Refinery Catalysts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.19 Billion |

| Market Size (2031) | USD 7.82 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

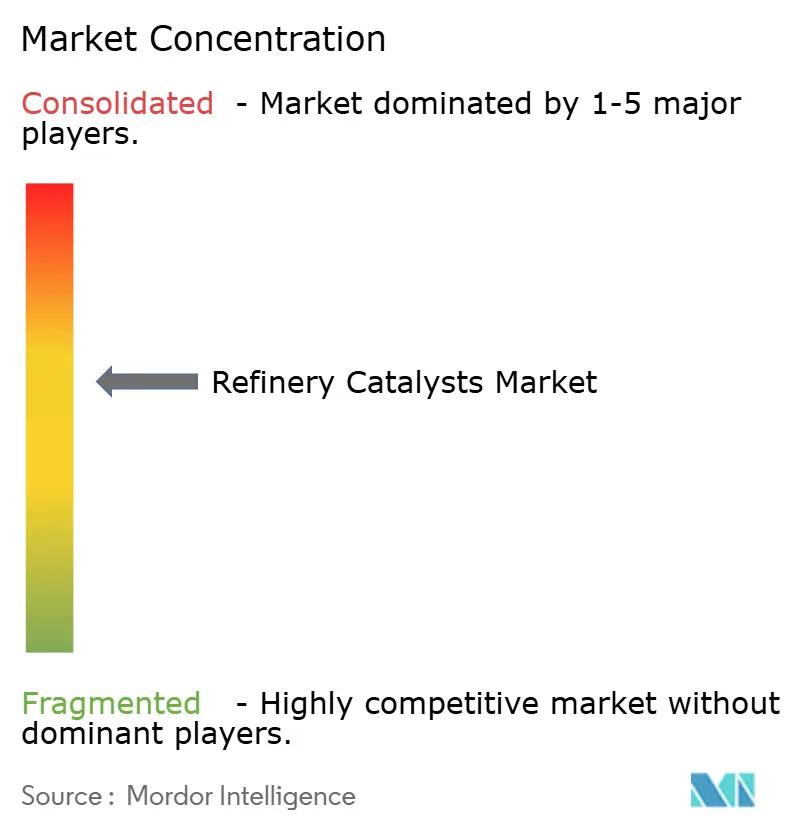

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refinery Catalysts Market Analysis by Mordor Intelligence

The Refinery Catalysts Market size is expected to increase from USD 5.73 billion in 2025 to USD 6.19 billion in 2026 and reach USD 7.82 billion by 2031, and is expected to grow at a CAGR of 4.79% over 2026-2031. Sulfur-compliance programs tie hydrotreating and hydrocracking catalyst replacement to regulation rather than to short-term crude price swings, supporting steady demand. Capacity additions in Asia-Pacific and the Middle East are broadening catalyst consumption across new and upgraded refinery units. The refinery catalyst market is shifting toward more complex formulations as refineries integrate fuel production with petrochemical output and seek higher yields per unit. This is creating a split between large-volume replacement catalysts, where manufacturing scale and supply reliability matter, and premium-performance catalysts bundled with digital monitoring tools and outcome-based service models. The market is supported by both regulatory demand and higher-value service-led offerings, even as customer buying patterns become more selective.

Key Report Takeaways

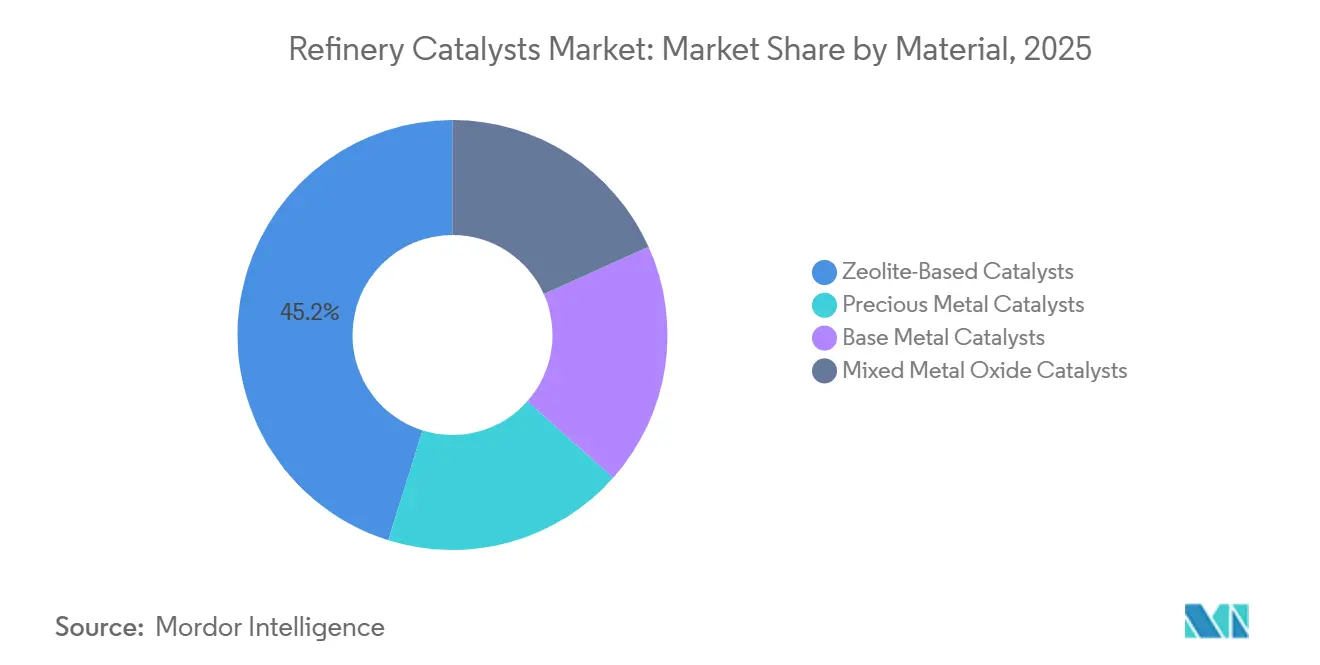

- By material, zeolite-based catalysts led with a 45.17% share in 2025, while mixed-metal oxide catalysts are projected to grow at a 5.52% CAGR through 2031.

- By process, fluid catalytic cracking accounted for 36.22% of demand in 2025, while hydrocracking is forecast to expand to 5.84% CAGR through 2031.

- By application, gasoline production accounted for 38.81% of demand in 2025, while jet fuel production is projected to grow at a 5.66% CAGR through 2031.

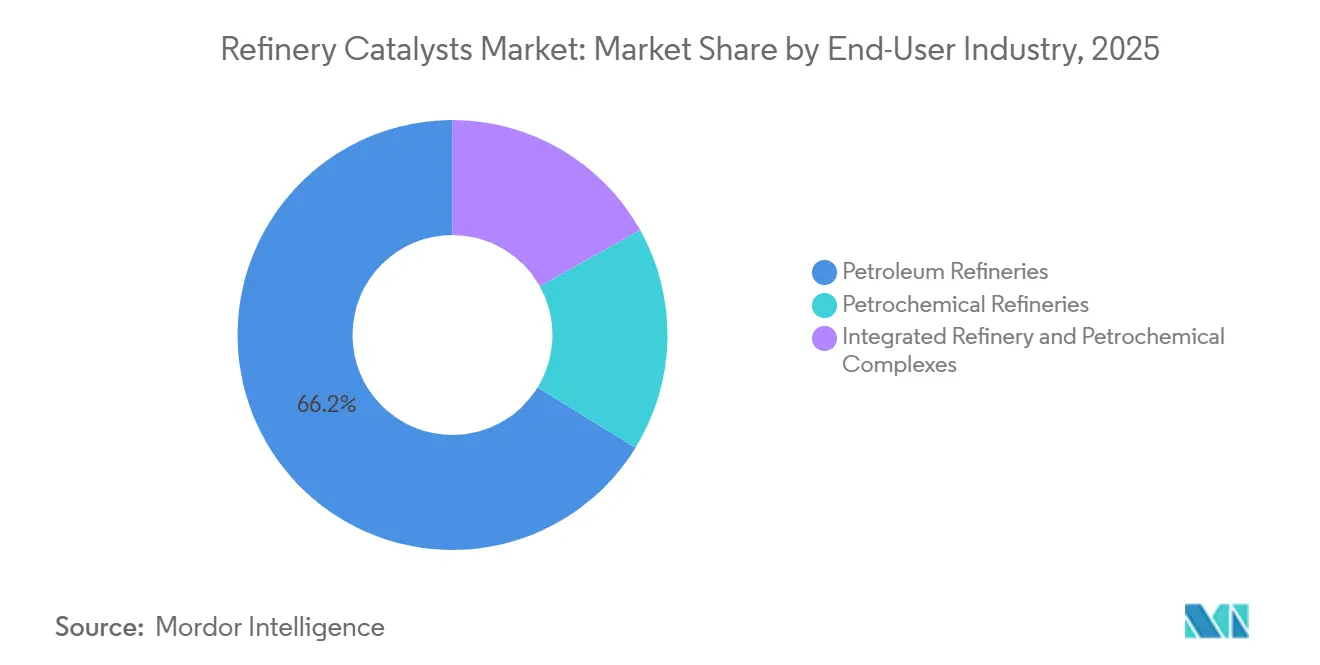

- By end-user industry, petroleum refineries accounted for 66.21% of demand in 2025, while integrated refinery and petrochemical complexes are expected to grow at 5.72% CAGR through 2031.

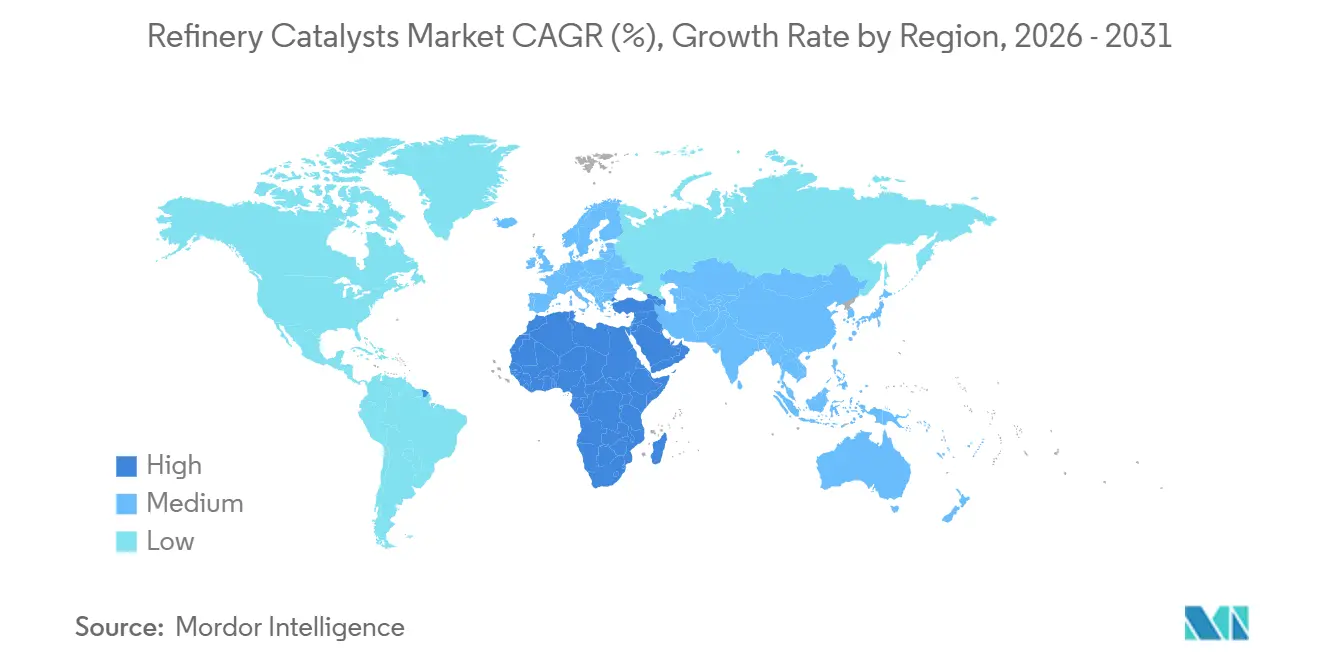

- By geography, Asia-Pacific accounted for 39.11% of demand in 2025, while the Middle East and Africa are projected to grow at a 5.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refinery Catalysts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Sulfur Regulations | +1.5% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Refinery Conversion Technologies | +0.9% | Global, with early gains in the Middle East and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for High-Value Products | +0.8% | Asia-Pacific core, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Cycle Length Optimization | +0.5% | Global | Long term (≥ 4 years) |

| Digital Catalyst Monitoring | +0.4% | North America and Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Co-Processing of Bio-Based Feedstocks | +0.4% | Europe and North America, with adoption emerging in Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Sulfur Regulations

Sulfur regulations are creating a durable demand floor for the refinery catalysts market by keeping hydrotreating, hydrodesulfurization, and hydrocracking activity closely tied to compliance requirements. The International Maritime Organization sulfur cap continues to support demand for high-activity hydrodesulfurization catalysts used in marine fuel production. In the United States, Tier 3 fuel standards keep gasoline sulfur content below 10 ppm, supporting ongoing naphtha hydrotreating catalyst replacement across North American assets[1]U.S. Environmental Protection Agency, “Tier 3 Motor Vehicle Emission and Fuel Standards,” U.S. Environmental Protection Agency, epa.gov. The same pattern is evident in China and India, where stricter fuel-quality rules and large refinery systems continue to favor higher-activity NiMo and CoMo formulations. These units cannot delay the use of compliant catalysts once fuel specifications are enforced. A further replacement wave could emerge if sulfur limits tighten in emission control areas, extending the regulatory pull on advanced hydroprocessing catalysts.

Rising Demand for High-Value Products

A shift in refinery spending toward better product quality and broader petrochemical integration is also supporting the refinery catalysts market. Asia is expected to account for 40% of global crude distillation unit capacity additions between 2026 and 2030, and India alone is expected to add nearly 2.3 million barrels per day of refining capacity by 2030. This scale of investment increases catalyst demand across cracking, treating, and conversion units rather than only in one process area. Jet fuel is the fastest growing application in the report, reflecting both aviation recovery and the push to support sustainable aviation fuel blending through existing refinery systems. Integrated refinery and petrochemical complexes are also growing faster than conventional end users, requiring suppliers to improve propylene, ethylene, and fuel yields simultaneously. The refinery catalysts market is therefore shifting toward customers that value formulation depth and refinery-specific optimization over standard replacement supply.

Digital Catalyst Monitoring

Digital catalyst monitoring is becoming more commercial, moving the refinery catalysts market toward service-led competition. In May 2026, Ketjen partnered with Imubit to launch real-time catalyst intelligence through the iKet Connect portal, linking refinery operating data with Ketjen formulation models and laboratory inputs. This gives refiners a clearer view of catalyst condition, replacement timing, and unit-level performance compared to periodic manual review. A 2025 study in the International Journal of Applied Mathematics showed that machine learning-based catalyst scheduling can combine soft sensing, life forecasting, and prescriptive optimization to maintain process stability across simulated runs. As a result, the refinery catalysts market is seeing suppliers generate recurring revenue from performance support in addition to physical replacement volumes. This dynamic also raises switching costs, as the data history associated with a supplier's platform becomes part of the operating value proposition.

Co-Processing of Bio-Based Feedstocks

Co-processing of bio-based feedstocks in existing hydrotreater and hydrocracker units is adding a new demand layer to the refinery catalysts market. The International Civil Aviation Organization (ICAO) identifies co-processing as a lower-capital route to sustainable aviation fuel production, supporting interest in catalyst systems that can process used cooking oils, animal fats, and other renewable inputs. Ketjen has developed its ReNewFine catalyst portfolio to fit into existing hydrotreaters while maintaining cycle length and yield performance. A 2025 study in Environmental Science & Technology found that co-processing bio-based intermediates at petroleum refineries can be a cost-effective route to certified sustainable aviation fuel. A 2026 study in Fuel noted that phenol derivatives in pyrolysis bio-oil remain difficult to handle in conventional co-processing without deeper pretreatment, highlighting a formulation challenge ahead. The refinery catalysts market is therefore seeing both a growth opportunity and a technical barrier emerge from the same trend toward renewable feedstocks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precious and Base Metal Price Volatility | -0.8% | Global, concentrated in regions reliant on imported platinum group metals | Short term (≤ 2 years) |

| Long Qualification Cycles | -0.5% | Global | Long term (≥ 4 years) |

| Slower Capex in Mature Markets | -0.4% | Europe and North America | Medium term (2-4 years) |

| Unit-Specific Performance Requirements | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precious and Base Metal Price Volatility

The refinery catalysts market faces immediate financial pressure from price swings in platinum group metals and other catalyst metals. Reforming and hydroisomerization catalysts are particularly exposed due to their dependence on high-value metal systems, which can shift procurement economics. When metal prices rise, refiners tend to increase regeneration, recover metal, and reuse existing catalyst before committing to new purchases. This approach protects customer budgets but limits new catalyst volume demand in affected product lines. As a result, the market faces a margin squeeze on the supplier side and purchase timing risk on the refinery side simultaneously. This pressure is most pronounced in applications where customers have flexibility to extend cycle life or reclaim value from spent catalyst inventories.

Long Qualification Cycles

New catalyst formulations face a barrier in the refinery catalysts market, as commercial approval at the unit level can take 12 to 36 months. Each refinery unit has its own feedstock, pressure profile, temperature range, metallurgy, and operating history, meaning a successful formulation at one site does not automatically transfer to another. This slows revenue conversion for new entrants and gives established suppliers an advantage through pre-qualified product libraries. Consequently, the share of the installed base that is open to replacement each year is smaller than the total base would suggest. Refiners generally prefer a known performance profile when managing compliance and uptime risk, even when alternatives appear attractive on paper. Innovation remains important, but commercial gains tend to materialize slowly unless the supplier already has an established track record with the customer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Zeolite Catalysts Anchor Demand Amid Mixed Oxide Momentum

Zeolite-based catalysts held 45.17% of the refinery catalyst market share in 2025, making them the dominant material category. Their position reflects strong selectivity in fluid catalytic cracking (FCC), particularly for gasoline and propylene production across the global installed base of refineries. The refinery catalysts market continues to rely on zeolite systems because they align with the scale, severity, and regeneration patterns of large cracking units. A 2025 study in Advances in Industrial and Engineering Chemistry found that hierarchical ZSM-5 structures improved catalytic activity for larger hydrocarbon molecules compared with conventional microporous forms. This is relevant because refiners seek stronger cracking performance without departing from proven zeolite families.

Precious metal catalysts remain important for reforming and hydroisomerization, where octane uplift and product-quality targets are demanding. Base-metal catalysts built around cobalt, molybdenum, nickel, and tungsten also remain essential across hydroprocessing units, with demand shifting toward more active nickel-molybdenum (NiMo) systems for heavier, higher-sulfur feedstocks. The refinery catalysts market is also seeing growing interest in mixed-metal oxide catalysts, which are forecast to expand at a 5.52% CAGR through 2031. These systems are valued for combining acid sites, redox behavior, and thermal stability in ways that suit integrated refinery and petrochemical operations. A 2025 ChemCatChem study on lanthanum-modified HY, HBETA, and HZSM-5 materials demonstrated how hybrid formulations can support selective gasoline desulfurization in FCC risers. The refinery catalysts market is therefore moving toward materials that do not fit neatly into a single traditional category, as refiners increasingly seek multifunctional performance from the same catalyst family.

By Process: FCC Retains Leadership While Hydrocracking Delivers Faster Growth

Fluid catalytic cracking accounted for 36.22% of demand in 2025, making it the largest process segment in the refinery catalysts market. Its lead reflects the scale of FCC unit installations and the continuous catalyst addition and withdrawal built into normal operation. The refinery catalysts market depends heavily on FCC because it remains a major route to gasoline and propylene output in complex refining systems. BASF reinforced that position in May 2026 by opening a new applied research and development center for FCC catalysts in Attapulgus, Georgia, adjacent to its largest global refinery catalyst manufacturing site[2]BASF SE, “BASF Boosts Refinery Catalyst Innovation With New R&D Center in Attapulgus, Georgia,” BASF SE, basf.com. That move indicates that suppliers continue to see value in improving FCC formulations for conventional heavy oils and lower-carbon feed streams.

Hydrotreating and catalytic reforming continue to represent major supporting volumes, with NiMo and CoMo systems dominating treating applications and platinum-on-alumina systems anchoring reforming needs. Hydrocracking is the fastest-growing process in the refinery catalysts market, with a 5.84% CAGR through 2031, supported by demand for ultra-low-sulfur diesel, jet-grade kerosene, and lubricant base stocks from heavier feeds. This growth is attracting attention because hydrocracking performance depends on the balance between cracking and hydrogenation, which raises the commercial value of formulation quality. The refinery catalysts market also plays a smaller but strategic role in isomerization and alkylation catalysts, as refiners continue to require high-octane blending components under tighter fuel quality regulations. Process demand is therefore distributed across both large established conversion units and premium specialty applications, favoring suppliers that can support high-throughput commodity systems while maintaining margins in technically demanding units.

By Application: Gasoline Holds Scale While Jet Fuel Expands Faster

Gasoline production accounted for 38.81% of demand in 2025, making it the largest application in the refinery catalysts market. This reflects the size of the existing motor fuel pool and the catalyst requirements associated with hydrotreating, FCC, and catalytic reforming across the global refinery fleet. Diesel remained the second-largest application and continued to require significant catalyst spending in hydrotreating and hydrocracking, particularly in markets enforcing very low sulfur specifications. Lubricants and petrochemical feedstocks remained smaller in volume but supported premium catalyst pricing because their product specifications are narrower and less forgiving.

Jet fuel is the fastest-growing application in the refinery catalysts market, with a 5.66% CAGR projected through 2031. This reflects the combined effect of aviation traffic recovery and the need to develop practical routes for sustainable aviation fuel through existing refining assets. The International Civil Aviation Organization (ICAO) has identified co-processing as a lower-capital path for refinery-based sustainable aviation fuel production, directly supporting catalyst demand in hydroprocessing units. A 2025 study in Environmental Science & Technology also found that co-processing at petroleum refineries can be a cost-effective certified pathway for sustainable aviation fuel. The refinery catalysts market is therefore seeing jet fuel shift from a standard distillate outlet to a premium catalyst demand segment with distinct selectivity and metal loading requirements. Other applications will continue to grow, but jet fuel now exerts a stronger incremental pull on advanced hydroprocessing systems.

By End-User Industry: Petroleum Refineries Lead While Integrated Complexes Accelerate

Petroleum refineries accounted for 66.21% of demand in 2025, giving them the largest end-user position in the refinery catalysts market. Their lead reflects the scale of conventional refining infrastructure across Asia-Pacific, North America, and the Middle East, as well as the number of catalyst-consuming units in a full-complexity refinery. The refinery catalysts market depends on these operators because they purchase across cracking, treating, reforming, and support processes rather than within a single narrow application. Petrochemical refineries remain a smaller but technically demanding outlet, particularly in units designed for ethylene, propylene, and aromatics production. This customer base tends to prioritize specialized formulation performance and product slate control over simple replacement volume.

Integrated refinery and petrochemical complexes are projected to grow at a 5.72% CAGR through 2031, making them the fastest-growing end-user category in the refinery catalysts market. This pattern reflects a broader downstream shift in which national oil companies pursue chemical revenue streams alongside fuels output. In December 2024, Aramco and ExxonMobil signed a venture framework agreement to evaluate an expansion of a new petrochemical complex tied to the SAMREF refinery in Yanbu, Saudi Arabia. Projects of this type are significant because they bring catalyst packages for FCC, hydrocracking, and reforming together at a single site rather than across separate units. The refinery catalysts market is well-positioned for this customer group because integrated assets require both larger site-level volumes and more complex performance targets. That combination gives suppliers a stronger basis for offering long-term technical support and performance-based digital services alongside formulation supply.

Geography Analysis

Asia-Pacific accounted for 39.11% of the global refinery catalyst market share in 2025, making it the largest regional demand center. The region leads due to a combination of refinery capacity additions, stricter fuel specifications, and a shift toward integrated refining and petrochemical systems. OPEC expects Asia to account for 40% of global crude distillation unit capacity additions between 2026 and 2030, with India alone expected to add nearly 2.3 million barrels per day by 2030. This scale provides a strong base for both conversion catalysts and compliance-driven hydroprocessing systems. Japan and South Korea support demand through higher-complexity refining and petrochemical integration, even though throughput growth in these markets is more mature.

North America remains a technical center for the refinery catalysts market, as regulatory compliance, renewable fuel integration, and advanced formulation work continue to drive catalyst upgrades. EPA Tier 3 fuel standards keep sulfur-reduction efforts ongoing across U.S. gasoline production systems. BASF reinforces the region's role in formulation development through its Attapulgus research and manufacturing base, which will support next-generation Fluid Catalytic Cracking (FCC) catalyst development in 2026. Europe follows a different path, with slower refinery capital spending but more focused catalyst activity around digital monitoring and co-processing of renewable feedstocks. South America represents a steadier demand base, where specialized hydroprocessing needs in countries such as Brazil support quality-driven consumption even without major new capacity additions.

The Middle East and Africa are forecast to post the fastest refinery catalysts market CAGR of 5.84% through 2031. Growth is driven by Saudi Arabia's downstream expansion agenda, ADNOC's integrated strategy, and a broader push to localize higher-value refining inputs. In April 2025, Axens expanded its Axens Catalyst Arabia Limited facility in Saudi Arabia, becoming the first company to manufacture tail gas treatment catalysts in the region, with sulfur recovery capability of up to 99.9%. In March 2026, Ketjen and Saudi Aramco Technologies Company signed a joint development agreement to co-develop next-generation FCC catalysts for Aramco refineries. Refinery projects in African markets such as Nigeria, Kenya, and Tanzania add a longer-term growth layer, with regional demand expected to widen as import substitution programs advance.

Competitive Landscape

The refinery catalysts market is moderately consolidated at the technology tier, with BASF, W. R. Grace, Honeywell UOP, Johnson Matthey, Haldor Topsoe, and Albemarle forming the main group of established global suppliers. Their positions are supported by proprietary zeolite synthesis, multi-metal formulation expertise, testing infrastructure, and long refinery qualification histories. Market entry is difficult for new players because performance validation takes time, and each customer site has a distinct operating profile. Domestic Chinese suppliers are gaining ground in cost-focused FCC applications for local demand, but higher-performance hydroprocessing and specialty reforming catalysts continue to favor global incumbents. As a result, price competition is stronger in standard replacement segments than in premium formulation categories.

Recent developments illustrate how established suppliers are positioning themselves in the market. BASF opened a new fluid catalytic cracking (FCC) catalyst research and development center in Attapulgus, Georgia, in May 2026. In the same month, Ketjen announced a partnership with Imubit, connecting catalyst expertise with real-time optimization and digital monitoring through the iKet Connect platform. In March 2026, Ketjen also signed a joint development agreement with Saudi Aramco Technologies Company, demonstrating how suppliers are using co-development to secure early adoption in major refining systems. These moves indicate that competition in the refinery catalysts market extends beyond catalyst chemistry to include data access, site-level optimization, and closer integration with customer operating decisions.

Opportunities remain in the refinery catalysts market for mixed bio- and petroleum-based feedstock solutions, as no supplier has established a dominant position in that emerging application. A similar gap exists in integrated regeneration service management, where value continues to shift between catalyst manufacturers and third-party regeneration providers. Data accumulation is also reshaping the competitive landscape, as each monitored unit provides the platform owner with improved performance feedback for future recommendations. This creates a structural advantage that formulation-only competitors cannot replicate quickly, even when their chemistry is strong. Suppliers with credible digital tools therefore gain more than a service layer; they gain stronger customer retention and a clearer path to performance-linked pricing. Competitive intensity remains high, but the strongest players are broadening their advantage through services and co-development rather than relying solely on product offerings.

Refinery Catalysts Industry Leaders

Albemarle Corporation

W. R. Grace and Co.

BASF

Haldor Topsoe A/S

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BASF opened a new R&D center for FCC catalyst development in Attapulgus, Georgia, co-located with its largest global refinery catalyst manufacturing facility. The center focuses on applied research into next-generation FCC formulations for lower-carbon and circular feedstocks, with integrated quality assurance laboratories designed to accelerate technology scale-up.

- May 2026: Ketjen partnered with Imubit to launch real-time catalyst intelligence services through the iKet Connect portal, integrating Ketjen's proprietary catalyst models and laboratory data with Imubit's closed-loop AI platform for FCC and hydroprocessing units. Pilot deployments are active with customers in North America and Europe, with expansion to additional regions planned for the remainder of 2026.

Global Refinery Catalysts Market Report Scope

Refinery catalysts are specialized materials used in petroleum processing to accelerate chemical reactions, converting heavy crude oil into high-value products such as gasoline, diesel, and petrochemical feedstocks. Key processes include Fluid Catalytic Cracking (FCC), hydrotreating, and catalytic reforming, which utilize porous zeolite or metal-based catalysts.

The refinery catalysts market is segmented by material, process, application, end-use industry, and geography. By material, the market is segmented into zeolite-based catalysts, precious metal catalysts, base metal catalysts, and mixed metal oxide catalysts. By process, the market is segmented into fluid catalytic cracking, hydrotreating, hydrocracking, catalytic reforming, alkylation, isomerization, and other refining processes. By application, the market is segmented into gasoline production, diesel production, jet fuel production, petrochemical feedstocks, lubricants and base oils, and other applications. By end-use industry, the market is segmented into petroleum refineries, petrochemical refineries, and integrated refinery and petrochemical complexes. The report also covers market size and forecasts for refinery catalysts across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Zeolite-Based Catalysts |

| Precious Metal Catalysts |

| Base Metal Catalysts |

| Mixed Metal Oxide Catalysts |

| Fluid Catalytic Cracking |

| Hydrotreating |

| Hydrocracking |

| Catalytic Reforming |

| Alkylation |

| Isomerization |

| Other Refining Processes |

| Gasoline Production |

| Diesel Production |

| Jet Fuel Production |

| Petrochemical Feedstocks |

| Lubricants and Base Oils |

| Other Applications |

| Petroleum Refineries |

| Petrochemical Refineries |

| Integrated Refinery and Petrochemical Complexes |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Zeolite-Based Catalysts | |

| Precious Metal Catalysts | ||

| Base Metal Catalysts | ||

| Mixed Metal Oxide Catalysts | ||

| By Process | Fluid Catalytic Cracking | |

| Hydrotreating | ||

| Hydrocracking | ||

| Catalytic Reforming | ||

| Alkylation | ||

| Isomerization | ||

| Other Refining Processes | ||

| By Application | Gasoline Production | |

| Diesel Production | ||

| Jet Fuel Production | ||

| Petrochemical Feedstocks | ||

| Lubricants and Base Oils | ||

| Other Applications | ||

| By End-User Industry | Petroleum Refineries | |

| Petrochemical Refineries | ||

| Integrated Refinery and Petrochemical Complexes | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Refinery Catalysts Market?

The Refinery Catalysts Market size is expected to increase from USD 5.73 billion in 2025 to USD 6.19 billion in 2026 and reach USD 7.82 billion by 2031, and is expected to grow at a CAGR of 4.79% over 2026-2031.

Which catalyst material leads to current demand?

Zeolite-based catalysts led demand, with a 45.17% share in 2025, as they remain central to fluid catalytic cracking and large-scale gasoline and propylene production.

Which refinery process is growing the fastest through 2031?

Hydrocracking is forecast to grow at a 5.84% CAGR through 2031, supported by rising demand for ultra-low-sulfur diesel, jet fuel, and lubricant base stocks.

Why is jet fuel becoming a stronger catalyst demand area?

Jet fuel is projected to grow at a 5.66% CAGR through 2031, driven by aviation recovery and sustainable aviation fuel co-processing, which are expected to create stronger demand for advanced hydroprocessing catalysts.

Page last updated on: