Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

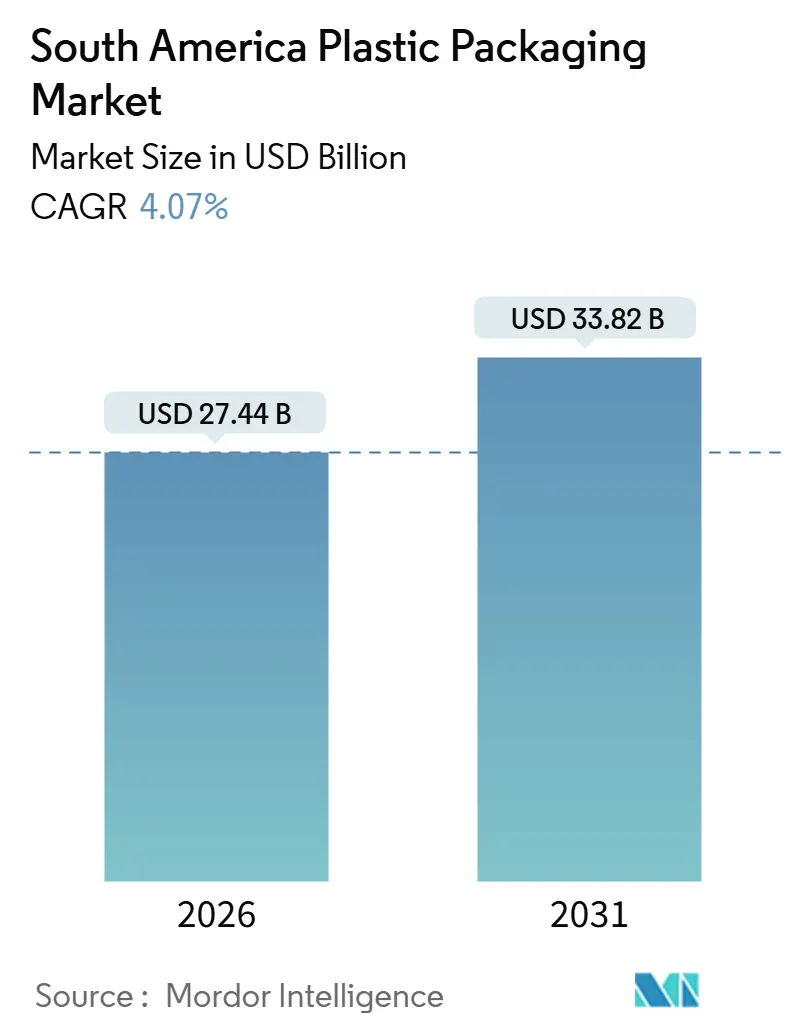

| Market Size (2026) | USD 27.44 Billion |

| Market Size (2031) | USD 33.82 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Plastic Packaging Market Analysis by Mordor Intelligence

The South America plastic packaging market size is estimated at USD 27.44 billion in 2026 and is projected to reach USD 33.82 billion by 2031, representing a 4.07% CAGR over the forecast period. Macro-level demand is driven by rising urban incomes, e-commerce expansion, and food exports; however, margin pressure from extended producer responsibility (EPR) laws is forcing converters to accelerate lightweighting, downgauging, and the integration of recycled content. Flexible formats are gaining ground as parcel carriers charge by volume rather than weight, while rigid containers continue to hold a share in carbonated beverages, dairy products, and bulk chemicals. Nearshoring shifts are redrawing supply chains, with Colombia absorbing spillover assembly work from Mexico and pulling bottle, cap, and label demand southward.

Key Report Takeaways

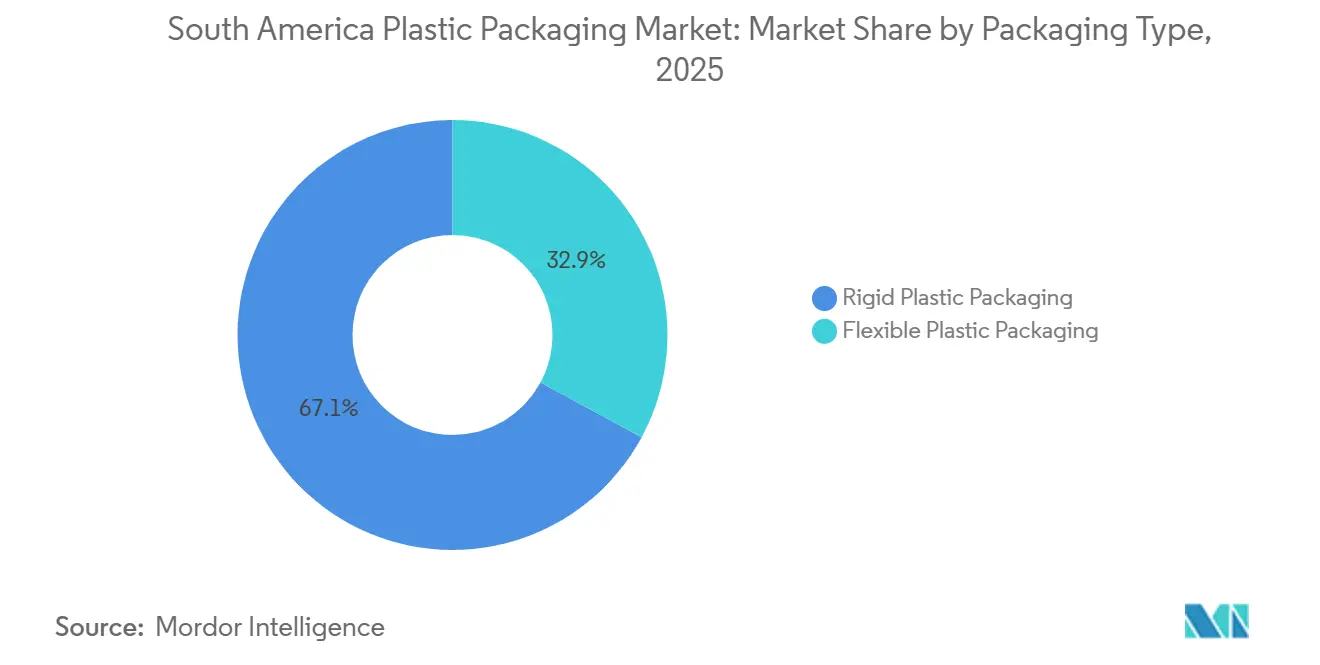

- By packaging type, rigid plastic captured 67.12% of the South America plastic packaging market share in 2025.

- By material, the South America plastic packaging market size for bioplastics is projected to grow at a 5.56% CAGR between 2026-2031.

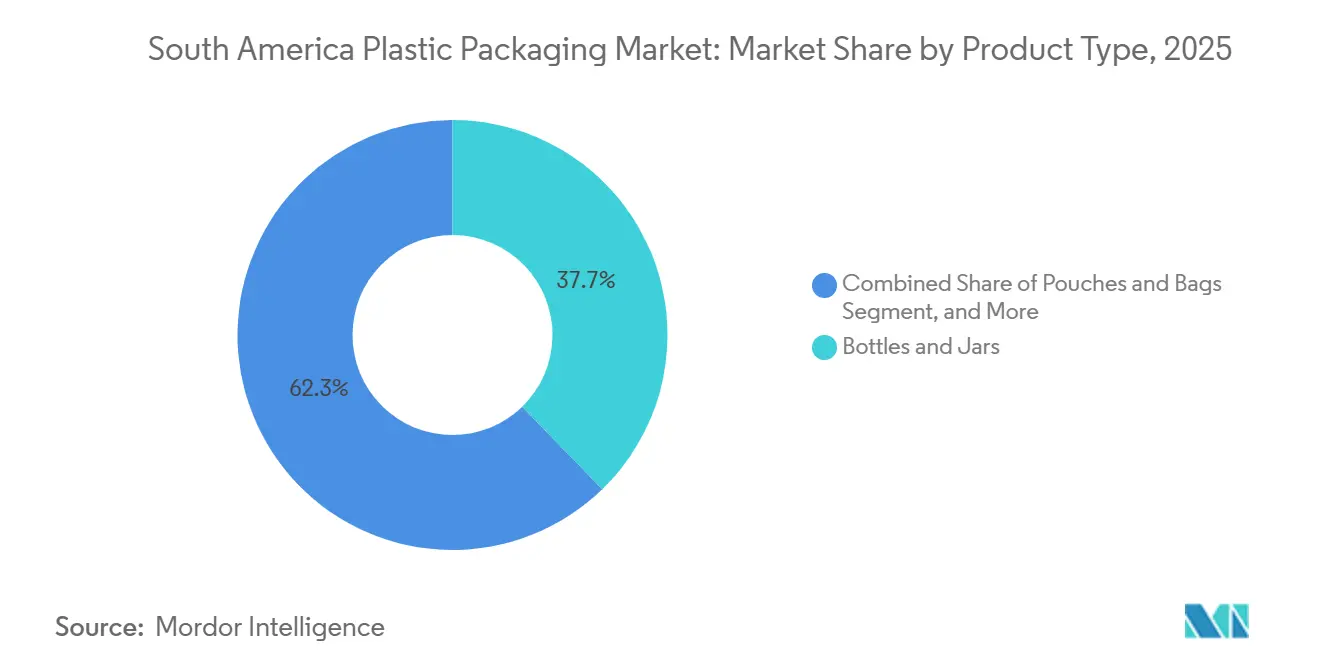

- By product type, bottles and jars captured 37.74% of the South America plastic packaging market share in 2025.

- By end-user, the South America plastic packaging market size for personal care packaging is projected to grow at a 6.21% CAGR between 2026-2031.

- By country, Brazil captured 40.28% of South America plastic packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Convenient and Lightweight Packaging | +0.9% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Rapid Growth of E-Commerce Deliveries in South America | +1.2% | Brazil, Argentina, Colombia, Peru | Short term (≤ 2 years) |

| Expansion of the Food and Beverage Processing Sector | +0.7% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Nearshoring of Consumer Goods Manufacturing to Mexico Accelerating Demand | +0.6% | Colombia, Brazil | Medium term (2-4 years) |

| Government-Supported Tax Incentives for Recycled Content Integration | +0.4% | Brazil, Chile, Uruguay | Long term (≥ 4 years) |

| Emergence of Mono-Material Flexible Films Enabling Local Brand Compliance | +0.3% | Chile, Argentina, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Convenient and Lightweight Packaging

Urbanization is shrinking household meal-prep windows, prompting brands to shift to single-serve pouches, portion-controlled trays, and on-the-go snack packs. Unit volume for condiment pouches surged in Brazil and Colombia in 2024 as retailers expanded grab-and-go shelves. Brand owners who master downgauging can reduce resin usage by up to 15% without compromising barrier performance, thereby trimming both costs and carbon footprint. Braskem demonstrated parity in puncture resistance for its sugarcane-based I’m Green polyethylene at a 20% lower gauge, allowing converters to meet lightweight mandates without costly machinery changes. Flexible laminates that incorporate laser-scored, easy-open features further enhance consumer convenience and improve brand perception.

Rapid Growth of E-Commerce Deliveries in South America

E-commerce penetration in Brazil reached 12% of retail sales in 2024 and is expected to continue tracking higher in Argentina and Colombia, exposing parcels to repeated handling and thereby elevating protective packaging requirements. Mercado Libre disclosed that packaging accounted for 18% of its 2024 fulfillment costs and is piloting reusable polypropylene totes on high-frequency urban lanes, signaling a potential shift away from disposable mailers.[1]Mercado Libre, “Annual Report 2024,” investor.mercadolibre.com Converters supplying bubble wrap, air pillows, and cushioned pouches therefore enjoy volume upside, yet must also prepare for a medium-term pivot toward durable returnable containers that amortize cost over multiple trips.

Expansion of the Food and Beverage Processing Sector

Brazil’s processed-food output expanded 4.2% year-on-year in 2025, with poultry, instant coffee, and fruit concentrates topping export lists. Because long, humid supply chains drive higher moisture-barrier needs, brands historically over-packaged, inflating resin usage. Nestlé’s Brazilian plants consumed 12% more polyethylene per ton of product than their European counterparts. New barrier-coating technologies now deposit nanolayers of aluminum oxide on thinner polyethylene films, yielding equal protection at 30% lower material cost, thus unlocking margin and sustainability gains for early adopters.

Nearshoring of Consumer Goods Manufacturing to Mexico Accelerating Demand

As consumer-goods assembly migrates from Asia to Mexico, component supply is splintering southward. Plastipak’s USD 35 million PET bottle plant in Bogotá supplies Coca-Cola FEMSA and Postobon, slicing lead times to 10 days and freight emissions by 60%. Converters that pair a rapid-prototyping cell near brand headquarters with high-volume lines in Brazil’s petrochemical belt can charge premium prices for agility and geographic redundancy. The South America plastic packaging market, therefore, benefits not only from local consumption but also from cross-border logistics flows that tether Colombia and Brazil to Mexican final-assembly hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulations on Single-Use Plastics and Extended Producer Responsibility | -0.8% | Chile, Uruguay, Colombia, Argentina | Short term (≤ 2 years) |

| Volatility in Raw Material Prices Linked to Crude Oil | -0.6% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Chronic Shortages of Post-Consumer Resin Collection Infrastructure | -0.4% | Argentina, Colombia, Peru | Long term (≥ 4 years) |

| Growing Influence of Zero-Waste Retail Formats in Urban Centers | -0.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on Single-Use Plastics and Extended Producer Responsibility

Chile now bans polystyrene foam containers and requires 30% recycled content in rigid packs by 2026, driving up compliance costs for smaller converters that must buy certified flake at USD 1,200-1,400 per ton. Uruguay’s 2024 EPR decree shifted USD 50-70 million in yearly collection expenditures onto brand owners. Under Brazil’s Decree 12,688, companies face fines of BRL 5,000-50,000 (USD 1,000-10,000) per ton for failing to meet collection targets. These mandates accelerate industry consolidation, favoring suppliers with in-house recycling, chain-of-custody traceability, and reporting infrastructure.

Volatility in Raw Material Prices Linked to Crude Oil

Brent crude oscillated between USD 70 and USD 90 per barrel in 2024, translating into polyethylene spot swings of USD 1,050-1,350 per ton in Brazil. Because pass-through clauses often lag 60-90 days, converters suffer margin compression when resin spikes mid-contract. Braskem invoked force majeure clauses on some long-term agreements after naphtha prices rose 18% sequentially in the third quarter of 2024. Brand owners are responding with take-or-pay deals that secure volume and price ceilings, reducing spot liquidity for smaller processors in the South America plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Formats Edge Ahead

Rigid plastic packaging accounted for 67.12% of 2025 revenue, driven by beverage bottles, food trays, and household-chemical containers that require structural strength and tamper-evident features. The South America plastic packaging market size for rigid formats is expected to rise modestly but cede market share to flexible options growing at a 6.62% CAGR through 2031. E-commerce parcel fees, based on volumetric weight, are prompting detergents and fabric softeners to be packaged in stand-up pouches that fit tightly inside ship-ready boxes. In Brazil’s northeast, last-mile costs can often exceed the value of products for low-density liquids, making flexible packaging the logical choice. Amcor lifted its flexible revenue share to 42% in 2024 after adding rotogravure capacity that prints high-definition graphics on matte films.

Rigid formats still dominate the carbonated drinks and dairy industries, where internal pressure and oxygen barrier requirements exceed current laminate capabilities. PET bottle lightweighting programs reduced the mass of a 500 milliliter bottle from 28 grams in 2020 to 22 grams in 2024 without compromising burst strength. Polypropylene caps, a USD 1.8 billion subsegment, are shifting to tethered designs that comply with Chile’s 2024 litter-prevention rules. As converters tackle downgauging, the South America plastic packaging market continues to balance cost, performance, and regulatory compliance across both rigid and flexible lines.

By Material: Polyethylene Retains Primacy While Bioplastics Gain Traction

Polyethylene held a 43.18% share of the 2025 market thanks to its versatility in films and bottles. The South America plastic packaging market share for polyethylene will erode slightly as bio-based and chemically recycled grades grow faster. Polypropylene follows, with a roughly 28% share, as it is preferred for its high-temperature tolerance in closures and microwave-safe containers. PET captures 18% in high-clarity bottles and trays. Bans on polystyrene foam have driven the use of this resin into single-digit territory, while bioplastics, currently at less than 3%, are projected to post a 5.56% CAGR through 2031. Brazil reduces the import duty on polylactic acid when used in food contact, providing a cost advantage. Braskem’s I’m Green polyethylene achieved carbon-negative status in 2024, sequestering 3.2 tons of CO₂ per ton of resin produced, and now commands a 10-15% premium that global personal-care brands are willing to pay to meet their net-zero pledges.

Mechanical recycling of polypropylene remains limited by mixed-waste streams and melt-flow challenges; however, chemical-recycling pilots in São Paulo convert contaminated PP back into naphtha feedstock, thereby closing the loop for caps and tubs. As recycled-content targets tighten, the South America plastic packaging market is expected to shift toward resin-agnostic strategies, where converters optimize blends of virgin, mechanically recycled, and bio-based polymers based on application, barrier needs, and price spread.

By Product Type: Pouches and Bags Outperform

Bottles and jars accounted for 37.74% of the revenue in 2025 and continue to dominate the market for beverages, condiments, and household chemicals. Yet, pouches and bags, with an 18% share base, will grow at the fastest rate of 5.78% annually to 2031, outpacing other categories. Spouted pouches for fruit juices, energy drinks, and liquid soaps are nibbling away at the market share of aseptic cartons and rigid bottles. Tetra Pak reported a 6% decline in Brazilian volume for its 200 milliliter single-serve line in 2024, following the rise in popularity of stand-up pouches.[2]Tetra Pak, “Market Performance Report Brazil 2024,” tetrapak.com Zipper-reclosable bags for premium coffee and dried fruits command 20-30% price premiums on the shelf. Constantia Flexibles launched a mono-material polyethylene zipper pouch in Chile, eliminating polypropylene zippers and achieving 100% PE construction, which enables collection through existing LDPE streams.

Caps and closures, a 12% subsegment, are migrating from compression-molded HDPE to injection-molded PP with integrated tamper bands and tethered features. Films and wraps, accounting for approximately 11% of the market share, track warehouse automation growth; stretch film demand increases with the addition of each new fulfillment center. The South America plastic packaging market size for films benefits from improved pallet-stability requirements in regional e-commerce hubs.

By End-User: Personal Care Climbs the Value Ladder

Food applications delivered 32.51% of 2025 volumes, reflecting South America’s export orientation in meat, fruit, and processed snacks. Beverages follow at roughly 28%. Personal care is the smallest of the big three at 15% but will outpace all others at a 6.21% CAGR as premium beauty trends sweep Brazil, Colombia, and Chile. Natura reported that 68% of 2024 launches featured refillable or recyclable packs, up from 52% in 2022. Airless pump dispensers double product shelf life and limit the use of preservatives, prompting converters to master precision injection and piston-assembly techniques.

Pharmaceuticals, at 12%, are pivoting to unit-dose blister packs with serialization to combat counterfeits. Gerresheimer introduced a cold-form blister line with inline printing and track-and-trace capabilities at its São Paulo plant in 2024. Household and industrial chemicals, accounting for approximately 13%, rely on HDPE jugs and drums that can withstand aggressive formulations. Across segments, the South America plastic packaging industry increasingly leverages design-for-recycling and refill models to satisfy both regulators and Gen-Z consumers.

Geography Analysis

Brazil contributed 40.28% of 2025 revenue, making it the anchor market in the region. EPR rules now require 25% post-consumer collection by 2026 and 45% by 2030, driving USD 180 million in pledged mechanical-recycling investments from5 Braskem, Amcor, and Sealed Air. E-commerce, which already accounts for 12% of Brazilian retail, drives demand for corrugated polyethylene mailers, air pillows, and stretch film. Mercado Libre’s 14 fulfillment centers consumed an estimated 45,000 tons of flexible packaging in 2024, underlining how last-mile logistics fortify the South America plastic packaging market in its largest economy.

Colombia is expected to deliver the highest national CAGR of 5.84% from 2026 to 2031. Nearshoring has given Bogotá new PET bottle, closure, and label capacity, including Plastipak’s 400 million-unit facility that slashes lead times to 10 days.[3]Plastipak, “Bogotá PET Plant Inauguration,” plastipak.com Colombia’s EPR law establishes a USD 40 million annual collection pool through 2027, leading to curbside pilots in the capital and Medellín. Zero-waste retail is thriving in Chapinero and Usaquén, where more than 120 stores now sell refillable household chemicals and bulk cosmetics, reducing sachet demand while creating opportunities for reusable rigid packaging.

Argentina and Chile, which together represent a roughly 30% share, are spearheading the adoption of mono-material flexible packaging. Chile’s ban on polystyrene foam and its 30% recycled-content rule for rigid packs by 2026 impose fines of CLP 10-100 million (USD 11,000-110,000) per infraction. AluPak consequently launched a plasma-coated mono-PE pouch that matches the performance of a foil laminate barrier without compromising recyclability. Argentina’s triple-digit inflation prompts consumers to opt for smaller pack sizes and refill pouches, which help keep shelf prices within psychological limits.

Competitive Landscape

The top five suppliers, Amcor, Braskem, Sealed Air, Sonoco, and Plastipak, control 35-40% of revenue, indicating moderate concentration. Global incumbents are expanding recycled-content capacity in Brazil’s São Paulo corridor while setting up satellite plants in Colombia and Chile to chase nearshoring demand. Amcor’s digital flexographic presses cut setup time from four hours to 45 minutes, enabling economical 5,000-unit runs for regional promotions. Sealed Air’s bubble-on-demand machines, installed in eight Mercado Libre centers, shaved packaging cost per parcel by 18% and void fill by 35%.

Regional challengers such as AluPak and Altopro thrive on short lead times, custom printing, and low minimum runs in secondary cities. Sonoco’s 60% stake in Conitex Sonoco, announced in May 2024, provides it with rotogravure capacity in Brazil’s northeast, enabling it to serve food brands within three weeks. Technology adoption from inline spectroscopic quality control to simulation-based lightweighting defines competitive advantage as much as scale.

Compliance credentials matter too: Unilever and Nestlé require all regional suppliers to achieve ISO 14001 and sign the Ellen MacArthur Foundation’s New Plastics Economy pledge by 2026. Companies that cannot document a chain of custody for recycled content risk being dropped from preferred supplier lists, underscoring a secular shift toward data-rich, circular economy-ready operations within the South America plastic packaging market.

South America Plastic Packaging Industry Leaders

-

Amcor plc

-

Sonoco Products Company

-

Gerresheimer AG

-

Sealed Air Corporation

-

Huhtamäki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its merger with Berry Global, creating a multiformat packaging leader; FY25 sustainability report details progress on recycle‑ready flexibles (AmPrima, AmLite) and circularity commitments impacting Latin America supply, specs, and PCR sourcing.

- March 2025: Aptar highlighted expanded consumer dispensing and beauty packaging capabilities (airless pumps, closures) across global sites; continued solution rollouts are pertinent for Brazilian and Andean personal care pack owners shifting to premium plastic dispensing.

- February 2025: Huhtamaki launched ProDairy recyclable single-coated paper cups (polymer content <10%) for yogurt/dairy applications. While manufactured in Europe, the format signals plastic-light cup options relevant for Latin American FMCG portfolios.

- January 2025: TOPPAN Holdings agreed to acquire Sonoco’s Thermoformed and Flexible Packaging (TFP) business, combining Sonoco’s North and South American customer base with TOPPAN’s packaging expertise; closing expected in H1 2025, implications for Brazilian flexible packaging supply and lead times.

South America Plastic Packaging Market Report Scope

The South America Plastic Packaging Market refers to the regional industry focused on the production, distribution, and consumption of plastic-based packaging solutions for various sectors such as food and beverage, pharmaceuticals, personal care, household products, and industrial goods. This market encompasses a wide range of packaging formats and technologies designed to protect products, ensure convenience, and support branding.

The South America Plastic Packaging Market Report is Segmented by Packaging Type (Rigid Plastic Packaging, Flexible Plastic Packaging), Material (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene and Expanded Polystyrene, Bioplastics), Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Pouches and Bags, Films and Wraps), End-User (Food, Beverage, Personal Care, Pharmaceuticals, Household and Industrial Chemicals), and Geography (Brazil, Argentina, Chile, Colombia, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Packaging Type

| Rigid Plastic Packaging |

| Flexible Plastic Packaging |

By Material

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and Expanded Polystyrene (PS and EPS) |

| Bioplastics |

By Product Type

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Pouches and Bags |

| Films and Wraps |

By End-User

| Food |

| Beverage |

| Personal Care |

| Pharmaceuticals |

| Household and Industrial Chemicals |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Packaging Type | Rigid Plastic Packaging |

| Flexible Plastic Packaging | |

| By Material | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and Expanded Polystyrene (PS and EPS) | |

| Bioplastics | |

| By Product Type | Bottles and Jars |

| Trays and Containers | |

| Caps and Closures | |

| Pouches and Bags | |

| Films and Wraps | |

| By End-User | Food |

| Beverage | |

| Personal Care | |

| Pharmaceuticals | |

| Household and Industrial Chemicals | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America plastic packaging market?

The market is valued at USD 27.44 billion in 2026 and is forecast to reach USD 33.82 billion by 2031.

Which packaging type is growing fastest in South America?

Flexible plastic packaging is expected to rise at a 6.62% CAGR through 2031, driven by e-commerce parcel growth and logistics cost savings.

How do EPR laws affect plastic packaging suppliers?

New regulations in Brazil, Chile, and Uruguay transfer collection costs to brand owners, favor suppliers with in-house recycling, and accelerate consolidation.

Which country will post the highest growth in demand?

Colombia is projected to grow at a 5.84% CAGR, thanks to nearshoring and the addition of new bottle, cap, and label capacity.

Why are bioplastics gaining traction in the region?

Tax incentives, carbon-negative credentials of sugarcane-based polyethylene, and brand sustainability pledges are driving a 5.56% CAGR for bioplastics through 2031.

What competitive advantages help regional converters win contracts?

Short lead times, small minimum order quantities, custom printing, and documented recycled-content chain-of-custody increasingly tilt decisions toward agile local players.

Page last updated on: