North America Cafes And Bars Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

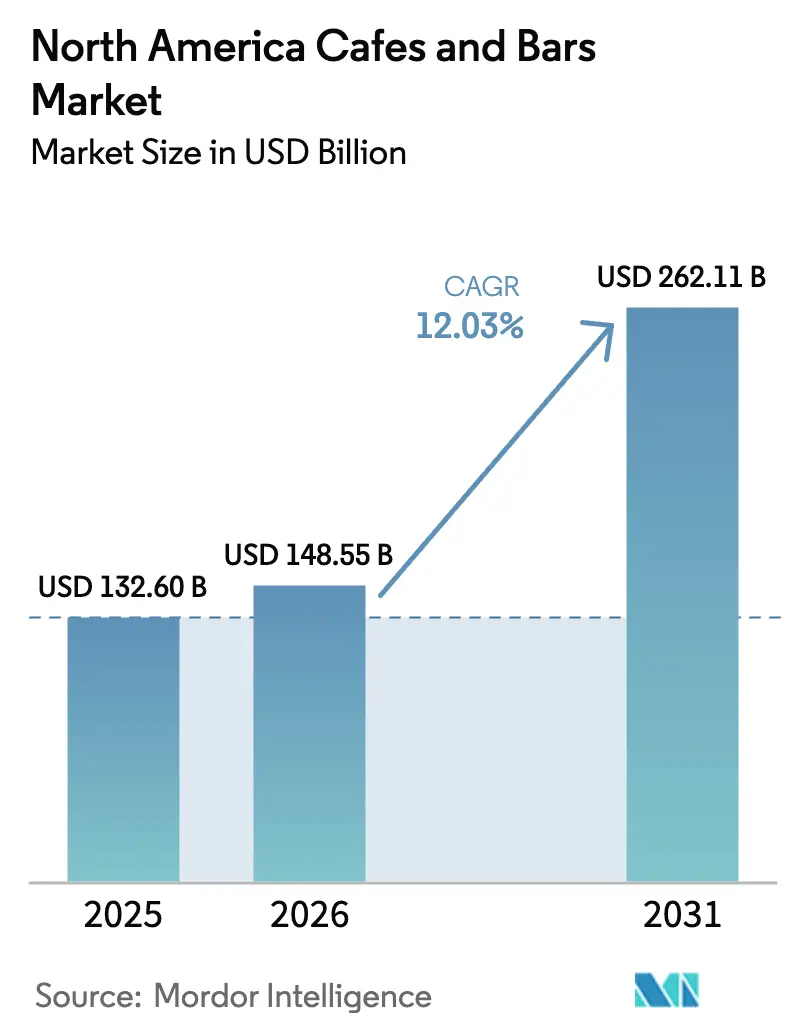

| Base Year Market Size (2025) | USD 132.60 Billion |

| Market Size (2026) | USD 148.55 Billion |

| Market Size (2031) | USD 262.11 Billion |

| Growth Rate (2026 - 2031) | 12.03% CAGR |

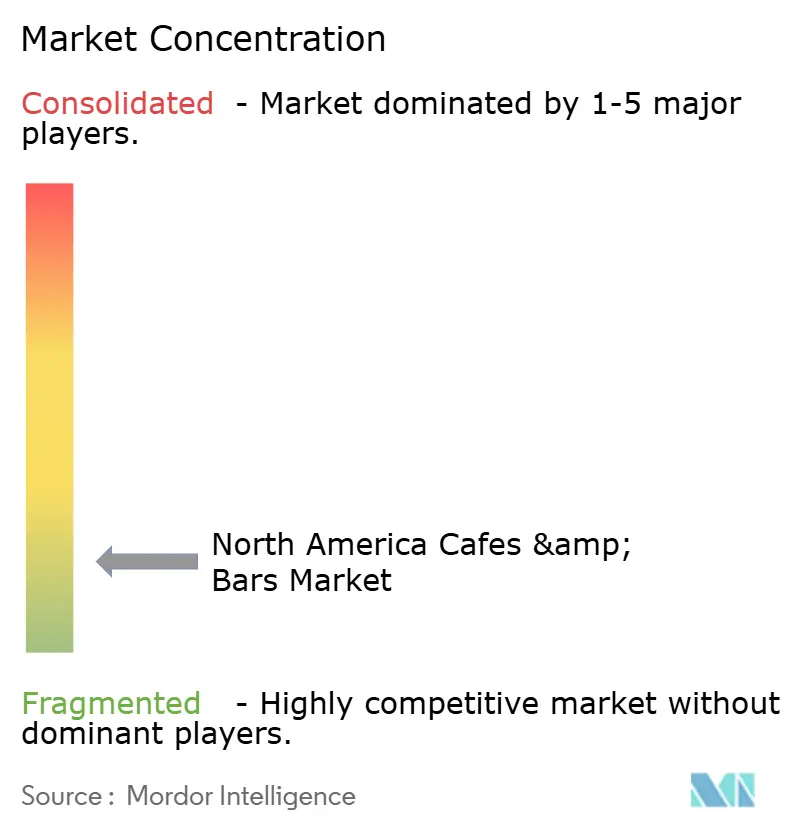

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Cafes And Bars Market Analysis by Mordor Intelligence

The North America Cafes and Bars market size was valued at USD 132.60 billion in 2025 and estimated to grow from USD 148.55 billion in 2026 to reach USD 262.11 billion by 2031, at a CAGR of 12.03% during the forecast period (2026-2031). Driven by changing consumer lifestyles and a burgeoning coffee culture, the North American Cafes and Bars market is witnessing robust growth. Millennials and Gen Z consumers are gravitating towards unique experiences and high-quality, customizable food and beverage options. They now favor specialty coffee, craft beers, and innovative cocktails, moving away from traditional offerings. Post-pandemic, there's been a notable resurgence in social gatherings, solidifying cafes and bars as pivotal social hubs. Technology plays a significant role in this evolution, with digital ordering, loyalty programs, and mobile apps enhancing both convenience and customer engagement. Supporting this momentum, government and industry associations, like the National Coffee Association in the US, emphasize the market's strength, noting that 67% of adults now consume coffee daily. Product innovations are also shaping the landscape, with the introduction of "better-for-you" (BFY) non-alcoholic beverages catering to health-conscious consumers, and a surge in plant-based options, including alternative milks and vegan dishes, on major chain menus. Adding to the market's dynamism, international players like South Korea's Camel Coffee, which unveiled its inaugural US outlet in April 2024, are making their mark.

Key Report Takeaways

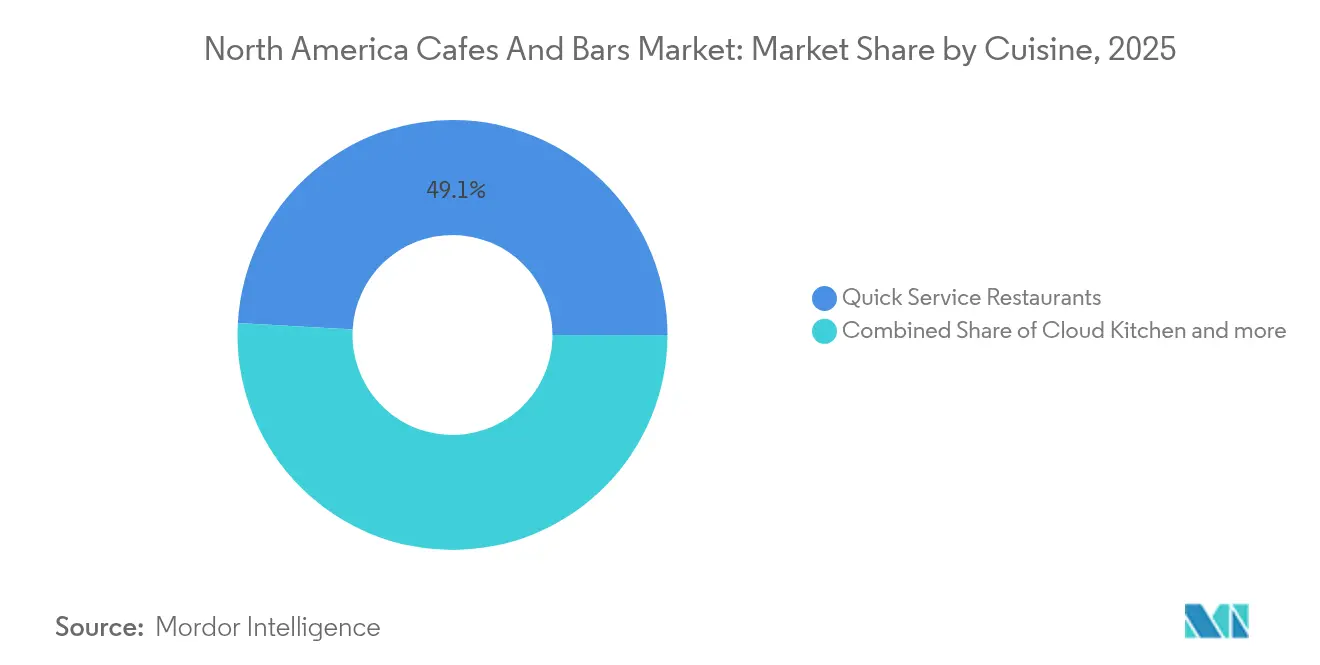

- By cuisine, quick service restaurants led with 49.12% of the North America cafes and bars market share in 2025, while Cloud Kitchens recorded the fastest expansion at a 14.42% CAGR through 2031.

- By outlet, independent outlets captured 55.88% of the 2025 revenue and are also projected to grow the quickest, at a 13.78% CAGR, to 2031.

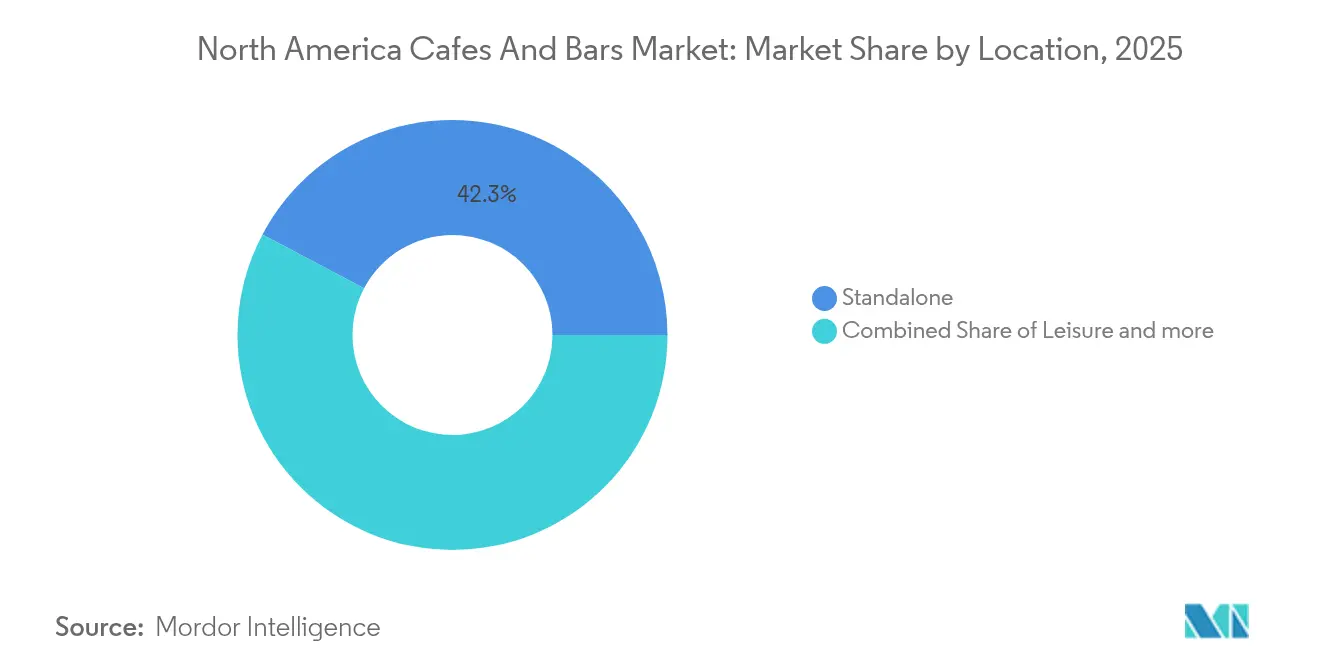

- by location, standalone formats secured a 42.25% share in 2025; Leisure locations posted the top growth outlook at a 14.69% CAGR through 2031.

- By service, dine-in held 55.97% of spending in 2025, whereas Delivery is forecast to advance at a 14.41% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cafes And Bars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong coffee culture and specialty beverage demand | +2.8% | North America, with the highest intensity in the Northeast United States and urban Canada | Long term (≥ 4 years) |

| Adoption of digital technology | +2.1% | Global, with early adoption in United States metropolitan areas | Medium term (2-4 years) |

| Changing consumer preferences for health and wellness | +1.7% | North America, particularly among Gen Z and Millennials | Long term (≥ 4 years) |

| Innovation in product offerings and service models | +1.9% | North America, with spillover to urban centers | Medium term (2-4 years) |

| Tourism and domestic travel | +1.5% | United States tourism destinations, Canadian urban centers, and border regions | Short term (≤ 2 years) |

| Emphasis on sustainability and ethical sourcing | +1.2% | North America, with premium positioning in urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong coffee culture and specialty beverage demand

North America's coffee consumption is undergoing a profound transformation, signaling shifts that transcend conventional market dynamics. In 2024, 45% of American adults embraced specialty coffee, marking a historic first where it eclipsed traditional coffee consumption. On average, specialty coffee aficionados indulge in 2.8 cups daily, outpacing the 1.8 cups consumed by their traditional counterparts, as reported by the Specialty Coffee Association[1]Source: Specialty Coffee Association (SCA), "2024 National Coffee Data Trends", sca.coffee. The Northeast stands out, with 61% of its residents consuming specialty coffee in the past week, highlighting regional pockets of premium demand that bolster higher-margin operations. Specialty formats, excluding espresso, like cold brew and nitro coffee, saw a 7% year-over-year surge. Meanwhile, ready-to-drink specialty coffee usage skyrocketed over 83% since 2023, underscoring a consumer trend willing to pay a premium for both convenience and quality. Demographic shifts bolster this cultural evolution: 66% of 25-39-year-olds are weekly specialty coffee consumers, laying the groundwork for continued premium demand growth. This trend isn't confined to coffee; functional beverages are also on the rise. Adaptogenic and wellness-centric drinks are gaining popularity as consumers gravitate towards products that resonate with their health-conscious lifestyles.

Adoption of digital technology

Digital technology is reshaping North America's Cafes and Bars market, boosting operational efficiency, enhancing customer experiences, and facilitating personalized marketing. This shift is marked by the rise of mobile ordering apps, contactless payment systems, and data analytics platforms. Industry bodies, like the National Restaurant Association (NRA), underscore technology's strategic role. Their "State of the Restaurant Industry 2024" report revealed that 55% of operators intend to boost tech investments, aiming to tackle labor challenges and cater to the growing consumer demand for convenience[2]Source: National Restaurant Association, "National Restaurant Association Technology Landscape report", restaurant.org. Major coffee chains, for example, have upgraded their mobile apps to provide tailored rewards and simplify pick-up processes. Noteworthy product innovations include using artificial intelligence (AI) for predictive inventory management, minimizing waste, and employing AI-driven chatbots for enhanced customer service. Furthermore, there's a rising inclination towards "smart kitchen" technologies and back-of-house automation, adeptly handling orders from various digital platforms, ensuring swift service and precise order fulfillment. The American Beverage Association (ABA) champions tech-driven efficiency initiatives in distribution. This broad embrace of digital tools not only caters to consumer preferences but also serves as a crucial strategy for market players striving to stay competitive and profitable amidst operational challenges.

Changing consumer preferences for health and wellness

In North America, cafes and bars are evolving in response to a pronounced shift in consumer preferences towards health and wellness. Patrons are now gravitating towards functional beverages and healthier food choices that resonate with their lifestyle aspirations. Heightened awareness of the diet-health nexus, coupled with concerns over lifestyle-induced ailments like obesity, has led consumers to prioritize preventive health measures. They are also demanding transparency in ingredient sourcing and nutritional labeling. For instance, the Organic Trade Association reported that U.S. organic food sales reached about USD 65.4 billion in 2024, up from USD 63.8 billion in 2023[3]Source: Organic Trade Association, "U.S. Organic Industry Survey 2025", ota.com. Industry bodies are taking note: the National Restaurant Association highlights a growing appetite for clean labels, organic offerings, and sustainable practices. Recent product innovations underscore this market shift: major chains are broadening their plant-based selections with alternative milks like oat and almond, there's a rising popularity of non-alcoholic substitutes for classic cocktails, and functional beverages are making waves, featuring ingredients such as probiotics and adaptogens (think adaptogenic lattes). Juice and smoothie bars, eyeing robust growth, are rolling out "superfood smoothies" and plant-based bowls brimming with diverse vegetables, herbs, and spices, directly appealing to the health-centric consumer and fueling market growth.

Innovation in product offerings and service models

In North America, cafes and bars are innovating their product offerings and service models to keep pace with rapidly changing consumer preferences. This innovation is evident in menu diversification, with a strong focus on health-conscious, plant-based, and premium options to cater to a sophisticated palate. For instance, the National Restaurant Association's "What's Hot Culinary Forecast 2024" underscores the rising trend of functional beverages and sustainable choices. In line with this, cafes and bars are rolling out products like "adaptogenic lattes" infused with mushrooms and herbs, and a broader selection of low-ABV or non-alcoholic craft cocktails. On the service front, innovations are largely driven by a quest for convenience and efficiency. The market is embracing digital transformation, evident in the surge of mobile ordering, partnerships for delivery, and the rise of contactless payments. A standout move in 2024 was DoorDash unveiling its AI-driven voice ordering tech, streamlining phone orders and cutting down wait times. Additionally, AI is playing a pivotal role in predictive inventory management, helping businesses curb waste and manage costs. Beyond these, many establishments are enhancing the customer experience by offering robust Wi-Fi and dedicated workspaces, making them attractive spots for remote workers. This relentless drive for innovation keeps the North American cafe and bar scene vibrant, competitive, and on a growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense market saturation and high competition | -1.8% | North America, particularly urban markets and established chains | Medium term (2-4 years) |

| Labor shortages and high employee turnover | -2.3% | North America, with an acute impact in metropolitan areas | Short term (≤ 2 years) |

| Operational complexity and overhead costs | -1.4% | North America, affecting independent operators disproportionately | Medium term (2-4 years) |

| Supply chain disruptions and volatility | -1.9% | Global impact with regional variations in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense market saturation and high competition

In North America, cafes and bars grapple with intense market saturation and fierce competition, leading to squeezed profit margins, challenges in customer acquisition, and heightened costs for differentiation. With choices spanning from independent cafes to expansive national chains, businesses frequently find themselves in price wars and aggressive marketing battles, jeopardizing profitability -especially for smaller, independent operators. Industry associations, including the National Restaurant Association, underscore these challenges. Their "State of the Restaurant Industry 2024" report spotlighted competition as a primary concern, emphasizing the ongoing struggle to attract and retain customers. While U.S. bodies like the Small Business Administration (SBA) and Canada's BDC provide assistance programs, these efforts don't alter the fundamentally hyper-competitive landscape. In light of these challenges, businesses are compelled to innovate their product offerings and service models. For example, in 2024, chains rolled out unique, limited-time menu items - like a major chain's "sparkling elderflower cold brew" - to create buzz and draw in customers. Looking ahead to 2025, service model innovations are set to include bolstered delivery and off-premise dining options, which the NRA highlights as increasingly significant to total sales, especially as traditional dine-in segments become saturated. These examples underscore the relentless pressure on businesses to adapt and innovate in a fiercely competitive environment.

Labor shortages and high employee turnover

Labor shortages and high employee turnover significantly restrain the North American Cafes and Bars market, directly impacting operational efficiency, service quality, and overall profitability. The industry consistently struggles to attract and retain workers due to demanding work environments, a lack of benefits, and competitive wages offered by other sectors. This leads to a shallow talent pool and increased training costs. A 2024 National Restaurant Association survey highlights the widespread nature of this challenge, revealing that 77% of operators faced difficulties in hiring and retaining staff. Consequently, businesses experience reduced operating hours, service slowdowns, and heightened labor costs, all of which squeeze profit margins. While government sources haven't directly tackled the private sector's turnover issues, they've extended support, such as the US Small Business Administration's Restaurant Revitalization Fund, during peak crises. In light of these challenges, businesses increasingly turn to technology and innovation as mitigative measures. Notable product developments in 2024 and 2025 showcase this trend: AI-powered ordering kiosks are becoming commonplace, mobile apps facilitate seamless ordering and payment, and some chains are introducing back-of-house automation, like robotic arms for food preparation, to lessen reliance on manual labor. Such technological adaptations emerge as vital strategies for market players, enabling them to sustain operations and manage costs amid the ongoing labor crisis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: QSR Dominance Drives Cloud Innovation

In 2025, Quick Service Restaurants (QSRs) held a commanding 49.12% market share, skillfully leveraging operational efficiency and brand recognition to fend off intensifying competition from emerging formats. Meanwhile, Cloud Kitchen concepts, with a 14.42% CAGR growth projected through 2031, are shaking up traditional models. They are capitalizing on the surging demand for delivery and maintaining reduced overheads, allowing for swift scaling and market entry. Bars and Pubs, while generating notable sales in 2024, are witnessing a slight downturn. This shift is attributed to changing consumer preferences, leaning more towards experiential dining and specialty beverages. Cafes, positioned at the premium end of the culinary spectrum, are reaping rewards from the rising specialty coffee culture. Their per-transaction values are bolstered by a focus on artisanal beverage preparation and a trend towards experiential consumption.

Juice, Smoothie, and Dessert Bars, alongside Specialist Coffee and Tea Shops, are carving out niche markets. They're riding the wave of health-conscious consumer trends and adopting premium positioning strategies. The lines between traditional segments are blurring, as seen in the merger of Five Watt Coffee and Sencha Tea Bar. Their new venture, Amplified Experiences, is set to launch a third brand that melds coffee, tea, and boba offerings. Technology adoption isn't uniform across the board. QSRs are at the forefront, embracing automation and mobile ordering. In contrast, specialty establishments prioritize artisanal preparation and direct customer engagement. While all cuisine segments must adhere to the FDA Food Code updates, the intricacies of implementation differ. This variance is largely influenced by the sophistication of operations and the nuances of food handling processes.

By Outlet: Independent Innovation Outpaces Chain Efficiency

In 2025, independent outlets command a leading 55.88% market share and are set to grow at a brisk 13.78% CAGR through 2031. Their success underscores an entrepreneurial knack for swiftly adapting to local tastes and emerging trends. This agility allows them to pivot towards specialty offerings and unique experiences, carving out a community-centric niche that larger chains find hard to replicate on a grand scale. Meanwhile, chained outlets, bolstered by operational efficiency and brand clout, are not standing still. Major players, like Starbucks, are making bold moves with plans for 2,000 new U.S. locations by 2025 and a hefty USD 450 million investment in equipment upgrades, aiming to boost throughput and trim labor needs. The competitive landscape is heating up: chains are turning to franchise models to tap into local insights, while independents are harnessing technology to scale their operations.

Franchise dynamics are shifting, melding the efficiency of chains with the nimbleness of independents. Take Caribou Coffee, a regional favorite, which is adding 159 new stores in 2024, all while staying attuned to local nuances. Yet, it's not all smooth sailing for independent operators. They're grappling with mounting pressures from operational complexities, rising labor costs, and tech demands. A report from the National Restaurant Association highlights the strain: 38% of independents, despite seeing revenue growth in 2024, are still navigating unprofitability. The lines between outlet types are starting to blur. Independents are adopting operational standards reminiscent of chains, while chains are dabbling in local tweaks and community-centric strategies. And the financial world is taking note: private equity and venture capital activity remains vigorous, backing both independent expansions and chain acquisitions, signaling a vote of confidence in both outlet formats, even amidst their challenges.

By Location: Standalone Strength Meets Leisure Growth

In 2025, standalone locations secured a 42.25% share of the market, leveraging their destination allure, ample parking, and operational adaptability to craft an optimal customer experience. Leisure spots, buoyed by a tourism resurgence and heightened discretionary spending on experiences, are witnessing the swiftest growth at a 14.69% CAGR projected through 2031. Retail venues, with their steady foot traffic and strategic convenience positioning, are especially advantageous for grab-and-go formats and operations catering to commuters' habitual consumption. While lodging locations cater to a captive audience, they grapple with challenges stemming from diminished business travel and evolving accommodation trends, leading to unpredictable demand.

Travel hubs, encompassing airports and transit centers, are on the mend from pandemic setbacks. Yet, they lag behind historical performance benchmarks, grappling with enduring shifts in business travel dynamics and the ebb and flow of international visitors. This segmentation of locations mirrors broader transformations in consumer mobility and lifestyle choices. Leisure-centric venues are reaping rewards from a surge in domestic tourism spending, which, as reported by the World Travel and Tourism Council, hit USD 1.37 trillion in 2024, surpassing pre-pandemic figures by 9%. Standalone operations, with their unmatched flexibility, are pioneering innovations in format and customer experience. This adaptability has birthed concepts like drive-thru-only and pickup-centric designs, aligning seamlessly with evolving consumer tastes. However, regulatory compliance presents a varied landscape: travel and lodging venues face heightened scrutiny from health departments and security entities, complicating operations and inflating costs.

By Service Type: Dine-in Resilience Drives Delivery Expansion

In 2025, the dine-in service held a dominant 55.97% market share, underscoring the lasting allure of experiential consumption and social interactions that epitomize the premium coffee and bar scene. Meanwhile, the delivery service is reshaping the competitive arena, boasting a robust 14.41% CAGR growth projected through 2031. This surge is fueled by an increasing demand for convenience and the expansion of technology platforms, which not only attract new customers but also extend service hours. The takeaway service strikes a balance, merging the dine-in's experiential charm with the convenience of delivery. It appeals to consumers who prioritize quality and speed but wish to avoid premium service charges. Notably, a report from the National Restaurant Association highlighted a shift in consumer behavior, with 49% of restaurants reporting a rise in off-premise sales in 2024 compared to 2019.

Across these service types, the integration of technology varies. Delivery operations, for instance, require advanced systems for order management, routing optimization, and quality preservation, which can be daunting challenges for independent operators. Starbucks stands out with its diverse service strategy: its delivery segment has seen an impressive 80% year-over-year growth, and its mobile order and pay feature accounted for a significant 31% of U.S. transactions, highlighting the synergy in optimizing various service types. Labor dynamics also shift across these services. Dine-in venues lean on skilled baristas and attentive customer service, whereas delivery-centric models can streamline operations with fewer front-of-house staff and automated prep systems. Regulatory nuances further complicate the landscape: delivery services grapple with stringent food safety transportation mandates and the added complexities of third-party platform compliance, both of which escalate operational costs.

Geography Analysis

In 2025, the U.S. led the revenue race with a commanding 46.12% share, buoyed by its rich specialty coffee culture and a thriving domestic travel scene. However, a regulatory patchwork poses challenges: while some states cling to the 1995 Food Code, others have swiftly adopted the 2022 version. Labor conditions present a mixed bag, with Midwest markets enjoying sub-4% unemployment, in stark contrast to double-digit rates in coastal cities. These disparities, coupled with varying minimum wage standards and tipped-credit phaseouts, demand tailored pay structures across regions. Meanwhile, brands eyeing expansion find new opportunities as infrastructure investments enhance access to highway rest areas and airport concessions.

Canada is set to take off, boasting the fastest growth trajectory at a projected 15.95% CAGR through 2031. This surge is fueled by rising domestic travel spending and a notable rebound in international visitors. Canada's immigration policies further bolster the sector's labor force, with over a quarter of food-service staff being foreign-born and immigrant owners making up more than half. Health Canada's updated additive regulations pave the way for ingredient innovations, and with provincial wages trailing behind major U.S. metros, businesses enjoy a competitive edge. Additionally, the stability of the Canadian dollar against the USD helps mitigate import inflation on coffee, equipment, and packaging.

Mexico, along with the broader North American landscape, presents a promising upside. In Mexico, declining unemployment and increasing real incomes are driving demand for discretionary beverages. Simultaneously, resort corridors benefit from heightened café demand, thanks to a boost in tourism receipts. While carbon pricing initiatives slightly elevate operating costs, they also encourage the adoption of low-emission equipment, serving as a marketing advantage. Cross-border dynamics play a crucial role: a dip in Canadian and Mexican visitors has reduced outlet traffic in border counties. However, domestic migration trends towards Sun Belt cities are creating fresh catchment areas. Furthermore, with green-bean invoices pegged in USD, fluctuations in exchange rates are influencing menu pricing strategies. Collectively, these factors underscore the diverse momentum propelling the North American cafes and bars market.

Competitive Landscape

The market shows a moderate concentration, with Starbucks commanding nearly 40% of the outlets as the dominant player. However, regional chains and rapidly growing independents dilute its price-setting power. Starbucks is investing USD 600 million into digital personalization and advanced brewing algorithms. Additionally, it's introducing Clover Vertica brewers, which reduce hot-coffee assembly time to just 36 seconds. Dutch Bros, having surpassed 850 units, achieved a remarkable 39% sales growth in 2024, driven by their drive-thru-only outlets manned by lively teams. Meanwhile, Caribou has struck a USD 260 million licensing deal with JDE Peet’s, broadening its packaged products reach to 30 more countries, thereby boosting its domestic brand presence.

With 84% of finance executives anticipating an uptick in mergers and acquisitions, the appetite for deals is palpable. Roll-ups are zeroing in on multi-shop independents, unlocking their EBITDA potential through shared roasting, bulk purchasing, and standardized loyalty technology. Automation firms are joining forces with established roasters: Octane Coffee’s rapid 10-second service is drawing interest from landlords for spaces typically deemed too small for traditional cafés. Equipment manufacturers are shifting their approach, moving from singular sales to a Robotics-as-a-Service model. This transition turns a capital expense into an operational one, making it more palatable for mid-tier operators. The competitive landscape is increasingly defined by AI-driven ordering, seamless payment processes, and a commitment to sustainability, attributes that are proving more challenging to replicate than standard commodity lattes.

Regional nuances heighten the competition. In California, rising mandated wages push chains to adopt more robotics, while independent shops leverage a culture of tipping to bridge pay disparities. In Canada, ownership by immigrants enriches the beverage landscape with offerings like bubble tea, cardamom cold brew, and horchata espressos, fostering strong local loyalty. U.S. convenience stores and grocery cafés intensify the competition, capitalizing on their high foot traffic and bulk coffee buying power to challenge specialty pricing.

North America Cafes And Bars Industry Leaders

-

Dutch Bros Inc.

-

Inspire Brands Inc.

-

Restaurant Brands International Inc.

-

Smoothie King Franchises Inc.

-

Starbucks Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bub's Bakery was launched as a collaborative effort between acclaimed pastry chef Melissa Weller and 55 Hospitality Group. Situated in a prime Manhattan location, the bakery was set to revive classic American baking traditions with a modern twist. Known for her expertise in lamination and fermentation, Weller planned to offer a rotating selection of artisanal breads, pastries, and café items.

- January 2025: Central Burrard was launched by the ownership group behind CRAFT Beer Market. Central Burrard offers a spacious and accessible casual dining experience in Vancouver. The establishment was designed as an all-day spot, serving a diverse menu that covers brunch, lunch, and dinner. It features an extensive selection of local craft beers on tap, an array of cocktails, and classic pub-style food executed with care.

- July 2024: Vela Bar y Cocina was launched in Chicago’s vibrant River North district and established itself as a popular new spot for Latin-inspired cuisine and creative cocktails. The establishment offers a lively atmosphere that transitions seamlessly from a casual dining spot to a buzzing bar in the evening. The menu features a variety of small plates designed for sharing, alongside larger main courses, emphasizing fresh ingredients and bold flavor profiles.

- May 2024: The team behind Takenaka introduced their new "Uni Bar" concept in Gastown. Building on the popularity of their Japanese food truck, this brick-and-mortar location includes a menu that specializes in fresh uni (sea urchin) dishes and oysters, complemented by a curated selection of Japanese sake, craft beers, and specialty cocktails.

North America Cafes And Bars Market Report Scope

Bars & Pubs, Cafes, Juice/Smoothie/Desserts Bars, Specialist Coffee & Tea Shops are covered as segments by Cuisine. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location. Canada, Mexico, United States are covered as segments by Country.| Bars and Pubs |

| Cafes |

| Juice/Smoothie/Desserts Bars |

| Specialist Coffee and Tea Shops |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Cuisine | Bars and Pubs |

| Cafes | |

| Juice/Smoothie/Desserts Bars | |

| Specialist Coffee and Tea Shops | |

| Outlet | Chained Outlets |

| Independent Outlets | |

| Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| Service Type | Dine-in |

| Takeaway | |

| Delivery | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms