraint hindering rapid adoption?

High upfront costs for advanced systems remain a significant short-term barrier, especially in price-sensitive regions.

How is artificial intelligence influencing this space?

AI analytics improve diagnostic accuracy and enable SaaS revenue models that deliver higher margins than hardware sales.

Page last updated on: