United Kingdom White Glove Delivery Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

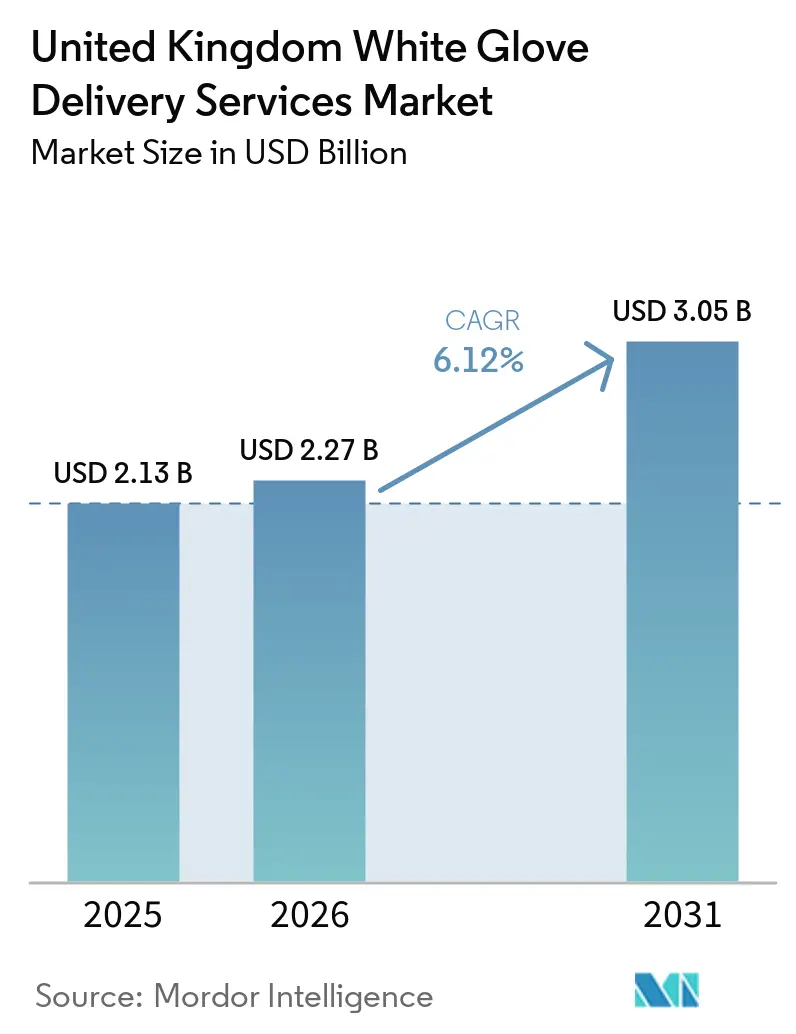

| Base Year Market Size (2025) | USD 2.13 Billion |

| Market Size (2026) | USD 2.27 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

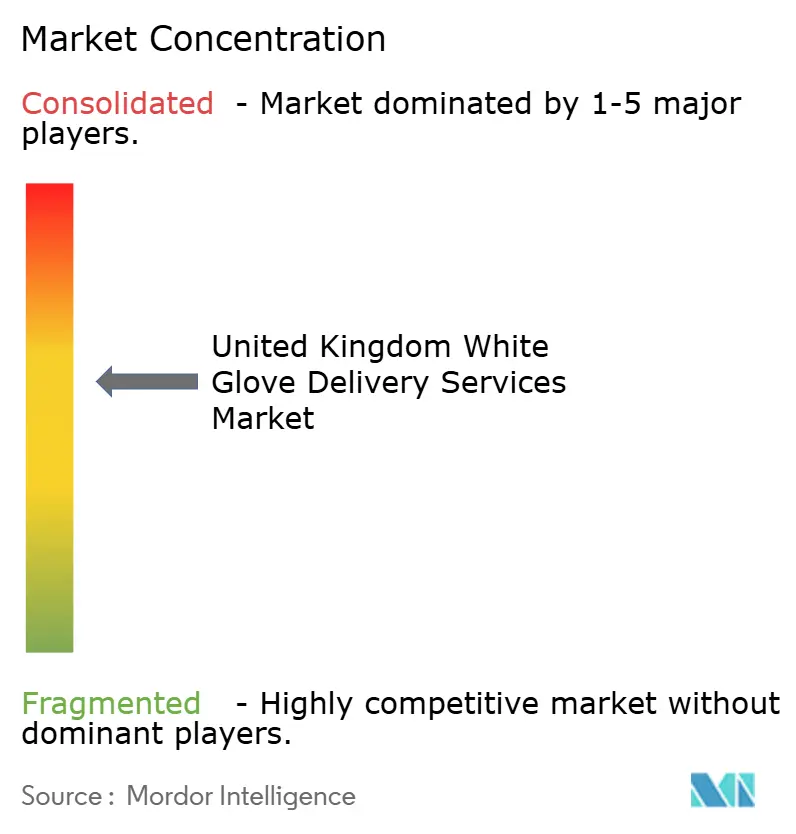

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom White Glove Delivery Services Market Analysis by Mordor Intelligence

The United Kingdom white glove delivery services market size is projected to be USD 2.13 billion in 2025, USD 2.27 billion in 2026, and reach USD 3.05 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

Rising online sales of bulky items like furniture and large appliances are expanding demand for two-person crews that can place products in the room of choice, assemble them, and clear packaging. Retailers are leaning on specialist logistics partners to improve post-purchase satisfaction, a shift reinforced by survey findings that reliability matters more than raw speed for most United Kingdom shoppers. Consolidation among third-party logistics providers is boosting route density and spreading the high fixed costs of premium fleets across more stops. Meanwhile, London’s Ultra Low Emission Zone and other clean-air policies are nudging operators toward electric and low-carbon trucks, raising upfront capital needs but lowering long-term running costs.[1]Transport for London, “Ultra Low Emission Zone (ULEZ),” tfl.gov.uk

Key Report Takeaways

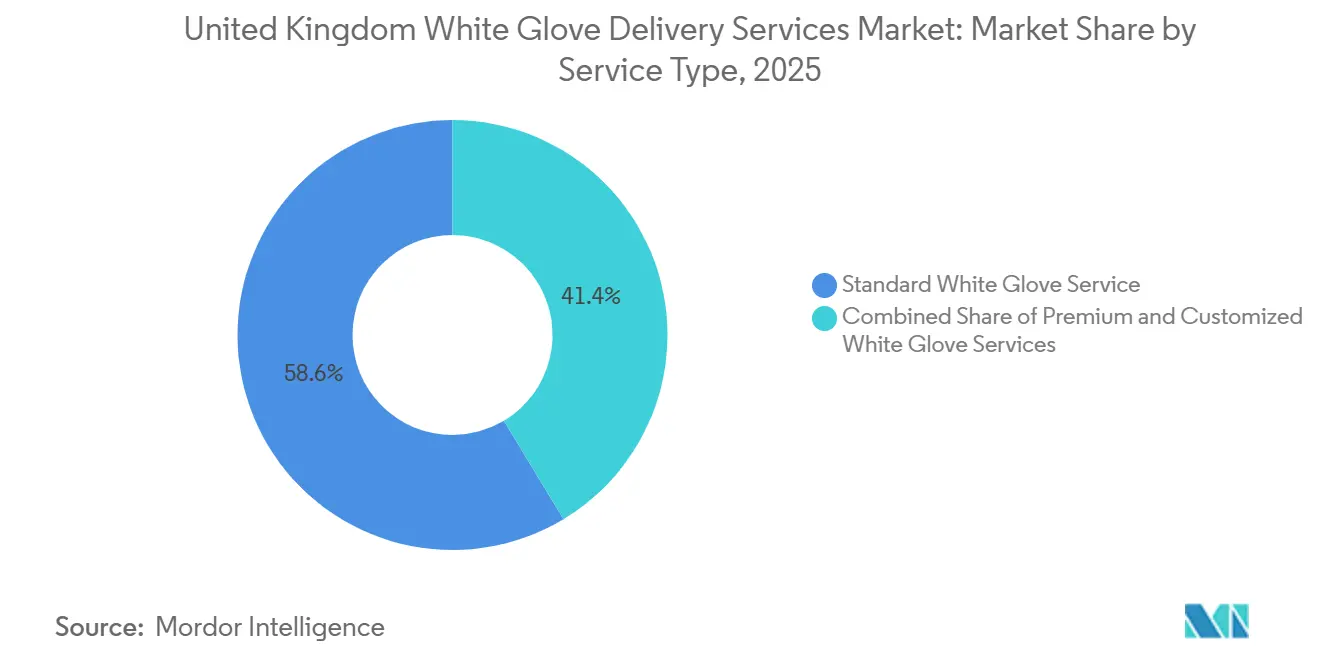

- By service type, standard white glove service held 58.63% of the United Kingdom white glove delivery services market share in 2025; premium white glove service is projected to expand at a 13.65% CAGR through 2031.

- By end-user industry, furniture and home goods accounted for 45.46% of the United Kingdom white glove delivery services market size in 2025, while consumer electronics and appliances is forecast to grow at a 13.69% CAGR through 2031.

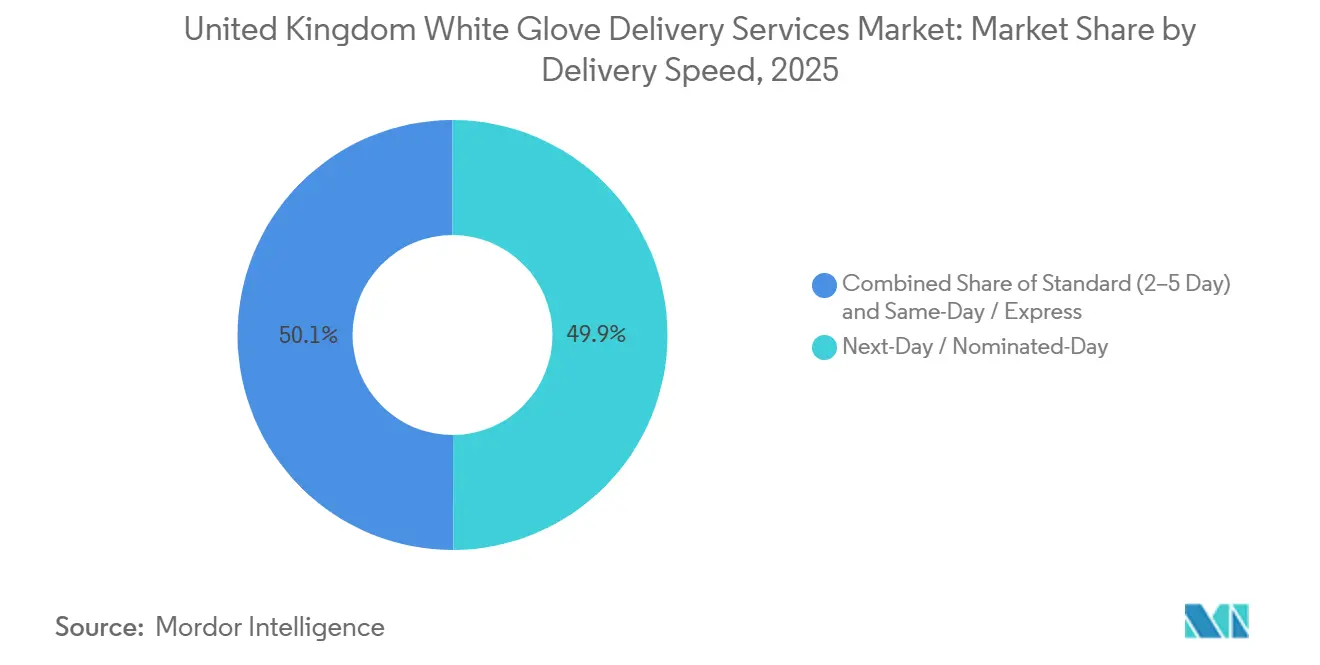

- By delivery speed, next-day / nominated-day accounted for 49.93% of the United Kingdom white glove delivery services market share in 2025, whereas same-day /express is poised for a 15.87% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom White Glove Delivery Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom in Bulky-Item Categories | +2.1% | Nationwide, with clusters in Greater London, Manchester, Birmingham | Medium term (2-4 years) |

| Customer-Experience-Led Value-Added Delivery Demand | +1.5% | National, urban centers lead adoption | Short term (≤2 years) |

| Returns Handling and Reverse Logistics Integration | +0.9% | National, strong in the London and Midlands e-commerce corridors | Medium term (2-4 years) |

| Consolidation and Capital Inflow from Global 3PLs | +0.8% | National | Long term (≥4 years) |

| Smart-Home Device Bundle Installations | +0.6% | Greater London and Southeast England | Medium term (2-4 years) |

| ULEZ-Driven Shift to Compliant Premium Fleets | +0.4% | Greater London, expanding Clean Air Zones nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom in Bulky-Item Categories

Online sales of large items such as sofas, refrigerators, and big-screen televisions climbed 14.7% year on year in January 2026, the sharpest monthly rise since 2021. Bulky products require two-person crews for safe, room-of-choice delivery, so every uptick in this retail segment expands the addressable market for United Kingdom white glove delivery services. National data show the online share of total retail sales reached 28.2% in February 2026, with furniture and appliances among the fastest movers. Retailers are therefore retooling checkout flows to surface assembly add-ons, converting a cost center into a revenue stream. This structural shift is expected to support steady volume growth for premium crews well beyond the forecast window.[2]Office for National Statistics, “Retail sales, Great Britain,” ons.gov.uk

Customer-Experience-Led Value-Added Delivery Demand

Consumer sentiment analysis reveals that United Kingdom shoppers overwhelmingly identify poor delivery communication as their primary logistics frustration. Additionally, there is near-universal consumer dissatisfaction when couriers leave parcels in unsecured or unsafe locations. This favors the United Kingdom white glove delivery services market because appointment scheduling, call-ahead notifications, and in-home handoff are standard features. IKEA’s February 2025 integration with TaskRabbit shows the commercial upside: customers who chose assembly lifted average order value by 4.7 times and cut returns on complex items by roughly 40%. Value-added reliability, not raw speed, is proving to be the stronger loyalty driver.

Returns Handling and Reverse Logistics Integration

Returns remain a pain point, with 25% of consumers naming shipping cost as their biggest complaint and others citing refund delays and awkward drop-offs. White-glove operators now bundle disassembly, repackaging, and condition checks into a single visit, giving retailers a single vendor for both outbound and inbound flows. Adding reverse legs raises vehicle utilization, which is vital in a labor-intensive two-person model. Logistics firms such as EV Cargo have launched dedicated furniture and appliance return programs that promise better recovery values and faster resale cycles. These enhancements deepen customer contracts and help stabilize revenue during non-peak seasons.

Consolidation and Capital Inflow from Global 3PLs

Three landmark deals reshaped the competitive map in 2025-2026: Jacky Perrenot bought ArrowXL, DSV absorbed Schenker, and GXO gained Wincanton after regulatory clearance. Larger balance sheets now underwrite fleet electrification, warehouse automation, and shared networks that spread two-person fixed costs across more stops. Open-book contracts, which made up 79% of Wincanton’s 2024 revenue, allow inflation pass-through and protect margins. As capital intensity rises, smaller regional carriers may struggle to match service levels, opening acquisition or subcontracting opportunities. Scale, therefore, is becoming a decisive competitive variable.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor and Operating Cost Premium | -0.7% | National, acute in London and Southeast England | Short term (≤ 2 years) |

| Shortage of Skilled Two-Person Crews | -0.5% | National, shortages pronounced in the Midlands and the North | Medium term (2-4 years) |

| Damage Liability and Insurance Costs | -0.3% | National, most significant in the luxury goods and electronics lanes | Medium term (2-4 years) |

| Fragmented Subcontractor Networks Impacting Service Consistency | -0.2% | Nationwide, especially outside major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Labor and Operating Cost Premium

Average heavy-goods-vehicle wages climbed from USD 41,000 in 2020 to USD 55,000 in 2025 after converting from sterling, while the National Living Wage rose 6.7% to USD 15.3 per hour in April 2025. Employer payroll taxes also increased, adding roughly USD 1.9 billion in extra labor costs across the logistics sector. Two-person crews double payroll per stop, and tight appointment windows cap daily drop density, squeezing profit per route. Fleet electrification reduces fuel spend but requires a significant capital outlay for trucks and depot chargers. Operators tied into legacy fixed-price contracts risk margin erosion unless they renegotiate to open-book terms.

Shortage of Skilled Two-Person Crews

While acute HGV driver vacancies stabilized throughout 2024, a severe structural deficit persists as approximately 49% of the active United Kingdom commercial driver pool is aged 50 or older, accelerating retirement-driven attrition. Although license testing capacity has improved, retirements still outpace new entrants. White-glove work compounds the challenge because it needs physical strength, in-home etiquette, and technical assembly skills beyond standard driving. Companies like Wincanton run “People Campus” resourcing hubs across 18 sites to smooth peaks, yet the underlying labor pool remains tight. The persistent shortfall elevates overtime costs, increases reliance on subcontractors, and can cap growth even when demand is strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Premium Tiers Capture Installation Revenue

Standard white glove service accounted for 58.63% of the United Kingdom white glove delivery services market share in 2025, underscoring its role as the default two-person, room-of-choice option for bulky products. Demand in this core segment is anchored to furniture and appliance retailers that prize reliable appointment windows over raw speed. Yet the premium tier is where margin expansion lies. Premium white glove service is projected to grow at a 13.65% CAGR through 2031 as retailers increasingly bundle assembly, smart-home setup, and haul-away into checkout flows. IKEA’s TaskRabbit integration, priced at USD 41.3 per job, lifted attach rates by 50% and reduced complex-item returns by roughly 40%, proving consumers will pay for turnkey convenience.

The upsell potential explains why global 3PLs such as GXO Logistics and DHL have integrated scheduling portals that surface premium add-ons at the point of booking. Larger fleets also support bespoke services such as climate-controlled art transport and white-glove handling for medical devices, areas where specialist insurers such as Lloyd’s underwrite high-value cargo at 0.50% of declared value. Open-book contracts, which accounted for 79% of Wincanton’s 2024 revenue, let operators pass through wage and fuel inflation to shippers, protecting profitability even as service complexity rises. As a result, the premium and customized tiers are expected to add more than USD 280 million to the United Kingdom white glove delivery services market size by 2031, despite representing a smaller volume base today. Operators that combine live tracking, certified technicians, and emissions-compliant trucks are best placed to capture this growth.

By End-User Industry: Electronics Surge on Smart-Home Demand

Furniture and home Goods led end-user demand, accounting for 45.46% of the United Kingdom white glove delivery services market size in 2025, reflecting the inherent need for two-person crews to position, assemble, and remove packaging for sofas, wardrobes, and dining sets. Online retail sales of household goods climbed 6.8% month on month in February 2025 and continued to outpace overall e-commerce growth into 2026, sustaining high baseline volumes for this segment. Retailers emphasize reliability over speed; a survey showed only 4% of shoppers truly expect same-day delivery, while 83% are satisfied with a two-to-four-day window if communication is clear. White-glove offerings that guarantee room-of-choice placement and time-definite slots, therefore, remain sticky.

Consumer electronics and appliances is on track to be the fastest-growing vertical, advancing at a 13.69% CAGR between 2026 and 2031 as connected devices proliferate. Large-screen televisions, smart refrigerators, and multi-component sound systems require wall mounting or Wi-Fi pairing, which standard parcel networks cannot deliver economically. Retailers integrate service prompts directly into checkout; when customers opt for installation, average order value jumps 4.7 times and post-sale returns plunge, mirroring the results IKEA recorded in February 2025. As Generation Z households upgrade rental flats into tech-enabled living spaces, electronics will add disproportionate incremental dollars to the United Kingdom white glove delivery services market size. Providers that certify crews for basic electrical work and smart-home configuration will enjoy higher margins and stronger contract renewal rates.[3]International Trade Administration, “United Kingdom - eCommerce,” trade.gov

By Delivery Speed: Express Gains in Dense Urban Routes

Next-day / nominated-day delivery dominated with 49.93% of 2025 demand, proving that certainty trumps ultrafast promises for most bulky-item buyers in the United Kingdom white glove delivery services market. A 2025 survey confirmed the point: 83% of United Kingdom shoppers deem a two-to-four-day window reasonable if tracking is accurate, whereas only 4% truly expect same-day service. Batch routing within fixed appointment windows also boosts vehicle utilization, a key cost lever for two-person crews. Consequently, global integrators such as FedEx have focused investment on predictive ETA alerts rather than pure speed.

Same-day / express delivery, however, is forecast to post a 15.87% CAGR through 2031, concentrated in London, Manchester, and Birmingham, where dense postcodes support rapid fulfillment economics. Technology start-ups such as Hived, which raised USD 38.8 million in July 2025, use AI to cluster jobs and cut empty miles in real time. Yet rapid-delivery networks experience 104.5% higher delays when promises slip, so operators need robust contingency planning. For now, express tiers remain a premium upsell that buyers select for high-value items or special occasions, adding profitable pockets rather than displacing the core next-day base. As Clean Air Zones widen, electric van availability will shape how broadly express coverage can scale across the United Kingdom white glove delivery services market.

Geography Analysis

Greater London is the largest demand center for the United Kingdom white glove delivery services market, reflecting the capital’s dense population, high disposable income, and strict Ultra Low Emission Zone (ULEZ) standards that favor fleet-compliant, value-added operators. Retailers report that two-person crews in London average 5.2 stops per van per day, versus 3.4 in the rest of the country, because short travel distances compress dwell time and increase asset utilization. Same-day and nominated-day delivery tiers gain particular traction in the capital, helped by advanced booking portals that let consumers select a two-hour window capability that is financially viable only where address density supports tight routing. Greater London also hosts most of the nation’s smart-home installations, so crews certified for Wi-Fi pairing and wall mounting capture above-average ticket values. As the ULEZ footprint expanded in August 2025, operators already running Euro 6 diesel, liquefied natural gas, or battery-electric trucks avoided the USD 15.6 daily penalty and won incremental corporate contracts tied to Scope 3 carbon targets.

South-East and East England form the next-largest corridor, anchored by distribution parks along the M1 and M25 motorways that shorten line-haul legs into London while covering affluent suburban catchments such as Surrey, Kent, and Hertfordshire. Furniture chains and electronics retailers exploit these hubs to offer next-day room-of-choice service to roughly 19 million residents within a 90-minute drive. Warehouse automation is more advanced here than in any other region; DHL’s July 2025 roll-out of 1,000 picking robots began at its Milton Keynes campus, trimming unit handling costs by 22% and freeing human labor for in-home assembly work. Clean-air regulations in Oxford, Brighton, and Canterbury mirror London’s model, so fleets that invested early in alternative fuels can serve multiple cities without incurring daily surcharges. The region’s fast broadband coverage also underpins real-time tracking portals that message customers 30 minutes before arrival, a service feature that surveys rank as the most powerful loyalty driver after on-time performance.

The Midlands and North of England contribute steady but more cost-sensitive volumes, with Birmingham, Manchester, and Leeds acting as consolidation nodes for two-person networks extending into surrounding rural districts. Same-day service is viable only inside these metropolitan rings; elsewhere, retailers push nominated-day windows to balance wage pressure against lower address density. Labor shortages are most acute here: nearly 24% of firms reported heavy-goods-vehicle vacancies in 2025, forcing wider use of subcontractors who may lack installation credentials. Nonetheless, the Midlands logistics “Golden Triangle” remains attractive for new fulfilment centers because it sits within four hours’ drive of 90% of the UK population. GXO Logistics plans to fold Wincanton’s Lutterworth campus into its national control tower in 2026, a move expected to lift first-attempt delivery success by 3 percentage points through tighter asset pooling. Scotland, Wales, and Northern Ireland together supply a modest share of national revenue but are forecast to outpace national growth because parcel carriers are retreating from bulky freight there, creating white space for specialists with cross-docking and ferry links in place.[4]Department for Business and Trade, “UK Logistics: The Golden Triangle,” gov.uk

Competitive Landscape

Intense rivalry characterizes the United Kingdom white glove delivery services market as global integrators DHL, United Parcel Service (UPS), and FedEx fight for the same premium contracts that specialist firms such as Wincanton and Bishopsgate Logistics target. The three multinationals lean on deep capital pools to roll out electric heavy-goods vehicles and warehouse robotics faster than regional peers, a capability that aligns with retailers’ net-zero pledges and helps win multi-year frameworks. Large fleets also enable shared-network models, which lower empty-mile ratios and improve crew utilization, a decisive edge when labor and fuel costs are rising. At the same time, niche operators focused on fine art or medical devices defend their turf through bespoke crating, climate-controlled trucks, and stringent compliance with the Medicines and Healthcare Products Regulatory Agency that bigger players rarely match.

A second layer of rivalry comes from aggressive consolidation that is redrawing market boundaries. Jacky Perrenot’s June 2025 acquisition of ArrowXL gave the French group an instant national footprint, while DSV’s USD 15.6 billion purchase of Schenker in 2025 created a logistics giant with end-to-end coverage. GXO Logistics closed its USD 965 million takeover of Wincanton in mid-2024, a move that folded Wincanton’s two-person fleet into GXO’s global control tower and elevated open-book contracts to 79% of revenue. These deals raise the minimum efficient scale required to compete in the United Kingdom white glove delivery services market, squeezing smaller independents that cannot finance fleet electrification or advanced routing platforms.

Technology is the third competitive lever. DHL invested USD 700 million in July 2025 to install 1,000 picking robots and expand real-time tracking across the United Kingdom white glove delivery services market, trimming warehouse labor hours by 22%. Wincanton’s EyeQ control tower, coupled with exclusive UK rights to the Zeus subcontractor-management platform, cuts road miles by more than 10% while boosting first-attempt delivery success. Start-ups such as Hived apply artificial-intelligence clustering to same-day jobs, promising retailers 15% fewer failed slots and transparent carbon dashboards. Collectively, these digital upgrades tilt share toward operators that can prove on-time, in-full metrics and real-time visibility capabilities, now viewed as table stakes by omnichannel merchants.

United Kingdom White Glove Delivery Services Industry Leaders

AIT Home Delivery

DHL Group

XPO Logistics

GXO Logistics (Wincanton Specialist Services)

Rhenus Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AIT Worldwide Logistics, the parent company of the United Kingdom-based AIT Home Delivery (formerly Panther Logistics), partnered with Greenbriar Equity Group to aggressively accelerate its global expansion through 2030.

- January 2026: DX Group signed a strategic partnership with Rhenus Logistics to assume full responsibility for Rhenus's two-person home delivery services across the UK and Ireland.

- July 2025: DHL Group significantly upgraded its UK fleet to meet strict urban emission standards, doubling its liquefied natural gas (LNG) fleet to 60 trucks.

- June 2025: GXO Logistics received final CMA clearance to integrate Wincanton after agreeing to divest Wincanton’s dedicated grocery warehousing business.

United Kingdom White Glove Delivery Services Market Report Scope

| Standard White Glove Service |

| Premium White Glove Service |

| Customized White Glove Service |

| Furniture and Home Goods |

| Consumer Electronics and Appliances |

| Healthcare and Medical Devices |

| Luxury Goods and Art |

| Other (Industrial Machinery, E-commerce and Retail, etc.) |

| Standard (2 to 5 Day) |

| Next-Day / Nominated-Day |

| Same-Day / Express |

| By Service Type | Standard White Glove Service |

| Premium White Glove Service | |

| Customized White Glove Service | |

| By End-User Industry | Furniture and Home Goods |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Devices | |

| Luxury Goods and Art | |

| Other (Industrial Machinery, E-commerce and Retail, etc.) | |

| By Delivery Speed | Standard (2 to 5 Day) |

| Next-Day / Nominated-Day | |

| Same-Day / Express |

Key Questions Answered in the Report

What is the projected value of the United Kingdom white glove delivery services market by 2031?

The market is forecast to reach USD 3.05 billion by 2031, expanding at a 6.12% CAGR over 2026-2031.

Which service type is growing fastest in two-person delivery?

Premium white glove service, which bundles assembly and smart-home setup, is expected to rise at a 13.65% CAGR through 2031.

Why are electronics driving future white-glove volumes?

Smart-home devices and large-screen televisions need in-home installation, pushing consumer electronics and appliances to a 13.69% CAGR and lowering costly product returns.

How are clean-air rules influencing fleet investment?

London’s ULEZ imposes daily charges on non-compliant vehicles, so operators are adding electric, LNG, and HVO-powered trucks to stay penalty-free and win sustainability-focused contracts.

What labor issue threatens capacity expansion?

A 33% year-on-year rise in heavy-goods-vehicle driver vacancies and an aging workforce limit the supply of skilled two-person crews, pressuring wages and margins.

How is consolidation reshaping competition?

Major acquisitions by Jacky Perrenot, DSV, and GXO Logistics are raising the scale threshold, allowing larger fleets to optimize routes and invest in automation.

Page last updated on: