Telemonitoring Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

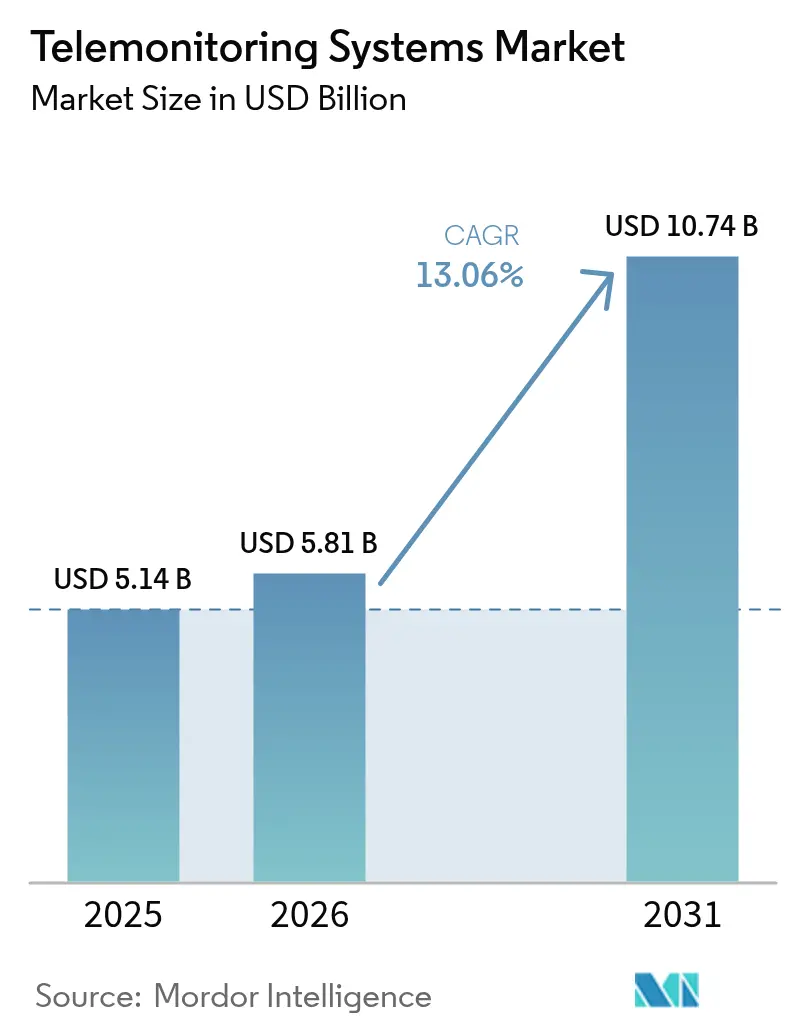

| Market Size (2026) | USD 5.81 Billion |

| Market Size (2031) | USD 10.74 Billion |

| Growth Rate (2026 - 2031) | 13.06% CAGR |

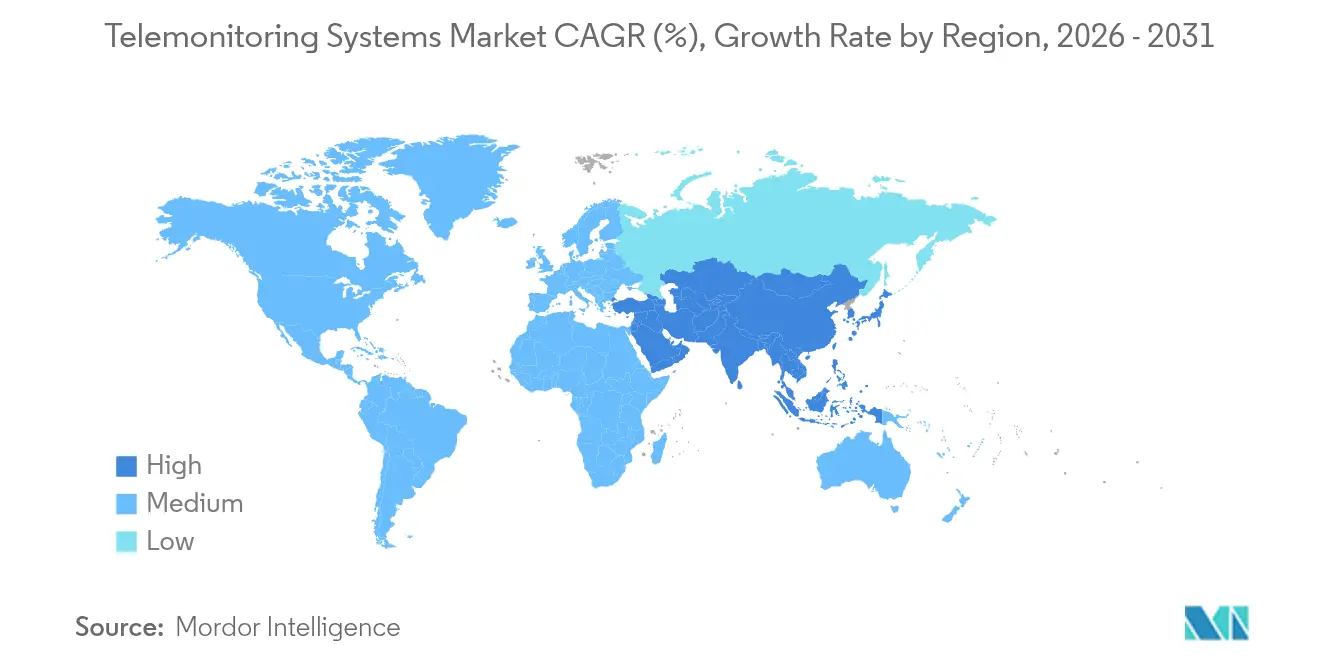

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telemonitoring Systems Market Analysis by Mordor Intelligence

The telemonitoring systems market size is expected to grow from USD 5.14 billion in 2025 to USD 5.81 billion in 2026 and is forecast to reach USD 10.74 billion by 2031 at 13.06% CAGR over 2026-2031. This growth reflects the rapid transition from episodic care to home-based, predictive models that use artificial intelligence (AI) to convert continuous data feeds into real-time clinical guidance.[1]Jonathan Blum, “Lessons from CMS’ Acute Hospital Care at Home Initiative,” Centers for Medicare & Medicaid Services, cms.gov Recent reimbursement changes—most notably the Centers for Medicare & Medicaid Services (CMS) expansion of Remote Patient Monitoring (RPM) and the debut of Advanced Primary Care Management billing codes—have made these systems financially sustainable for providers. AI-equipped cardiac platforms now detect atrial fibrillation weeks earlier than legacy monitors, while consumer-grade continuous glucose monitors (CGMs) are moving beyond diabetes care to wider metabolic-health applications. North America leads adoption thanks to aggressive Hospital-at-Home rollouts, whereas Asia-Pacific emerges as the fastest-growing region on the back of 5G infrastructure and supportive digital-health policies.

Key Report Takeaways

- By product type, cardiac systems led with 30.92% revenue share in 2025; glucose-level systems are projected to expand at a 17.02% CAGR through 2031.

- By component, devices accounted for 81.55% of the telemonitoring systems market share in 2025, while software platforms are forecast to grow at a 15.05% CAGR between 2026-2031.

- By connectivity technology, Bluetooth/Low-Energy held 35.02% share in 2025; cellular networks are expected to post the fastest 16.21% CAGR through 2031.

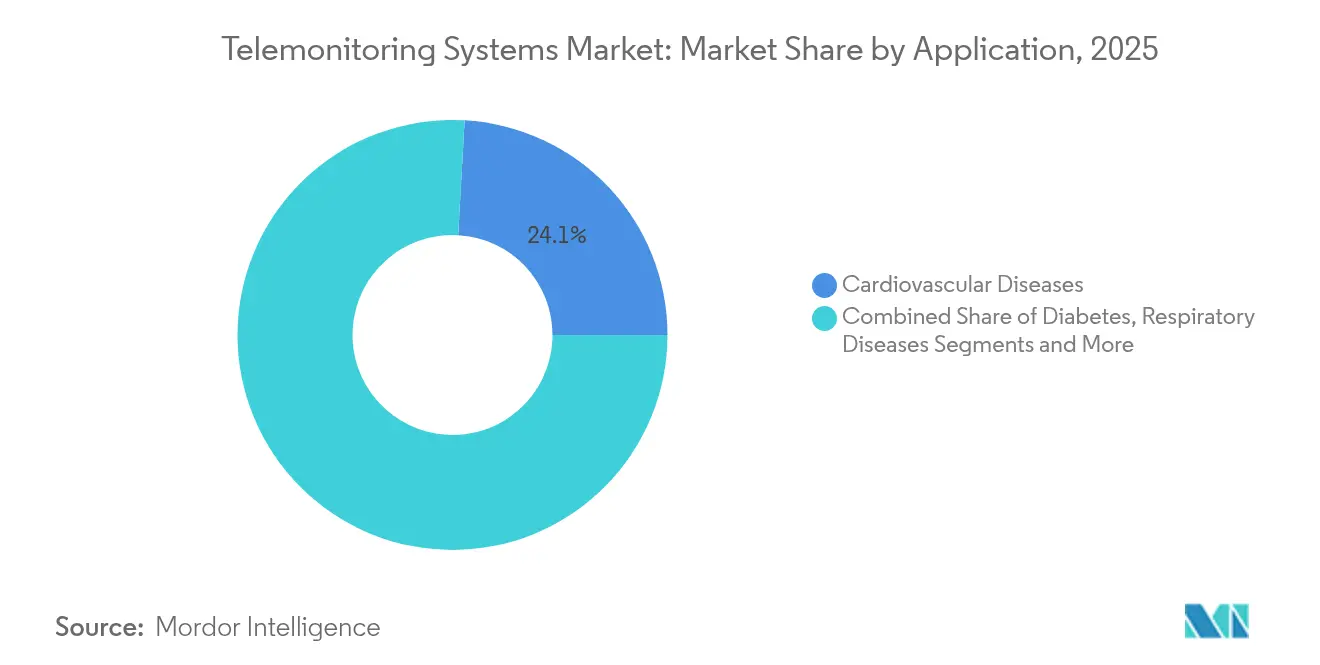

- By application, cardiovascular monitoring captured 24.10% of the telemonitoring systems market size in 2025, whereas diabetes management is advancing at a 15.88% CAGR to 2031.

- By end-user setting, hospitals and specialty clinics maintained 42.66% share in 2025, while home-care environments are set to rise at a 15.42% CAGR over the forecast period.

- By geography, North America dominated with 39.41% market share in 2025; Asia-Pacific is the fastest-growing region, climbing at a 14.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telemonitoring Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Chronic Disease Burden & Ageing Population | + 2.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expansion Of Reimbursement Codes For RPM & Telehealth | + 3.1% | North America primary, EU secondary adoption | Medium term (2-4 years) |

| Tech Advances In Wearables & 5G Connectivity | + 2.4% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Pressure To Cut Readmissions & Hospital Costs | + 2.2% | Global, with early gains in US health systems | Short term (≤ 2 years) |

| Capacity-Driven "Hospital-At-Home" Roll-Outs | + 1.9% | North America & EU, pilot expansion to APAC | Medium term (2-4 years) |

| AI-Powered Predictive Analytics Turns RPM Data Into Billable Insight | + 2.6% | Global, with technology hubs leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic Disease Burden & Ageing Population

An unprecedented rise in multimorbidity and an aging demographic underpin demand for continuous monitoring far beyond traditional clinical walls. Japan illustrates the challenge: 29% of its citizens are already over 65, spurring nationwide digital-health initiatives that position telemonitoring as a workforce-saving solution. The Japanese Society of Ningen Dock’s endorsement of multi-parameter MCG screening underlines clinician confidence in proactive, tech-enabled chronic-disease management. In rural China, education and income shape willingness to adopt telemedicine, suggesting implementation programs must address socioeconomic hurdles to unlock full population health benefits.[2]Yusi Yin, “Factors Influencing the Adoption of Telemedicine Services Among Middle-Aged and Older Patients With Chronic Conditions in Rural China,” BMC Health Services Research, bmchealthservres.biomedcentral.com Chronic-care telemonitoring, costing roughly USD 10 per patient-day versus USD 500 for a hospital bed, gives providers a compelling economic incentive to scale programs.

Expansion of Reimbursement Codes for RPM & Telehealth

CMS’s 2025 Physician Fee Schedule allows providers to layer Advanced Primary Care Management payments on top of existing RPM codes, boosting revenue per enrolled patient. Permanent coverage for audio-only visits and simplified Federally Qualified Health Center billing expands access in low-resource settings. Yet only a dozen US states reimburse Hospital-at-Home under Medicaid, and EU payment policies vary sharply, with Germany and Belgium far ahead of peers in digital-device integration.[3]Tanguy Renault, “Towards Harmonizing Assessment and Reimbursement of Digital Medical Devices in the EU Through Mutual Learning,” Nature Digital Medicine, nature.comClinicians welcome the American Medical Association’s newly added RPM codes, but still face complex documentation rules that can slow scaling.

Tech Advances in Wearables & 5G Connectivity

Standalone 5G medical networks in China illustrate latency-free data transmission, enabling real-time remote procedures such as the world’s first 5G robotic thyroidectomy spanning 1,200 km. Cellular and NB-IoT links are growing at 16.78% CAGR because they function reliably where Wi-Fi falters, an advantage for rural or mobile patients. Closed-loop CGMs—for example Abbott’s FreeStyle Libre 2 Plus paired with Tandem’s insulin pump—exemplify how wearables feed algorithmic dosing to preempt hypoglycemic events.

Pressure to Cut Readmissions & Hospital Costs

US health systems face Medicare penalties tied to avoidable readmissions, pushing executives toward telemonitoring that flags deterioration early, lowers acute events, and reduces length of stay. Early adopters report savings of USD 1,300-1,550 per patient episode through avoided emergency visits and shorter admissions. In Europe, bundled-payment experiments reveal similar gains, reinforcing the move from volume to outcomes-based contracting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural ICT & Broadband Gaps | -1.8% | Global, concentrated in rural US, developing regions | Long term (≥ 4 years) |

| Cyber-Security / Privacy Breaches | -1.2% | Global, with heightened concern in EU under GDPR | Medium term (2-4 years) |

| Clinician Workflow Overload From Raw RPM Data | -1.5% | Global, particularly acute in understaffed health systems | Short term (≤ 2 years) |

| Patchy Non-US Reimbursement & Evidence Thresholds | -1.1% | International markets excluding North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rural ICT & Broadband Gaps

Roughly 3 million Americans living in broadband “deserts” cannot transmit high-resolution sensor data, limiting telemonitoring reach where chronic-disease rates are often highest. Greene County Health System in Alabama, for instance, operates with speeds a tenth of what electronic health records require, forcing nurses to revert to manual vitals checks. Digital inequities also span device ownership and literacy; only 46% of rural households subscribe to fixed broadband versus 67% of urban peers.

Cyber-Security / Privacy Breaches

Continuous data-flow architecture expands the threat surface. GDPR imposes fines up to 4% of global turnover for breaches, forcing EU providers to invest heavily in encryption and zero-trust frameworks. In North America, ransomware attacks on hospital IoT devices have doubled since 2023, leading to downtime that jeopardizes patient safety and erodes trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cardiac Systems Drive Clinical Validation

Cardiac platforms held 30.92% of telemonitoring systems market share in 2025, thanks to well-established reimbursement and FDA-cleared devices such as Abbott’s Assert-IQ, which offers six-year battery life and AI-enhanced arrhythmia detection. Glucose-monitoring devices are projected to expand at 17.02% CAGR, propelled by consumer wellness trends and OTC CGM approvals. This segment’s rise widens the telemonitoring systems market by attracting non-diabetic users keen on metabolic fitness.

Preventive care models are spurring multi-parameter monitors that aggregate ECG, SpO₂, and blood pressure in one wearable, echoing the market’s pivot from single-metric tools to holistic platforms. COPD and hypertension devices fill niche needs but face slower growth until broader clinical guidelines endorse remote management.

By Component: Software Platforms Accelerate Integration

Hardware captured 81.55% revenue in 2025, but software is advancing at a 15.05% CAGR, reflecting the industry’s recognition that data unification and algorithmic insights drive value. Philips’ viQtor integration exemplifies software-centric ecosystems that streamline clinician dashboards. Telemonitoring systems market size for cloud-first analytics modules is expected to grow steadily as AI models mature and payors reimburse decision-support outputs.

Services—from implementation to training—form the glue that binds devices and platforms, ensuring long-term user adoption. GE HealthCare’s CareIntellect uses generative AI to condense cancer patient records, cutting data-retrieval time and underscoring how software reduces cognitive load.

By Connectivity Technology: Cellular Networks Enable Mobility

Bluetooth and BLE retained 35.02% share in 2025 due to energy economy and universal smartphone pairing. Cellular links, however, will notch the fastest 16.21% CAGR because they bypass Wi-Fi dependency, addressing gaps highlighted in broadband-constrained regions. The telemonitoring systems market size tied to cellular modules also benefits from favorable data-only subscription pricing by mobile operators.

The arrival of 5G private networks allows near-instant transfers crucial for imaging and remote interventions, as evidenced by China’s stand-alone deployments. Mesh strategies—combining Wi-Fi, cellular, and LP-WAN—are gaining traction as vendors build redundancy into rural-care solutions.

By Application/Condition: Diabetes Management Accelerates Growth

Cardiovascular monitoring remained dominant, capturing 24.10% of telemonitoring systems market size in 2025, buoyed by evidence that AI-based ECG analytics reduce stroke risk by 45%. Diabetes management is scaling at 15.88% CAGR, driven by automated insulin delivery ecosystems that personalize dosing.

Respiratory-care telemonitoring gains momentum through AI-enabled spirometry and inhaler-adherence sensors, while hypertension platforms integrate with smartwatch BP cuffs, transforming patient self-management. Rising awareness of chronic-kidney disease, oncology survivorship, and post-operative monitoring will open adjacencies for vendors seeking to diversify revenue.

By End-User Setting: Home Care Transforms Healthcare Delivery

Hospitals and specialty clinics retained 42.66% of telemonitoring systems market share in 2025 by embedding RPM into established protocols and electronic records. Yet home-care settings post a 15.42% CAGR, reflecting patient preference for comfort and the CMS Acute Hospital Care at Home waiver’s cost-saving results. Telemonitoring systems industry alliances with home-health agencies are accelerating as value-based contracts reward readmission avoidance.

Long-term-care facilities adopt fall-detection wearables and smart beds to extend staff capacity, whereas ambulatory surgical centers use short-term RPM bundles to prevent post-discharge complications. The Toronto Grace program illustrates scalability, overseeing 16,000 clients with ambitions to reach 30,000, proving remote monitoring is viable at province-wide scale.

Geography Analysis

North America commanded 39.41% of telemonitoring systems market share in 2025 on the back of reimbursement leadership and mature provider networks. CMS data show 31,000 patients treated via Hospital-at-Home since 2020 with lower mortality and spending, reinforcing payor confidence in remote care. Mass General Brigham’s 70-bed capacity demonstrates how large systems leverage telemonitoring to free inpatient beds for higher acuity cases. Enterprise deals between Philips and leading health systems are translating into nationwide rollouts of AI-enabled dashboards.

Asia-Pacific is the fastest-growing territory with a 14.29% CAGR to 2031, supported by proactive digital-health policies. Japan’s 7.29% market expansion underscores how demographic pressure catalyzes technology uptake, whereas China’s 5G private networks create infrastructure readiness for always-on monitoring. Bibliometric analysis reveals China jumped from 10th to 6th in telemedicine publications post-pandemic, reflecting amplified innovation spending.

Europe posts steady growth anchored by the WHO Regional Digital Health Action Plan, with Norway’s AI-assisted teleradiology programs setting benchmarks for cross-border data-sharing. Yet reimbursement fragmentation slows deployment speed. The forthcoming European Health Data Space and HTA regulation aim to harmonize evaluation criteria, which could reduce launch timelines.

Elsewhere, Middle East, Africa, and South America remain nascent but promising. Pilot programs in the United Arab Emirates and Brazil demonstrate viability once regulatory guardrails and broadband build-outs advance.

Regulatory Landscape

Telemonitoring systems sit between medical-device oversight and healthcare reimbursement. In the United States, the regulatory baseline is FDA device classification and clearance, and adoption also depends on Centers for Medicare & Medicaid Services (CMS) payment rules for Remote Patient Monitoring (RPM). CMS implemented CY 2026 Physician Fee Schedule policies effective January 1, 2026, reinforcing how coding and documentation pathways shape provider adoption and vendor go-to-market models. FDA actions in January 2026 that broadened enforcement discretion for certain wearable, sensor-based general wellness products, alongside its TEMPO (Technology-Enabled Meaningful Patient Outcomes) pilot intake activities in early 2026, point to an active policy environment for digital health devices that sit near the wellness-to-medical boundary.

In Europe, regulatory compliance is guided by the EU Medical Device Regulation (MDR 2017/745). Many telemonitoring devices align with Class IIa/IIb expectations and must meet requirements around clinical evidence, post-market surveillance, and economic-operator obligations. A notable 2026 operational milestone is the European Commission mandate that began May 28, 2026, requiring use of four functional EUDAMED modules by economic operators placing medical devices on the EU market, which increases the priority of regulatory data readiness and UDI-linked workflows for multinational telemonitoring portfolios. MDR-related certificate extension mechanisms referenced in the 2026 context reduce near-term withdrawal risk, but they do not remove the need for timely recertification, plus quality-management and cybersecurity controls.

Value Chain Analysis

The telemonitoring systems value chain runs from sensor and electronics inputs (biosensors, ASICs, batteries, substrates), through device OEM design and manufacturing, to connectivity enablement (Bluetooth/BLE, cellular/NB-IoT modules, and carrier services). Software then ingests, normalizes, and presents physiologic data to clinician dashboards. Upstream dependencies on specialized biosensor and MEMS supply, alongside regionally concentrated electronics manufacturing, can introduce lead-time volatility for wearable and home-monitoring hardware. That dynamic encourages OEMs to adopt multi-sourcing and tighter component qualification. As the market shifts from single-metric tools to integrated platforms, interoperability and cybersecurity assurance become gating steps between product development and provider procurement, consistent with security-focused guidance such as NIST NCCoE work on securing telehealth and remote patient monitoring environments.

Downstream, distribution and commercialization are shaped by health-system procurement (including GPO-driven contracting in the United States), public tenders and regional health authorities in Europe, and the expansion of hospital-at-home and home-care channels that bundle device logistics with onboarding and adherence support. Provider buyers increasingly prefer vendors that integrate with EHR workflows and can deliver services that reduce clinician burden from raw data, which elevates the role of implementation partners and clinical staffing and monitoring services within the chain. This has also supported an unbundling trend, as health systems separate device acquisition from remote interpretation and operational services, creating more distinct competitive arenas for device makers, platform vendors, and service operators.

Competitive Landscape

The telemonitoring systems market shows moderate concentration. Philips pairs deep imaging heritage with acquisitions such as smartQare to offer end-to-end ecosystems. Abbott’s portfolio spans cardiac monitors and CGMs, enabling cross-selling and data pooling that strengthen algorithm performance. Boston Scientific differentiates with HeartLogic and Bluetooth-enabled implantables that feed cloud analytics.

Platform players such as Teladoc Health pursue inorganic growth, acquiring Catapult Health and UpLift to widen chronic-condition programs. GE HealthCare invests in AI labs and oncology-centric RPM, signaling a shift from modality sales to subscription analytics. Niche start-ups focus on workflow software and rural connectivity, aiming to license technology to the giants.

Competitive success now hinges on regulatory savvy, payer engagement, and data-science excellence more than on hardware innovation alone. Vendors with clinically validated algorithms, broad device portfolios, and integration APIs will retain pricing power.

Telemonitoring Systems Industry Leaders

Abbott Laboratories

Koninklijke Philips NV

GE Healthcare

Medtronics plc

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale hospital-at-home and home-care programs are creating whitespace for enterprise-grade telemonitoring deployments that combine devices, workflow software, and logistics at regional scale. In May 2026, Philips, together with Cuviva and Vingmed, was selected to support Region Stockholm with hospital-at-home technology designed to cover up to 15,000 patients annually, indicating that public systems are formalizing remote monitoring as a standard layer of care delivery rather than a pilot. Similar scale signals are visible in respiratory and chronic-care pathways, where telemonitoring is being specified in multi-year service contracts, expanding addressable demand for multi-parameter monitoring, escalation workflows, and integrated analytics.

Reimbursement and procurement structures are also broadening the configurations of products and services, especially for shorter-duration monitoring episodes and public-sector buying. In July 2026, CMS proposed 2026 Physician Fee Schedule changes that introduced new codes for remote physiologic monitoring and remote therapeutic monitoring spanning 2 to 15 days of data collection, aligning payment with clinical scenarios that do not follow a full-month monitoring pattern. On the demand side, public procurement remains active, including a February 2026 U.S. Veterans Health Administration delivery order for peripheral equipment supporting remote patient monitoring home telehealth. These signals point to opportunities for vendors that can package flexible-duration programs, demonstrate secure interoperability, and support consortium-based deployments spanning hardware supply, platform integration, and lifecycle services.

Recent Industry Developments

- June 2026: MiniMed expanded its agreement with Abbott to commercialize integrated dual glucose-ketone sensors designed to work with MiniMed smart dosing systems. The initiative tightens interoperability between sensing and automated insulin delivery workflows, supporting more continuous, algorithm-driven monitoring in home settings.

- February 2025: Teladoc Health acquired Catapult Health for USD 65 million to broaden at-home testing and improve enrollment into chronic-condition programs. The deal strengthens Teladoc’s funnel for remote monitoring engagement by combining screening, risk identification, and ongoing virtual care pathways.

- August 2024: Abbott entered a global partnership with Medtronic to connect Abbott’s continuous glucose monitoring systems with Medtronic insulin delivery devices. This ecosystem alignment supports tighter device-to-platform integration and accelerates bundled chronic-disease management offerings that rely on continuous data feeds.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the telemonitoring systems market covers connected medical monitoring solutions that capture patient health readings and transmit them to a clinical team for follow-up or intervention, typically through a secure software platform paired with devices.

Scope exclusions: The sizing excludes general teleconsultation-only services, consumer fitness wearables, and basic emergency alert buttons that do not transmit clinical monitoring data.

Segmentation Overview

- By Product Type

- COPD Telemonitoring Systems

- Glucose Level Telemonitoring Systems

- Cardiac Telemonitoring Systems

- Blood-Pressure Telemonitoring Systems

- Multi-parameter/Other Systems

- By Component

- Devices

- Software Platforms

- Services

- By Connectivity Technology

- Bluetooth / Low-Energy

- Cellular / NB-IoT

- Wi-Fi / WLAN

- Wired

- By Application / Condition

- Cardiovascular Diseases

- Diabetes

- Respiratory Diseases (e.g., COPD, Asthma)

- Other Chronic & Acute Conditions

- By End-User Setting

- Hospitals & Specialty Clinics

- Home-care Settings

- Long-term Care Facilities

- Ambulatory Surgical & Out-patient Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the care settings where telemonitoring is used and to anchor assumptions that are hard to observe directly in a single data source. We reviewed public healthcare statistics and digital health adoption indicators, then cross-checked them with how remote monitoring is coded and reimbursed in practice.

For sizing inputs, we relied on sources such as the Centers for Medicare and Medicaid Services (CMS), the US FDA device databases, the World Health Organization, OECD health statistics, and peer-reviewed clinical and health economics journals that discuss remote monitoring outcomes and utilization patterns. We also used company annual reports, investor presentations, reputable press coverage, and selective paid subscriptions for company financials and patent databases to track product activity and pricing direction. The desk sources referenced are illustrative and not exhaustive, as many other public documents were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through interviews and surveys with hospital and home-care stakeholders, clinical operations teams, device and software channel partners, and reimbursement or payer-side experts across major regions. These discussions helped confirm what gets purchased as a system in routine procurement, how pricing is structured (device, software, and service bundles), and where adoption is accelerating or slowing. The insights were then used to adjust model assumptions and close data gaps where desk indicators were ambiguous.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 22% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 21% | EMEA: 35% |

| Smaller Players: 22% | Managers: 57% | Americas: 23% |

Market-Sizing & Forecasting

We built the market using a top-down approach where remote monitoring demand pools were reconstructed from care setting activity and eligible patient cohorts, then filtered through adoption rates for telemonitoring and typical system attach rates. Since telemonitoring is bought as a mix of devices and software, the model was converted into revenue using blended average selling prices (ASPs) that reflect common bundle structures and contract terms.

Key inputs used to keep the model grounded included chronic disease prevalence signals, hospital-at-home and post-acute monitoring program activity, remote monitoring reimbursement eligibility and coding trends, connectivity readiness for home monitoring, and renewal or replacement cycles for devices and platform licenses. To corroborate the totals, selective bottom-up approximations were also done using supplier revenue disclosures where available, channel feedback on unit volumes, and sampled ASP x volume checks in a few mature markets. When evidence was incomplete, we used conservative ranges and later narrowed them through primary feedback.

For forecasting, scenario analysis was used because policy changes, clinical staffing constraints, and payer coverage can shift adoption quickly in either direction. Assumptions for volume growth and ASP movement were agreed with industry respondents and then applied consistently by region and care setting to produce the forward view.

Data Validation & Update Cycle

Validation was done through triangulation across independent signals, including whether implied device volumes align with known care setting capacity and whether revenue per monitored patient stays within realistic reimbursement and budget boundaries. Outliers were flagged and reviewed in steps, first by checking unit economics and currency conversions, and then by confirming whether the variance is explained by a scope boundary or a timing issue.

Before sign-off, the model and assumptions go through peer review, and follow-up questions trigger selective re-contact with interviewees when a number moves beyond an expected band. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery check is completed so clients receive the most current view.

Mordor Intelligence's Telemonitoring Systems Market Estimate Compared With Other Published Estimates

Published market sizes for telemonitoring systems often do not match because the boundaries of what counts as a system and the timing of pricing assumptions are handled differently. Even a small change in whether service fees are included, or in which year average prices are converted to USD, can shift the total by a noticeable amount.

The biggest gap drivers usually come from how device-plus-platform bundles are treated, whether adjacent remote patient monitoring categories are folded in, and how fast ASPs are assumed to fall as volumes scale. In this study, ASP updates and currency conversion timing are refreshed with late-cycle checks before totals are finalized, which keeps the 2025 value aligned to a consistent pricing window and validation pass, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.14 B (2025) | |

| Industry Research Publisher A | USD 7.26 B (2025) | The estimate appears to apply a broader telemonitoring definition that can pull in wider remote monitoring spending, and it likely uses a higher blended ASP assumption for 2025 with a different currency timing, which lifts the reported value. |

| Global Industry Publisher B | USD 7.20 B (2025) | This figure seems to include a wider set of services around monitoring programs and not only system revenues, and the 2025 pricing may be based on earlier-year list prices rather than updated contract-level mixes, which can inflate the total. |

Looking across the three values, the spread is mainly explained by scope boundaries and how pricing gets translated into a single-year USD number. By tying volumes to realistic monitoring adoption signals and then validating ASPs through interviews and reasonableness checks, the resulting 2025 market size stays traceable to clear steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the projected value of the telemonitoring systems market by 2031?

The market is forecast to reach USD 10.74 billion by 2031, growing at a 13.06% CAGR.

Which product segment currently leads the telemonitoring systems market?

Cardiac telemonitoring systems lead with 30.92% revenue share in 2025.

Why are software platforms the fastest-growing component?

Providers need integrated analytics and AI decision support, driving software to a 15.05% CAGR.

How does reimbursement influence market growth?

CMS’s expanded RPM and Advanced Primary Care Management codes create multiple payment paths, accelerating US adoption.

What geographic region is expanding the quickest?

Asia-Pacific is projected to grow at 14.29% CAGR, boosted by 5G rollouts and supportive digital-health policies.

Page last updated on: