Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

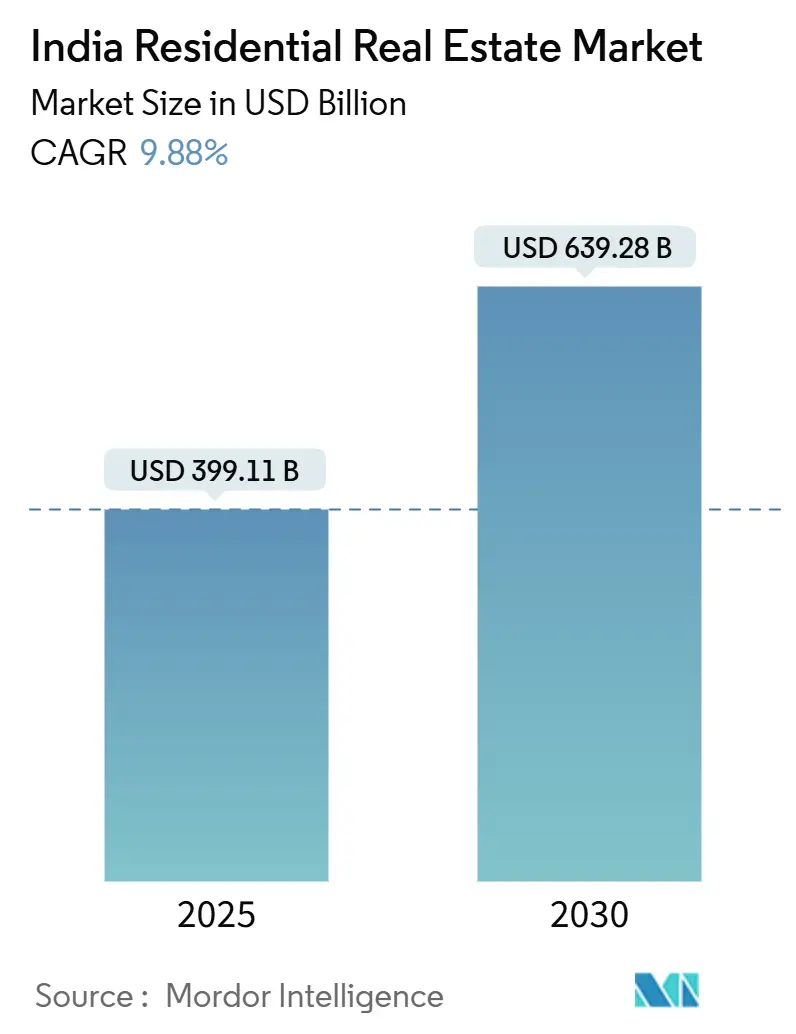

| Market Size (2025) | USD 399.11 Billion |

| Market Size (2030) | USD 639.28 Billion |

| Growth Rate (2025 - 2030) | 9.88% CAGR |

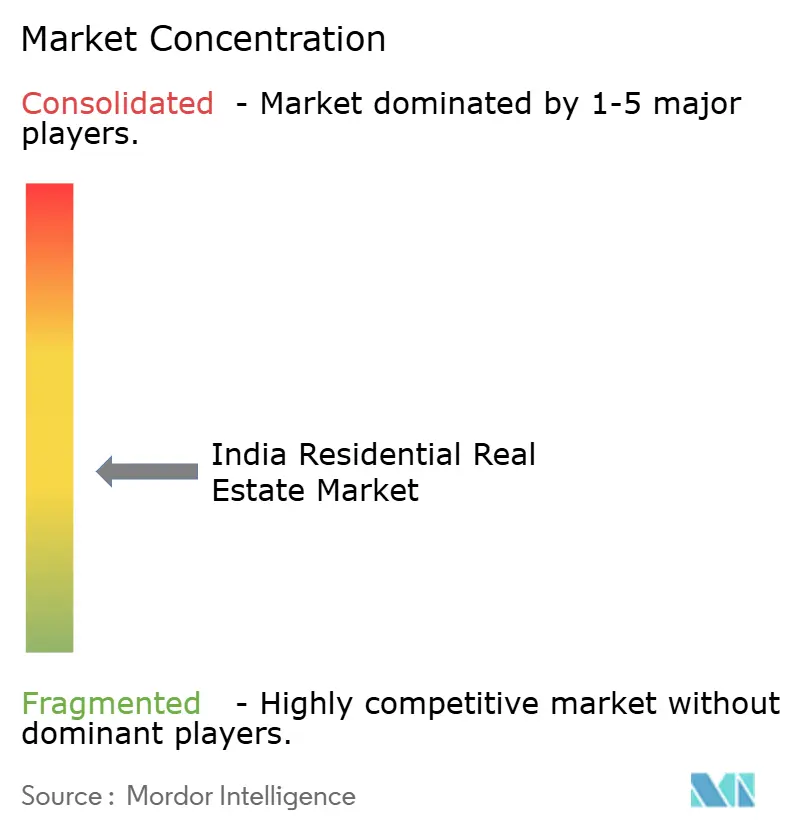

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Residential Real Estate Market Analysis by Mordor Intelligence

The India Residential Real Estate Market size is estimated at USD 399.11 billion in 2025, and is expected to reach USD 639.28 billion by 2030, at a CAGR of 9.88% during the forecast period (2025-2030). Demand is rising on the back of technology-sector hiring, government housing incentives, and lifestyle shifts toward larger dwellings in peripheral micro-markets. Faster approvals under PMAY-U and SWAMIH Fund deployment have unlocked stalled supply, while the June 2025 repo-rate reduction has lowered effective home-loan rates below 8%, improving affordability[1]Shaktikanta Das, “Monetary Policy Statement – June 2025,” Reserve Bank of India, rbi.org.in. Western India continues to lead transaction volumes, but East India is expanding fastest due to new infrastructure links and relatively low land costs. Developers are capturing suburban demand through township launches that pair apartments with plotted villas, indicating a decisive return to scale in the India residential real estate market.

Key Report Takeaways

- By region, Western India held 28% of India residential real estate market share in 2024, whereas East India is set to advance at a 10.58% CAGR through 2030.

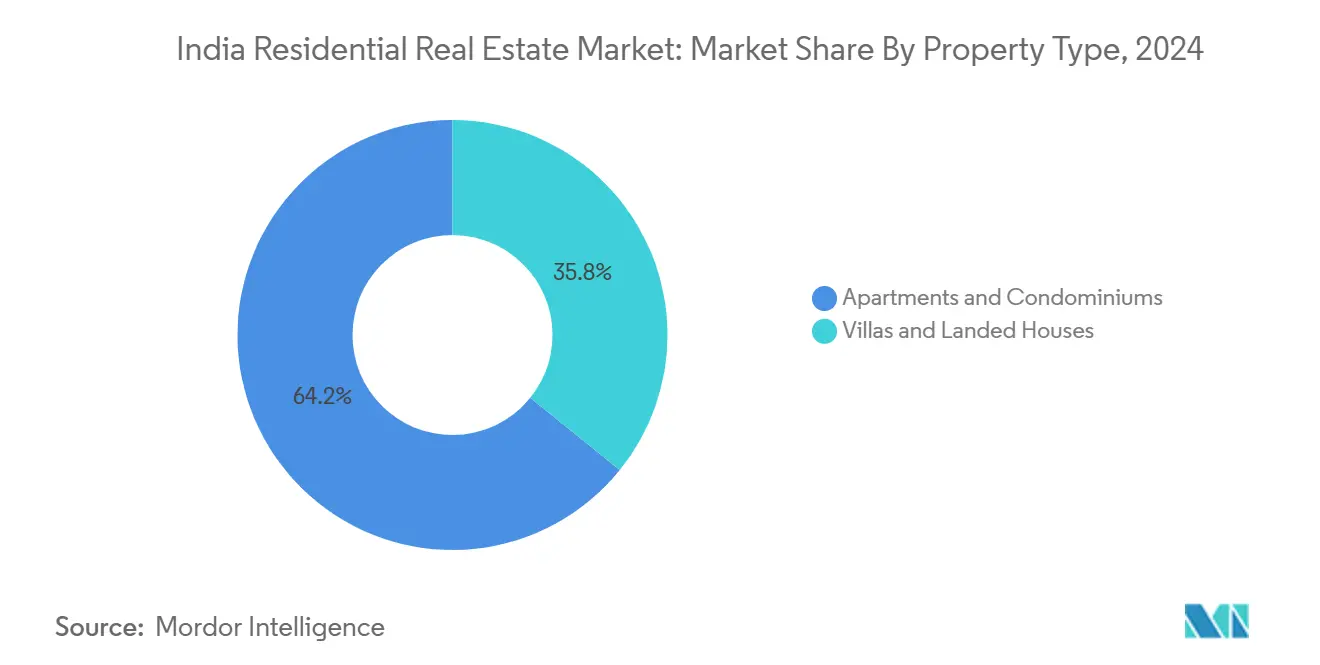

- By property type, apartments commanded 64.2% of India residential real estate market size in 2024; villas and landed houses are on track for a 10.30% CAGR through 2030.

- By price band, the mid-market segment captured 48% of India residential real estate market size in 2024, while affordable housing is forecast to expand at a 10.19% CAGR to 2030.

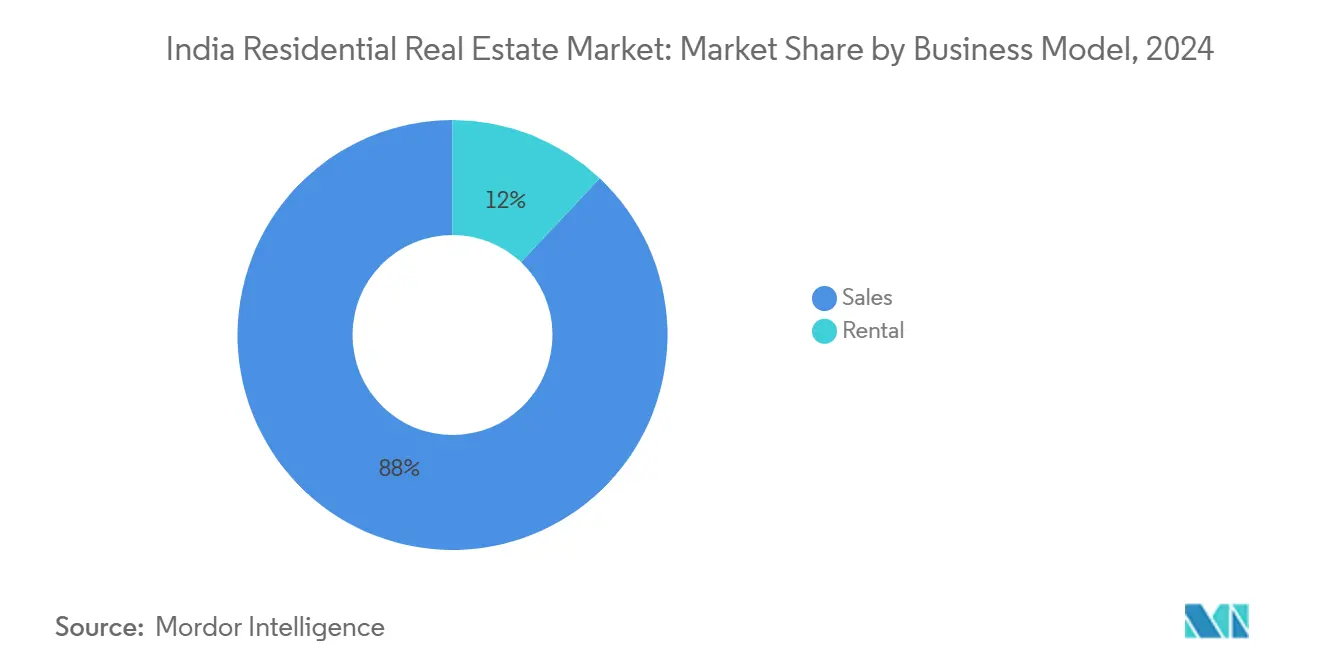

- By business model, sales transactions represented 88% of India residential real estate market size in 2024; rental activity is projected to accelerate at a 10.52% CAGR through 2030.

- By mode of sale, primary launches accounted for 64% of India residential real estate market size in 2024, with secondary transactions growing at an anticipated 10.42% CAGR to 2030.

India Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from IT/ITeS workforce concentrations in Bengaluru & Hyderabad driving mid-segment sales | +2.1% | South India and spillover cities | Medium term (2-4 years) |

| Expedited approvals under PMAY-U and SWAMIH Fund accelerating stalled affordable housing projects | +1.8% | National with early gains in NCR, MMR, and Bengaluru | Short term (≤ 2 years) |

| Rapid household nuclearization in urban India increasing unit absorption per 1,000 people | +1.5% | National, tier-1 and tier-2 cities | Long term (≥ 4 years) |

| Escalating interest from NRIs leveraging rupee depreciation to acquire premium homes in metros | +1.2% | Mumbai, Delhi-NCR, Bengaluru, Chennai | Medium term (2-4 years) |

| RERA-led transparency enhancing consumer confidence and sales velocity on digital platforms | +0.9% | National with higher impact in RERA-compliant states | Medium term (2-4 years) |

| Hybrid work model boosting peripheral suburb projects offering larger configurations | +0.7% | Metro peripheries and tier-2 cities | Long term (≥ 4 years) |

Source: Mordor Intelligence

Surging Demand from IT/ITeS Workforce Concentrations in Bengaluru & Hyderabad Driving Mid-segment Sales

Technology employment hubs have triggered localized demand surges that extend into suburban corridors of Bengaluru and Hyderabad. Hybrid work policies reinforce appetite for mid-segment apartments with home-office space, evidenced by a 4% rise in Bengaluru housing sales during H1 2024. Developers such as Prestige Group have responded with multi-tower launches in peripheral zones that offer improved amenities. Supply chain partners benefit from predictable volume pipelines, while municipal authorities accelerate infrastructure upgrades to sustain commuter flows. Continued momentum relies on persistent IT hiring and stable remote-working practices that keep mid-segment absorption elevated in the India residential real estate market.

Expedited Approvals under PMAY-U and SWAMIH Fund Accelerating Stalled Affordable Housing Projects

Government support has unlocked 90.25 lakh completed homes as of January 2025 and extended the scheme deadline to December 2025, aided by SWAMIH Fund financing that registered more than 6,500 apartments in Greater Noida[2]Manoj Joshi, “PMAY-U Progress Dashboard 2025,” Ministry of Housing & Urban Affairs, mohua.gov.in. Combined with PMAY-U 2.0’s Rs 10 lakh crore budget, these approvals shorten construction cycles and restore buyer confidence. Developers secure faster cash inflows, allowing rotation of capital into new phases. States that digitize permit workflows gain early household relocations, raising urban service demand and reinforcing property tax bases. The India residential real estate market therefore absorbs affordable units without re-introducing earlier execution risks.

Rapid Household Nuclearization in Urban India Increasing Unit Absorption per 1,000 People

City households are fragmenting into nuclear families that favor 2-3 BHK apartments. Sales across top eight metros reached an 11-year high of 1.73 lakh units in H1 2024, underscoring the demographic pivot. Developers refine apartment layouts to maximize natural light and storage within compact footprints. Mortgage lenders enlarge ticket-size bands that match salaried professional incomes, sustaining monthly installment affordability. This demographic driver has a multi-decade runway, ensuring that the India residential real estate market retains steady baseline demand even when cyclical factors soften.

Escalating Interest from NRIs Leveraging Rupee Depreciation to Acquire Premium Homes in Metros

Non-resident Indians have raised bookings for properties priced above Rs 5 crore, motivated by favorable exchange rates and long-term asset diversification. Luxury launches incorporate and market global quality benchmarks such as LEED certified materials and bespoke concierge services. Developers host virtual walk-throughs timed to overseas hours, shrinking decision cycles. Foreign currency inflows offset domestic funding gaps, adding depth to the India residential real estate market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently elevated input costs compressing developer margins and project launches | -1.4% | National with greater impact in infrastructure heavy regions | Short term (≤ 2 years) |

| Slow insolvency resolution for stressed projects prolonging supply overhang in NCR | -0.9% | NCR with spillover to other metro peripheries | Medium term (2-4 years) |

| High stamp duty and registration levies in key states dampening upgrade transactions | -0.8% | Maharashtra, Delhi, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Rising mortgage rates post-2022 pushing affordability index above 60 in tier-1 cities | -0.6% | Tier-1 cities with moderate impact elsewhere | Short term (≤ 2 years) |

Source: Mordor Intelligence

Persistently Elevated Input Costs Compressing Developer Margins and Project Launches

Steel and cement price stickiness has squeezed gross margins, forcing developers to widen premium inventory or slow affordable launches[3]Nandita Agarwal, “Input Cost Inflation and Project Viability,” National Real Estate Development Council (NAREDCO) White Paper, naredco.org.in. Affordable supply share fell to 18% in 2023 as material escalation outpaced consumer price sensitivity. Builders experiment with procurement cooperatives and contract indexation clauses to tame volatility. The India residential real estate market will reclaim lost momentum when commodity costs align with pre-COVID trends.

Slow Insolvency Resolution for Stressed Projects Prolonging Supply Overhang in NCR

Nearly 2.4 lakh delayed units constrain fresh launches because buyers hesitate to commit where legacy risks remain. Court-monitored completions such as NBCC’s Amrapali mandate for 22,000 flats aim to close the confidence gap. Progress depends on timely disbursal of resolution funds and municipal cooperation to release clearances. Faster clear-offs would free latent pent-up demand and normalize inventory levels in the India residential real estate market.

Segment Analysis

By Property Type: Apartment Dominance Drives Urban Density

Apartments & condominiums accounted for 64.2% of India residential real estate market share in 2024. High-rise formats fit land-scarce metros and enable shared utility costs. Developers capture scale economics through repeatable design templates, maintaining price points attractive to nuclear families. Villas & landed houses, although a smaller base, are forecast to rise at 10.30% CAGR, lifting India residential real estate market size for this segment. Post-pandemic preferences for private gardens and flexible indoor areas underpin demand. The hybrid work model legitimizes longer commutes, allowing villa buyers to choose peripheral plots where larger floorplates align with aspirational living.

The villa uptrend has prompted integrated townships that combine apartment towers, plotted developments, and recreational amenities. Such mixed-use formats diversify revenue and hedge project risk. For apartments, smart-home features and EV-charging infrastructure increasingly appear as standard, reinforcing consumer perceptions of value. In both cases, differentiated amenity packages remain the decisive factor that converts site visits to bookings, sustaining depth in the India residential real estate market.

By Price Band: Mid-Market Stability Anchors Growth

The mid-market tier held 48% of India residential real estate market size in 2024. Ticket sizes between Rs 40 lakh and Rs 1 crore align with white-collar income growth and favorable loan-to-value norms. This stability helps lenders keep delinquency rates low and encourages developers to prioritize volume. Affordable housing, projected to grow at 10.19% CAGR, benefits from PMAY-U subsidies and low-cost funding, yet margin stress persists because price ceilings tighten profit windows.

Listed developers have shifted toward premium and luxury projects where margin buffers absorb commodity shocks. Luxury bookings rose 49% year on year, aided by NRI inflows. Nonetheless, policy clarity on credit-linked subsidies and input tax rebates could re-accelerate affordable launches. Balanced execution across tiers keeps the India residential real estate market resilient across business cycles.

By Business Model: Sales Dominance Reflects Ownership Preferences

Sales transactions formed 88% of overall activity in 2024. Cultural preferences for tangible assets and tax deductions on mortgage interest maintain this skew. The rental sub-market, forecast to grow at 10.52% CAGR, gains from urban workforce mobility. Institutional landlords offer managed apartments with concierge and maintenance, attracting millennials and expatriates. Higher rental yields in select micro-markets provide investors a predictable cash flow alternative to traditional buy-and-sell strategies.

Digital lease management platforms enhance transparency and dispute resolution, encouraging participation by individual owners. Over time, increasing rental stock will moderate vacancy swings and deepen liquidity, improving the investment proposition across the India residential real estate industry.

By Mode of Sale: Primary Market Leadership Signals New Supply Confidence

Primary launches comprised 64% of activity in 2024, reflecting confidence in project execution post-RERA. Developers use milestone-linked payment plans to reduce buyer carrying costs. Better escrow monitoring ensures construction funds reach on-site deployment, improving trust. Secondary transactions, expected to grow at 10.42% CAGR, benefit from maturing housing stock and organized brokerage platforms that standardize documentation.

Healthy absorption of new projects and active resale liquidity create a virtuous cycle, attracting capital from domestic and overseas investors. The India residential real estate market therefore enjoys diversified transaction pathways that cushion cyclical demand swings.

Geography Analysis

Western India retained 28% of India residential real estate market size in 2024, anchored by Mumbai Metropolitan Region and Pune. Mumbai registered 1.41 lakh property deeds in 2024, with western suburbs accounting for 53% of December registrations. Upcoming infrastructure projects such as the Navi Mumbai International Airport and east-west metro corridors improve multi-node connectivity and unlock previously under-served precincts. Redevelopment of large precincts like Dharavi, where 43% of 108.99 hectares is earmarked for free sale, adds transformative inventory that renews investor attention.

South India benefits from Bengaluru’s technology corridor and Chennai’s industrial diversification. Hybrid work policies enlarge feasible residential catchments around Outer Ring Road and Whitefield. Hyderabad’s life-sciences cluster is another magnet for skilled migrants, spurring township launches by national developers. NRI remittances favor south-based projects due to perceived governance quality and historical rental yield consistency. These factors keep absorption velocity high and reduce unsold inventory in the India residential real estate market.

East India leads in growth with a 10.58% forecast CAGR through 2030. Kolkata’s average prices range between Rs 2,503 and Rs 8,242 per square foot, offering affordability relative to coastal metros. Upgrades to suburban rail and arterial roads shorten commuting time, boosting end-user sentiment. Simultaneously, Central India, typified by Indore, witnesses price escalations as commercial footprints expand. Godrej Properties’ Rs 200 crore land acquisition in Indore signals institutional confidence. Tier-2 corridors thus emerge as new growth poles, distributing demand more evenly across the India residential real estate market.

Competitive Landscape

The market shows moderate fragmentation, with top regional developers commanding city-specific mindshare while national brands scale via aggressive land banking. Godrej Properties allocated Rs 21,000 crore for acquisitions in FY 2025, targeting multi-city expansion. Adani Group is in advanced talks to acquire Emaar India for USD 1.5 billion, exemplifying ongoing consolidation. Embassy Group’s merger with Equinox India has pooled complementary land reserves and streamlined capital structure.

Players pursue margin defense by pivoting to premium offerings and employing design-build-operate models that reduce project risk. Digital engagement tactics such as virtual site visits and AI-based lead scoring shorten sales cycles. Institutional investors deepen funding channels, as Blackstone’s Rs 3,250 crore purchase of South City Mall confirms confidence in the wider property ecosystem.

Competitive advantage increasingly rests on execution track record, balance-sheet strength, and the ability to synchronize launches with infrastructure roll-outs, ensuring sustained traction in the India residential real estate market.

India Residential Real Estate Industry Leaders

-

Godrej Properties

-

Prestige Estate

-

DLF

-

Phoenix Mills

-

L&T Realty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Reserve Bank of India reduces the repo rate to 5.5%, pushing home-loan rates below 8%.

- May 2025: Maharashtra Housing and Area Development Authority allocates Rs 9,202 crore for 19,497 affordable units to be offered in a Diwali lottery.

- March 2025: Adani Group enters advanced talks to buy Emaar India for USD 1.5 billion.

- January 2025: Godrej Properties acquires a 24-acre parcel in Indore for Rs 200 crore, extending its tier-2 footprint.

India Residential Real Estate Market Report Scope

Residential real estate is an area developed for people to live in. As local zoning ordinances define, residential real estate cannot be used for commercial or industrial purposes. A complete background analysis of the Indian residential real estate market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, is included in the report.

The Indian residential real estate market is segmented by type (condominiums and apartments, villas, and landed houses). The report offers market size and forecasts in values (USD) for all the above segments.

| By Property Type | Apartments & Condominiums |

| Villas & Landed Houses | |

| By Price Band | Affordable |

| Mid-Market | |

| Luxury | |

| By Business Model | Sales |

| Rental | |

| By Mode of Sale | Primary (New-Build) |

| Secondary (Existing Home Resale) | |

| By Region | North India |

| South India | |

| West India | |

| East India | |

| Central India |

By Property Type

| Apartments & Condominiums |

| Villas & Landed Houses |

By Price Band

| Affordable |

| Mid-Market |

| Luxury |

By Business Model

| Sales |

| Rental |

By Mode of Sale

| Primary (New-Build) |

| Secondary (Existing Home Resale) |

By Region

| North India |

| South India |

| West India |

| East India |

| Central India |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the India residential real estate market?

The market is valued at USD 399.11 billion in 2025 and is forecast to reach USD 639.28 billion by 2030.

Which property type leads sales volumes?

Apartments and condominiums hold a 64.2% share, reflecting urban density and land economics.

Which region is growing fastest?

East India is projected to expand at a 10.58% CAGR through 2030, driven by infrastructure upgrades and affordable land.

How have recent interest-rate changes affected demand?

The June 2025 repo-rate cut to 5.5% pushed home-loan rates below 8%, improving affordability and stimulating bookings across tier-1 and tier-2 cities.

Page last updated on: June 19, 2025