Neopentyl Glycol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neopentyl Glycol Market Analysis by Mordor Intelligence

The Neopentyl Glycol Market size is expected to grow from USD 1.76 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.35 billion by 2031 at 5.24% CAGR over 2026-2031. The neopentyl glycol market is supported by the material's role in high-performance polyester resins, where its molecular structure contributes to heat stability, weather resistance, and long service life in demanding coating systems. Regulatory pressure on volatile organic compound emissions is pushing the market toward powder and waterborne formulations, particularly in coatings applications that require regulatory compliance and durable surface performance. BASF's October 2025 capacity addition in China, along with its launch of a reduced-carbon footprint product grade, indicates that competition in the neopentyl glycol market is advancing on two fronts: scale and lower-carbon product positioning. Price increases announced in Europe and North America during 2026 were absorbed without major signs of demand destruction, suggesting steady downstream reliance on neopentyl glycol (NPG) in resins and coatings, where substitution remains limited under current performance requirements. The market is also gaining support from insulation and lubricant applications, where thermal stability, formulation efficiency, and carbon documentation are becoming more important in supplier selection across developed end-use markets.

Key Report Takeaways

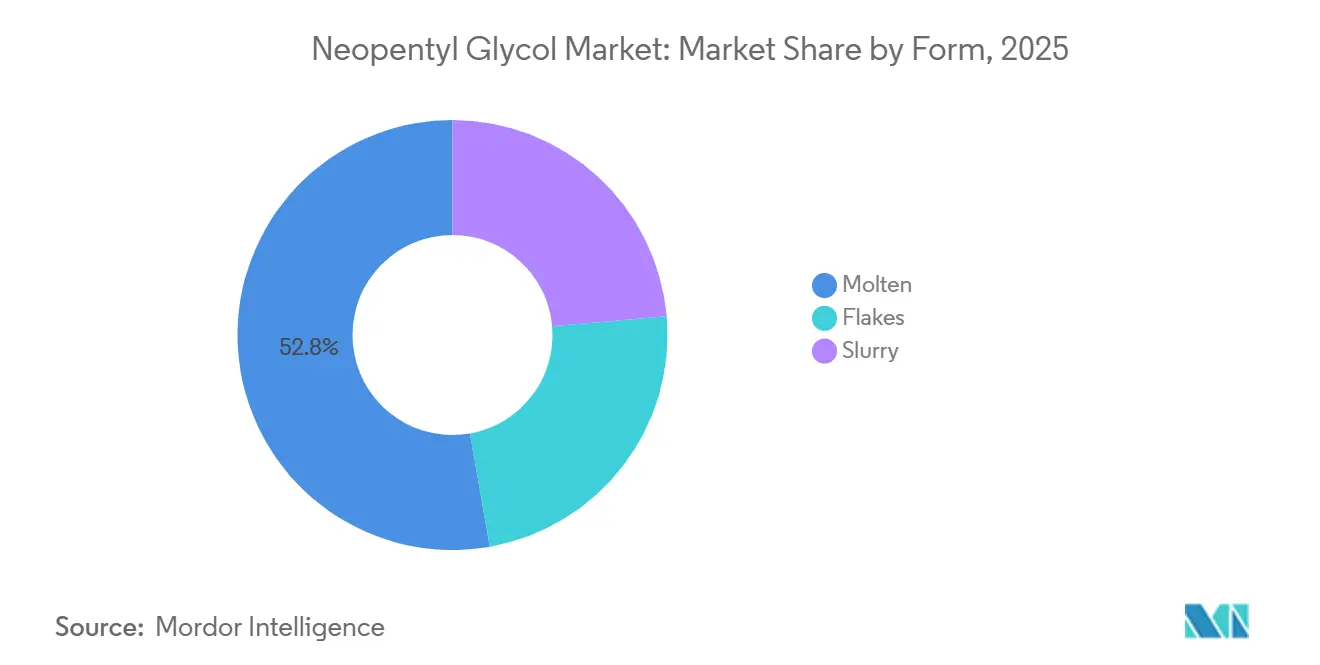

- By form, molten held 52.78% of revenue in 2025, while slurry is projected to expand at a 5.82% CAGR through 2031.

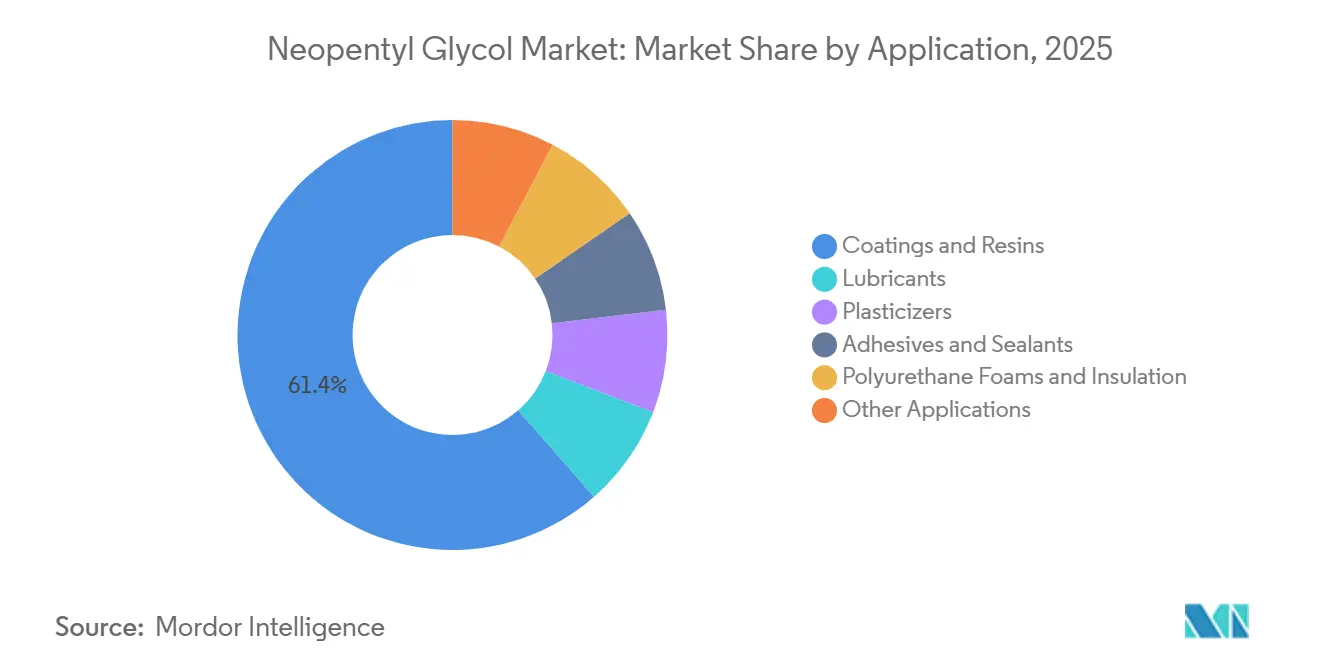

- By application, coatings and resins accounted for 61.44% of revenue in 2025, while polyurethane foams and insulation are forecast to grow at a 6.27% CAGR through 2031.

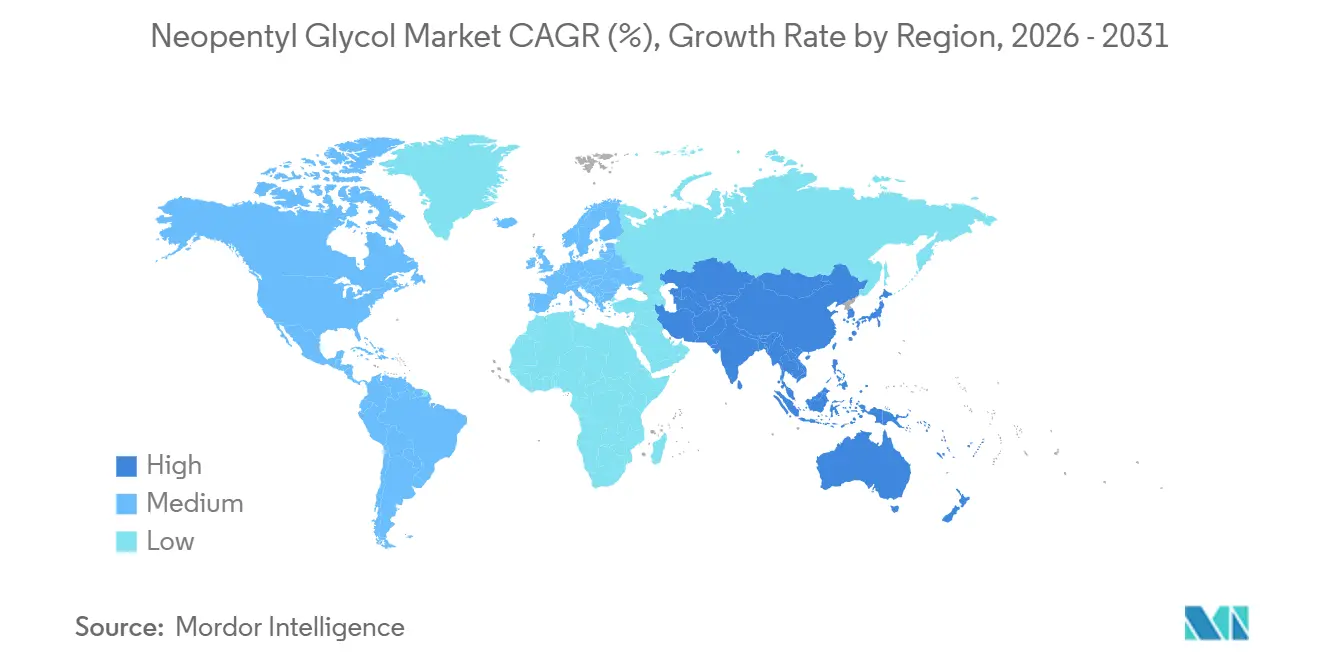

- By geography, Asia-Pacific represented 44.83% of global revenue in 2025 and is also the fastest-growing region with a projected 5.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Neopentyl Glycol Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Demand from Coatings and Resins Manufacturing | +2.5% | Global, strongest in China, India, Germany, and the United States | Long term (≥ 4 years) |

| Automotive Lightweighting and High-Performance Lubricants | +0.9% | Global, early gains in China, South Korea, and Germany | Medium term (2-4 years) |

| Shift Toward Low-Volatile Organic Compound (VOC) and Sustainable Formulations | +0.8% | China, the EU, and North America | Short term (≤ 2 years) |

| Growth in Bio-Based NPG Production | +0.5% | EU and North America, expanding to Asia-Pacific over the medium term | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Demand from Coatings and Resins Manufacturing

The neopentyl glycol (NPG) market continues to draw its largest demand from coatings and resins manufacturing, where NPG remains integral to saturated polyester and alkyd systems used in durable surface finishes. Its chemical structure enables resin formulators to improve weatherability, gloss retention, and hydrolytic resistance, keeping the NPG market closely tied to applications where early coating breakdown is not acceptable. China's tighter coating regulations in 2026 added further pressure on formulators to shift toward low-VOC systems, supporting demand for powder and waterborne resins in the country's large construction and industrial coatings base. BASF stated that powder coating resin systems can reduce VOC emissions by up to 50% compared with liquid coating alternatives, reinforcing the relevance of NPG-based polyester systems in compliance-driven formulations. Producers operating close to coating resin clusters hold an advantage, as reliable supply and process compatibility are as important as price in this segment. This positioning keeps coatings and resins at the center of the NPG market, even as downstream buyers continue to monitor costs and carbon intensity more closely.

Automotive Lightweighting and High-Performance Lubricants

The NPG market is also supported by automotive and industrial lubricant demand, where NPG-derived esters offer thermal stability, low volatility, and strong low-temperature performance. Sinochem noted that NPG-based synthetic ester lubricants are well-suited to high-performance applications such as electric vehicle gearbox oils, battery thermal management fluids, and high-speed motor lubricants[1]Sinochem, “Applications and Performance Characteristics of Neopentyl Glycol in Synthetic Ester-Based Lubricating Oils,” Sinochem, sinocheme.com. This is relevant because the NPG market is benefiting from a shift in lubricant specifications, not just from broader automotive output growth. In coatings, the same vehicle platform transition continues to support durable OEM and refinish systems that require stable resin chemistry and strong surface performance over long operating cycles. The NPG market therefore benefits from two linked automotive needs: lighter and more durable coated parts on one side, and higher-performance synthetic lubricants on the other. This dual exposure gives the NPG market a more balanced demand mix compared with specialty chemicals that depend on a single transportation end use.

Shift Toward Low-VOC and Sustainable Formulations

The NPG market is seeing a direct boost from regulatory moves toward low-VOC coating and resin systems across China, Europe, and North America. BASF announced successive NPG price increases in the United States and Canada in 2025 and 2026, and also raised NPG prices in Europe in March 2026, indicating that buyers continued to accept higher costs in compliance-linked applications. This suggests the NPG market retains pricing support, with resin systems selected for performance and regulatory reliability rather than raw material cost alone. China's mandatory coating standards, which took effect in June 2026, add to this pattern by raising compliance pressure in the world's largest consumer of NPG-linked coating systems. Low-VOC conversion often requires proven chemistry and stable supply, which favors suppliers with strong technical positioning in resins. As a result, the NPG market is becoming more closely aligned with downstream compliance spending and less exposed to short-term discretionary formulation changes.

Growth in Bio-Based Neopentyl Glycol (NPG) Production

The NPG market is developing a premium segment around lower-carbon, bio-based supply, though this remains smaller than the mainstream fossil-based segment. BASF launched Neopentyl Glycol NEOL at its Zhanjiang site in October 2025, with a reduced carbon footprint, using 100% renewable electricity and lower-carbon feedstocks. This indicates that the NPG market is no longer competing solely on cost, as carbon documentation is now part of supplier discussions in Europe and North America. Downstream buyers in coatings and related materials are increasingly screening suppliers for product footprint transparency, particularly where procurement policies track supply-chain emissions. The price premium for lower-carbon grades still limits adoption in cost-sensitive applications, but it creates a defensible tier for architectural coatings, automotive refinish systems, and other specification-driven uses. The NPG market is therefore gradually separating into standard-volume supply and premium documented supply, with the latter category likely to expand over time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock Price Volatility in Isobutyraldehyde and Formaldehyde | -1.1% | Global, most acute in China and North America | Short term (≤ 2 years) |

| Substitution Risk from Alternative Glycols | -0.7% | North America and Europe | Medium term (2-4 years) |

| High Handling and Storage Requirements for Solid-State NPG | -0.4% | Global, especially in emerging markets with weaker logistics systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

The neopentyl glycol market remains exposed to feedstock price swings because NPG production depends on isobutyraldehyde and formaldehyde, both derived from volatile upstream petrochemical chains. ChemNet reported that isobutyraldehyde prices in China rose 17.1% over one week in March 2025, with domestic prices increasing to CNY 7,533 per ton from CNY 6,433 per ton, as supply tightened and downstream demand improved. When feedstock costs move this quickly, producers must either accept lower margins or pass the increase on to customers. This creates risk for buyers in price-sensitive applications, where procurement teams may delay purchases, reduce inventory, or reassess formulation economics. The neopentyl glycol market is more stable in performance-critical coatings and lubricants than in downstream categories where cost swings can alter buying behavior more rapidly. This dynamic does not eliminate demand, but it can slow order timing and weaken profitability during periods of tight feedstock supply.

Substitution Risk from Alternative Glycols

The neopentyl glycol market faces substitution pressure from other specialty glycols, particularly in polyester resin systems, where formulators can adjust blends to balance cost and performance. Eastman's ChemPoint guidance indicates that alternatives such as 1,4-cyclohexanedimethanol and 2,2,4-trimethyl-1,3-pentanediol can offer suitable properties for weatherable, transparent, high-solids, or stain-resistant coatings[2]Eastman/ChemPoint, “Selecting Glycols for Polyester Resin Performance,” ChemPoint, chempoint.com. NPG retains a position in many established resin systems, though higher NPG pricing can encourage incremental reformulation in North America and Europe, particularly when buyers already source several diols from the same supplier network. The substitution risk is most visible at the margin, where a portion of demand can shift without requiring a complete redesign of downstream product families. The neopentyl glycol market faces reduced flexibility when feedstock pressure and substitution options rise simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Molten Dominates on Process Efficiency, Slurry Gains Ground in Sustainable Logistics

Molten accounted for 52.78% of the neopentyl glycol market share in 2025, reflecting its compatibility with continuous resin production lines that consume large daily volumes of NPG. Large plants prefer molten deliveries because the product moves directly into heated systems without the additional re-melting step required for flakes. This process advantage reduces energy loss in high-throughput polycondensation operations and helps stabilize production scheduling for coatings resin manufacturers. Molten form also suits regions where supply networks support heated tanks, pipeline handling, and rapid unloading at integrated chemical sites. These operational benefits explain why the neopentyl glycol market continues to favor molten form in large-scale production centers across Asia and parts of Europe.

Flakes remain relevant in the neopentyl glycol market where batch operations, smaller resin plants, or export logistics favor easier packaging and storage. Smaller buyers in India and Southeast Asia continue to use flakes where heated transport networks are less developed and plant configurations are not built around continuous molten input. However, flakes face gradual pressure as downstream users modernize handling systems and seek lower conversion costs in resin manufacturing. Slurry is the fastest-growing form in the neopentyl glycol market and is expected to expand at a 5.82% CAGR through 2031. It can be transported at ambient temperature, reducing the logistics burden associated with thermal maintenance. This form also appeals to buyers that evaluate delivery formats on the basis of carbon footprint and safety considerations, not only purchase price and purity.

By Application: Coatings and Resins Anchor Demand While PU Foams Outpace the Market

Coatings and resins accounted for 61.44% of the neopentyl glycol market in 2025, reflecting NPG's established role in polyester resin systems for powder coatings, alkyds, and related performance materials. This position is supported by NPG's contribution to applications requiring weather resistance, gloss retention, and long service life under industrial and construction conditions. Powder coatings remain important as they sit at the intersection of VOC regulation, durability requirements, and resin chemistry validated at commercial scale. Lubricants form another significant demand base, with NPG-derived polyol esters used in applications where thermal and oxidative stability narrow the range of suitable chemistries. Plasticizers, adhesives, sealants, and smaller specialty uses add further breadth to the neopentyl glycol market, though they do not match the volume of coating-led consumption.

Polyurethane foams and insulation are the fastest-growing application segment in the neopentyl glycol market, projected to grow at a 6.27% CAGR through 2031. Demand is supported by tighter building performance requirements, which are increasing interest in rigid closed-cell PU systems that rely on stable polyester polyol chemistry. NPG's contribution to thermal stability and process behavior makes it useful in formulations where insulation performance must be maintained over long service periods. This gives the neopentyl glycol market exposure to green construction and retrofit activity beyond coatings and transportation end uses. Over time, this broadens the demand profile of the neopentyl glycol market and reduces reliance on a single downstream segment.

Geography Analysis

Asia-Pacific accounted for 44.83% of global demand in 2025 and is projected to expand at a 5.93% CAGR through 2031, making it the primary regional growth engine of the neopentyl glycol market. The region combines large production clusters with substantial downstream consumption, which tightens logistics and supports strong integration between upstream NPG plants and coating resin users. China remains the dominant force in the neopentyl glycol market, as both the largest producer and consumer of NPG-linked resins and coatings. Tighter Chinese coating standards in 2026 provide additional support for powder and waterborne systems that use NPG-compatible resin chemistry. South Korea, Japan, India, and Southeast Asia also contribute to the neopentyl glycol market through electronics coatings, automotive supply chains, infrastructure materials, and specialty resin demand.

North America represents a high-value segment of the neopentyl glycol market, where buyers often prioritize grade consistency, technical service, and supply reliability over cost alone. Eastman and BASF remain central to the regional supply landscape, and the March 2026 price increase across North and Latin America indicated that market discipline held firm within a specification-driven customer base. The region is also notable for growing interest in lower-carbon grades and documented recycled or circular feedstock pathways, which align with the broader shift toward procurement transparency in coatings and advanced materials. Canada and Mexico contribute to the neopentyl glycol market primarily through cross-border automotive and industrial manufacturing links rather than independent growth patterns.

Europe continues to favor traceable, compliance-oriented supply in the neopentyl glycol market, particularly in Germany, the UK, France, and Italy, where demand from automotive and architectural coatings remains concentrated. BASF's March 2026 price increase of EUR 350 per metric ton (USD 406 per metric ton) indicates that European buyers continue to operate in a market that supports pricing for technically qualified supply. Lower-carbon grades and carbon footprint documentation carry greater weight in Europe than in most other regions, which strengthens the position of premium suppliers in the neopentyl glycol market. South America, the Middle East, and Africa remain smaller markets, but offer longer-cycle opportunities in industrial, architectural, and infrastructure coatings that require durable resin systems.

Competitive Landscape

The neopentyl glycol market is moderately consolidated among major global suppliers, with no single company dominating across all regions. BASF, Eastman, and other established producers shape the competitive landscape through scale, technical positioning, and pricing management across multiple end uses. In October 2025, BASF commissioned a new 80,000-metric-ton-per-year NPG plant at Zhanjiang, increasing its global capacity from 255,000 to 335,000 metric tons per year. This expansion strengthens BASF's presence in Asia while supporting supply reliability for downstream resin customers with regional production needs. BASF also launched NEOL NPG with a reduced product carbon footprint at the same site, indicating that premium differentiation is becoming a more visible part of the neopentyl glycol market.

Eastman participates in the neopentyl glycol market through both NPG supply and adjacent diol options that formulators consider when balancing cost and performance. The company's March 2026 price increase of up to USD 170 per metric ton in North and Latin America reflected a focus on value retention in performance applications that can absorb higher pricing. BASF's 2025 and 2026 price actions in North America reflect the same competitive pattern, where major producers are applying supply discipline rather than pursuing volume at any price. The neopentyl glycol market is therefore moving beyond a simple commodity contest toward a model where service, reliability, product carbon footprint, and application fit increasingly shape competitive outcomes.

Smaller and regional suppliers remain relevant in the neopentyl glycol market, as many customers require dependable local access, tailored grades, and practical support with formulation or handling requirements. Companies with broader specialty polyol or oxo-chemical portfolios can use those adjacent positions to deepen customer relationships even without a leading global NPG scale. Two competitive openings are emerging in the neopentyl glycol market: one around lower-carbon and bio-based supply, where commercially available offerings remain limited relative to future buyer interest, and another in specification-grade supply for high-performance lubricant esters and insulation materials, where quality consistency matters more than price. These factors keep the neopentyl glycol market moderately concentrated at the top, while remaining open enough for specialists to maintain positions in targeted end-use chains.

Neopentyl Glycol Industry Leaders

BASF

MITSUBISHI GAS CHEMICAL COMPANY, INC.

OXEA GmbH

Perstorp

Wanhua

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BASF announced successive price increases for NEOL NPG in the United States and Canada. A USD 0.07/lb increase was announced in February 2026, followed by an additional increase effective April 15, 2026, citing further escalation in logistics and raw material feedstock costs.

- October 2025: BASF inaugurated a new 80,000 metric-ton-per-year NPG plant at its Zhanjiang Verbund site in China, expanding its global NPG capacity from 255,000 to 335,000 metric tons annually. Simultaneously, BASF launched Neopentyl Glycol NEOL with a reduced product carbon footprint at Zhanjiang, produced using 100% renewable electricity and lower-carbon feedstocks. This marked the first commercial-scale low-carbon NPG offering targeting Asia-Pacific powder coating resin customers.

Global Neopentyl Glycol Market Report Scope

Neopentyl glycol (NPG) is a high-purity organic chemical compound valued for its stability. Primarily used as a building block for synthetic resins and polyester formulations, it enhances the resistance of paints, coatings, and plastics to heat, light, and water.

The neopentyl glycol market is segmented by form, application, and geography. By form, the market is segmented into flakes, molten, and slurry. By application, the market is segmented into coatings and resins, lubricants, plasticizers, adhesives and sealants, polyurethane foams and insulation, and other applications. The report also covers market size and forecasts for neopentyl glycol across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Flakes |

| Molten |

| Slurry |

| Coatings and Resins |

| Lubricants |

| Plasticizers |

| Adhesives and Sealants |

| Polyurethane Foams and Insulation |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Flakes | |

| Molten | ||

| Slurry | ||

| By Application | Coatings and Resins | |

| Lubricants | ||

| Plasticizers | ||

| Adhesives and Sealants | ||

| Polyurethane Foams and Insulation | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Neopentyl Glycol Market?

The Neopentyl Glycol Market size is expected to grow from USD 1.76 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.35 billion by 2031 at 5.24% CAGR over 2026-2031.

Which application generates the most demand for neopentyl glycol?

Coatings and resins led demand with a 61.44% revenue share in 2025, reflecting NPG’s strong role in polyester resins used in durable, low-VOC coating systems.

Which region leads to global consumption of neopentyl glycol?

Asia-Pacific led with 44.83% of global demand in 2025 and is also the fastest-growing region, with a projected 5.93% CAGR through 2031.

Why is regulatory pressure helping NPG demand?

Tighter VOC rules are pushing downstream users toward powder and waterborne systems, where NPG-based resin chemistry supports compliance, durability, and stable processing performance.

Page last updated on: