Smart Home Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

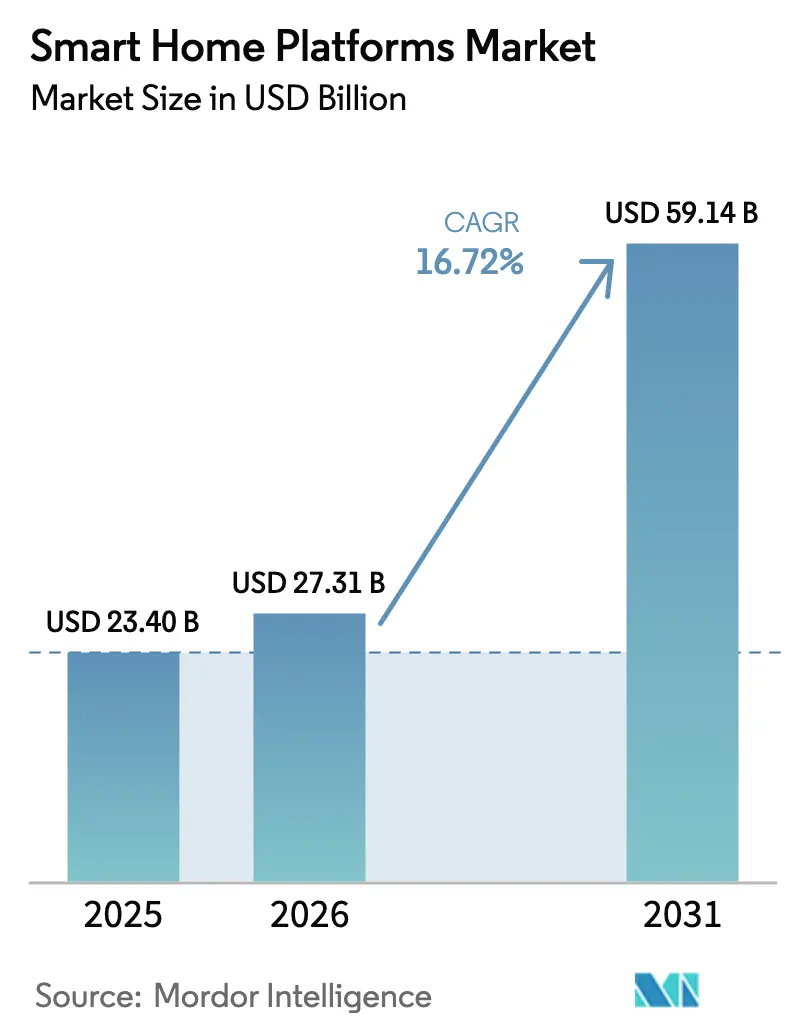

| Market Size (2026) | USD 27.31 Billion |

| Market Size (2031) | USD 59.14 Billion |

| Growth Rate (2026 - 2031) | 16.72% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Home Platforms Market Analysis by Mordor Intelligence

Smart home platforms market size in 2026 is estimated at USD 27.31 billion, growing from 2025 value of USD 23.4 billion with 2031 projections showing USD 59.14 billion, growing at 16.72% CAGR over 2026-2031. Growth reflects a decisive shift from device silos to unified ecosystems that run on the matter standard, now backed by more than 200 vendors. Telecom-driven subscription bundles, hybrid-work preferences that elevate home-office requirements, and steep energy costs in Europe and Japan continue to broaden the customer base for the smart home platforms market. Rising privacy awareness is steering product design toward edge-enhanced architectures, while government incentives for efficient housing upgrade adoption across key regions. Competitive intensity remains high as global giants battle niche specialists for control of the connected-home experience.

Key Report Takeaways

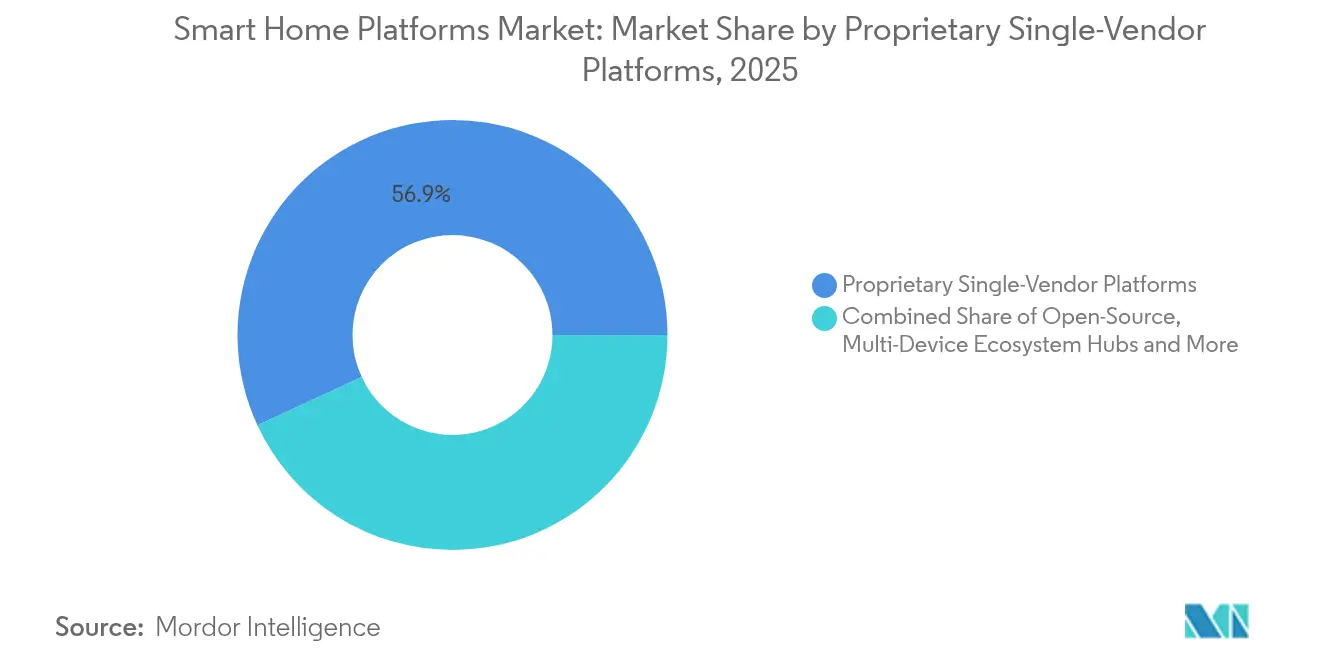

- By platform type, proprietary single-vendor platforms held 56.90% revenue share in 2025 in the smart home platform market, whereas open-source platforms are forecast to grow at an 18.05% CAGR through 2031.

- By communication technology, Wi-Fi led with 45.30% of smart home platforms market share in 2025, while thread and matter is projected to expand at a 23.10% CAGR.

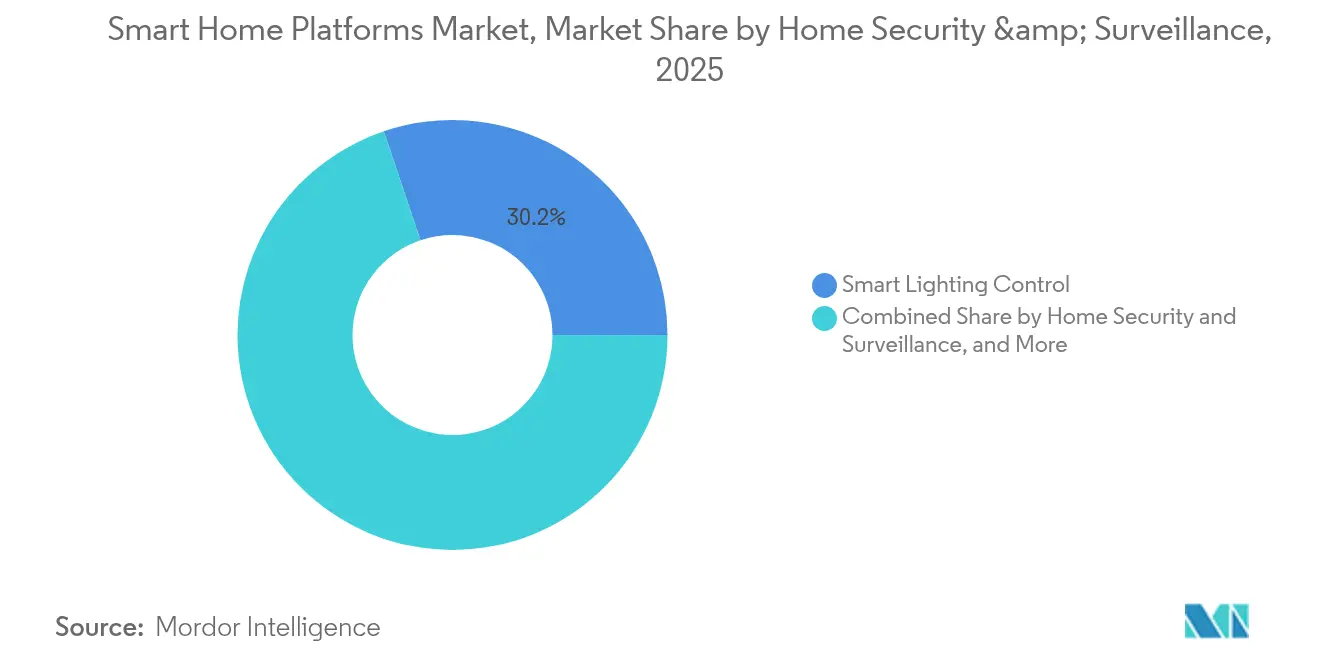

- By application, home security and surveillance commanded 30.10% of market share in the smart home platforms market in 2025, yet wellness and assisted living is set to rise at a 20.20% CAGR.

- By deployment model, cloud-based solutions accounted for 81.00% share of the smart home platforms market size in 2025; On-prem edge/local solutions are advancing at a 19.10% CAGR.

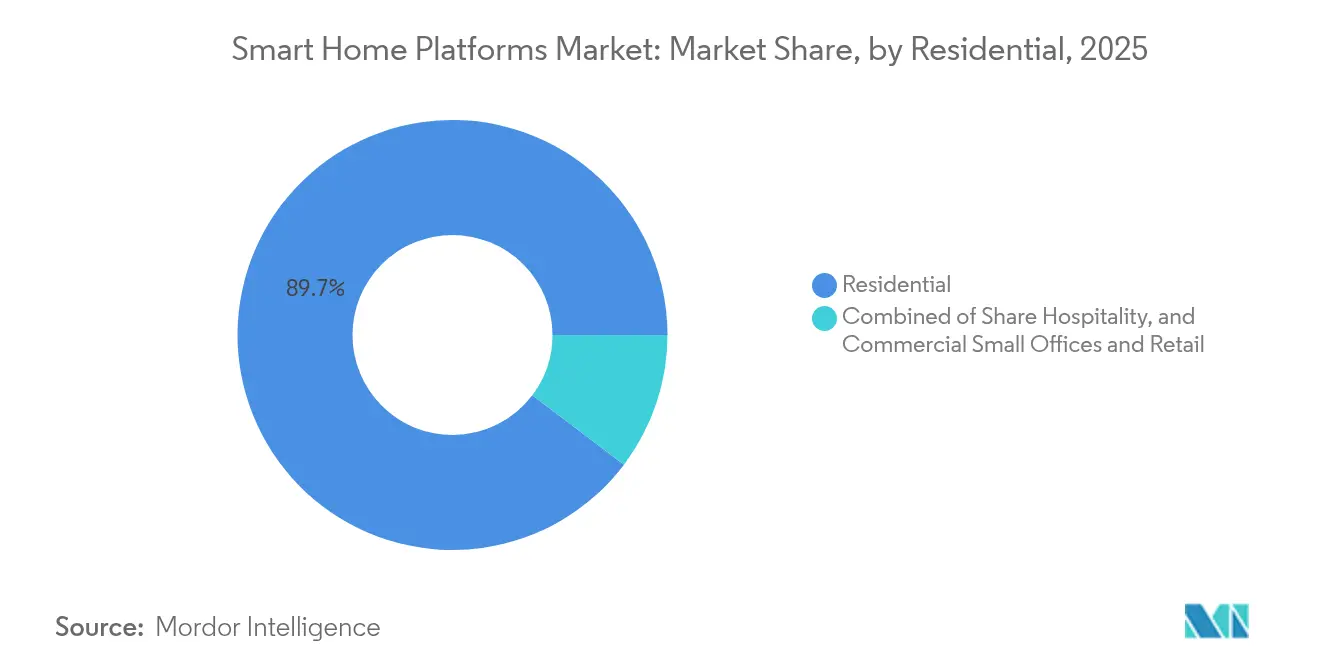

- By end-user, the residential segment represented 89.70% share in 2025, while hospitality is the fastest-growing cohort at a 16.95% CAGR in the smart home platform market.

- By sales channel, E-commerce and marketplaces captured 36.20% share in 2025, but telecom/ISP bundled services are rising quickest at 22.30% CAGR in the smart home platform market.

- Regionally, North America dominated with a 39.60% share in 2025, whereas the Middle East and Africa is forecast to post a 13.75% CAGR to 2031 in the smart home platform market..

- Amazon, Google, Apple, Samsung, and Comcast jointly controlled significant market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Home Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Matter Interoperability Standard Accelerating Ecosystem Convergence in North America and Europe | +4.5% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Telecom and ISP Bundling of Smart-Home Subscriptions Driving Platform Penetration Across Asia's Urban Middle Class | +3.8% | Asia-Pacific, with early adoption in China, Japan, South Korea | Short term (≤ 2 years) |

| Aging Population in Europe Boosting Demand for Remote Wellness and Assisted-Living Platforms Integrated with Healthcare Services | +3.2% | Europe, with strongest impact in Germany, Italy, France | Long term (≥ 4 years) |

| Rising Energy Prices in Europe and Japan Fueling Smart Energy-Management Platform Installations | +2.9% | Europe and Japan | Medium term (2-4 years) |

| Post-Pandemic Hybrid-Working Preference Increasing Demand for Integrated Home-Office Automation Solutions in North America | +2.1% | North America | Short term (≤ 2 years) |

| Government Incentives for Residential Energy-Efficiency Retrofits Subsidising Smart HVAC Platform Adoption | +1.8% | Global, with strongest impact in EU, UK, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of Matter interoperability standard accelerating ecosystem convergence

Matter is removing compatibility walls that once slowed the smart home platforms market. Devices now discover and link locally, bypassing cloud gateways for lower latency and sturdier privacy. The December 2024 release of Matter 1.4 added Wi-Fi routers, heat pumps, and solar panels, setting up whole-home energy orchestration. With cross-platform functionality top-of-mind for buyers, vendors must out-innovate rather than lock in users. Matter’s distributed compliance ledger further builds trust among Europe’s privacy-focused consumers.

Telecom and ISP bundling of smart-home subscriptions driving platform penetration

Communications providers now weave connected-home services into broadband contracts, cutting upfront costs and providing installation. Taiwan Mobile’s “Smarter Home” suite illustrates the model’s pull in urban Asia. Telcos recast themselves as digital life managers, and hardware brands are under pressure to partner or lose channel relevance. Early successes are spurring similar packages in Europe and Latin America, reshaping the smart home platforms market’s route-to-consumer strategies.

Aging population in Europe boosting demand for remote wellness and assisted-living platforms

Demographics turn Europe into a test bed for health-centric connected homes. Integrated systems blend motion sensors, fall detection, and vitals monitoring into secure portals that link seniors, caregivers, and clinicians. Adoption hinges on value clarity and affordability; platforms simplify interfaces for older adults while navigating stricter medical-data privacy rules. The focus on quality of life and hospital-stay reduction fuels a 20.9% CAGR in wellness solutions, making them a top growth lever for the smart home platforms market.

Rising energy prices in Europe and Japan fueling smart energy-management platform installations

Utility bills at multiyear highs shift energy management from nice-to-have to must-have. AI-driven controllers learn usage patterns and auto-shift loads to low-tariff periods. When paired with rooftop solar, batteries, and demand-response incentives, households become grid assets. Governments subsidize retrofit projects, speeding adoption and knitting the smart home platforms market into broader smart-grid initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and GDPR-Compliance Complexities Limiting Cloud-Based Platform Uptake in EU | -2.3% | European Union | Medium term (2-4 years) |

| Fragmented Connectivity Protocols in Emerging Markets Increasing Integration Costs for Platform Vendors | -1.9% | Asia-Pacific (excluding developed markets), Latin America, Africa | Short term (≤ 2 years) |

| High Up-Front Hardware Costs Restraining Adoption in Price-Sensitive Latin-American Households | -1.4% | Latin America | Medium term (2-4 years) |

| Limited Professional-Installer Network Hindering Large-Scale Deployment in Middle East and Africa | -1.1% | Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and GDPR-compliance complexities limiting cloud-based platform uptake

Europe’s rules mandate explicit consent, purpose limitation, and minimal data collection. Cloud models reliant on constant telemetry must redesign around edge processing and personal data stores, stretching small-vendor resources and narrowing competitive diversity. Privacy-by-design principles are now baseline requirements rather than differentiators within the smart home platforms market.

High up-front hardware costs restraining adoption in price-sensitive South American households

Comprehensive smart home kits often equal several months of household income. Currency swings and import duties inflate international brands’ prices, driving interest in local low-cost alternatives. Modular kits that let users add devices over time are gaining favor, yet adoption lags until prices align with regional purchasing power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Open-source gains pace while proprietary retains lead

Proprietary ecosystems controlled 56.90% of 2025 revenue. The smart home platforms market size for these offerings reflects polished UX and tightly curated devices. Open-source alternatives, however, are scaling at an 18.05% CAGR as technically inclined users seek flexibility and local control. Hybrid approaches now emerge—brands preserve signature user flows yet expose Matter APIs for third-party devices.

Open-source communities such as Home Assistant add integrations at rapid cadence, positioning themselves for enthusiasts and professional installers alike. Proprietary giants respond with deeper voice assistance, security layers, and subscription services. As interoperability expands, platform differentiation pivots toward AI-powered automations, data privacy assurances, and cross-vertical partnerships—hallmarks that set future winners in the smart home platforms industry.

By Communication Technology: Thread and Matter upend legacy protocols

Wi-Fi retained a 45.30% share in 2025 due to near-universal household presence. Still, thread and matter are charging ahead at a 23.10% CAGR, boosting mesh resilience and battery life. Multiprotocol hubs featuring dual radios smooth the migration path, maintaining backward compatibility while nudging consumers to IP-native stacks.

Upcoming Wi-Fi 6 and Wi-Fi 7 iterations mitigate congestion, supporting security cameras and high-bandwidth streams. Bluetooth low energy keeps a niche for mobile provisioning, yet Zigbee and Z-Wave face declining shipments. Cellular NB-IoT services secure use cases that require off-premise reach, such as perimeter sensors in vacation properties. As a result, the smart home platforms market evolves toward mixed-protocol homes under a single Matter-driven application layer.

By Application: Wellness and assisted living overtake security in growth momentum

Security and surveillance still led with 30.10% of 2025 spend, but wellness platforms tied to remote care are the fastest climbers. The smart home platforms market share for security remains defendable, buoyed by AI video analytics and biometric locks. Yet, aging-in-place solutions show higher user-reported satisfaction and stickiness, driving ecosystem expansion into health data management.

Energy-saving HVAC controls rise alongside soaring utility rates, and smart lighting remains the entry gateway for first-time users seeking immediate convenience. Multi-domain orchestration—where a fall alert triggers pathway lighting and unlocks doors for responders—shows how platform value compounds across categories, strengthening retention in the smart home platforms market.

By Deployment Model: Edge architectures challenge cloud primacy

Cloud-based products account for 81.00% of active systems. Nevertheless, privacy mandates and latency demands are pushing a 19.10% CAGR for on-prem edge deployments. Consumers gain faster response times, offline resilience, and reduced data exposure. Vendors combine local inference for sensitive triggers with cloud analytics for pattern recognition and firmware updates, creating balanced hybrid stacks.

Edge momentum spurs demand for compact AI accelerators, driving semiconductor design wins and new partnerships in the smart home platforms market. Larger providers bundle premium privacy tiers that process all personal video onsite, targeting European and enterprise clients subject to strict compliance.

By End-User: Hospitality adopts connected-room blueprints

Residential spaces account for 89.70% of 2025 shipments, yet hotels and vacation rentals expand at 16.95% CAGR. Platforms now store guest preferences in the cloud, recalling them across properties. Property managers automate energy-saving modes during vacancies, lowering utility bills and maintenance costs. Among residences, multi-family developers embed whole-building connectivity into standard amenities, elevating renter appeal.

Luxury homeowners pay for artisan-grade interfaces and voice-activated scenes, whereas mainstream buyers prefer incremental starter kits. The split allows tiered pricing strategies within the smart home platforms industry, ensuring broader reach without diluting premium margins.

By Sales Channel: Telecom bundles rewrite go-to-market math

E-commerce represented 36.20% of the 2025 volume, yet telecom bundles outpace all at 22.30% CAGR. Spreading hardware cost over service contracts cancels sticker shock and provides turnkey installation. OEM web stores still engage loyal followers, but must enhance experiential retail to match telco convenience. Professional integrators pivot to complex jobs—luxury villas, boutique hotels, and mixed-use developments—where expertise commands fees.

As telcos vie for household share of wallet, contract-based models generate predictable revenue for platform vendors while lowering churn for network operators. This symbiosis is cementing telecoms as central gatekeepers of the smart home platforms market.

Geography Analysis

North America controls 39.60% of revenue and sets usage trends that meld work, leisure, and energy management into single dashboards. U.S. adoption accelerates through Matter-compatible launches from top brands and strong broadband penetration. Canada’s colder climate heightens interest in learning thermostats and window insulators, while Mexico’s rising middle class benefits from fiber rollouts that unlock more sophisticated device ecosystems. Stateside competition features Big Tech vendors expanding subscription services, yet region-specific entrants thrive in security and HVAC niches.

Asia-Pacific encapsulates extremes—from South Korea’s gigabit apartments to rural India’s mobile-only households. Japan, Singapore, and South Korea enjoy mature ecosystems, often coordinated by telecom bundles. China’s domestic champions deliver feature-rich kits at lower prices, challenging multinational incumbents and exporting to Southeast Asia. Emerging economies, constrained by sporadic fixed networks, rely on cellular backhaul and super-apps for device control, sculpting a unique flavor to the smart home platforms market across the region.

Europe stays on a steady growth path thanks to proactive energy policies and demographic aging. The United Kingdom leads adoption in security, while Germany focuses on energy optimization. France and Italy implement assisted-living pilots to care for aging citizens. GDPR drives strong demand for on-prem solutions, and national retrofit grants speed installation of smart HVAC and lighting. The Middle East and Africa, though nascent, posts a 13.75% CAGR due to luxury developments in the Gulf and rising urban tech readiness in South Africa. Limited installer capacity and import tariffs temper rollout pace, yet government smart-city blueprints are carving future demand paths.

Competitive Landscape

Dominated by Amazon, Google, Apple, Samsung, and Comcast—collectively holds significant market share—the smart home platforms market exhibits high concentration. These firms wield scale benefits: mass-market hardware lines, cloud assets, and large R&D budgets. Each embeds AI engines that transform platforms from command-response layers into anticipatory services.

Mid-tier contenders find success in vertical slices. Edge-only hubs emphasize privacy for GDPR-sensitive customers. Rental-property platforms offer landlord dashboards for keyless entry and energy cycling. Wellness start-ups integrate medical-grade sensors, seeking certification advantages. Intellectual property battles intensify as companies patent machine-learning pipelines for occupancy detection and secure onboarding (e.g., US9412248B1), protecting moats around differentiated features.

Strategic plays in 2025 highlight energy orchestration and multimodal displays. Samsung’s Flex Connect balances appliance loads against grid signals, courting utility alliances. Apple’s FaceTime-enabled home display expands ecosystem stickiness within privacy-centric boundaries. Amazon penetrates safety niches with branded detectors, while Google rejuvenates Nest around Matter-native APIs. The surge of user-installable batteries and demand-response firmware underscores a pivot to resilience and sustainability as decisive purchase factors.

Smart Home Platforms Industry Leaders

Amazon.com Inc.

Alphabet Inc. (Google LLC)

Apple Inc.

Samsung Electronics Co. Ltd.

Comcast Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amazon introduced an Alexa-integrated CO + smoke detector, broadening its safety hardware line.

- April 2025: Apple launched a smart-home display with FaceTime and Matter control, expanding HomeKit’s reach.

- March 2025: Samsung unveiled SmartThings Flex Connect to coordinate appliance energy use with grid conditions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the smart home platforms market as the global revenue earned by software-centric and cloud-enabled control layers that integrate, automate, and remotely manage connected household devices, lighting, HVAC, security, entertainment, and kitchen through a single application, voice assistant, or hub. The model tracks license fees, subscription income, and embedded platform royalties paid by device makers rather than the sale of stand-alone hardware.

Scope exclusion: Sales of single-purpose smart speakers, cameras, or thermostats that lack an open application program interface remain outside the numbers.

Segmentation Overview

- By Platform Type

- Proprietary Single-Vendor Platforms

- Open-Source Platforms

- Multi-Device Ecosystem Hubs

- DIY App-Centric Platforms

- By Communication Technology

- Wi-Fi

- Bluetooth and BLE

- Zigbee

- Z-Wave

- Thread and Matter

- Cellular / NB-IoT

- Others

- By Application

- Smart Lighting Control

- Home Security and Surveillance

- HVAC and Energy Management

- Home Entertainment and Infotainment

- Smart Kitchen and Appliances

- Wellness and Assisted Living

- Others

- By Deployment Model

- Cloud-Based

- On-Prem Edge / Local

- By End-User

- Residential

- Hospitality

- Commercial Small Offices and Retail

- By Sales Channel

- Direct OEM

- E-Commerce and Marketplaces

- Professional Installer / Integrator

- Telecom / ISP Bundled Services

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chipset vendors, voice-assistant product managers, broadband bundle teams, and professional installers across North America, Europe, and Asia. These discussions filled gaps on active-user churn, hub attach rates, and emerging interoperability pain points, letting us recalibrate assumptions before final sign-off.

Desk Research

We began with public datasets from the International Telecommunication Union, US Energy Information Administration, Eurostat, China Academy of Information and Communications Technology, and the Broadband Forum, which describe household connectivity, electricity prices, and internet penetration shaping platform uptake. Company filings, investor decks, and respected trade publications revealed disclosed subscriber counts, tariff structures, and standards roadmaps. Paid resources such as D & B Hoovers and Dow Jones Factiva provided historical financials and news flow that anchor trend baselines. This list is illustrative; many other sources helped validate and clarify findings.

A second pass mapped policy and standards material, including Matter 1.2 specifications and regional data privacy rules, which guide geographic breakouts prepared by Mordor analysts. Together, these inputs outline the total addressable connected home base, platform pricing corridors, and technology mix for every region we cover.

Market-Sizing & Forecasting

We apply a top-down build that starts with connected home households by country and multiplies platform penetration and average subscription spend to size revenue pools. Then we corroborate results with selective supplier roll-ups of active accounts and service prices. Key variables include broadband household growth, Matter-enabled device shipments, installed voice-assistant base, real electricity prices, and telecom bundle adoption. A multivariate regression projects each driver to 2030, while scenario analysis adjusts for tariff shocks or standards delays. Weighted averages from primary interviews bridge gaps where disclosures are partial.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that compares anomalies with independent benchmarks and, when needed, triggers fresh expert callbacks. Reports refresh each year, and interim updates follow major mergers, standards releases, or tariff shifts so clients receive the most current view.

Why Mordor's Smart Home Platforms Baseline Commands Confidence

Published estimates often diverge because firms choose different product baskets, pricing assumptions, currency bases, and refresh cadences. Our disciplined scope and annual household-level rebuild make Mordor's baseline dependable.

Key gap drivers: Some publishers mix device revenue with platform fees, others model only voice-assistant software, and a few extrapolate outdated tariffs without primary validation, which inflates or deflates values versus our figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.40 B (2025) | Mordor Intelligence | - |

| USD 23.45 B (2025) | Global Consultancy A | Subscriber fees sourced only from public news, limited expert checks |

| USD 84.50 B (2024) | Industry Publisher B | Combines hardware sales with platforms and uses a single scenario forecast |

These comparisons show that Mordor's transparent variable selection, primary-backed assumptions, and yearly refresh deliver a balanced, traceable baseline decision makers can trust.

Key Questions Answered in the Report

How large is the smart home platforms market today?

The market is valued at USD 27.31 billion in 2026 and is expected to advance to USD 59.14 billion by 2031.

Which platform category is growing most quickly?

Open-source platforms lead growth at an 18.05% CAGR as users seek flexibility and independence from single-vendor lock-in.

Why is Thread and Matter adoption accelerating?

Thread and matter resolve device-compatibility issues, improve mesh reliability, and support IP-native communications, driving a 23.10% CAGR for this protocol group.

What role do telecom bundles play in adoption?

Telecom/ISP bundles lower upfront costs and provide turnkey installation, expanding market reach at a 22.30% CAGR, especially in dense Asian cities.

How does edge computing influence platform choices?

Edge deployments process data locally for faster response and stronger privacy, growing at 19.10% CAGR as regulations and user concerns intensify.

Page last updated on: