Poland Rigid Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

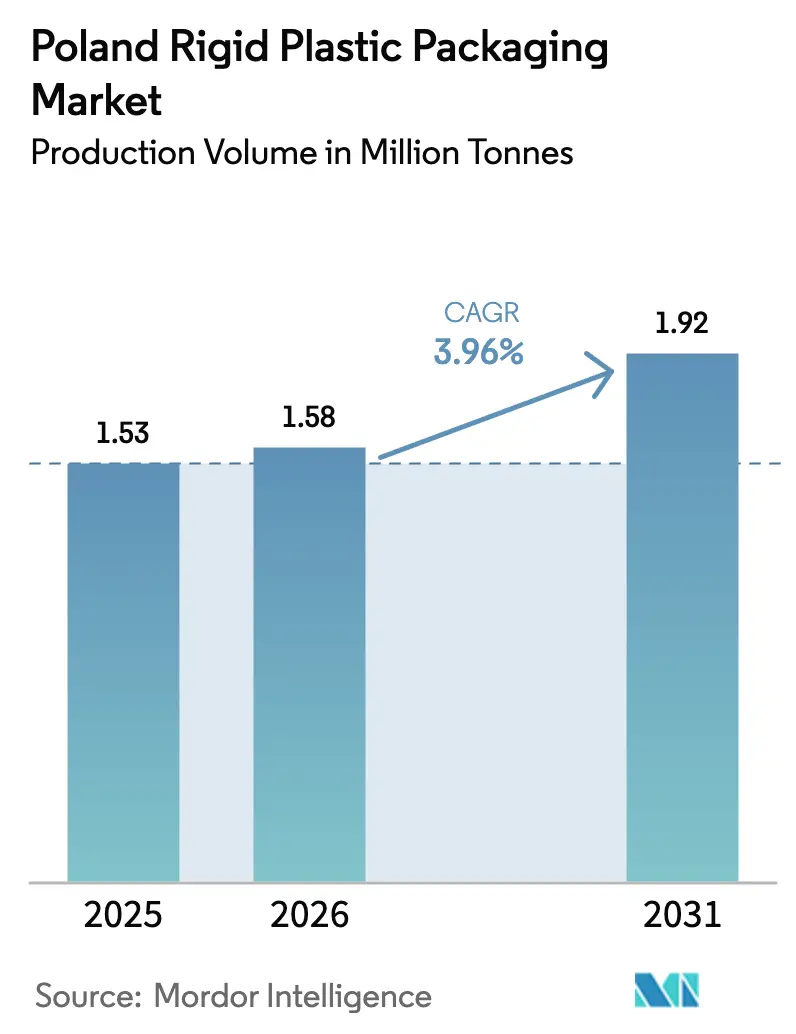

| Base Year Market Size (2025) | 1.53 Million tonnes |

| Market Volume (2026) | 1.58 Million tonnes |

| Market Volume (2031) | 1.92 Million tonnes |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The Poland rigid plastic packaging market size is expected to grow from 1.53 million tonnes in 2025 to 1.58 million tonnes in 2026, and is forecast to reach 1.92 million tonnes by 2031 at a 3.96% CAGR over 2026-2031. This trajectory highlights the Poland rigid plastic packaging market as both a Central European manufacturing hub and a proving ground for the European Union’s most ambitious circular-economy mandates. Rapid scale-up of food-grade recycling, mandatory tethered closures on beverage packs, and a nationwide deposit-return system are tightening post-consumer resin supply yet simultaneously opening margin opportunities for integrated converters. Brand owners are redesigning containers to satisfy recycled-content thresholds, while converters hedge virgin-polymer price swings by investing in chemical and mechanical recycling lines. Competition centers on access to certified rPET, automation that lowers energy intensity, and tooling that accommodates higher clamping pressures tied to new closure geometries.

Key Report Takeaways

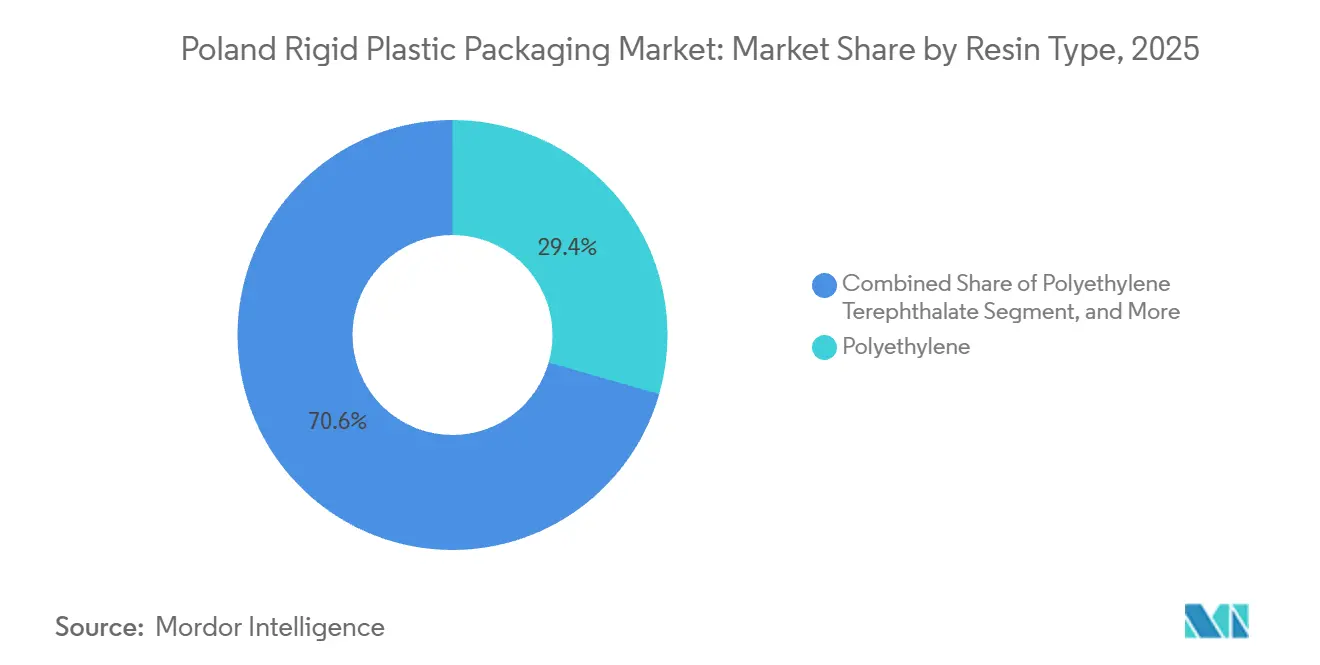

- By resin type, polyethylene commanded 29.43% of Poland rigid plastic packaging market share in 2025, while polyethylene terephthalate is forecast to advance at a 4.64% CAGR through 2031.

- By product type, bottles and jars led with 45.65% of Poland rigid plastic packaging market share in 2025, whereas caps and closures are set to expand at a 5.32% CAGR to 2031.

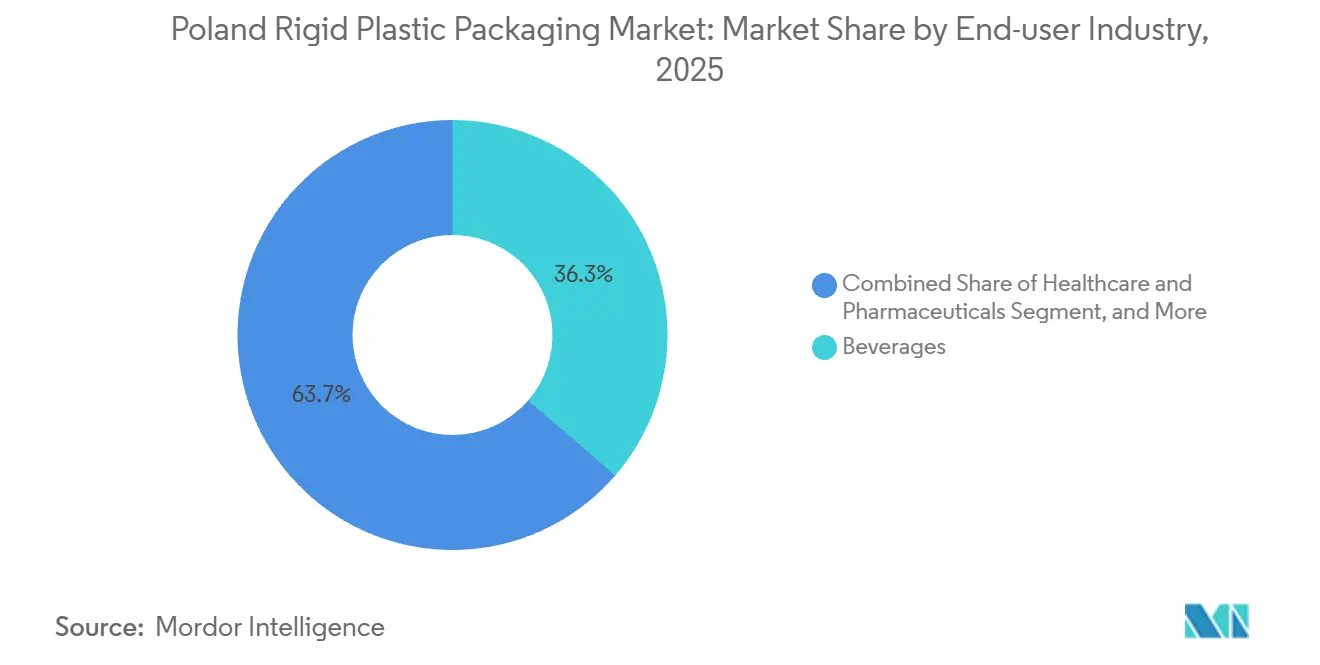

- By end-user industry, beverages accounted for 36.34% of demand in 2025, and healthcare and pharmaceuticals are projected to grow at a 4.87% CAGR between 2026 and 2031.

- By manufacturing process, injection molding represented 25.77% of Poland rigid plastic packaging market share in 2025, yet thermoforming is poised for a 4.55% CAGR thanks to multilayer films incorporating up to 75% post-consumer recycled content.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food-Grade PET Recycling Capacity Expansion | +1.2% | National, Radomsko and Podlaskie clusters | Medium term (2-4 years) |

| E-commerce Boom Driving Durable Parcel Packaging | +0.9% | Logistics hubs in Mazowieckie and Wielkopolskie | Short term (≤ 2 years) |

| Convenience and Ready-to-Eat Food Trends | +0.8% | Urban centers Warsaw, Kraków, Wrocław | Medium term (2-4 years) |

| Nearshoring of Cosmetic and Pharma Packaging | +0.7% | Wielkopolskie and Dolnośląskie FDI corridors | Long term (≥ 4 years) |

| Shift from Glass to PET in Craft Beverage Segment | +0.6% | Małopolskie and Dolnośląskie | Short term (≤ 2 years) |

| Government Incentives for Circular Economy Projects | +0.5% | National, NFOŚiGW grant recipients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food-Grade PET Recycling Capacity Expansion

Poland’s aggressive build-out of bottle-to-bottle infrastructure is redefining feedstock economics. ALPLA’s Radomsko unit, certified for 54,000 tonnes per year of EuCertPlast-compliant rPET, now anchors supply contracts with domestic bottle producers and Western European beverage brands. ORLEN has earmarked PLN 3.6 billion (USD 0.9 billion) for chemical recycling assets that depolymerize mixed waste into virgin-equivalent monomers, hedging against virgin-polymer volatility while boosting Poland’s export credentials. State grants worth PLN 1.1 billion (USD 0.275 billion) accelerate optical sorter and hot-wash line installation, but the new deposit-return scheme, effective October 2025, adds retail-level complexity that could raise reverse-logistics costs above earlier forecasts. Whether the collection network reaches the 65% recycling target for 2035 depends on harmonizing municipal sortation with high-throughput bottle counting centers.

E-commerce Boom Driving Durable Parcel Packaging

With the national online retail turnover expected to hit PLN 192 billion by 2028, parcel networks are specifying impact-resistant containers that withstand automated sorters and urban micro-fulfillment hubs. Injection-molded HDPE clamshells and thick-wall PP mailers reduce product returns and align with courier dimensional-weight pricing. However, European Commission rules obligate merchants to give consumers bring-your-own-container options, forcing converters to design returnable rigid mailers featuring scannable labels and tamper-evident hinges. Copolymers with higher impact values and optimized gate designs help meet new durability protocols, albeit at the cost of longer cycle times and higher energy draw.

Convenience and Ready-to-Eat Food Trends

Dual-income city households favor portion-controlled, microwave-safe trays, spurring demand for multilayer PET formats that balance barrier performance with recyclability. Klöckner Pentaplast’s kp ReClose film enables up to 20 peel-reseal cycles and contains 75% rPET, dropping seamlessly into existing thermoformers.[1]Klöckner Pentaplast, “Multi-layer rigid films,” kpfilms.comEVOH barriers extend chilled meat shelf life beyond 12 days, cutting food waste and allowing retailers to optimize truckloads. The trade-off is higher analytical-testing expense, since Regulation 2025/351 tightens limits on non-intentionally added substances, pushing converters to deploy inline spectrometers and traceability software.

Nearshoring of Cosmetic and Pharma Packaging

Tighter supply-chain risk criteria in post-pandemic Europe encourage multinationals to relocate fill-finish lines to Poland. Sarantis Group’s fully automated Polipak plant, fitted with ISO 9001, ISO 14001, and Blue Angel certifications, exemplifies the level of compliance now necessary to win pharmaceutical contracts. Aseptic blow-fill-seal modules in cleanroom environments have lifted demand for high-clarity PP vials and injection-molded HDPE closures with tamper evidence. The tougher migration-limit regime in force since September 2026 under Regulation 2025/351 further privileges suppliers with robust batch-record systems and validated GMP documentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Plastics Levy and Single-Use Directive | -0.8% | EU-wide, Poland compliance from August 2026 | Short term (≤ 2 years) |

| Price Volatility of Virgin Polymers | -0.6% | Global feedstock markets | Short term (≤ 2 years) |

| Low Household Sorting Rates Limiting rPET Feedstock | -0.5% | National municipal systems | Medium term (2-4 years) |

| Rise of Refill-and-Reuse Retail Formats | -0.3% | Warsaw, Kraków, Wrocław urban pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Plastics Levy and Single-Use Directive

The upcoming Packaging and Packaging Waste Regulation enforces recyclability by 2030 and levies fees on non-recyclable formats, directly squeezing converter margins.[2]European Commission, “Packaging waste,” environment.ec.europa.euBrand owners now face penalties unless PET beverage bottles contain at least 30% recycled material by 2030, rising to 65% in 2040. PFAS thresholds effective August 2026 add compliance hurdles for barrier-coated applications. Smaller molders, unable to finance tethered-closure tooling or secure certified resin, risk exit, accelerating market consolidation.

Price Volatility of Virgin Polymers

In April 2025, European polyethylene and polypropylene contracts both fell by EUR 55 per tonne, while clear bottle scrap climbed due to summer beverage demand.[3]British Plastics Federation, “Price Reports March 2024,” bpf.co.uk The divergent price path forces converters to renegotiate formulas mid-quarter, straining customer relationships. Overcapacity at European crackers, plus opportunistic imports, undermines any attempt to pass through cost upticks. Integrated recyclers with depolymerization units can buffer swings, but independent processors endure squeezed spreads that delay automation upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Captures Momentum from Recycling Mandates

Polyethylene terephthalate is projected to expand at a 4.64% CAGR to 2031, buoyed by beverage brands pivoting from glass and heightened availability of food-grade rPET through domestic capacity expansions. The Poland rigid plastic packaging market size for PET applications is set to swell as converters race to meet the 30% recycled-content rule in the beverage segment. In contrast, polyethylene retained a 29.43% Poland rigid plastic packaging market share in 2025 but will grow more modestly as lightweighting and mono-material substitution reduce virgin HDPE and LDPE demand. First movers with EuCertPlast-certified flakes, such as ALPLA, can lock in multiyear offtake agreements, while mid-tier processors struggle to secure supply amidst seasonal rPET price spikes. Beyond mainstream polymers, niche bio-based PE and PLA remain cost-disadvantaged, though state grants could foster pilot volumes once sortation schemes mature.

Upgrade paths differ across resin families. Bottle manufacturers are already engineering stretch-blow-molded PET grades that withstand 61 bar carbonation with 15% wall reductions while maintaining top-load integrity. Meanwhile, PP molders are exploring talc-reinforced grades to achieve microwave stability for ready meals without compromising recyclability, although post-consumer PP streams remain less developed than PET. Policy-driven phase-outs of polystyrene laminates encourage a shift to mono-material PP pots, forcing yogurt brands to revamp decoration methods away from full-body sleeves that hinder near-infrared sorting.

By Product Type: Tethered Closures Redefine Cap Economics

Bottles and jars accounted for 45.65% of 2025 volume, anchoring the Poland rigid plastic packaging market although per-unit resin usage is falling through lightweighting. Caps and closures will outpace all other formats at a 5.32% CAGR because every beverage container up to 3 liters sold after July 2024 must feature a tethered closure. The Poland rigid plastic packaging market size for closure systems is therefore poised to accelerate as converters retool molds, add high-tonnage presses, and migrate to 26 millimeter neck finishes. ENGEL e-cap cells demonstrate the cycle-time savings possible when higher injection pressures are balanced against servo-drive energy recovery, making total cost of ownership competitive.

Rigid-tray demand remains healthy, fed by urban shoppers prioritizing convenience meals. Multilayer thermoform designs pair clear PET bases with PP lids to deliver clarity and microwave safety, yet the push for mono-material construction is steering development toward peel-reseal barrier films and inline delamination technologies. Intermediate bulk containers sustain steady volume in industrial chemicals, supported by post-consumer HDPE usage that reduces Scope 3 emissions. Ancillary products such as pallets and crates expand in parallel with e-commerce warehouse build-outs.

By End-User Industry: Healthcare Outpaces Beverage Growth

Beverages captured 36.34% of 2025 demand, underlining their status as the biggest buyer group in the Poland rigid plastic packaging market. Nonetheless, healthcare and pharmaceuticals will chart the highest CAGR at 4.87% as drug makers co-locate filling lines with clinical-trial hubs. The Poland rigid plastic packaging market size for regulated healthcare formats benefits from stricter migration-limit rules that favor domestic suppliers with ISO 13485 and ISO 15378 certifications. Pet care and nutraceuticals, often packed in HDPE jars and PP scoops, extend the growth runway by borrowing child-resistant closure designs from pharma.

Food processors remain steady customers, adopting high-barrier trays that lengthen chilled chain logistics and cut shrink. Cosmetics and personal care brands specify amber PET jars with 30% rPET content to meet corporate sustainability pledges, but refill-and-reuse pilots in Warsaw grocery chains could shave single-use volumes if consumer adoption accelerates. Industrial chemicals rely on UN-certified drums, with blow-molders qualifying for dual approvals so containers can ship solvents one day and agricultural inputs the next.

By Manufacturing Process: Thermoforming Accelerates on Multilayer Films

Injection molding still delivered 25.77% of 2025 volume, yet thermoforming will grow faster, at 4.55% CAGR, as brand owners retrofit form-fill-seal lines to run 75% rPET barrier webs. The Poland rigid plastic packaging market share captured by thermoforming rises when multilayer films integrate thin EVOH cores that remain within recyclability thresholds. Automated stacker-packer modules shorten changeover times, making short runs economical for private-label chilled foods.

Blow molding, central to beverage bottles and household-chemical flasks, continues to innovate around ultra-lightweighting. Top-load simulations, optimized base cups, and crystallization ovens permit 19-gram 1.5-liter water bottles without paneling. Compression molding keeps relevance in specialty closures where shorter melt residence reduces color shift and taste transfer. Extrusion of rigid PVC sheets into construction profiles benefits from home-renovation stimulus in 2026, although societal pressure may switch these profiles to recycled PET-G in the medium term.

Geography Analysis

Central voivodeships dominate production due to proximity to retailers, export corridors, and grant funding pools. Mazowieckie and Wielkopolskie host mega-warehouses that necessitate just-in-time container deliveries, while Śląskie’s dense highway grid favors cross-border shipments into Czechia and Slovakia. Łódzkie’s Radomsko plant anchors Poland’s rPET loop by washing and pelletizing collected bottles at EuCertPlast standards. Western investor confidence is visible in Środa Wielkopolska, where Sarantis built a 24,000 m² automated site interfaced with robotic shuttle racks and GMP-compliant clean-rooms.

Craft brewers clustering in Małopolskie and Dolnośląskie increasingly adopt PET to minimize breakage along mountainous delivery routes, despite lingering consumer preference for glass. Podlaskie receives circular-economy grants for multilayer PolyAl recycling, raising local feedstock availability for sheet extruders. Yet recycling rates are hamstrung by household sorting below 29%, leaving the Poland rigid plastic packaging market dependent on imported flake or chemical-recycling intermediates to hit the 50% recycling target for 2025. A nationwide deposit scheme now recovers beverage containers but has yet to encompass household chemical bottles, limiting PET-grade feedstock diversity.

Urban refill pilots in Warsaw, Wrocław, and Kraków reveal the logistical friction of store-installed dispensers, slow consumer uptake, cleaning regimen complexity, and lost marketing real estate. Even so, the upcoming EU rule compelling takeaway outlets to permit personal containers could widen the model beyond detergents into foodservice. E-commerce growth originating in Mazowieckie parcel hubs offsets some single-use erosion by raising demand for rigid returnable mailers that amortize across subscription cycles.

Competitive Landscape

The market concentration is moderate. ALPLA and Logoplaste maintain economies of scale in stretch-blow-molding halls mated with inline cap cells, yet mid-sized Polish thermoformers such as KGL and Prosperplast win contracts through agile toolrooms capable of multi-format changeovers. Vertically integrated recyclers have gained bargaining power because rPET scarcity enables them to quote premium flake to captive molding operations and external accounts alike.

Compliance investments differentiate players. ALPLA’s EuCertPlast certificate facilitates tender wins with beverage brands under recycled-content pressure, while KGL’s in-house research center enables bespoke tray geometries that survive –40 °C blast freezing and 200 °C reheating. Sarantis, backed by foreign capital, goes after pharma and cosmetics niches that value ISO-based quality regimes and low volatile-organic-compound plants. Smaller enterprises either enter toll-grinding alliances to secure flake or consider mergers to muster capital for tethered-closure tooling.

Technology roadmaps emphasize inline vision systems that track contaminants at 2.5 meter-per-second conveyor speeds, satisfying Regulation 2025/351 demand for batch-level documentation. Simultaneously, electric press adoption lowers Scope 2 emissions and qualifies for National Fund feed-in tariffs. Strategic bets on depolymerization, such as ORLEN’s USD 0.9 billion outlay, hedge against virgin price swings while opening license-to-operate narratives with climate-conscious brand owners.

Poland Rigid Plastic Packaging Industry Leaders

ALPLA Werke Alwin Lehner GmbH and Co KG

Sonoco Products Company

Mondi Poznań Sp. z o.o.

Greiner Packaging International GmbH

PLASTAN Kacprzyk Sp. z o.o. Sp. k.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Poland’s Ministry of Climate and Environment opened a public consultation on expanding the deposit-return scope to include household chemical bottles by 2028.

- October 2025: Poland implemented a nationwide deposit-return system with a PLN 0.5 deposit on beverage bottles and cans up to 3 liters, setting off reverse-logistics investments valued at PLN 23.1 billion (USD 5.775 billion) over ten years.

- August 2025: Draft legislation on extended producer responsibility proposed a 30-35% recycled-content requirement in plastic packaging by 2030.

- February 2025: Commission Regulation 2025/351 tightened food-contact purity and documentation rules, with a transition deadline of Sep 2026.

Poland Rigid Plastic Packaging Market Report Scope

The scope of the study characterizes the rigid plastic packaging market based on the product's raw materials, including PP, PE, PET, and other raw materials used across various end-use industries such as food, pharmaceuticals, beverage, personal care, industrial and automotive, and more. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The Poland Rigid Plastic Packaging Market Report is Segmented by Resin Type (Polyethylene, Polyethylene Terephthalate, Polypropylene, Polystyrene and EPS, and Other Resin Types), Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Intermediate Bulk Containers, Drums, and Other Product Types), End-user Industry (Food, Beverage, Healthcare and Pharmaceuticals, Cosmetics and Personal Care, Industrial Chemicals, Building and Construction, and Other End-user Industries), and Manufacturing Process (Injection Moulding, Blow Moulding, Thermoforming, Compression Moulding, Extrusion, and Other Manufacturing Process). The Market Forecasts are Provided in Terms of Volume (Million Tonnes).

| Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polyethylene Terephthalate | |

| Polypropylene | |

| Polystyrene and EPS | |

| Other Resin Types |

| Bottles and Jars |

| Trays and Containers |

| Caps and Closures |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Other Product Types |

| Food | Candy and Confectionery |

| Dairy and Frozen | |

| Meat, Poultry and Seafood | |

| Other Food Types | |

| Beverage | |

| Healthcare and Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Industrial Chemicals | |

| Building and Construction | |

| Other End-user Industries |

| Injection Moulding |

| Blow Moulding |

| Thermoforming |

| Compression Moulding |

| Extrusion |

| Other Manufacturing Process |

| By Resin Type | Polyethylene | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polyethylene Terephthalate | ||

| Polypropylene | ||

| Polystyrene and EPS | ||

| Other Resin Types | ||

| By Product Type | Bottles and Jars | |

| Trays and Containers | ||

| Caps and Closures | ||

| Intermediate Bulk Containers (IBCs) | ||

| Drums | ||

| Other Product Types | ||

| By End-user Industry | Food | Candy and Confectionery |

| Dairy and Frozen | ||

| Meat, Poultry and Seafood | ||

| Other Food Types | ||

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Industrial Chemicals | ||

| Building and Construction | ||

| Other End-user Industries | ||

| By Manufacturing Process | Injection Moulding | |

| Blow Moulding | ||

| Thermoforming | ||

| Compression Moulding | ||

| Extrusion | ||

| Other Manufacturing Process | ||

Key Questions Answered in the Report

How fast is demand growing for food-grade recycled PET in Poland?

Food-grade rPET volumes are increasing at about 4.6% CAGR through 2031 as beverage brands chase the 30% recycled-content mandate.

Which segments benefit most from the tethered-closure rule?

Closure manufacturers gain, with caps and closures projected to post a 5.32% CAGR as every beverage bottle up to 3 liters now needs an attached cap.

Why are pharmaceutical firms investing in local packaging plants?

Tightened migration limits and risk-diversification strategies make nearshore ISO-certified facilities attractive for aseptic fill-finish operations.

What is the main challenge in meeting Poland’s recycling targets?

Low household sorting rates, still below 29%, restrict the flow of clean post-consumer flake needed for recycled-content mandates.

How will the deposit-return system impact processors?

The scheme secures higher collection rates for PET bottles but raises reverse-logistics costs, favoring vertically integrated recyclers with established take-back channels.

Are refill-and-reuse formats likely to replace single-use rigid packs?

Trials are underway in major cities, yet broad adoption hinges on consumer convenience, cleaning logistics, and regulatory incentives expanding beyond beverage containers.

Page last updated on: