Saudi Arabia Cosmetic Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

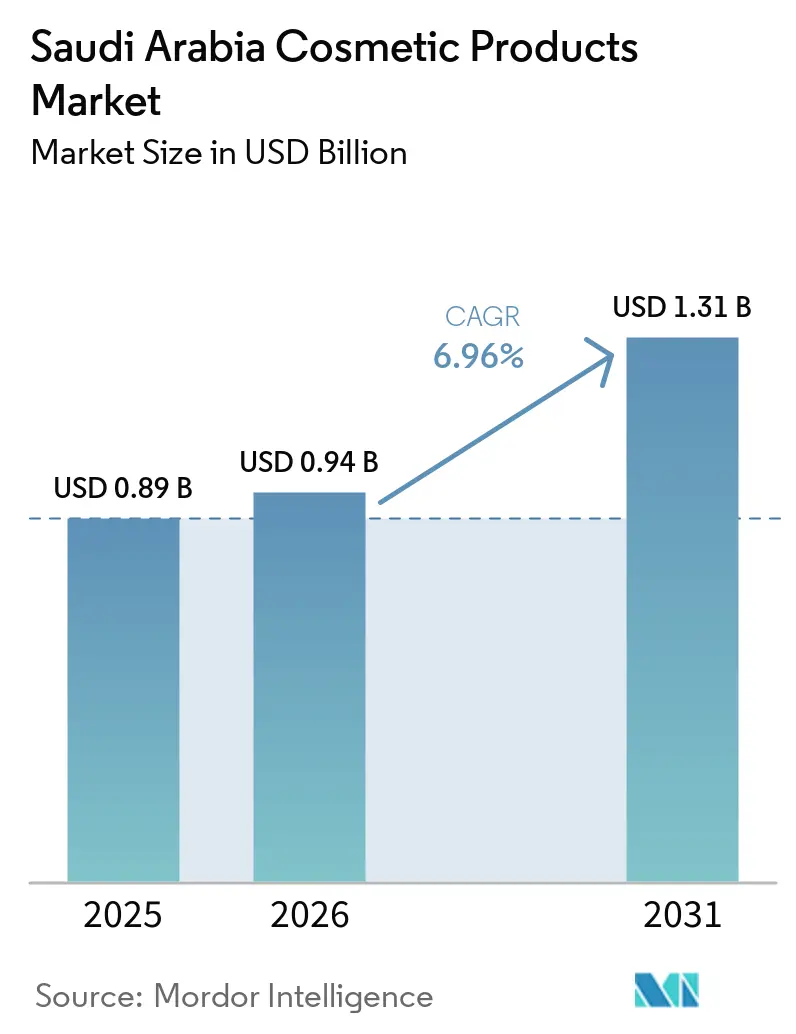

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Cosmetic Products Market Analysis by Mordor Intelligence

The Saudi Arabia cosmetic products market size was valued at USD 0.89 billion in 2025 and estimated to grow from USD 0.94 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 6.96% during the forecast period (2026-2031). The market's growth is primarily driven by the Vision 2030 initiative, which has created a favorable business environment through enhanced regulatory frameworks and increased global investment. The country's large young population, increasing consumer spending power, and growing number of working women contribute to market expansion. The retail landscape is evolving with the proliferation of specialty beauty stores and luxury department stores, while high digital connectivity has led to the adoption of omnichannel strategies by retailers. E-commerce platforms and social media significantly influence consumer behavior in discovering and purchasing beauty products. While international brands maintain a strong presence, local manufacturers are expanding their portfolios to meet regional preferences, particularly in the growing halal cosmetics segment. The market also reflects global wellness trends with increasing demand for natural and organic beauty products, driven by heightened awareness of personal grooming among both men and women.

Key Report Takeaways

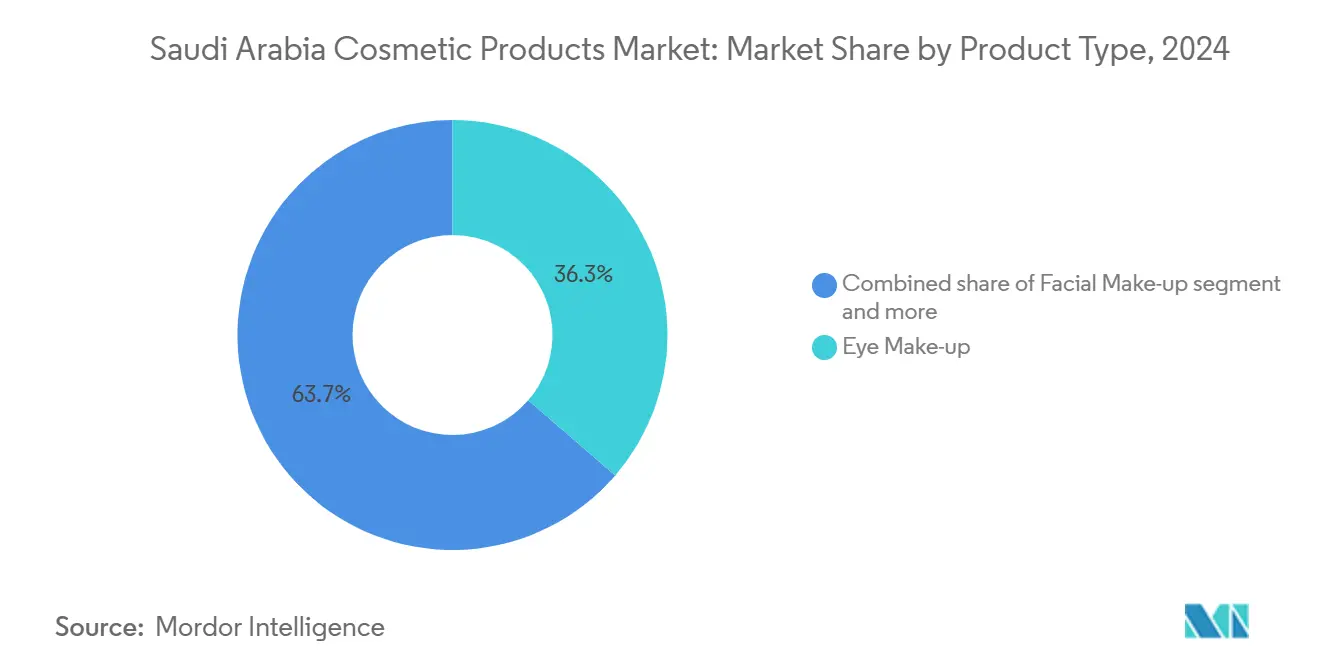

- By product type, eye make-up led with 36.34% revenue share in 2024, while facial make-up is projected to expand at a 7.34% CAGR to 2030.

- By category, mass products held 69.34% of the Saudi Arabian cosmetics market in 2024, whereas the premium segment is forecast to grow at a 7.83% CAGR through 2030.

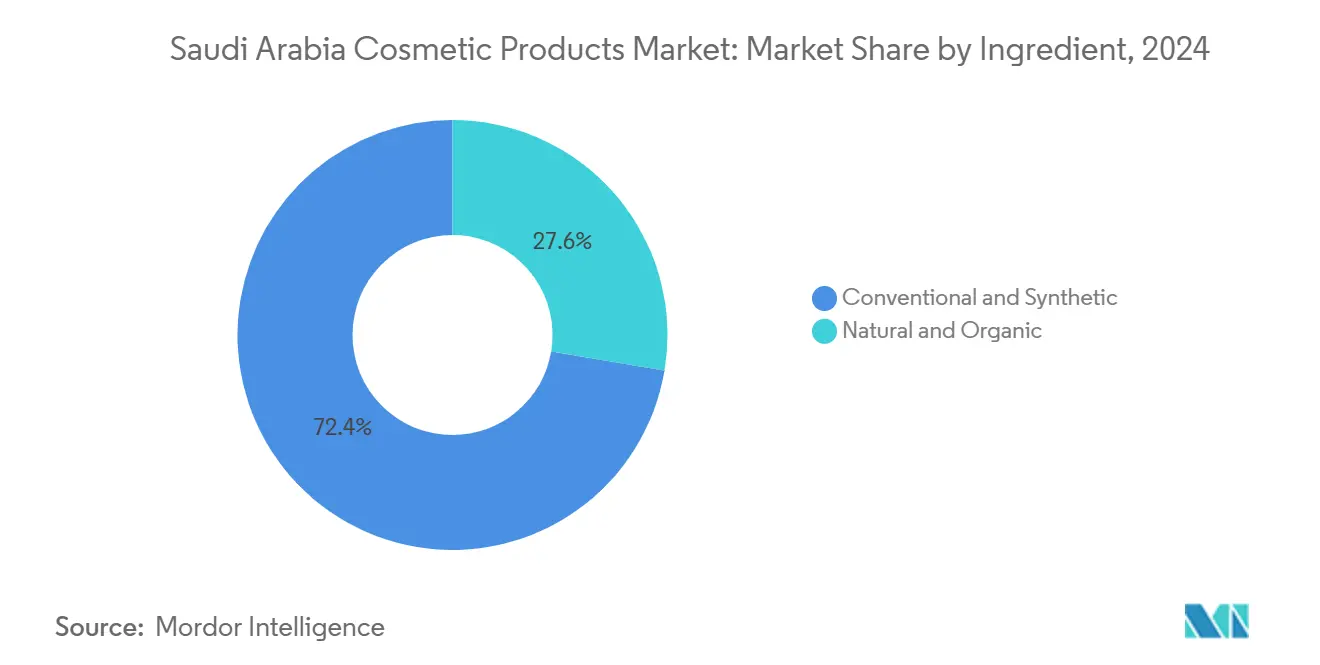

- By ingredient type, conventional and synthetic formulations captured a 72.46% share in 2024; the natural and organic segment is anticipated to rise at a 6.86% CAGR to 2030.

- By distribution channel, specialty stores accounted for 57.34% of the Saudi Arabia cosmetics market in 2024, while online retail is advancing at an 8.25% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influence of social media platforms | +1.2% | National, with concentrated impact in Riyadh, Jeddah, Dammam | Short term (≤ 2 years) |

| Strong demand from expat population | +0.8% | National, with early gains in Eastern Province, Riyadh | Medium term (2-4 years) |

| Rising demand for halal-certified cosmetic products | +0.9% | National, with spillover to broader GCC region | Long term (≥ 4 years) |

| Increasing female workforce participation | +1.1% | National, with accelerated adoption in major urban centers | Medium term (2-4 years) |

| Growing preference for natural and organic products | +0.7% | National, with premium segment concentration in Riyadh, Jeddah | Long term (≥ 4 years) |

| Expansion of retail infrastructure | +0.6% | National, with flagship developments in Riyadh, Jeddah | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Influence of Social Media Platforms

Social media platforms, particularly Instagram, TikTok, and Snapchat, have transformed the Saudi Arabian cosmetics market by creating direct-to-consumer channels that bypass traditional retail distribution. Young consumers in Saudi Arabia increasingly make purchase decisions based on beauty influencers, trends, and user-generated content on these platforms. Local and international cosmetics brands have intensified their social media marketing efforts and influencer collaborations to showcase products, engage with consumers, and build brand awareness. The rise of social commerce enables direct purchasing through these platforms, while real-time product demonstrations and reviews enhance transparency and trust. The visual nature of these platforms particularly appeals to the younger Saudi demographic, who constitute a significant portion of cosmetics consumers. According to the International Trade Administration, Saudi Arabia has one of the highest smartphone penetration rates globally at 97%, with mobile broadband internet subscriptions surpassing most advanced markets [1]Source: International Trade Administration, “Saudi Arabia – eCommerce,” trade.gov . The country ranks tenth worldwide for internet speed, further facilitating the growth of social media-driven cosmetics sales.

Strong Demand from Expat Population

A diverse international community, comprising residents from various Asian, Western, and Middle Eastern countries, encompasses different skin types, cultural beauty practices, and product preferences, driving retailers to maintain comprehensive product portfolios ranging from Asian beauty innovations to Western luxury cosmetics. According to the General Authority of Statistics, non-Saudis constitute 44.4% of the overall Saudi population in 2024 [2]Source: General Authority of Statistics, “Population Was 35.3 Million as of Mid-2024,” ksa.directory. This cultural diversity has led to the introduction of specialized products catering to different skin types, preferences, and beauty routines, creating opportunities for both mass-market and premium beauty products. The high disposable income among skilled expatriate workers, combined with their familiarity with international brands, drives the consumption of premium cosmetic products, while the growing number of working expatriate women has increased the demand for makeup, skincare, and personal care products. The presence of numerous shopping malls and beauty retail outlets in major expatriate-populated cities like Riyadh, Jeddah, and Dammam, coupled with strong social media engagement and awareness of global beauty trends, facilitates easy access and consistent demand for innovative cosmetic products.

Rising Demand for Halal-Certified Cosmetic Products

The halal cosmetics segment in Saudi Arabia is experiencing unprecedented growth, driven by increasing consumer awareness and religious considerations in the predominantly Muslim market. The Saudi Food and Drug Authority (SFDA) has implemented stringent regulations for halal certification, requiring compliance for products containing animal-derived ingredients. This regulatory framework has created both challenges and opportunities for international brands, as they must reformulate products to meet halal standards while addressing the growing demand for ethical and transparent sourcing practices. The SFDA's role extends to ensuring product safety and compliance through various electronic services for product registration and safety alerts, while recent memoranda of understanding for mutual recognition of product quality assurance may facilitate international trade in the cosmetics sector. According to the Population Estimation Publication 2024, Saudi Arabia's total population is estimated at 35.3 million people in mid-2024, with an annual growth rate of 4.7% compared to 2023[3]Source: General Authority of Statistics, “Population Estimates Publication 2024", stats.gov.sa. This expanding population base further strengthens the market potential for halal cosmetics in the region.

Increasing Female Workforce Participation

The increasing female workforce participation in Saudi Arabia is significantly influencing the cosmetics market growth, driven by a rising demand for workplace-appropriate makeup, skincare, and personal care products. The growing disposable income among working women has enhanced their purchasing power for premium cosmetic products, while workplace dress codes and professional appearance requirements have boosted the consumption of everyday makeup and grooming products. The expansion of women in customer-facing roles, particularly in retail and corporate sectors, has accelerated the demand for cosmetics and influenced the growth of retail channels and beauty services that cater to working women's specific needs and time constraints. According to the General Authority for Statistics, the labor force participation rate of Saudi females has reached 36.2%, indicating a substantial shift in employment demographics [4]Source: General Authority for Statistics, “Labor Force Indicators Q4 2024,” stats.gov.sa . This ongoing transformation in the workforce composition is expected to continue driving the growth of the Saudi Arabian cosmetics market in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns over product safety and ingredients | -0.9% | National, with heightened sensitivity in urban centers | Short term (≤ 2 years) |

| Rising concerns over counterfeit products | -1.1% | National, with concentrated impact in border regions and online channels | Medium term (2-4 years) |

| Strict regulatory requirements for cosmetic products | -0.7% | National, with compliance costs affecting smaller players | Long term (≥ 4 years) |

| High competition from international brands is limiting opportunities | -0.8% | National, with premium segment concentration in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Concerns Over Product Safety and Ingredients

Consumer vigilance regarding cosmetic ingredients has intensified in Saudi Arabia, with safety and transparency becoming paramount purchase considerations. The Saudi Food and Drug Authority (SFDA) has implemented strict regulations, including a comprehensive list of prohibited and restricted ingredients, while requiring manufacturers to comply with safety standards and proper ingredient disclosure. The Saudi Ministry of Health emphasizes the importance of checking ingredient lists and avoiding products that may cause skin irritation or allergies. The Saudi Standards, Metrology and Quality Organization (SASO) reinforces product safety through testing for harmful substances and issuing quality certifications. These regulatory requirements have increased operational costs for companies, as they must invest in quality testing and certification processes. Additionally, social media platforms have amplified consumer concerns, leading to rapid shifts in purchasing behavior and forcing companies to reformulate products with natural and halal-certified ingredients. This comprehensive regulatory framework and increasing consumer awareness create significant market entry barriers and compliance costs for cosmetics manufacturers, potentially restraining market growth in Saudi Arabia.

Rising Concerns Over Counterfeit Products

The proliferation of counterfeit cosmetics in Saudi Arabia presents significant challenges to consumer safety and brand integrity, particularly through unregulated online marketplaces. In response, the Saudi Intellectual Property Authority has implemented strict measures, including blocking 2,500 websites and confiscating nearly 1 million counterfeit products in 2023, while imposing fines and imprisonment for violations. The Saudi Standards, Metrology and Quality Organization (SASO) has strengthened product examination protocols and quality standards, while counterfeiters continue to exploit e-commerce growth and consumer price sensitivity to distribute potentially harmful or ineffective products. This issue extends beyond immediate health risks and lost sales, as consumers who experience poor results from counterfeit products often attribute their negative experiences to legitimate manufacturers, eroding brand equity and customer trust. To address these challenges, regulatory bodies have increased investments in detection technology, cross-border cooperation, and consumer education, while legitimate brands have implemented authentication technologies and secure distribution channels, though these measures increase operational costs that affect consumer pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eye Make-up Lead Cultural Expression

Eye makeup commands a dominant 36.34% share of the Saudi beauty market in 2024, reflecting deep-rooted cultural preferences that emphasize expressive eye makeup within traditional modest dress codes. This segment's prominence aligns with Islamic fashion requirements, while facial make-up exhibits the strongest growth trajectory at 7.34% CAGR through 2030, driven by increased workplace participation and social media influence. Lip and nail products maintain consistent performance through seasonal launches and color trends, while the resurgence of traditional kohl demonstrates the successful fusion of cultural heritage with modern beauty preferences.

The market's evolution is shaped by practical considerations, with international brands developing heat-resistant formulations suitable for Saudi Arabia's extreme temperatures that often exceed 45°C. Social media plays a crucial role in driving product innovation, particularly in eye cosmetics, as these products photograph well and enable creative expression within cultural parameters. This has led to advances in packaging, application tools, and the development of color ranges specifically formulated for Middle Eastern skin tones, meeting both functional and aesthetic requirements of Saudi consumers.

By Category: Mass Market Dominance Faces Premium Challenge

Mass products dominate the Saudi Arabian market with a 69.34% share in 2024, driven by price-conscious younger consumers and families with multiple beauty users, while the premium segment grows at 7.83% CAGR through 2030 due to rising affluence. The mass market's strength lies in its widespread accessibility through hypermarkets, pharmacies, and online platforms serving diverse income levels and regions, though the distinction between mass and premium segments continues to blur as mass brands introduce upscale lines and luxury brands launch more accessible options.

The premium segment thrives in urban centers like Riyadh and Jeddah, where professional women and affluent families prioritize quality and brand prestige. Local brands such as Asteri have successfully entered the premium space by highlighting clean formulations and cultural authenticity, while experiential retail investments and e-commerce platforms like Nice One Beauty enhance premium brand accessibility across Saudi Arabia, demonstrating the viability of online-first strategies in the premium beauty market.

By Ingredient Type: Natural Transition Accelerates Among Youth

Conventional and synthetic ingredients dominate the market with a 72.46% share in 2024, supported by established supply chains, regulatory approvals, and consumer familiarity with proven formulations across product categories. While natural and organic ingredients demonstrate strong growth potential at 6.86% CAGR through 2030, driven by Generation Z consumers' emphasis on sustainability and ingredient transparency, this segment particularly benefits from halal certification requirements due to plant-based ingredients' alignment with Islamic dietary principles.

The transition toward natural ingredients presents significant supply chain challenges, requiring specialized sourcing, storage, and preservation systems that increase manufacturing complexity and costs. International brands address these challenges by investing in regional natural ingredient sourcing and partnering with local suppliers to develop authentic Middle Eastern formulations using traditional ingredients like argan oil, rose water, and desert botanicals. This approach aligns with broader sustainability initiatives, including eco-friendly packaging and ethical sourcing practices, supporting Saudi Arabia's Vision 2030 environmental objectives while meeting consumer demands for environmentally responsible products.

By Distribution Channel: Digital Transformation Reshapes Retail

Specialty stores dominate the Saudi Arabian beauty market with a 57.34% share in 2024, leveraging their strengths in expert consultation, product curation, and experiential services that resonate with local consumers seeking guidance in beauty purchases. While supermarkets and hypermarkets serve convenience-driven purchases, and pharmacies cater to specific product categories, the online retail segment is experiencing rapid growth at an 8.25% CAGR through 2030, driven by improved logistics, secure payment systems, and mobile-first shopping experiences that align with Saudi Arabia's 82% digital consumption rate among young consumers.

Beauty brands are adapting to evolving consumer preferences by implementing omnichannel strategies that seamlessly integrate online and offline experiences. Physical stores now serve multiple purposes beyond traditional retail, functioning as fulfillment centers, experience venues, and customer service hubs, while maintaining their core advantage of providing personalized service, product testing opportunities, and culturally sensitive guidance that online channels cannot fully replicate.

Geography Analysis

Saudi Arabia's cosmetics market, the largest in the Gulf Cooperation Council, is experiencing robust growth supported by the country's Vision 2030 initiative. This strategic program strengthens the industry by diversifying the economy, empowering citizens and businesses, and enhancing investment opportunities. Through Monsha'at, the General Authority for Small and Medium Enterprises, beauty entrepreneurs receive mentorship, training, and networking opportunities across major Saudi cities, facilitating the expansion of local cosmetics brands and beauty-focused businesses.

The Kingdom's geographic location between Europe, Asia, and Africa provides strategic advantages for beauty brand distribution and cultural exchange. Consumer preferences vary significantly across regions, with Riyadh and Jeddah serving as primary market centers featuring substantial retail developments. The Eastern Province benefits from oil industry expatriate populations with higher beauty spending ratios, while the western region, particularly Mecca and Medina, presents opportunities for halal-certified products due to religious tourism. The Saudi Food and Drug Authority's leadership in halal cosmetics certification creates competitive advantages for brands seeking broader Muslim market access.

Saudi Arabia's robust digital infrastructure, characterized by high smartphone penetration and government support for cashless transactions, facilitates e-commerce growth in beauty retail. Regional variations reflect distinct cultural and demographic differences, with northern regions showing stronger preferences for traditional products like ithmid kohl, while southern regions demonstrate higher adoption of international brands. The development of NEOM and other megaprojects creates new consumer segments with unique beauty preferences. The country's climate necessitates heat-resistant, long-wearing formulations that can maintain performance in the Arabian Peninsula's challenging environmental conditions.

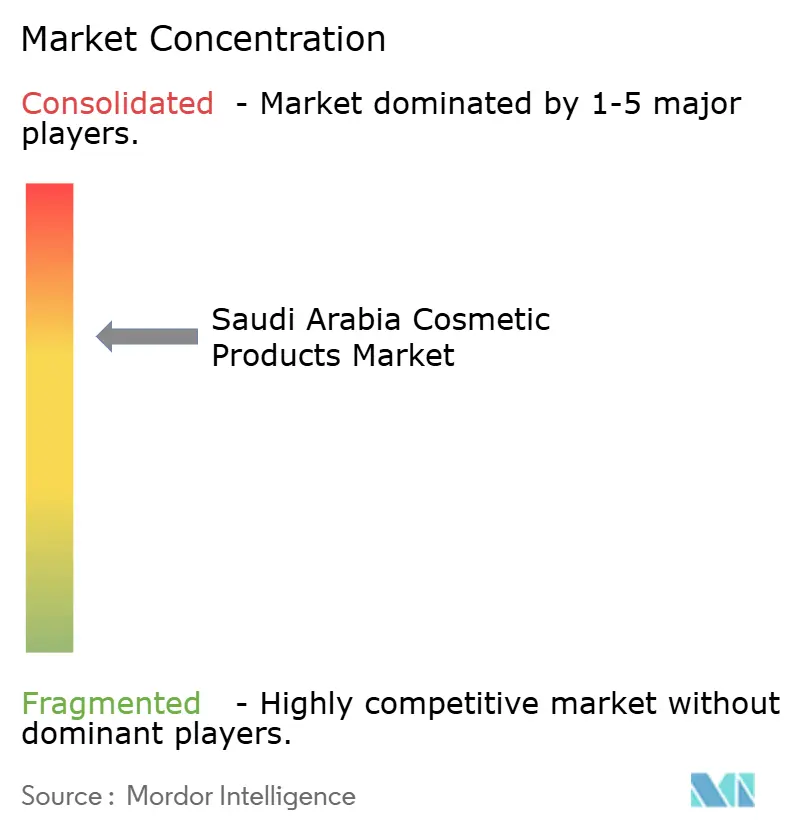

Competitive Landscape

The Saudi Arabian cosmetics market maintains a moderately consolidated market, where global companies like L'Oréal, Estée Lauder, and LVMH compete alongside regional and local retailers across various price points and distribution channels. Market participants are expanding their retail presence through omnichannel distribution strategies, as demonstrated by Asteri Beauty's 2023 online launch and subsequent expansion into brick-and-mortar retail with four stores across Saudi Arabia in 2024. These stores incorporate local cultural heritage in their design while offering vegan and cruelty-free cosmetics formulated for extreme weather conditions.

The Saudi Food and Drug Authority (SFDA) enforces strict regulations for halal certification and restricted cosmetic ingredients, creating opportunities for companies focusing on clean formulations. Local brands like Asteri, Moonglaze, and Jayla have successfully challenged established market hierarchies by combining international quality standards with local cultural narratives and ingredient preferences. This demonstrates the ability of Saudi entrepreneurs to compete effectively in premium segments, where cultural authenticity and halal certification take precedence over traditional brand heritage.

Technology adoption has emerged as a significant differentiator in the market, with brands implementing AR try-on experiences, AI-powered skin analysis, and personalized product recommendations. The competitive landscape benefits agile companies that can adapt to rapid trend cycles and leverage social media influence. While opportunities exist in men's grooming, sustainable packaging, and technology-enhanced beauty experiences, regulatory compliance and counterfeit prevention create barriers that advantage established players with robust quality systems and legal resources.

Saudi Arabia Cosmetic Products Industry Leaders

-

L'Oréal S.A.

-

LVMH Moët Hennessy Louis Vuitton SE

-

Coty Inc.

-

The Estee Lauder Companies Inc.

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ulta Beauty partnered with Alshaya Group to expand its presence in the Middle East, including plans to enter the Saudi Arabian market, reflecting the growing demand for cosmetics in the region

- January 2025: L'Oréal launched a new line of halal-certified skincare products specifically formulated for the Middle Eastern market, addressing growing demand for culturally-compliant beauty solutions.

- November 2024: Kosas, a clean beauty brand, launched in Saudi Arabia with a range of skincare-infused makeup products. The company selected its product line to meet local beauty preferences, featuring items such as the Revealer Concealer, Cloud Set Baked Setting Powder, and BB Burst Tinted Gel Cream Moisturizer.

Saudi Arabia Cosmetic Products Market Report Scope

Cosmetics are products applied to the body for cleansing, beautifying, and altering appearance. These include makeup products for the face, eyes, lips, and nails that enhance physical appearance, hygiene, and well-being. The Saudi Arabian cosmetics market is segmented by product type, category, ingredient type, and distribution channel. Based on product type, the market is segmented into facial cosmetics, eye cosmetics, and lip and nail make-up products. The category segment is divided into premium and mass products. Based on ingredient type, the market is segmented into natural and organic and conventional/synthetic. Based on the distribution channels, the market is segmented into specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Facial Make-up |

| Eye Make-up |

| Lip and Nail Make-up |

| Premium Products |

| Mass Products |

| Natural and Organic |

| Conventional and Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Facial Make-up |

| Eye Make-up | |

| Lip and Nail Make-up | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural and Organic |

| Conventional and Synthetic | |

| By Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia cosmetics market?

The market is valued at USD 0.94 billion in 2026.

How fast is the Saudi Arabia cosmetics market expected to grow?

It is projected to register a 6.96% CAGR, reaching USD 1.31 billion by 2031.

Which product segment holds the largest Saudi Arabia cosmetics market share?

Eye cosmetics lead with 36.34% revenue share in 2024.

Which distribution channel is growing the quickest?

Online retail is forecast to expand at an 8.25% CAGR through 2030.

Page last updated on: