Retractable Awnings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

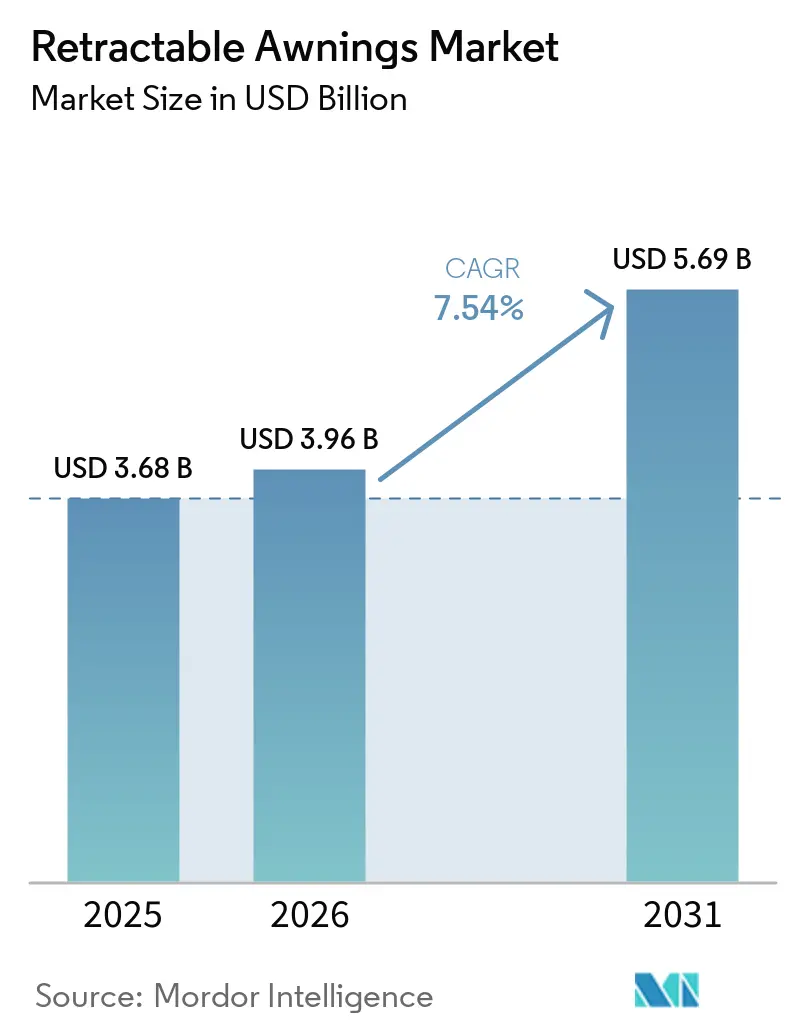

| Market Size (2026) | USD 3.96 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retractable Awnings Market Analysis by Mordor Intelligence

The Retractable Awnings Market size was valued at USD 3.68 billion in 2025 and is estimated to grow from USD 3.96 billion in 2026 to reach USD 5.69 billion by 2031, at a CAGR of 7.54% during the forecast period (2026-2031). Legislative changes in California and the European Union now recognize exterior shading as a measure of energy efficiency, increasing the demand for motorized and sensor-based systems. Rising construction costs in Japan and Australia have redirected capital toward retrofit solutions, which provide cooling savings while preserving existing facades. Post pandemic, hospitality operators have invested in outdoor revenue spaces, while homeowners increasingly view patios as essential living areas and actively pursue integration with smart-home ecosystems. These evolving trends have driven the retractable awnings market toward closer alignment with building automation, environmental certifications, and funding for performance-based renovations.

Key Report Takeaways

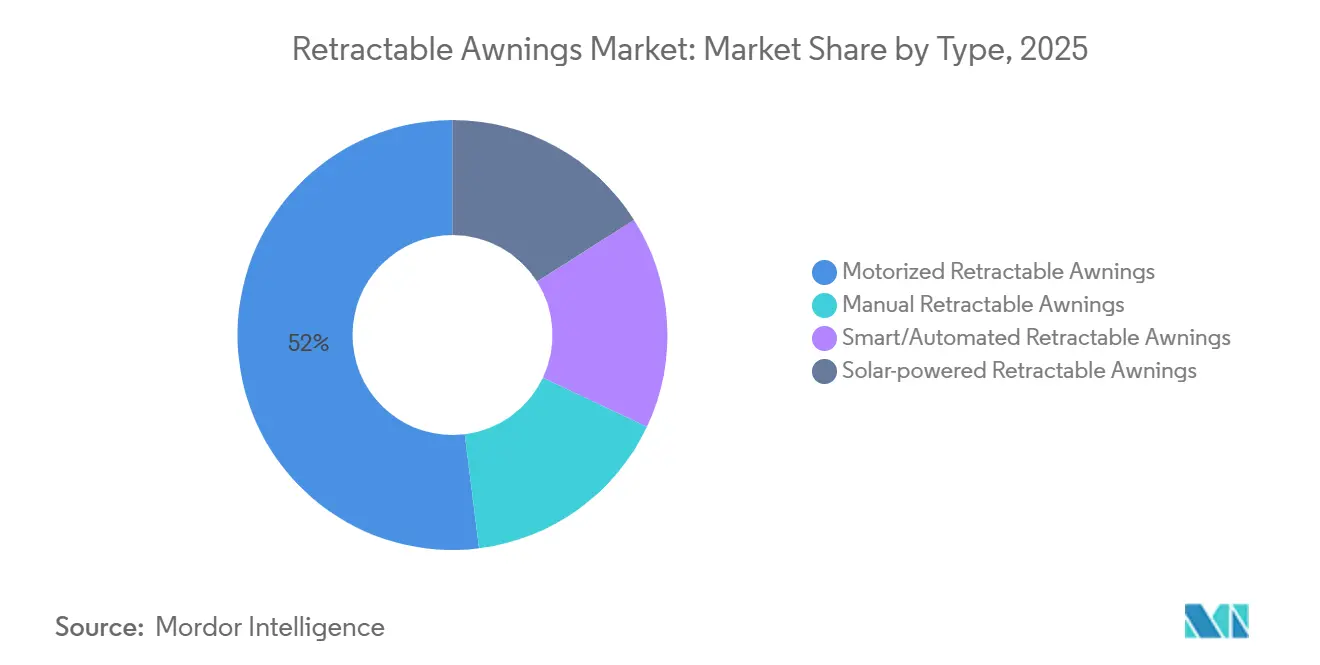

- By type, motorized units led with 51.97% of the retractable awnings market share in 2025, while smart and automated variants are expected to advance at an 8.37% CAGR between 2026 and 2031.

- By product category, patio formats accounted for 40.41% of the Retractable awnings market size in 2025; freestanding designs are expected to record the highest projected CAGR at 8.56% between 2026 and 2031.

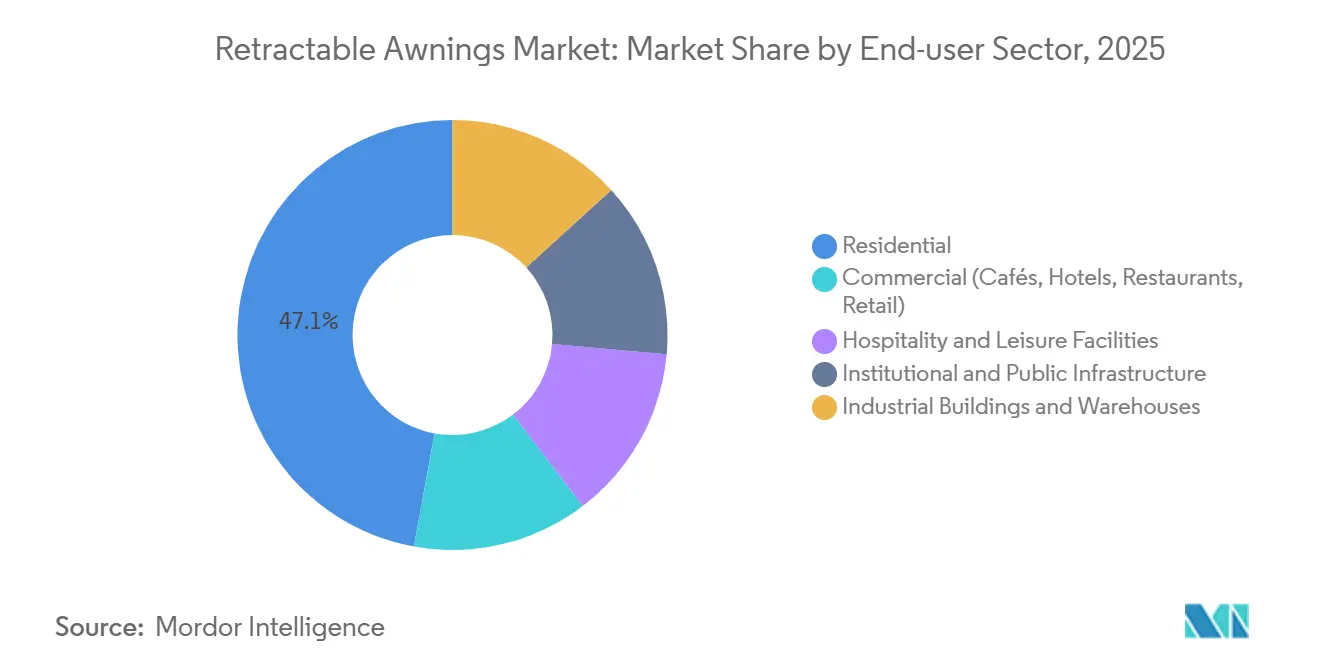

- By end-user sector, residential demand captured 47.13% share of the Retractable awnings market size in 2025, whereas commercial venues are expected to progress at an 8.90% CAGR between 2026 and 2031.

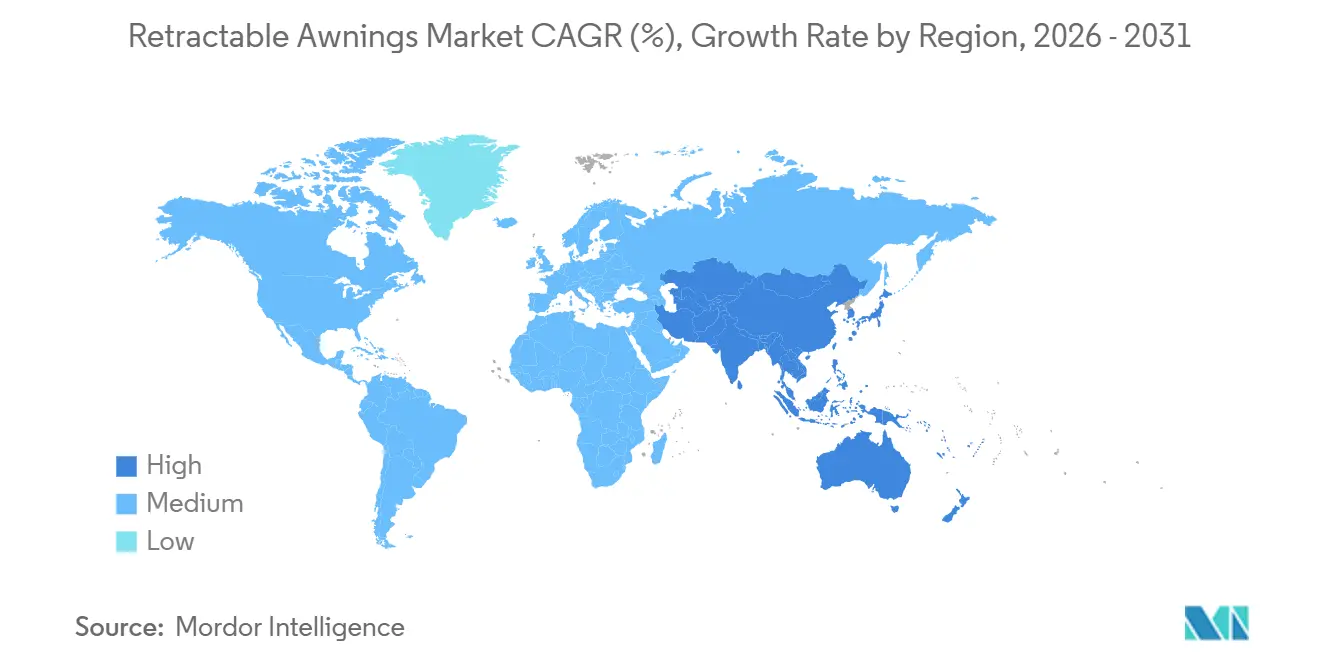

- By geography, North America commanded 38.41% of 2025 revenue, yet Asia-Pacific is forecast to grow at an 8.77% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retractable Awnings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of outdoor-living spaces in single-family homes | +1.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Heightened energy-efficiency codes spurring passive-cooling retrofits | +2.1% | Europe, California, APAC developed markets | Long term (≥ 4 years) |

| Smart-home ecosystem pulls for motorized and app-controlled shading | +1.5% | Global, strongest in North America and the EU | Short term (≤ 2 years) |

| Pandemic-accelerated "back-yard upgrading" for hospitality-at-home | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Government tax credits for exterior shading in green-building schemes | +1.1% | North America (commercial 179D), select EU member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Outdoor-Living Spaces in Single-Family Homes

Homeowners are increasingly treating patios and terraces as essential extensions of their living spaces. As real estate prices continue to rise, property owners are optimizing their existing spaces. Professional custom installations not only ensure structural integrity but also help to maintain warranties. There is a rising demand for eco-friendly fabrics, especially those made from recycled PET blends. Furthermore, with voice control features from leading smart-home assistants, awnings have evolved into programmable tools for climate management[1]Somfy Projects, “Automating Solar Shading Improves Facade Performance,” somfy.co.uk. Dealer networks are capitalizing on service revenues through annual maintenance programs. Collectively, these trends are driving a consistent premium demand in the retractable awnings market.

Heightened Energy-Efficiency Codes Spurring Passive-Cooling Retrofits

California's 2025 Title 24 update and the EU's Directive 2024/1275 are now incorporating exterior shading into their compliance software. This integration formalizes the budget allocations for retractable products in renovation passports. Consequently, commercial building owners are increasingly seeking dynamic shading solutions, targeting measurable reductions in their yearly energy consumption. Additionally, standardized life-cycle data and hourly performance metrics have emerged as crucial for product specification. Suppliers who effectively document their solar-heat-gain savings and improvements in daylight autonomy are positioned to secure a competitive advantage, ensuring their inclusion on energy-retrofit priority lists for the forecast period 2026–2031.

Smart-Home Ecosystem Pull for Motorized and App-Controlled Shading

Platforms such as Somfy TaHoma, Control4, and Q-SYS enable awnings to autonomously respond to sensor cues, mimic human activity, and heed utility demand signals. Installers can tailor features to meet client ROI expectations using a tiered pricing model: starting from basic motorization, moving to sensor automation, and culminating in full smart integration. Evidence from field studies indicates that automated shading can lead to significant reductions in HVAC cooling costs, which justifies the premium pricing. Furthermore, commercial plug-ins capable of managing up to forty motors from a single gateway not only simplify commissioning but also attract institutional buyers.

Pandemic-Accelerated Back-Yard Upgrading for Hospitality at Home

As hybrid work trends take hold and outdoor socializing continues to rise, spending on decks, pergolas, and balcony upgrades is expected to increase significantly. Awnings, now equipped with integrated heating strips and LED lighting, are enhancing patio usability during cooler evenings, effectively reducing payback periods. Fabric suppliers are emphasizing UPF ratings to protect outdoor furnishings, and many are extending warranty periods to five years or more. This trend reinforces the perception of awnings as durable fixtures rather than seasonal adornments. With discretionary funds previously allocated for travel now being redirected, homeowners are increasingly investing in permanent backyard assets, driving growth in the retractable awnings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs of motorized assemblies | -1.2% | Global, most acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Strong seasonality in cold and snow-prone regions | -0.7% | Northern Europe, Canada, northern U.S. states, Russia | Long term (≥ 4 years) |

| Low installer density in emerging economies | -0.6% | ASEAN, India, South America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Costs of Motorized Assemblies

Homeowners who are mindful of costs often avoid premium units, even when these units offer documented cooling savings. In addition to the initial premium, these homeowners face extra costs such as electrical coordination, control programming, and regular motor servicing. To address these concerns, vendors have introduced battery-powered and solar-powered motors. These advancements not only reduce the need for extensive cabling but also suggest lower energy bills. Furthermore, innovations such as the PowerView XL Motor, which features quieter drives and enhanced torque, have become more suitable for larger shades, making the price difference more justifiable[2]Caster Communications, “Hunter Douglas Enhances PowerView with Smarter Access,” castercomm.com.

Strong Seasonality in Cold and Snow-Prone Regions

Restaurants and cafés in Scandinavia, Canada, and the Northern United States can only fully utilize their spaces for six months each year, which compresses their revenue payback timelines. Winter snow loads require retraction and secure storage, while the spring surge places strain on installer capacities. In response to these challenges, manufacturers are improving wind-resistance ratings and promoting infrared heater options to extend patio seasons. However, despite these efforts, seasonality remains a significant challenge for the retractable awnings market during the forecast period of 2026–2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Smart Automation Drives Premium Tier Growth

Smart and automated systems are expected to grow at an 8.37% CAGR from 2026 to 2031, outpacing the broader retractable awnings market. By 2025, motorized units captured a notable 51.97% of the market revenue, highlighting their established presence. Although the market for solar-powered retractable awnings remains modest, it is witnessing rapid growth, driven by the labor-saving benefits of wiring-free installations. Sustainability metrics are becoming crucial in product specifications, with energy auditors using these details to assess retrofit ROI. Building owners are showing a preference for products that easily integrate with energy dashboards.

Additionally, features such as automated wind retraction are proving advantageous, as they reduce fabric replacement rates. These savings help justify the higher initial investment, leading to a greater adoption of smart models in multifamily, hospitality, and institutional sectors. However, in rental properties, where payback concerns are significant, manual formats remain dominant.

By Product Type: Freestanding Solutions Gain Traction

In 2025, patio installations accounted for 40.41% of total revenue. Freestanding structures, however, are experiencing significant growth, with an 8.56% CAGR projected for the forecast period of 2026–2031. This growth is primarily attributed to hotels and multifamily developers avoiding drilling into curtain-wall facades. Large-span models, extending up to 36 m² and featuring integrated lighting, are being transformed into modular outdoor rooms that can be repositioned with changing seasons. Additionally, vertical-drop formats of retractable awnings are gaining popularity in dense urban balconies, where projection clearance poses a challenge.

Window and door awnings provide specialized solutions for glare control, while pergola styles offer a combination of shading, rain protection, and ambient lighting. This diverse product portfolio not only expands the addressable market for vendors but also helps distributors bridge seasonal gaps effectively.

By End-User Sector: Commercial Hospitality Leads Growth

In 2025, residential buyers accounted for 47.13% of the demand, highlighting a longstanding tradition of backyard enhancements in the North-American and European regions. On the other hand, commercial venues, particularly cafés and hotels, are projected to expand at an 8.90% CAGR during the forecast period of 2026–2031, making the most of their outdoor spaces. While the retractable awnings market for institutions such as schools and libraries is modest, it has shown stability, with budget-sensitive entities favoring passive cooling methods over mechanical alternatives.

Hospitality operators have increasingly turned to RGB-capable lighting strips and integrated heaters, enabling evening services and extended usage during the shoulder season, which has subsequently boosted average selling prices. Furthermore, multifamily developers have incorporated balcony shading, not only to cater to tenant sustainability preferences but also to differentiate their rental offerings.

Geography Analysis

North America captured 38.41% of 2025's revenue, boasts a strong single-family homeownership rate, and a dense dealer network. In California, Title 24 compliance projects spotlighted real-time monitoring of automated shading, elevating awnings to measurable energy assets. While Canada's market faced seasonal ups and downs, Mexico enjoyed a steady year-round dining demand, making a strong case for permanent installations.

Asia-Pacific, with a projected CAGR of 8.77% during the forecast period of 2026 to 2031, is expected to emerge as the fastest-growing region in the retractable awnings market. Japan, Singapore, and Australia led the way, emphasizing smart-home integration and ESG financing for energy retrofits. As construction costs climbed, property owners turned to shading retrofits, enjoying cooling benefits without the burden of hefty capital expenses. Meanwhile, while India and ASEAN markets showed promise, they required installer training and localized support to fully realize their potential.

Europe's path was influenced by Directive 2024/1275, underscoring shading's role in energy certifications. In the competitive arena, Germany, France, and Italy took the lead, emphasizing design, while consumers gravitated towards recycled fabric collections. The Nordic regions, despite short summer seasons, capitalized on their high purchasing power and environmental awareness, and Southern Europe witnessed steady demand, largely fueled by the hospitality sector.

Competitive Landscape

The retractable awnings market is moderately consolidated. European brands are competing fiercely in the retractable awnings market, prioritizing design accolades, product lifecycle transparency, and smart-home system integration. New opportunities are emerging in solar-powered cassettes, mood lighting with programmable LEDs, and fabrics certified by the Global Recycled Standard and OEKO-TEX. As ESG investors intensify their focus on embodied emissions, lifecycle disclosures - such as verified carbon footprints for motors - are becoming crucial in procurement decisions. Vendors that effectively combine performance metrics with attractive designs and robust installer programs are positioned to outperform their smaller competitors in the near future.

Retractable Awnings Industry Leaders

SunSetter Products

Warema Renkhoff SE

markilux GmbH + Co. KG

Somfy Systems Inc

KE USA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Bloomin' Blinds formed a partnership with Somfy Systems Inc to embed motorized shading into its in-home service model, expanding smart-home options for the United States homeowners.

- April 2024: Thomas Sanderson launched a new range of smart electric pergola awnings. These awnings provide extensive shade and transform outdoor spaces into inviting rooms, ideal for entertainment, relaxation, or outdoor basking. These awnings are offered in 45 retractable fabric options with the luxury of optional LED lighting and heating.

Global Retractable Awnings Market Report Scope

A retractable awning is a versatile shading system consisting of a fabric canopy and a mechanical frame, designed to extend for sun and light rain protection or retract and roll away when not in use. It provides adjustable coverage without requiring a permanent structure.

The retractable awnings market is segmented by type, product type, end-user sector, and geography. By type, the market is segmented into manual retractable awnings, motorized retractable awnings, smart/automated retractable awnings, and solar-powered retractable awnings. By product type, the market is segmented into patio awnings, window awnings, door awnings, freestanding awnings, pergola awnings, and vertical-drop awnings. By end-user sector, the market is segmented into residential, commercial (cafés, hotels, restaurants, retail), hospitality and leisure facilities, institutional and public infrastructure, and industrial buildings and warehouses. The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Manual Retractable Awnings |

| Motorized Retractable Awnings |

| Smart/Automated Retractable Awnings |

| Solar-powered Retractable Awnings |

| Patio Awnings |

| Window Awnings |

| Door Awnings |

| Freestanding Awnings |

| Pergola Awnings |

| Vertical-drop Awnings |

| Residential |

| Commercial (Cafés, Hotels, Restaurants, Retail) |

| Hospitality and Leisure Facilities |

| Institutional and Public Infrastructure |

| Industrial Buildings and Warehouses |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Manual Retractable Awnings | |

| Motorized Retractable Awnings | ||

| Smart/Automated Retractable Awnings | ||

| Solar-powered Retractable Awnings | ||

| By Product Type | Patio Awnings | |

| Window Awnings | ||

| Door Awnings | ||

| Freestanding Awnings | ||

| Pergola Awnings | ||

| Vertical-drop Awnings | ||

| By End-user Sector | Residential | |

| Commercial (Cafés, Hotels, Restaurants, Retail) | ||

| Hospitality and Leisure Facilities | ||

| Institutional and Public Infrastructure | ||

| Industrial Buildings and Warehouses | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the Retractable awnings market in 2031?

The market is forecast to reach USD 5.69 billion by 2031 from USD 3.96 billion in 2026.

How fast is the Retractable awnings market growing between 2026 and 2031?

It is projected to expand at a 7.54% CAGR during the forecast period of 2026 to 2031.

Which product category is expanding fastest?

Freestanding systems are advancing at an 8.56% CAGR during the forecast period of 2026 to 2031 as hospitality venues seek modular shade solutions.

Which region shows the highest growth potential?

Asia-Pacific is poised for the fastest regional growth at an 8.77% CAGR during the forecast period of 2026 to 2031.

Why are smart and automated awnings gaining traction?

Building owners value integration with energy dashboards and automated wind retraction, which lowers HVAC costs and extends fabric life.

Page last updated on: