Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

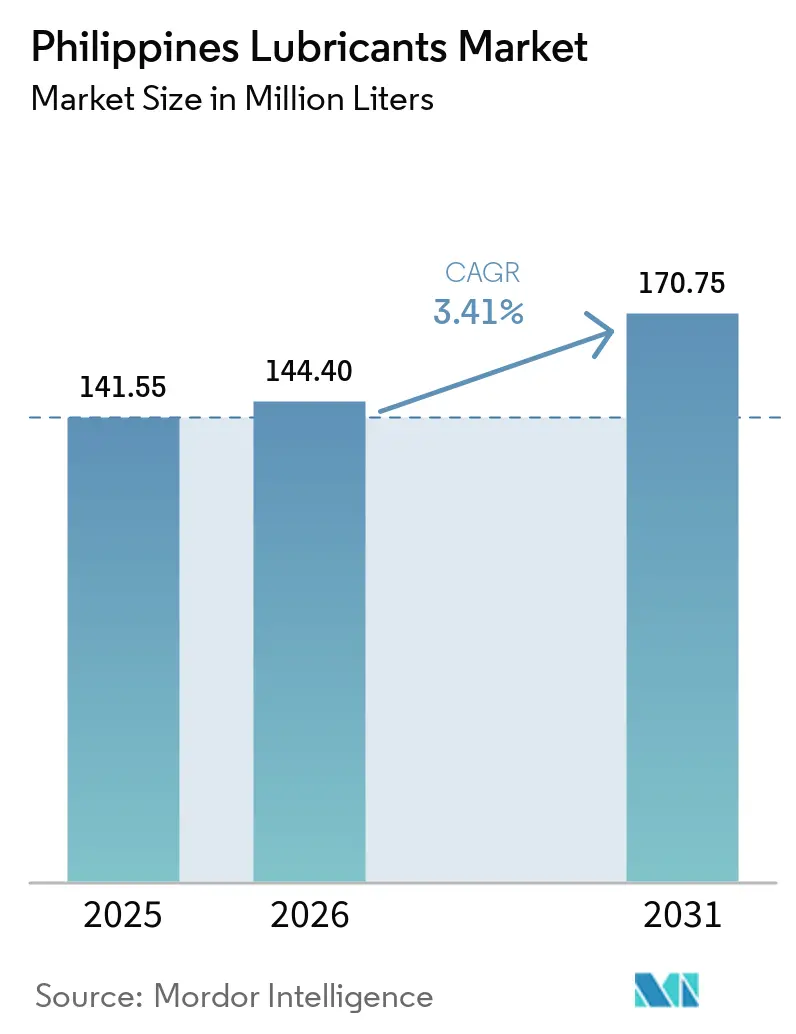

| Base Year Market Size (2025) | 141.55 Million liters |

| Market Volume (2026) | 144.40 Million liters |

| Market Volume (2031) | 170.75 Million liters |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Lubricants Market Analysis by Mordor Intelligence

The Philippines Lubricants Market size was valued at 141.55 million liters in 2025 and is estimated to grow from 144.40 million liters in 2026 to reach 170.75 million liters by 2031, at a CAGR of 3.41% during the forecast period (2026-2031). This expansion is propelled by PHP 1.545 trillion (USD 26.6 billion) infrastructure spending in 2024, brisk manufacturing output tied to electronics and textiles, and the 1.68-million-unit motorcycle sales volume that keeps demand for two-stroke and four-stroke oils elevated. At the same time, a 61.5% jump in electric-vehicle registrations in the first half of 2024 signals an impending ceiling for conventional engine-oil volumes, pushing suppliers to diversify into e-axle greases and thermal-management fluids. Competitive focus is shifting toward premium synthetics, bio-based formulations, and omnichannel delivery as Shell, Petron, and emerging Gulf and Middle-East entrants expand e-commerce, quick-lube bays, and franchise networks. Near-term upside continues to come from heavy equipment on Build-Better-More mega-projects, while regulatory headwinds, 12% VAT, PHP 10 per-litre excise, and tighter used-oil rules, compress margins for small distributors that lack scale.

Key Report Takeaways

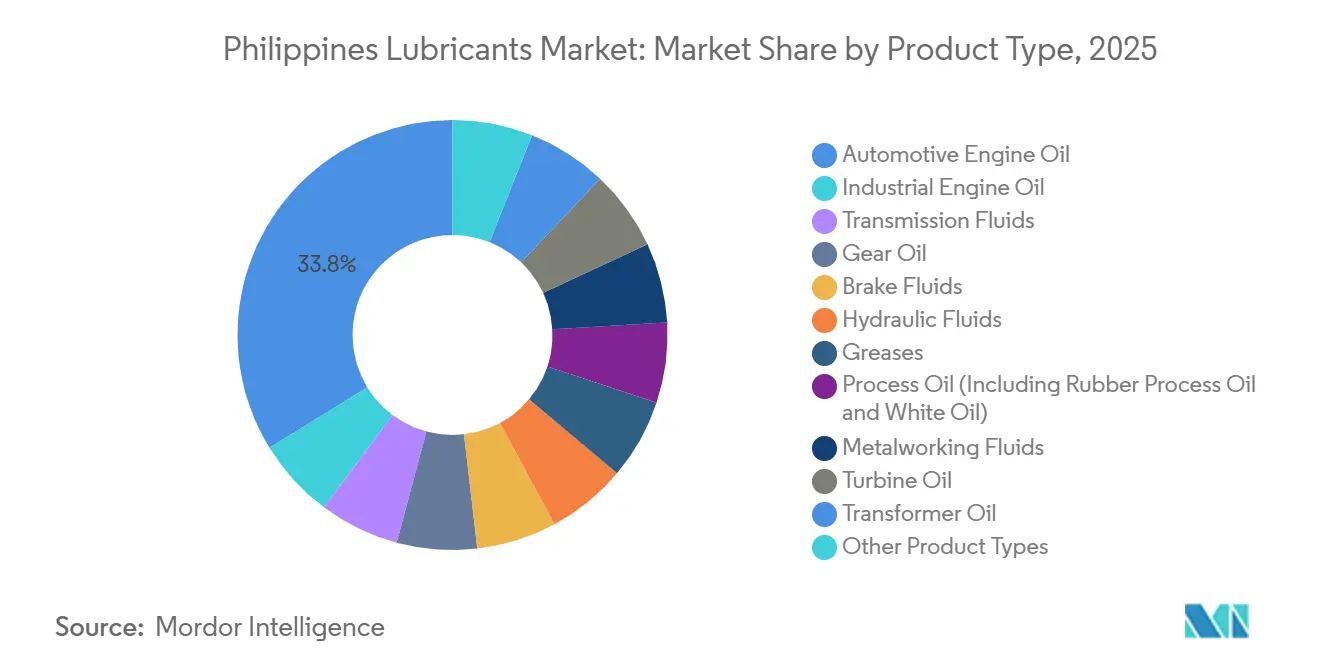

- By product type, automotive engine oil led with 33.78% of the Philippines lubricants market share in 2025; industrial engine oil is forecast to expand at a 3.15% CAGR through 2031.

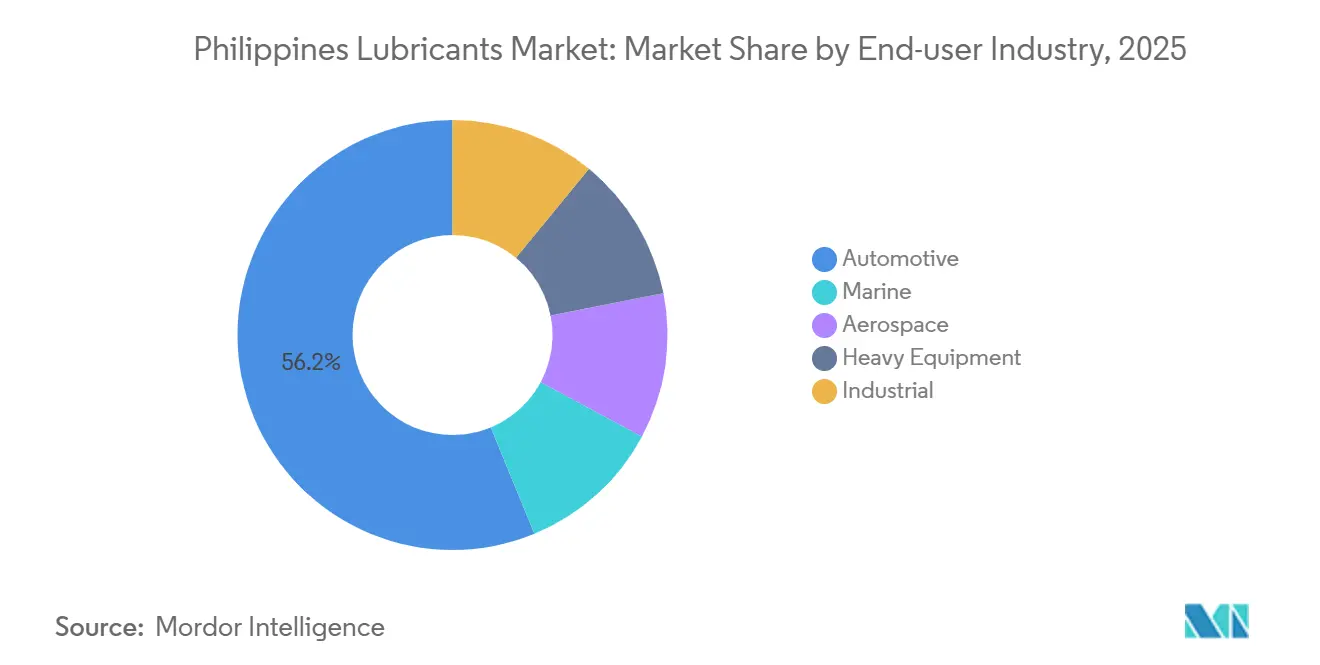

- By end-user industry, the automotive segment captured 56.23% of the Philippines lubricants market size in 2025, while industrial applications are advancing at a 3.05% CAGR to 2031.

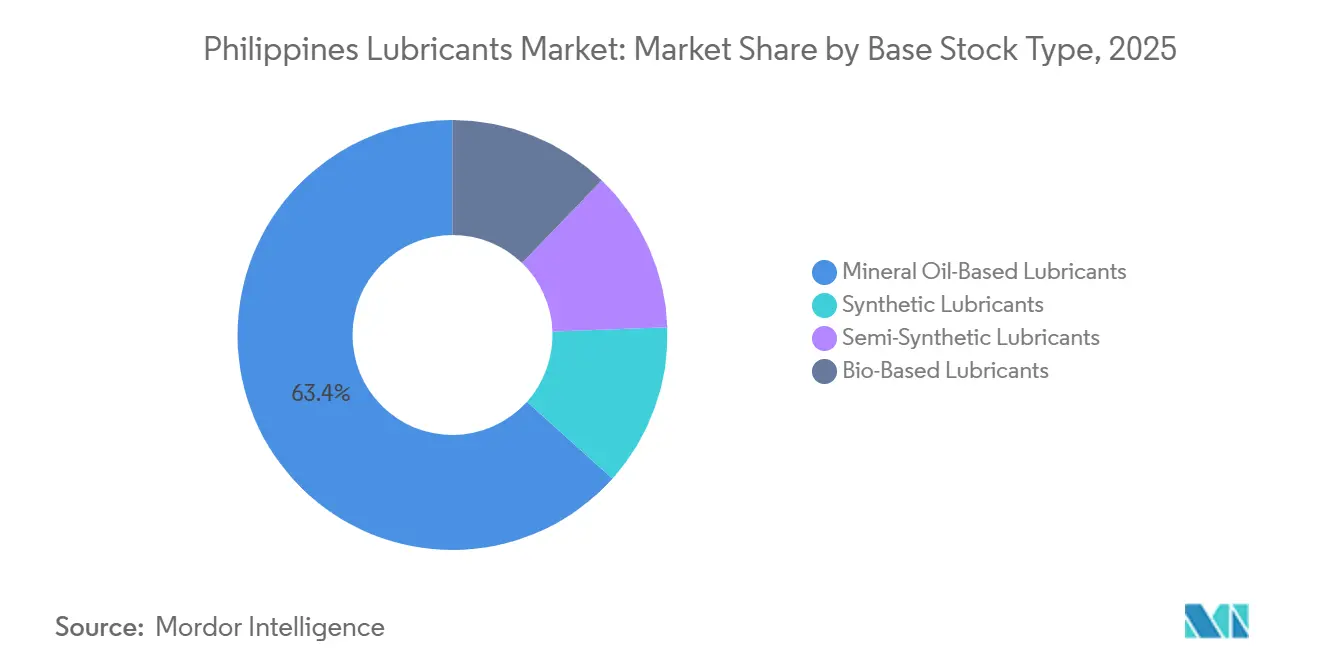

- By base stock type, mineral oil-based lubricants dominated with a 63.35% share in 2025; bio-based lubricants are projected to grow at a 3.59% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing construction mega-projects | +0.9% | Metro Manila, Cebu, Davao infrastructure corridors | Medium term (2-4 years) |

| Industrial digitalization and predictive maintenance | +0.5% | Luzon manufacturing hubs (Cavite, Laguna, Batangas) | Long term (≥ 4 years) |

| Ride-hailing and motorcycle fleet growth | +0.7% | Urban centers nationwide | Short term (≤ 2 years) |

| OEM-backed low-viscosity synthetics | +0.4% | National dealership networks | Medium term (2-4 years) |

| Rapid e-commerce and quick-lube expansion | +0.3% | Highly urbanized provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Construction Mega-Projects (Build-Better-More)

The PHP 1.545 trillion (USD 26.6 billion) outlay in 2024, equal to 5.8% of GDP, underwrites large road, rail, and bridge builds that keep excavators, cranes, and concrete mixers running in punishing duty cycles. Equipment owners shorten drain intervals, inflating demand for high-zinc hydraulic fluids and extreme-pressure greases. Projects such as the Bataan–Cavite Interlink Bridge and Metro Manila Subway require thousands of heavy machines that rely on Group II base-oil blends for soot control[1]Asian Infrastructure Investment Bank, “Bataan–Cavite Interlink Bridge Factsheet,” aiib.org. Yet capital-outlay pauses before elections pared spending to 4.2% of GDP in Q1-Q3 2025, swinging lubricant orders sharply from quarter to quarter. Suppliers with multi-regional depots, notably Shell’s 10 warehouses and Petron’s 21,000-outlet network, are best placed to flex inventories. Power projects tied to new rail lines also lift turbine-oil pull-through, reinforcing the premium segment.

Industrial Digitalization Boosting Predictive-Maintenance Grade Lubricants

Government Industry 4.0 programs and the Advanced Manufacturing Center spur adoption of sensor-equipped machinery that favors longer-life synthetic hydraulics[2]Department of Trade and Industry, “Industry 4.0 Roadmap,” dti.gov.ph. Only 14.9% of factories had deployed IoT maintenance by 2024, but early movers in electronics and metalworking already specify OEM-approved zinc-free oils rated beyond 10,000 hours in ASTM D943 testing. Chevron Clarity and equivalents command sizeable premiums and often bundle oil-analysis services. Small and medium manufacturers still default to mineral-based AW 68 fluids, so vendors such as Shell push mobile oil-analysis vans to up-sell synthetics, a model that hinges on scaling technical staff as much as stock volume.

Rapid Growth of Ride-Hailing and Motorcycle Fleets Demanding High-Temperature 4T Oils

Motorcycle sales hit 1.68 million units in 2024 and Grab’s fleet topped 60,000 riders in 2025, forcing engines to operate in stop-and-go heat that degrades mineral 20W-50 oils quickly. Petron’s Sprint Scooter Oil, launched in November 2025, targets this duty profile with a high-phosphorus additive pack, while SEAOIL rolls out a five-grade portfolio to capture fleet contracts. Cost-per-kilometre is the metric for ride-hailing operators, so blended semi-synthetics balance price against oxidative stability.

OEM-Backed Low-Viscosity Synthetic Oils with Extended-Warranty Pull-Through

Honda, Toyota, and Nissan increasingly specify SAE 0W-20 and 5W-30 synthetics and tie warranty validity to their use. Shell and Petron secure OEM approvals, cementing captive volumes via dealer channels even as 10,000–15,000 km drain intervals lower litres-per-vehicle. Winning new-car buyers is therefore more critical than retaining older, lower-mileage vehicles, which helps explain Shell’s aggressive TikTok and Shopee campaigns in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electric and hybrid-vehicle uptake | -0.6% | Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Counterfeit and adulterated lubricants | -0.3% | Provincial markets with diffuse distribution | Short term (≤ 2 years) |

| Escalating used-oil compliance costs | -0.2% | Metro Manila and major regional centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Penetration of Electric and Hybrid Vehicles

EV registrations jumped from 13,000 in 2023 to 21,000 by mid-2024 on the back of import-duty and VAT exemptions under RA 11697, and the government targets a 50% EV sales mix by 2040. Charging stations surpassed 800 sites in 2024, anchored by Meralco, Shell Recharge, and AC Energy. Hybrids still use engine oil but at roughly 60–70% of internal-combustion volume; full battery EVs eliminate it. Suppliers hedge by launching specialized dielectric-cooling fluids, yet the transition is expected to shave 0.6 percentage points off the Philippines lubricants market CAGR.

Proliferation of Counterfeit/Adulterated Lubricants

DTI seizures of fake Shell products highlight rampant relabeling of used oil and mineral dilutions that retail 30% below genuine packs. With 11,923 retail outlets nationwide, monitoring is patchy. Brand owners risk warranty disputes and forced price-cuts to defend share. Mid-tier players like SEAOIL capitalize by promoting Philippine National Standards certification as a quality marker, yet enforcement gaps persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Engine Oil Climbs as Power and Construction Drive Demand

Automotive Engine Oil, while still accounting for 33.78% of 2025 volume, faces a gradually flattening curve as hybrids lengthen drain intervals. Transmission fluids benefit from automatic-transmission uptake in passenger cars, now 48% of 2024 sales. Greases, metalworking, turbine, and transformer oils remain niche but margin-rich pockets, reinforcing supplier moves toward value-added industrial blends. The Philippines lubricants market size for Industrial Engine Oil is projected to grow faster than any other product family through 2031. Industrial Engine Oil is poised to outpace automotive grades at a 3.15% CAGR, fueled by 29,853 MW of installed power capacity and around-the-clock genset operations that mandate high-soot-load formulations.

Smaller players must pick sides: high-volume, low-margin automotive oils vulnerable to counterfeits, or low-volume, high-spec industrial blends that require technical support. SEAOIL’s strategy spans both, leveraging 700+ stations for retail pull while marketing ISO VG 150–320 gear oils to crushing plants.

By End-User Industry: Industrial Users Accelerate Despite Automotive Dominance

Automotive retained 56.23% of 2025 demand, but Industrial applications are set for a 3.05% CAGR on the back of power-plant overhauls, Laguna and Batangas metalworking expansions, and new textile capacity in Batangas. Marine lubricants grow with MARINA’s sulphur-cap rules that require low-ash cylinder oils, while construction equipment links automotive and industrial demand. The Philippines lubricants market share captured by Industrial users is forecast to widen each year of the outlook.

Fleet maintenance contracts for Grab, Foodpanda, and Angkas illustrate cross-over potential, allowing suppliers to bundle automotive and industrial volumes into single agreements. New entrants ADNOC and Aramco, via their 25% stakes in Unioil, aim to exploit this adjacency by pairing Valvoline automotive lines with ProForce industrial fluids.

By Base Stock Type: Mineral Oils Still Rule but Bio-Based Fluids Surge

Mineral oils maintained a 63.35% share in 2025 thanks to low cost and compatibility with legacy equipment. Synthetic and semi-synthetic blends grow in line with OEM viscosity shifts and extended warranties, and Shell reports premium-grade penetration hit 29% in 2024. Bio-based lubricants, catalyzed by the B3 to B5 biodiesel roadmap, are on course for the fastest 3.59% CAGR, although uptake is constrained by limited domestic feedstock and performance skepticism. The Philippines lubricants market size captured by synthetic and bio-based grades rises steadily through 2031 as suppliers use carbon-neutral labeling to justify higher unit prices.

Geography Analysis

Luzon accounts for roughly 53% of retail outlets and over 70% of economic activity, making it the focal point for lubricant consumption. Mega-projects such as the North–South Commuter Railway channel volumes into Calabarzon and Central Luzon, where Petron’s Bataan refinery and Shell’s Tabangao import facility provide supply redundancy. Visayas, anchored by Cebu’s trans-shipment hub, and Mindanao, with its mining clusters, offer faster growth albeit from a smaller base. Marine traffic across 800+ RoRo routes sustains demand for trunk-piston and cylinder oils.

Logistics realities of 7,641 islands inflate transport costs; hence, Shell’s 10 depots and Petron’s nationwide haulage fleet confer a cost edge. E-commerce partly mitigates geographic fragmentation, yet quick-lube bays in Metro Manila, Cebu, and Davao still handle the bulk of change-outs for warranty compliance. Used-oil audits concentrate in big cities, adding to the compliance gradient that favors incumbents.

Competitive Landscape

The Philippines Lubricants market is moderately consolidated. Shell grew lubricant volumes 10% and doubled e-commerce turnover in 2024, while Petron’s net income jumped 37% in the first nine months of 2025, reflecting refinery productivity gains and a 21,000-outlet footprint. New-wave competition centers on premiumization, digital selling, and rapid-service bays. Technology differentiators include carbon-neutral formulations, sensor-ready synthetics, and bundled oil-analysis services. Shell reports 18% of its local range is now carbon-neutral, and Chevron markets Clarity Hydraulic AW as 10,000-hour oxidation-stable.

Philippines Lubricants Industry Leaders

Petron Corporation

Shell plc

Chevron Corporation

SEAOIL Philippines, Inc.

Phoenix Petroleum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: HELLA Philippines unveiled a fresh range of engine oils and lubricants tailored for the Philippine market. Developed with advanced German technology, these oils underwent rigorous testing to ensure optimal performance under the tropical conditions on Philippine roads. The comprehensive lineup includes engine oils, transmission fluids, gear oils, and additional products.

- June 2025: Repsol Lubricants, through its newly formed joint venture, commenced local production in the Philippines. The inaugural product off the line is Maker Hydroflux EP 68, an industrial lubricant, with an initial output of 60 drums. The local production will allow the company to better meet the needs of the market and explore new opportunities, primarily in the industrial segment.

Philippines Lubricants Market Report Scope

Lubricant products are made from a combination of base oils and additives. The composition of base oil in the formulation of lubricants is primarily between 75-90%. Base oils possess lubricating properties and make up to 90% of the final lubricant product.

The market is segmented based on product type, end-user industry, and base stock type. The market is segmented by product type into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil, metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. The market sizing and forecasts for each segment are based on volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is size of the Philippines Lubricants market?

The Philippines Lubricants Market size was valued at 141.55 million liters in 2025 and is estimated to grow from 144.40 million liters in 2026 to reach 170.75 million liters by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

What is the expected CAGR for Philippine lubricant demand to 2031?

The Philippines Lubricants market is forecast to expand at a CAGR of 2.96% during 2026-2031.

Which product type is growing fastest?

Industrial Engine Oil is projected to grow at a 3.15% CAGR through 2031.

Why are bio-based lubricants gaining traction?

The B3–B5 biodiesel mandate raises lubricity standards and supports bio-based fluid adoption.

How are suppliers countering counterfeit products?

By emphasizing certified supply chains, quick-lube services, and serialized packaging for traceability.

Page last updated on: