Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

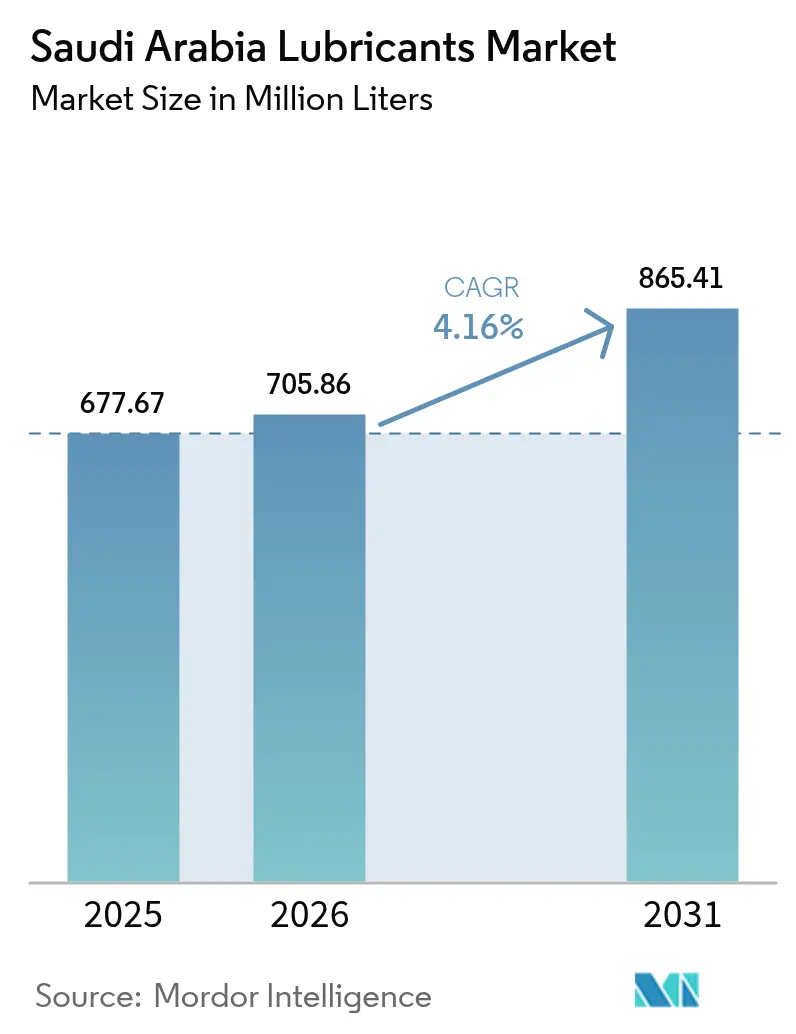

| Base Year Market Size (2025) | 677.67 Million Liters |

| Market Volume (2026) | 705.86 Million Liters |

| Market Volume (2031) | 865.41 Million Liters |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

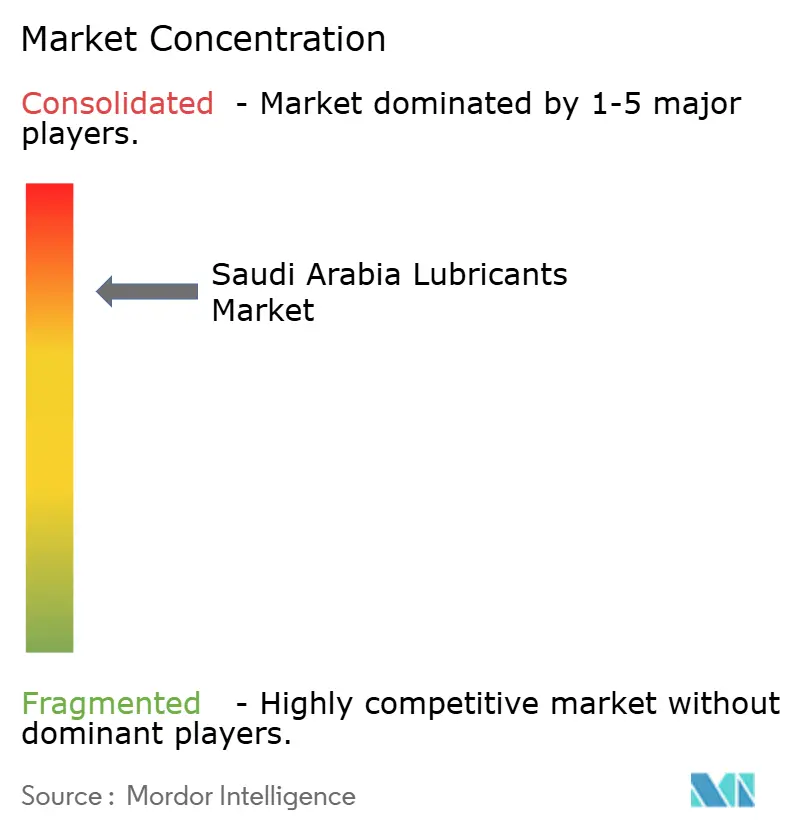

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Lubricants Market Analysis by Mordor Intelligence

The Saudi Arabia Lubricants Market size was valued at 677.67 Million Liters in 2025 and estimated to grow from 705.86 Million Liters in 2026 to reach 865.41 Million Liters by 2031, at a CAGR of 4.16% during the forecast period (2026-2031). Solid demand stems from Vision 2030-driven industrial projects, steady vehicle-parc expansion, and large-scale power-generation investments. Consolidation moves such as Saudi Aramco’s Valvoline acquisition and a potential Castrol bid add technological depth while deepening domestic value-chain integration. Growth is also enabled by localization initiatives like Luberef’s LubeHUB, which reduces import dependencies for base oils and additives. Meanwhile, the shift toward low-SAPS synthetics, rapid digitalization of distribution, and rising consumption in petrochemical hubs sustain positive volume momentum even as electric-vehicle (EV) adoption begins trimming long-term engine-oil demand.

Key Report Takeaways

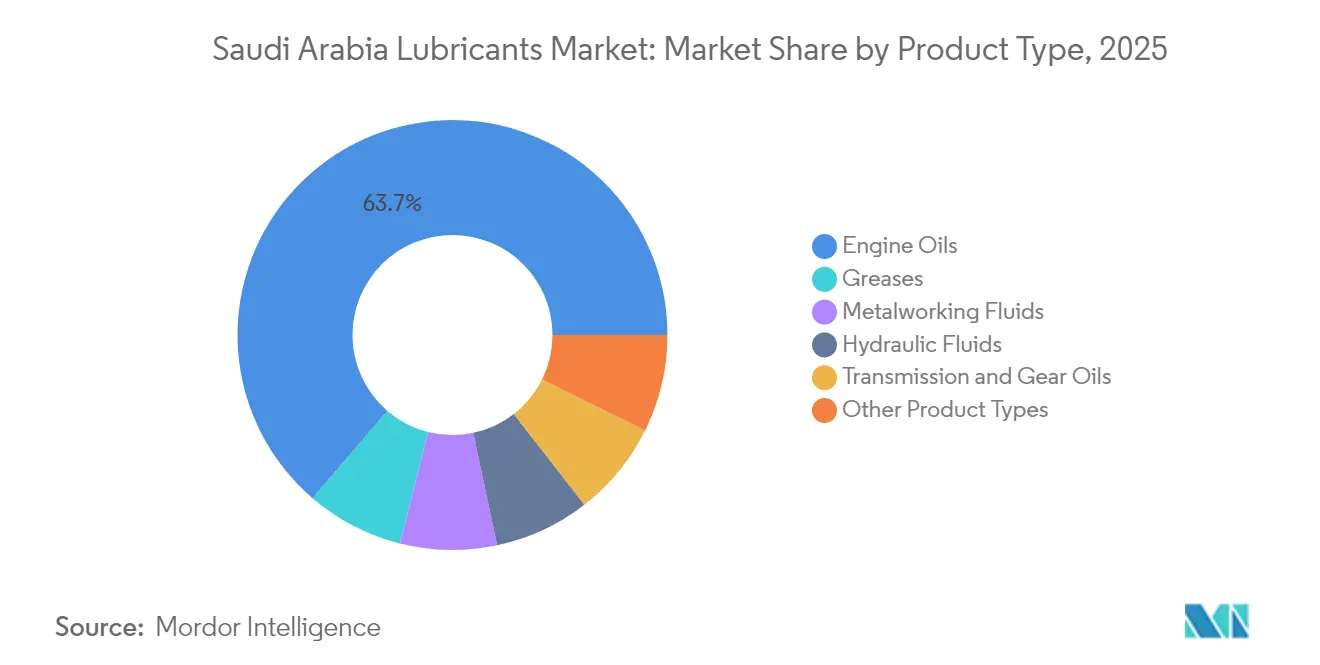

- By product type, engine oil led with 63.72% of Saudi Arabia lubricants market share in 2025; greases are projected to record the fastest 4.55% CAGR through 2031.

- By distribution channel, distributor/retailers held 62.58% of the Saudi Arabia lubricants market size in 2025, whereas direct-channel sales are advancing at a 15.35% CAGR to 2031.

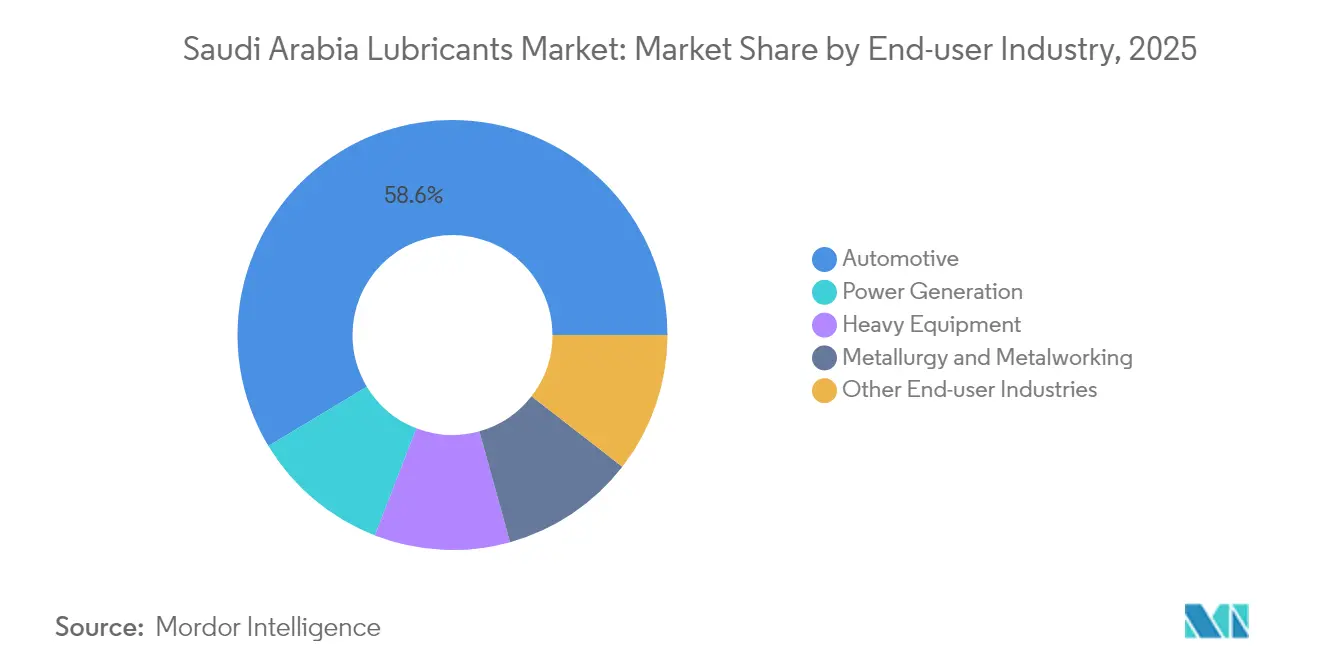

- By end user industry, automotive applications captured 58.64% share of the Saudi Arabia lubricants market size in 2025, while power-generation demand is growing at a 4.52% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued growth of Saudi vehicle parc | +1.2% | National, concentrated in Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Vision-2030 led industrial diversification | +1.5% | National, with Eastern Province and Yanbu leading | Long term (≥ 4 years) |

| Shift to low-SAPS and premium synthetics | +0.8% | National, driven by automotive OEM requirements | Medium term (2-4 years) |

| Luberef LubeHUB supply localization | +0.6% | National, with Yanbu as production hub | Long term (≥ 4 years) |

| Growth of investments in power-generation sector | +0.9% | National, with NEOM and gas-fired projects leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Growth of Saudi Vehicle Parc

Saudi Arabia’s expanding vehicle stock keeps lubricant volumes buoyant. Commercial fleets operating in extreme heat and dust require frequent fluid changes, lifting per-vehicle consumption. Telematics-based maintenance programs used by fleet operators are, however, nudging demand toward longer-lasting premium synthetics that lower downtime. Automotive-specific services, including condition-monitoring and OEM-approved formulations, now form a core differentiator for suppliers courting national-fleet contracts.

Vision-2030 Led Industrial Diversification

National Industrial Development and Logistics Programme (NIDLP) incentives are reshaping demand, with over USD 130 billion invested in new factories since 2016. Eastern Province petrochemical complexes such as Amiral and PlasChem Park generate steady orders for hydraulic fluids, metalworking fluids, and specialty greases for precision equipment. SABIC’s NUSANED initiatives promote local catalyst and additive production, pressing suppliers to deliver high-performance formulations aligned with Industry 4.0 manufacturing. These changes deepen the Saudi Arabia lubricants market’s exposure to heavy-industry buyers while encouraging vertical integration of additive chemistry within the Kingdom.

Shift to Low-SAPS and Premium Synthetics

Euro 6 tailpipe norms and OEM warranty rules are accelerating the pivot toward low-SAPS and fully synthetic engine oils. Local marketers highlight performance gains such as extended drain intervals, improved oxidation resistance, and better cold-start protection. APSCO’s Mobil synthetic range, for instance, is positioned as a premium solution for turbocharged gasoline direct-injection engines[1]Arabian Petroleum Supply Company, “Mobil synthetic oils,” apsco.com.sa. Domestic additive capacity slated by Farabi Petrochemicals and Richful will underpin formulation agility and pricing leverage once online. Higher per-liter margins on synthetics also cushion producers against feedstock volatility.

Luberef Lubehub Supply Localization

Luberef’s Yanbu-based LubeHUB delivers Group II base oils via dedicated pipelines, cutting logistics costs for downstream blenders while stimulating inward investment in finished-lube plants. Base-oil capacity now stands at 1.6 million t/y, with Group III feasibility under review. Incentives across 13 specialty-product categories, from transformer oils to white oils, further embed Saudi Arabia as a regional lubricant-manufacturing hub. Localization ensures stable feedstock pricing, faster customization, and export potential to Africa and South Asia where demand is rising sharply.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV penetration trimming engine-oil volumes | -0.8% | National, with urban centers leading adoption | Long term (≥ 4 years) |

| Crude-linked base-oil price volatility | -0.6% | National, affecting all market segments | Short term (≤ 2 years) |

| Counterfeit and grey-import lubricants | -0.4% | National, concentrated in aftermarket channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Penetration Trimming Engine-Oil Volumes

EV registrations tripled to about 800 units in 2024, and policy targets call for 500,000 units of annual domestic output by 2030. Although absolute numbers remain low, every battery-electric vehicle displaces 4-6 liters of engine oil consumption per service interval. Charging-infrastructure build-outs under the state-backed eViq initiative will accelerate adoption in metropolitan corridors. Lubricant suppliers are hedging exposure by developing gearbox fluids for hybrids, dielectric coolants for battery packs, and specialty greases for charging disconnects, positioning for a gradual product-mix shift rather than outright volume collapse.

Counterfeit and Grey-Import Lubricants

SASO conformity rules require SABER certification and Arabic labeling before customs clearance, but non-compliant imports still reach informal channels. Recent enforcement led to 39 fuel-station closures for fraudulent practices[2]Ministry of Commerce, “Closure of 39 fuel stations,” mc.gov.sa . Counterfeits erode brand equity and increase warranty-claim risks. Legitimate marketers respond with tamper-evident packaging, QR-code verification, and dealer-education programs to reassure professional workshops and consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Types: Engine-Oil Dominance Amid Synthetic Transition

Engine oil generated 63.72% of the total 2025 volume, thanks to the Kingdom’s large vehicle parc and harsh climate that necessitates frequent changes. The Saudi Arabia lubricants market size for engine oil is still expected to advance, but at a moderating pace as fleet operators stretch drain intervals through synthetics. Greases, although on a smaller base, will clock the fastest 4.55% CAGR to 2031, supported by industrial machinery, renewable-energy bearings, and construction equipment needs. Hydraulic-fluid demand tracks infrastructure roll-outs, while metalworking fluids benefit from factories added under NIDLP. The forthcoming domestic additive plant enhances formulation flexibility, supporting specialized blends for aerospace and pharmaceutical machining.

Digitization and predictive-maintenance adoption in manufacturing increase the appetite for sensor-friendly lubricants integrated with IoT platforms. Suppliers are therefore bundling fluids with analytics dashboards that flag contamination or viscosity shifts in real time. Overall, premium product tiers capturing higher margins help offset slower growth in conventional mineral-oil categories.

By Distribution Channel: Digital Transformation Accelerating Direct Sales

Distributor/retailers retained 62.58% share in 2025, upheld by nationwide workshop networks and credit facilities. Yet direct orders are growing 15.35% CAGR as fleets link procurement to telematics dashboards that auto-reorder based on consumption thresholds. This evolution embeds technical-service contracts and boosts data transparency. Gasoline stations remain essential for do-it-yourself car owners, though EV charging points planned at major service areas may gradually cannibalize shelf space formerly devoted to engine oil.

Large tenders from logistics operators increasingly specify digital-invoice integration and KPI-based performance guarantees, favoring suppliers with e-commerce portals and API connectivity. Consequently, competition shifts from pure price to total cost-of-ownership metrics validated by data-sharing agreements.

By End User Industry: Automotive Leadership Faces Power-Generation Challenge

Automotive users consumed 58.64% of the 2025 volume, anchored by passenger-car density in Riyadh and Jeddah and heavy-duty trucks hauling construction materials across giga-projects. Fleet upgrades to Euro 6 diesel engines lift demand for low-ash formulations. Nonetheless, the power-generation sector is set for the quickest 4.52% CAGR as more combined-cycle plants, wind farms, and green-hydrogen electrolyzers come online. High-temperature turbine oils with 7,000-hour drain targets and dielectric fluids for battery-storage modules command premium pricing.

Heavy-equipment operators spanning mining to cement enjoy Vision 2030 stimulus, keeping demand stable for extreme-pressure greases. Metallurgy and metalworking volumes grow in tandem with local steel and aluminum capacity additions. Diversifying end-use profiles shields the Saudi Arabia lubricants market from single-sector shocks.

Geography Analysis

Petrochemical giants Aramco, SABIC, and Sadara drive continuous demand for compressors and hydraulic fluids. Yanbu’s LubeHUB further cements the province’s status as a feedstock nucleus. Central Region spearheads automotive lubricant consumption due to Riyadh’s highest vehicle density and government fleets that embed OEM-approved synthetics. Dealer-backed service contracts stimulate repeat purchase cycles and data-driven maintenance scheduling.

Western Region’s Red-Sea port logistics and religious-tourism vehicle traffic sustain multi-grade engine oil demand. Luberef’s Jeddah base-oil plant ensures localized supply resilience. Northern and Southern territories remain smaller but fast-growing as mining concessions and cross-border trade expand heavy-equipment parks requiring specialized greases tolerant of dust and altitude extremes. NEOM’s northwest giga-project introduces renewable-centric lubricant niches, gearbox oils for 80-meter turbines, and biodegradable hydraulic fluids for solar-tracker actuators.

Infrastructure uniformity across regions benefits from SASO standards and SABER digital conformity checks, guaranteeing quality consistency. This regulatory harmonization encourages national roll-outs of differentiated product lines without regional formula tweaks, streamlining inventory and branding strategies.

Competitive Landscape

The Saudi Arabian lubricants market is concentrated in nature. Shell, ExxonMobil, BP-Castrol, and Chevron rely on technology leadership and international brand equity, whereas Aramco leverages feedstock integration via Luberef and newly acquired Valvoline trademarks. Local independents like FUCHS and Petromin cultivate niche trust through localized blending, technical-service labs, and quick-lube chains. Market entry barriers elevate as SASO tightens conformity assessments and demands Arabic safety data sheets. Nonetheless, the planned additive plant promises to democratize advanced chemistry access, possibly lowering formulation costs for home-grown brands and intensifying price competition in mid-tier product categories.

Saudi Arabia Lubricants Industry Leaders

BP P.L.C (Castrol)

ExxonMobil Corporation (Arabian Petroleum Supply Company (APSCO))

Petromin Corporation

Saudi Arabian Oil Co. (SAUDI ARAMCO)

Shell PLC (Aljomaih and Shell Lubricating oil company Limited (JOSLOC))

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Saudi Aramco confirmed it is evaluating a USD 6-8 billion acquisition bid for BP’s Castrol unit, aiming to broaden its downstream lubricants footprint and extend global reach.

- March 2023: Saudi Aramco completed its USD 2.65 billion purchase of Valvoline’s global products business, adding a renowned consumer brand to its growing lubricants portfolio.

Saudi Arabia Lubricants Market Report Scope

By Product Types

| Engine Oils |

| Greases |

| Hydraulic Fluids |

| Metalworking Fluids |

| Transmission and Gear Oils |

| Other Product Types |

By Distribution Channel

| Distributor/Retailers |

| Gasoline Stations |

| Direct Channel |

By End-user Industry

| Automotive |

| Power Generation |

| Heavy Equipment |

| Metallurgy and Metalworking |

| Other End-user Industries |

| By Product Types | Engine Oils |

| Greases | |

| Hydraulic Fluids | |

| Metalworking Fluids | |

| Transmission and Gear Oils | |

| Other Product Types | |

| By Distribution Channel | Distributor/Retailers |

| Gasoline Stations | |

| Direct Channel | |

| By End-user Industry | Automotive |

| Power Generation | |

| Heavy Equipment | |

| Metallurgy and Metalworking | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the Saudi Arabia lubricants market in 2026?

It totals 705.86 million liters in 2026 and is expected to grow at a 4.16% CAGR to reach 865.41 million liters by 2031.

Which product dominates lubricant demand in the Kingdom?

Engine oil commands 63.72% of 2025 volume, reflecting the sizeable on-road vehicle parc and harsh desert operating conditions.

What channel is expanding fastest for lubricant sales?

Direct-channel purchases linked to digital fleet-management platforms are increasing at a 15.35% CAGR through 2031.

Which end-use sector shows the quickest growth?

Power-generation applications are projected to rise at a 4.52% CAGR, driven by gas-fired IPPs and renewable-energy projects.

How is Vision 2030 influencing lubricant demand?

Vision 2030-led industrial diversification fuels consumption of hydraulic fluids, metalworking fluids, and specialty greases in new manufacturing hubs.

Page last updated on: