Nuclear Medicine Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

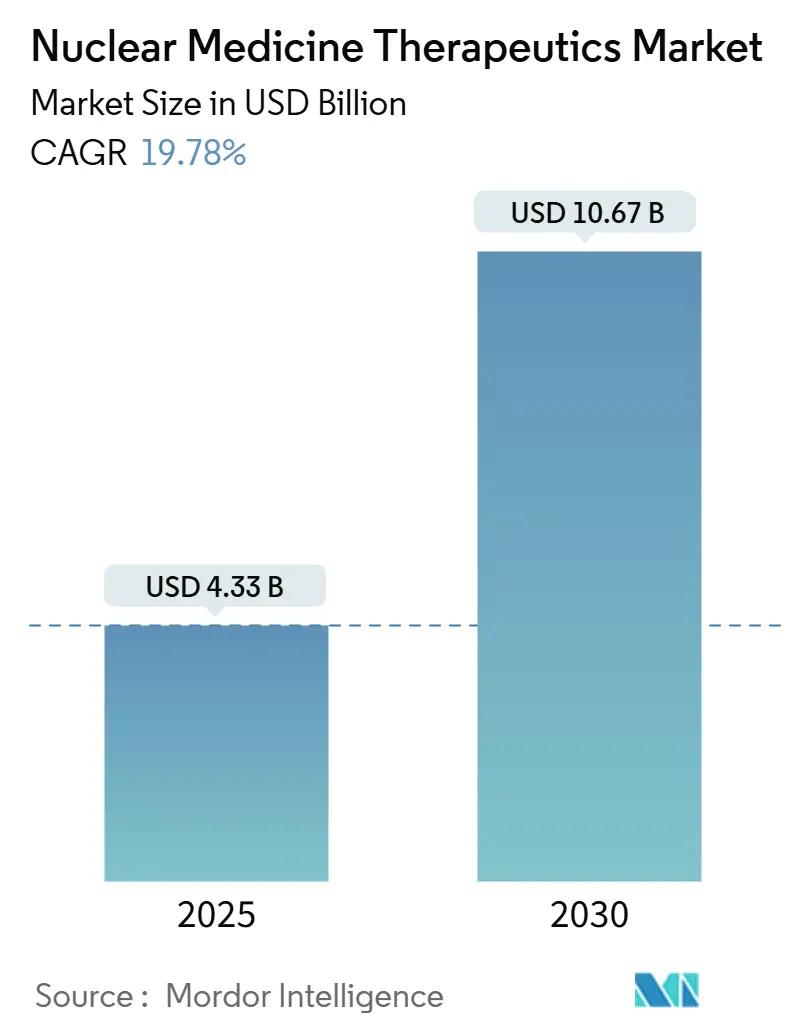

| Market Size (2025) | USD 4.33 Billion |

| Market Size (2030) | USD 10.67 Billion |

| Growth Rate (2025 - 2030) | 19.78% CAGR |

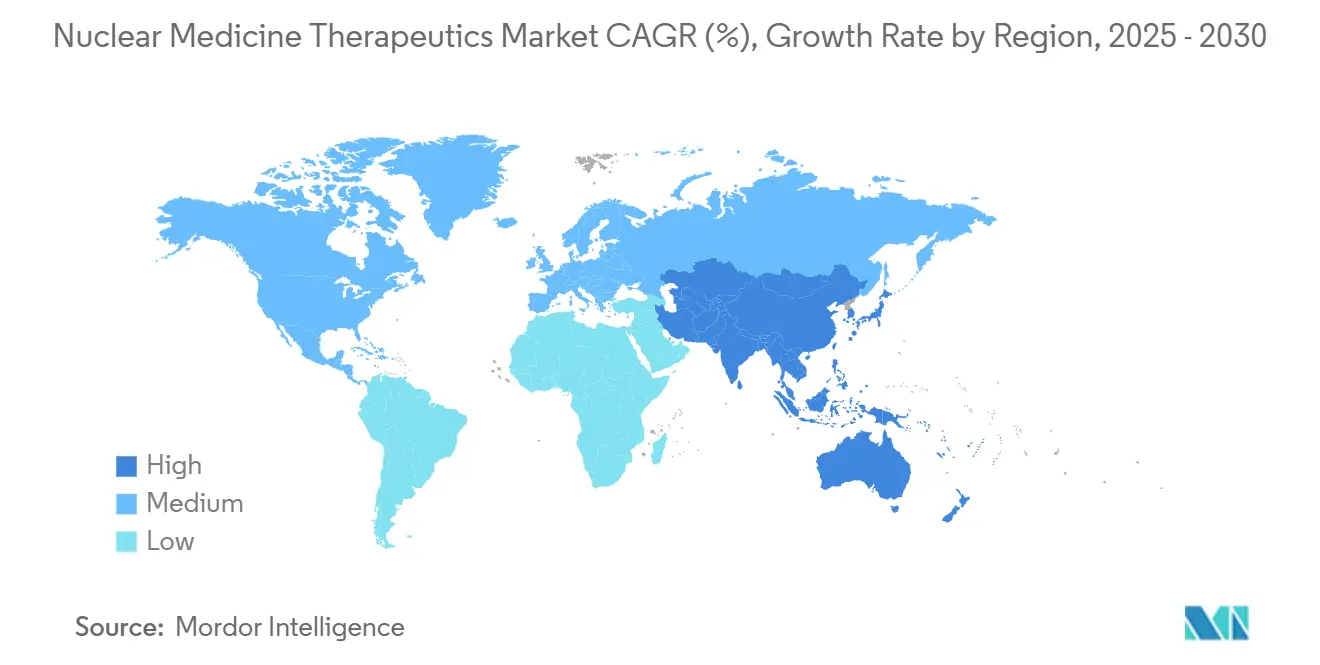

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuclear Medicine Therapeutics Market Analysis by Mordor Intelligence

The nuclear medicine therapeutics market stands at USD 4.33 billion in 2025 and is forecast to reach USD 10.67 billion by 2030, advancing at a 19.78% CAGR. Demand accelerates as radiopharmaceuticals shift from palliative options toward first-line treatments across oncology, neurology, and cardiology. Breakthroughs in alpha-emitting isotopes, growing reimbursement support, and a steady pipeline of theranostic agents continue to expand procedure volumes. Manufacturers pursue in-house isotope production to curb supply bottlenecks, while hospitals adopt artificial-intelligence-enabled dosimetry to improve outcomes. Regionally, strong North American infrastructure anchors the nuclear medicine therapeutics market, but Asia Pacific’s rapid build-out of cyclotrons and specialized clinics positions it as a long-term growth engine.

Key Report Takeaways

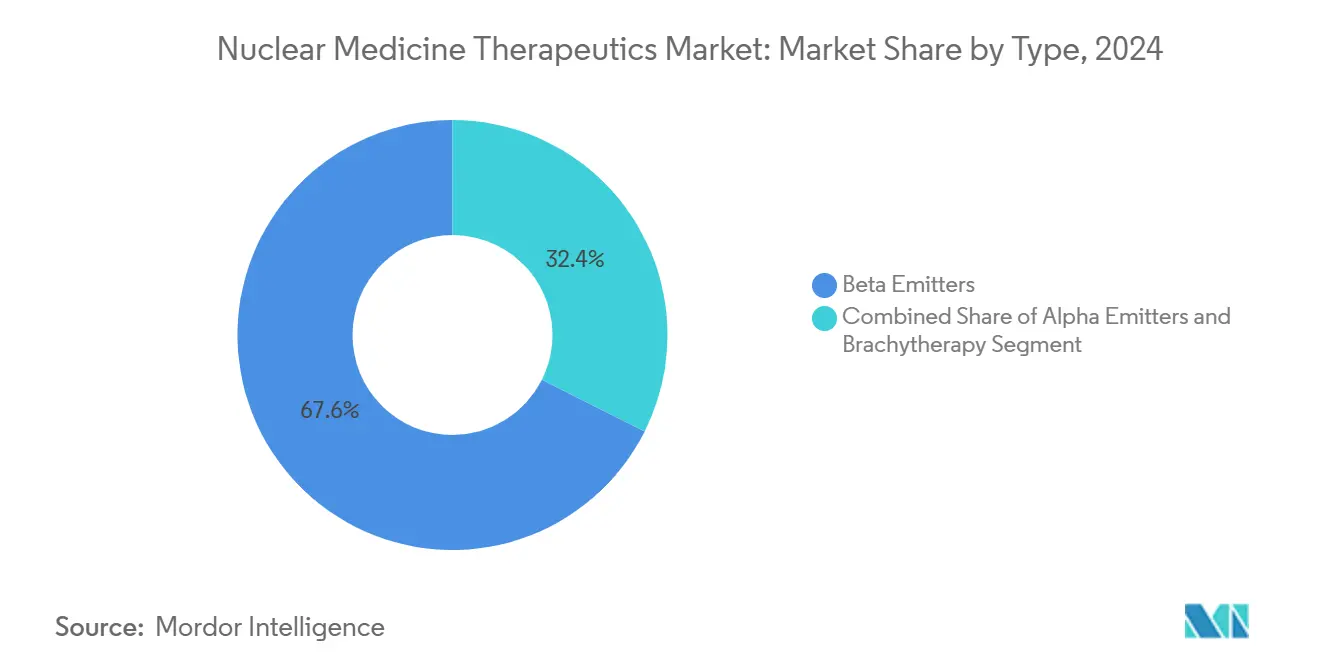

- By type, beta emitters led with 67.58% of nuclear medicine therapeutics market share in 2024; alpha emitters record the highest 23.55% CAGR through 2030.

- By therapeutic modality, targeted radioligand therapy accounted for 49.56% of the nuclear medicine therapeutics market in 2024; boron neutron capture therapy grows fastest at 20.11% CAGR to 2030.

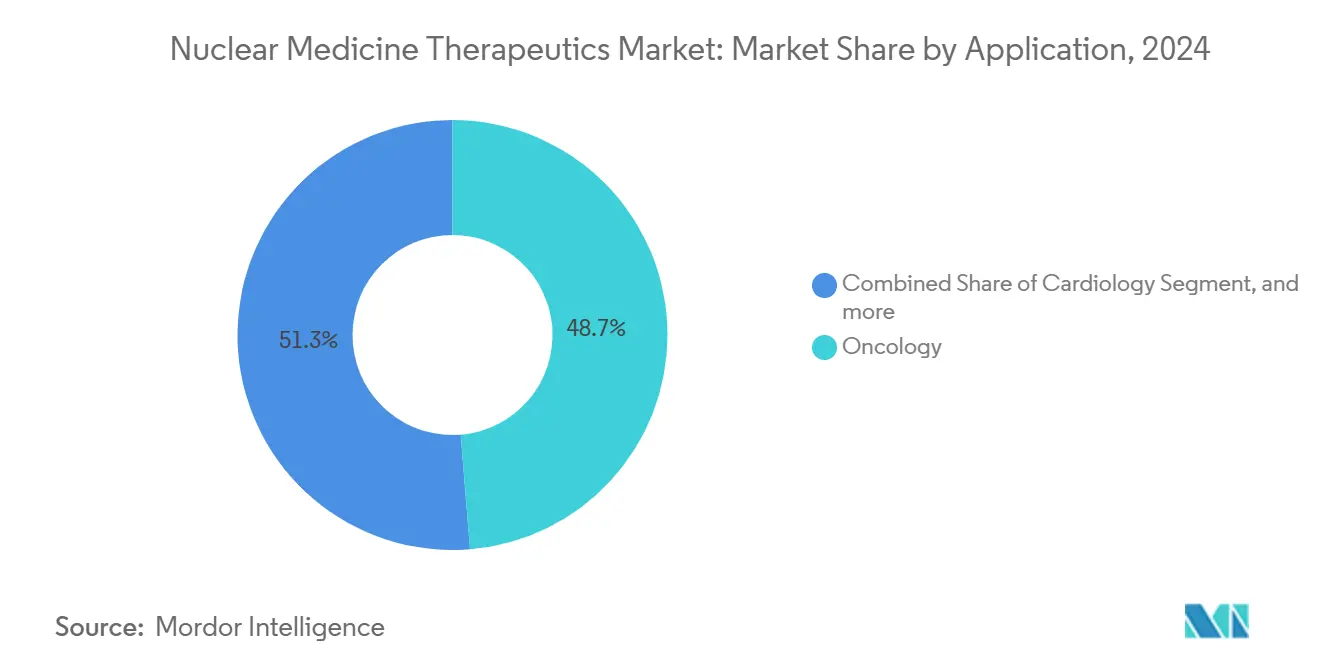

- By application, oncology held 48.68% share of the nuclear medicine therapeutics market size in 2024, whereas neurology is set to grow at 21.29% CAGR between 2025-2030.

- By end-user, hospitals and cancer centers captured 57.26% share of the nuclear medicine therapeutics market in 2024, while radiopharmacies expand at 20.31% CAGR.

- By geography, North America dominated with 46.12% share of the nuclear medicine therapeutics market in 2024; Asia Pacific shows the fastest 22.43% CAGR through 2030.

Global Nuclear Medicine Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of cancer | 4.20% | Global | Long term (≥ 4 years) |

| Advances in targeted radiopharmaceuticals | 5.80% | North America, EU, APAC core | Medium term (2-4 years) |

| Rising demand for minimally invasive and precision medicine | 3.10% | Global | Medium term (2-4 years) |

| Strategic initiatives of market players and product launches | 2.70% | Global | Short term (≤ 2 years) |

| Expansion of nuclear medicine infrastructure | 2.40% | APAC core, MEA spill-over | Long term (≥ 4 years) |

| Improved clinical evidence and reimbursement support | 1.60% | North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Burden of Cancer

Global cancer incidence is projected to exceed 29.9 million new cases by 2040, intensifying demand for alternatives to surgery and chemotherapy. Alpha-emitting agents such as actinium-225 PSMA therapy deliver concentrated energy to tumors with minimal collateral damage, shifting protocols toward radiopharmaceutical first-line use. Companies expedite research programs, and Pluvicto has become the first blockbuster radioligand, validating commercial potential. Theranostics now allow clinicians to image, treat, and follow tumors in one workflow, reducing redundant therapies and improving quality of life.

Advances in Targeted Radiopharmaceuticals

Lead-212 and terbium-161 represent the next wave of isotopes. Orano Med opened the world’s first industrial-scale lead-212 plant in January 2025, ensuring reliable supply for alpha programs. Preclinical data show terbium-161 outperforms lutetium-177 in lymphoma models, opening new avenues for hematologic malignancies. Enhanced chelators and vectors extend half-life in vivo, broadening indications such as beta-amyloid plaque targeting for Alzheimer’s disease[1]Society of Nuclear Medicine and Molecular Imaging, “Novel Radionuclide Therapy Represents Potential Paradigm Shift in the Treatment of Alzheimer’s Disease,” snmmi.org.

Rising Demand for Minimally Invasive and Precision Medicine

Healthcare systems embrace therapies that shorten hospital stays and improve safety. Flurpiridaz F-18 won FDA approval for cardiac imaging, enabling stress tests with higher diagnostic accuracy than SPECT. Machine-learning-driven dosimetry reduces patient exposure by producing instant dose calculations from a single time point[2]Journal of Nuclear Medicine, “Instant Single-Time-Point Dosimetry Using Machine Learning,” jnm.snmjournals.org . Companion diagnostics ensure only biomarker-fit patients receive therapy, improving outcomes and reducing cost overruns.

Strategic Initiatives of Market Players

Vertical integration defines competitive strategy. Curium’s acquisition of Monrol in March 2025 secures lutetium-177 output for global customers. GE HealthCare gained full control of Nihon Medi-Physics to consolidate its radiopharmacy network in Japan, the world’s most cyclotron-dense nation. Telix’s FDA approval of Gozellix in March 2025 expands prostate imaging choices and supports therapy planning.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of radiopharmaceutical procedures | -2.80% | Global, especially emerging markets | Medium term (2-4 years) |

| Stringent regulatory and licensing barriers | -1.90% | Global | Long term (≥ 4 years) |

| Complex production and short life of radioisotopes | -2.10% | Global | Medium term (2-4 years) |

| Scarcity of trained radiochemists | -1.40% | Developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Radiopharmaceutical Procedures

Therapies based on lutetium-177 often exceed USD 50,000 per course, presenting affordability hurdles. CMS now reimburses diagnostic radiopharmaceuticals above USD 630 separately, improving hospital economics[3]Society of Nuclear Medicine and Molecular Imaging, “CMS Adjusts Nuclear Medicine Reimbursement Policy, Expanding Access to Life-Saving Scans,” snmmi.org. Outcome-based pricing and risk-sharing contracts are under exploration, allowing wider adoption without eroding margins.

Complex Production and Short Life of Radioisotopes

The 10-day half-life of actinium-225 and 10.6-hour half-life of lead-212 tighten logistics windows. Alternative accelerator-based methods can generate carrier-free lutetium-177, reducing dependence on aging reactors. Regional production hubs in China and the United States shorten supply chains and buffer against geopolitical disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Beta Emitters Drive Market Leadership

Beta emitters controlled 67.58% of the nuclear medicine therapeutics market in 2024 as clinicians favored established isotopes such as lutetium-177 and iodine-131. Lutetium-177’s uptake accelerated after SHINE Technologies introduced high-specific-activity Ilumira, delivering tighter tumor targeting and easing manufacturing constraints. Alpha emitters post the strongest trajectory: the nuclear medicine therapeutics market size for alpha emitters is projected to expand at 23.55% CAGR through 2030, driven by commercial actinium-225 output from Eckert & Ziegler.

Alpha emitters’ high LET radiation cuts treatment cycles, improving patient convenience. Lead-212’s practical half-life supports centralized production, while radium-223 retains value for bone metastases. Beta-based yttrium-90 broadened beyond hepatocellular carcinoma into synovectomy, extending the nuclear medicine therapeutics market’s clinical footprint.

By Therapeutic Modality: Targeted Radioligand Therapy Leads Innovation

Targeted radioligand therapy delivered 49.56% of overall revenue in 2024. The PSMAfore Phase 3 study confirmed lutetium-177 PSMA-617’s median progression-free survival advantage in taxane-naive prostate cancer. Real-world evidence showed 73.5% overall survival at follow-up for Pluvicto-treated patients. BNCT follows with a 20.11% CAGR, leveraging novel boron-containing nanoparticles that pair neutron activation with immune checkpoint inhibition.

Radio-immunotherapy marries monoclonal antibodies with high-energy isotopes, opening hard-to-reach solid tumors. Automated planning tools limit operator variability, supporting a broader user base and expanding the nuclear medicine therapeutics market even in smaller treatment centers.

By Application: Oncology Dominance with Neurology Emergence

Oncology retained 48.68% market contribution in 2024, led by prostate, neuroendocrine, and thyroid cancers. Neuroendocrine lesions respond well to lead-212 and actinium-225 labeled somatostatin analogs, an advantage that widens treatment options. Neurology shows a 21.29% CAGR; bismuth-213 agents eliminated up to 100% of beta-amyloid plaques in preclinical Alzheimer’s models.

Cardiology benefits from flurpiridaz-enhanced perfusion imaging, and endocrinology continues to rely on iodine-131 for thyroid malignancies. Pain palliation using bone-seeking isotopes remains relevant for metastatic patients who cannot tolerate systemic chemotherapy.

By End-user: Hospitals Lead While Radiopharmacies Accelerate

Hospitals and cancer centers captured 57.26% revenue in 2024, aided by cross-functional nuclear medicine teams. UChicago Medicine’s theranostic center exemplifies integrated care that merges imaging, planning, and therapy. Radiopharmacies expand fastest at 20.31% CAGR as distributed manufacturing lowers transport time and radiation loss. Jubilant Radiopharma’s network delivers turnkey solutions under single fee-per-test models, easing adoption for community hospitals.

Academic institutes partner with industry to bridge commercialization gaps, while specialty clinics adopt same-day discharge protocols, boosting throughput and supporting broader nuclear medicine therapeutics market penetration.

Geography Analysis

North America generated 46.12% revenue in 2024 on the back of 2,000+ PET/CT units and favorable CMS reimbursement that unbundles high-priced isotopes. The United States hosts an expanding isotope production base, as Novartis invests over USD 200 million in domestic facilities to hedge against imports. Sutter Health’s AI-imaging partnership with GE HealthCare democratizes advanced services across California.

Asia Pacific records the fastest 22.43% CAGR. China licensed over 40 radiopharmaceuticals and targets 10 million annual procedures by 2035, underpinning local demand. SHINE Technologies partners with Primo Biotech to distribute lutetium-177 across Taiwan, Japan, South Korea, and Singapore, solidifying supply lines. Australia’s new production complexes and strong government support create a regional export hub.

Europe shows steadier expansion, backed by robust R&D and EMA approvals, yet reactor outages expose supply fragilities. Orano’s thorium-228 project seeks to add redundancy to isotope chains. Middle East and Africa progress slowly, although Israel and Saudi Arabia plan cyclotron-based facilities that will seed future growth.

Competitive Landscape

Market leaders blend therapy development with isotope supply to protect margins and guarantee continuity. Novartis vertically integrates through multiple U.S. reactors, shrinking external dependence. Lantheus crossed the USD 1 billion sales mark with PYLARIFY, proving scale economics in targeted imaging. Siemens Healthineers offers end-to-end theranostic platforms encompassing scanners, software, and therapy solutions.

Emerging specialists focus on radioisotope innovation. SHINE’s low-waste, non-reactor approach could redefine the nuclear medicine therapeutics market by reducing production risk and environmental footprint. Actinium Pharmaceuticals partners with Memorial Sloan Kettering to extend the Actimab-A program into new indications. IBA and Jubilant deploy next-generation compact cyclotrons that localize PET isotope output, shortening lead times.

White-space opportunities persist in neurodegenerative diseases and rare cancers. Companion diagnostics bundled with therapeutic agents allow tailored regimens that enhance efficacy and pricing power. Companies that unite supply security with clinical evidence stand to capture the greatest share of future nuclear medicine therapeutics market growth.

Nuclear Medicine Therapeutics Industry Leaders

Bayer AG

Curium Pharma

Lantheus Holdings

Novartis AG

Telix Pharmaceuticals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Curium finalized the acquisition of Monrol to boost lutetium-177 output and expand its PET footprint.

- January 2025: SHINE Technologies and Primo Biotech partnered to distribute Ilumira across key Asia-Pacific markets.

- December 2024: Eckert & Ziegler began commercial actinium-225 production, enlarging global alpha-emitter supply.

- June 2024: Orano Med opened the first industrial-scale lead-212 facility, reinforcing alpha-therapy pipelines.

Global Nuclear Medicine Therapeutics Market Report Scope

As per the scope of the report, nuclear medicine therapeutics involves using radioactive substances to treat diseases, primarily cancer. It delivers targeted radiation to destroy diseased cells while minimizing damage to healthy tissue. Common examples include radioiodine therapy for thyroid cancer and radiopharmaceuticals for neuroendocrine tumors. This approach offers a personalized and effective treatment option in modern medicine.

The nuclear medicine therapeutics market is segmented by Type (Alpha Emitters, Beta Emitters, and Brachytherapy), Therapeutic Modality (Radio-Immunotherapy, Brachytherapy, Targeted Radioligand Therapy (RLT), and Boron Neutron Capture Therapy (BNCT)), Application (Oncology, Cardiology, Endocrinology, Neurology, and Pain Palliation/Bone Metastasis), and End User (Hospitals & Cancer Centers, Specialty Clinics, Academic & Research Institutes, and Radiopharmacies), and geography (North America, Europe, Asia Pacific, South America, and Middle East & Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Alpha Emitters | Radium-223 (Ra-223) & Alpharadin |

| Actinium-225 (Ac-225) | |

| Lead-212 / Bismuth-212 | |

| Others | |

| 5.1.2 Beta Emitters | Iodine-131 (I-131) |

| Lutetium-177 (Lu-177) | |

| Yttrium-90 (Y-90) | |

| Others | |

| 5.1.3 Brachytherapy | Cesium-131 |

| Iodine-125 | |

| Palladium-103 |

| Targeted Radioligand Therapy (RLT) |

| Radio-immunotherapy |

| Brachytherapy |

| Boron Neutron Capture Therapy (BNCT) |

| Oncology |

| Cardiology |

| Endocrinology (Thyroid, Parathyroid) |

| Neurology |

| Pain Palliation / Bone Metastasis |

| Hospitals & Cancer Centers |

| Specialty Clinics |

| Academic & Research Institutes |

| Radiopharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Alpha Emitters | Radium-223 (Ra-223) & Alpharadin |

| Actinium-225 (Ac-225) | ||

| Lead-212 / Bismuth-212 | ||

| Others | ||

| 5.1.2 Beta Emitters | Iodine-131 (I-131) | |

| Lutetium-177 (Lu-177) | ||

| Yttrium-90 (Y-90) | ||

| Others | ||

| 5.1.3 Brachytherapy | Cesium-131 | |

| Iodine-125 | ||

| Palladium-103 | ||

| By Therapeutic Modality | Targeted Radioligand Therapy (RLT) | |

| Radio-immunotherapy | ||

| Brachytherapy | ||

| Boron Neutron Capture Therapy (BNCT) | ||

| By Application | Oncology | |

| Cardiology | ||

| Endocrinology (Thyroid, Parathyroid) | ||

| Neurology | ||

| Pain Palliation / Bone Metastasis | ||

| By End-user | Hospitals & Cancer Centers | |

| Specialty Clinics | ||

| Academic & Research Institutes | ||

| Radiopharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the market ?

The market is valued at USD 4.33 billion in 2025.

How fast is the nuclear medicine therapeutics market expected to grow?

It is projected to expand at a 19.78% CAGR, reaching USD 10.67 billion by 2030.

Which segment holds the largest nuclear medicine therapeutics market share?

Beta emitters command 67.58% share, led by lutetium-177 applications.

Which region will grow the fastest through 2030?

Asia Pacific shows the highest 22.43% CAGR due to infrastructure expansion and rising procedure volumes.

Why are alpha emitters gaining traction?

They deliver higher-energy radiation over shorter paths, improving tumor control while reducing collateral damage, and commercial supply chains for actinium-225 and lead-212 are now in place.

Page last updated on: