Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.96 Billion |

| Market Size (2026) | USD 31.29 Billion |

| Market Size (2031) | USD 54.87 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

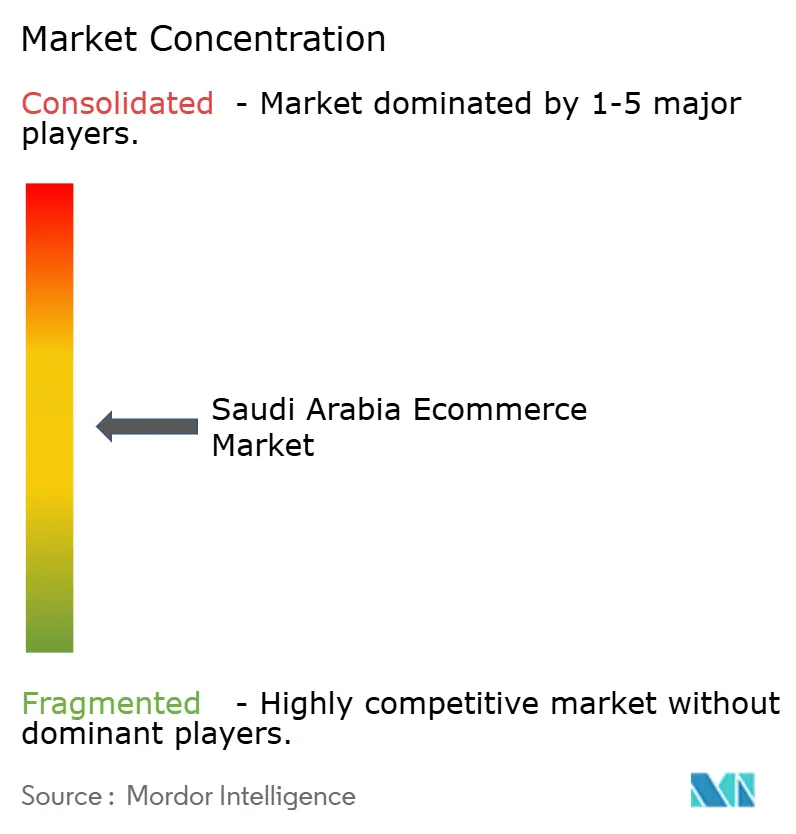

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia E-commerce Market Analysis by Mordor Intelligence

Saudi Arabia E-commerce Market size in 2026 is estimated at USD 31.29 billion, growing from 2025 value of USD 27.96 billion with 2031 projections showing USD 54.87 billion, growing at 11.92% CAGR over 2026-2031.

Underscoring the Kingdom’s rapid digital-commerce transition. Momentum stems from Vision 2030 infrastructure investments, 99% internet penetration, and 78% 5G coverage, which together create an always-connected consumer base. Cash-to-card migration via the Mada network, surging Gen-Z social-commerce engagement, and AI-powered last-mile innovations further accelerate uptake. Platforms integrate biometric payments and dark-store logistics to lift conversion rates and compress delivery times, while regulatory clarity around the Personal Data Protection Law (PDPL) increases shopper confidence and raises entry barriers for under-capitalized newcomers. Competitive dynamics feature Amazon.sa, Noon and fast-growing local enablers Zid and Salla scaling AI personalization and SME onboarding, even as high rural fulfilment costs temper nationwide adoption.

Key Report Takeaways

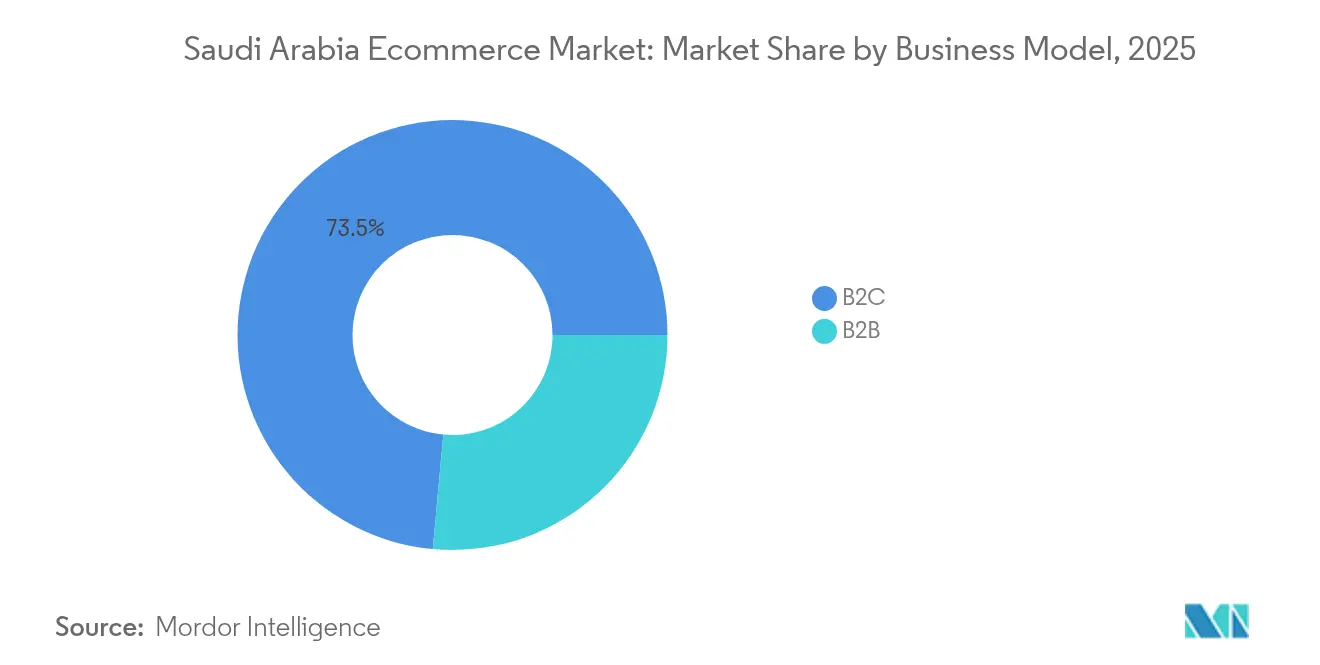

- By business model, B2C transactions held 73.54% of Saudi Arabia e-commerce market share in 2025, while B2B is advancing at a 13.45% CAGR through 2031.

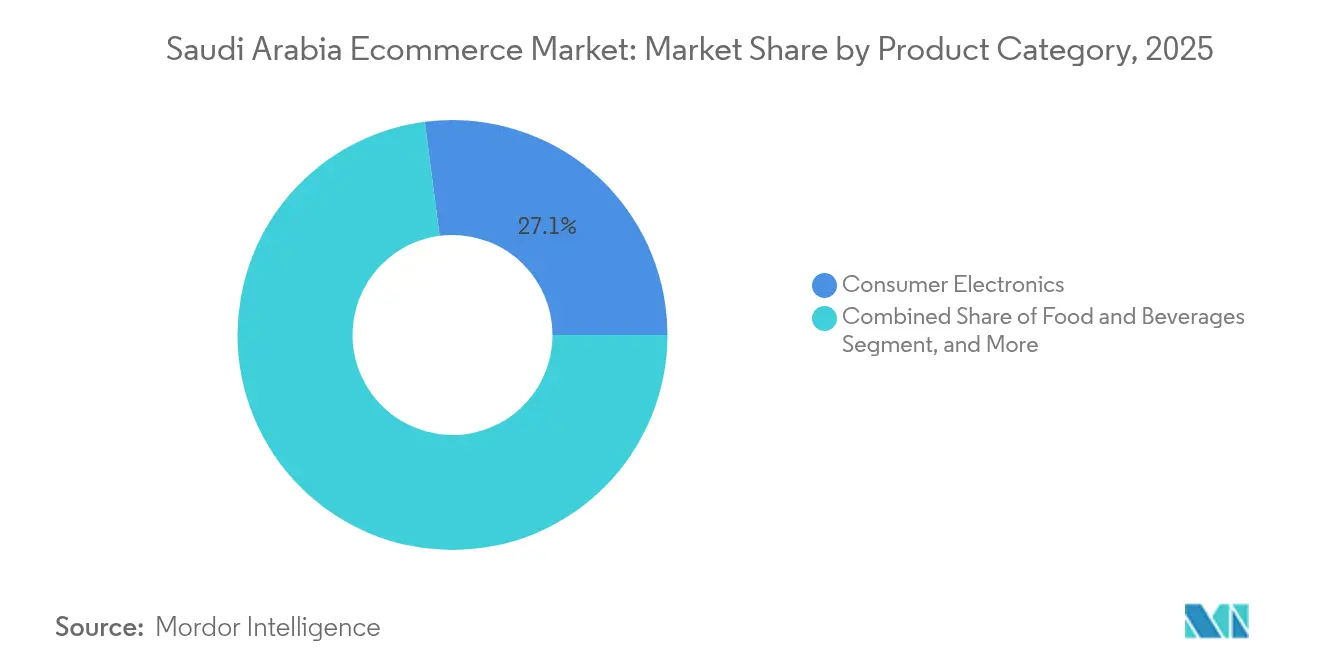

- By product category for B2C e-commerce, consumer electronics commanded 27.06% of the Saudi Arabia E-commerce Market size in 2025, whereas grocery and food and beverages rose at a 13.72% CAGR toward 2031.

- By payment mode for B2C e-commerce, credit/debit cards led with 42.62% share of the Saudi Arabia e-commerce market size in 2025; digital wallets record the fastest 14.71% CAGR to 2031.

- By device type for B2C e-commerce, smartphones delivered 77.98% revenue share in 2025 and expand at a 13.07% CAGR through 2031.

- By geography, Riyadh contributed 35.01% revenue share in 2025; Eastern Province posts the highest 12.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 99% internet penetration and 78% 5G coverage | +2.1% | Riyadh, Makkah, Eastern Province | Medium term (2-4 years) |

| Cash-to-card shift via Mada network | +1.8% | Urban centers nationwide | Short term (≤ 2 years) |

| Rapid grocery-delivery adoption in Tier-2 | +1.4% | Dammam, Jeddah suburbs, Khobar | Medium term (2-4 years) |

| SME onboarding through Monsha’at programs | +1.2% | Industrial clusters | Long term (≥ 4 years) |

| Gen-Z social-commerce acceleration | +1.6% | Metropolitan areas | Short term (≤ 2 years) |

| AI-powered fulfilment and dark stores | +1.3% | Urban corridors, expanding to Tier-2 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

99% Internet Penetration and 5G Coverage Spur Mobile Commerce

Nationwide 5G now covers 78% of residents and pairs with near-universal internet access to create friction-free shopping journeys. Government fiber roll-outs and Fixed Wireless Access in remote areas shorten the urban-rural digital gap. Streaming-era consumers expect sub-second page loads; platforms respond with edge-hosting and progressive-web-app architectures that boost mobile checkout completion. 5G low-latency supports augmented-reality product trials and real-time order tracking, raising trust levels and basket sizes. Telco-retailer partnerships bundle zero-rated data plans with marketplace subscriptions, cementing smartphone primacy within the Saudi Arabia E-commerce Market.

Mada Network Accelerates the Cash-to-Card Shift

The National Payment Network processed USD 52.6 billion in ecommerce sales during 2024, a 25.8% lift from 2023. Contactless Mada debit cards interoperate with Apple Pay and mada Pay, enabling PIN-free taps below SAR 100 and deterring COD usage. Merchant fees remain capped, incentivizing ubiquitous acceptance. Government wage digitalization funnels salaries directly into accounts, reinforcing card habits and raising the Saudi Arabia E-commerce Market’s electronic-payment penetration.

Rapid Grocery-Delivery Adoption in Tier-2 Cities

Dark-store operators like Nana opened 30 micro-fulfilment hubs in Riyadh and target 50 countrywide, promising 15-minute drop-offs.[1]Wamda, “Nana Opens Dark Stores Across Riyadh,” wamda.com AI demand-forecasting slashes spoilage, making low-margin grocery viable online. Provincial consumers embrace subscription produce boxes and voice-activated re-orders, lifting average order frequency. FMCG brands engage via shoppable livestreams, leveraging localized dialect influencers to deepen reach beyond major metros.

SME Digitization Through Monsha’at

Monsha’at deployed SAR 800 million to digitize 824 SMEs, linking subsidies to storefront activation milestones. Zid and Salla provide turnkey catalogs, logistics APIs and inventory-syncing, compressing go-to-market from months to days. B2B portals integrate purchase-order financing and dynamic discounting, translating to 13.63% CAGR for the segment. Vision 2030’s goal to raise SME GDP share to 35% ensures sustained policy backing and venture-capital inflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile costs outside metro corridors | -1.4% | Rural and remote regions | Medium term (2-4 years) |

| Cross-border return-logistics complexity | -0.8% | International marketplace flows | Long term (≥ 4 years) |

| Low BNPL trust among older shoppers | -0.6% | 45+ demographics | Short term (≤ 2 years) |

| Cyber-fraud and data-sovereignty compliance | -1.1% | Platforms hosting Saudi resident data | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Delivery Costs Limit Rural Reach

Sparse-population routes double per-package costs versus city drops, hurting service-level economics in the Saudi Arabia E-commerce Market’s hinterlands.[2]Shipa, “Cracking Last-Mile Delivery Challenges in the GCC,” shipa.com Non-standardized addresses delay routing-algorithm efficacy. Consolidated pick-up points and drone pilot trials offset part of the gap, yet breakeven timelines stretch for independent couriers. Vision 2030 road upgrades and postcode roll-outs gradually narrow disparities but near-term drag persists.

Cyber-Fraud and Compliance Complexity

PDPL obliges local data hosting, consent logging and DPO appointments, raising platform overhead.[3]Clyde & Co, “Saudi Arabia’s Personal Data Protection Law Becomes Enforceable,” clydeco.com CITC’s Cybersecurity Regulatory Framework layers additional controls including mandatory security-incident reporting. Cross-border analytics stacks require anonymization gateways to satisfy data-sovereignty, complicating global SaaS integrations and deterring some foreign entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: SME Digitization Catalyzes B2B Uptake

B2C dominated with 73.54% revenue in 2025 as pandemic-era habits normalized digital grocery, fashion and electronics shopping. Meanwhile, Monsha’at-backed onboarding propels B2B to a 13.45% CAGR, enlarging Saudi Arabia E-commerce Market size for wholesalers and manufacturers.

B2B marketplaces integrate credit-scoring and invoice-financing modules, enabling bulk buyers to secure 30-day terms and stimulating order volumes. Zid’s merchants process SAR 1.6 billion in annual sales, showcasing platform scalability. Compliance features such as PDPL-ready document vaults differentiate enterprise offerings, positioning B2B portals for sustained uptake among export-oriented SMEs.

By Payment Mode: Wallet Adoption Outpaces Card Dominance

Credit/ Debit Cards retained 42.62% share of Saudi Arabia E-commerce Market size in 2025 owing to deep bank integration and fee ceilings. Yet mobile wallets post 14.71% CAGR, reflecting mobile-first behavior.

STC Pay’s 8 million users leverage real-time peer-to-merchant transfers and QR codes at pop-up retail. Apple Pay and Google Pay surge among Gen-Z as biometric login heightens trust. SAMA’s digital-banking sandbox streamlines licensing, prompting neobank entrants that bundle e-wallets with micro-savings and BNPL plugins, further diversifying payment rails.

By Product Category: Dark-Store Grocery Outpaces Electronics

Consumer electronics led with 27.06% revenue in 2025, buoyed by predictable SKUs and price transparency. food and beverages enjoys 13.72% CAGR as ultrafast fulfilment re-trains shopper expectations.

Operators deploy AI to predict neighborhood stock-keeping and adjust planograms daily, reducing wastage. Loyalty schemes tie grocery baskets to pharmacy and pet-care add-ons, lifting cross-sell. Electronics demand persists for flagship smartphones and gaming rigs, but category growth moderates amid longer replacement cycles and used-device marketplaces.

By Device Type: Smartphone Commerce Reigns Supreme

Smartphones captured 7 7.98% share in 2025 andsustain a 13.07% CAGR, confirming Saudi Arabia E-commerce Market’s mobile-first DNA. Progressive-web-app compression enables 1-second load on 3G fallback, widening rural access.

Voice-assisted ordering via Arabic-language smart assistants debuts in 2025, targeting hands-free re-plenishment. Desktop persists for high-ticket B2B RFQs requiring spreadsheet uploads, yet share erodes. Wearables and car-infotainment screens represent next-frontier touchpoints as 5G latency falls below 10 ms.

Geography Analysis

Riyadh leads the Saudi Arabia e-commerce market with a 35.01% share, buoyed by dense fulfilment nodes and affluent civil-service demographics. The province hosts Amazon’s USD 5.3 billion AWS region and Noon’s robotics hub, ensuring same-day delivery and AI personalization at scale.

Makkah Province ranks second, powered by Jeddah’s port logistics and religious-tourism retail peaks. Peak-season demand triggers seasonal hiring sprees and cross-docking pop-ups that compress customs-to-customer dwell time.

Eastern Province posts the fastest 12.76% CAGR as petrochemical diversification and port upgrades at Dammam catalyze disposable-income growth. Cross-Gulf proximity drives international marketplace sales and import-duty optimization via bonded zones. Outlying regions wrestle with high last-mile costs but benefit from Vision 2030 road grids and postcode rollout that gradually lower delivery friction.

Competitive Landscape

Amazon’s AWS division has announced plans to deploy over USD 5.3 billion to establish a dedicated cloud region in Saudi Arabia. This large-scale investment will expand local computing capacity and strengthen the digital infrastructure that supports the country’s fast-growing e-commerce ecosystem.In July 2024, Noon selected Adyen as its payments technology partner, enabling more sophisticated fraud-management tools and a unified checkout framework across its major markets, including Saudi Arabia, the UAE, and Egypt.

Saudi Arabia’s online retail enablement space continues to be shaped by Salla and Zid, which play pivotal roles in supporting SMEs entering e-commerce. Salla alone now serves over 80,000 merchants, backed by a USD 130 million pre-IPO funding round aimed at accelerating product and platform enhancements. In 2024, Salla also integrated STC Bank-the Kingdom’s first licensed digital bank-as a payment option across its network of online stores. Saudi beauty retailer Nice One recently completed its listing on the Saudi Exchange. Funds raised are being deployed toward technological upgrades, expanded logistics capabilities, and broader omnichannel initiatives to strengthen its position in domestic and regional markets.

BinDawood Holding is channeling close to USD 390 million into automation technologies and new delivery facilities to scale its online grocery and retail operations. The spending focuses on enhancing robotic systems, dark-store automation, and distribution infrastructure to support higher e-commerce demand. Regional AI provider qeen.ai, whose tools are used by merchants across the Middle East including in Saudi Arabia, reports customer case studies indicating that its AI-generated product content can increase add-to-cart rates by roughly 30%.

Saudi Arabia E-commerce Industry Leaders

Amazon Inc.

Noon AD Holdings Ltd.

Jarir Marketing Company

United Electronics Company

Nahdi Medical Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Apple launched a localized online store, its first direct ecommerce channel in the Kingdom.

- May 2025: Amazon and HUMAIN pledged over USD 5 billion for an AI zone in Riyadh to host sovereign-cloud and robotics R&D.

- March 2025: Diriyah Company opened talks with Alshaya Group and Starbucks on a 1,000-store lifestyle retail cluster integrating online-to-offline journeys.

- February 2025: NEOM and Samsung C&T formed a SAR 1.3 billion robotics JV to automate construction, indirectly boosting ecommerce infrastructure.

Saudi Arabia E-commerce Market Report Scope

The Saudi Arabian e-commerce market is defined based on the revenues generated from the sales of various end-user applications, such as food, beverage, consumer electronics, fashion and appraisal, beauty and personal care, furniture, home, and other end users. The analysis is based on market insights captured through secondary and primary research. The market also covers the major factors impacting its growth in terms of drivers and restraints.

The Saudi Arabia e-commerce market is segmented by type (B2C e-commerce [applications [beauty and personal care, consumer electronics, fashion and apparel, food and beverage, furniture, and home, others (toys, DIY, media, etc.)] and B2B e-commerce). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Business Model

| B2B |

| B2C |

By Product Category for B2C E-commerce

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories for B2C E-commerce |

By Payment Mode for B2C E-commerce

| Credit/ Debit Cards |

| Mobile Wallets |

| Other Payment Modes for B2C E-commerce |

By Device Type for B2C E-commerce

| Smartphone |

| Desktop / Laptop |

| Other Device Types for B2C E-commerce |

| By Business Model | B2B |

| B2C | |

| By Product Category for B2C E-commerce | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories for B2C E-commerce | |

| By Payment Mode for B2C E-commerce | Credit/ Debit Cards |

| Mobile Wallets | |

| Other Payment Modes for B2C E-commerce | |

| By Device Type for B2C E-commerce | Smartphone |

| Desktop / Laptop | |

| Other Device Types for B2C E-commerce |

Key Questions Answered in the Report

What is the forecast value of Saudi Arabia’s online retail sector by 2031?

It is projected to reach USD 54.87 billion, growing at a 11.92% CAGR between 2026 and 2031.

Which payment method is expanding fastest among Saudi online shoppers?

Mobile wallets led by STC Pay are registering a 14.71% CAGR, outpacing card growth.

Why is grocery delivery a hot-growth niche in the Kingdom?

Dark-store roll-outs in Tier-2 cities enable 15-minute drop-offs and are propelling a 13.72% CAGR in the grocery segment.

How does Vision 2030 support ecommerce SMEs?

Monsha’at has disbursed SAR 800 million to digitize 824 SMEs, fueling B2B marketplace expansion.

What keeps rural ecommerce penetration below metro levels?

High last-mile delivery costs and non-standard addresses inflate fulfilment expenses outside major cities.

Page last updated on: