Morocco Sandwich Panels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

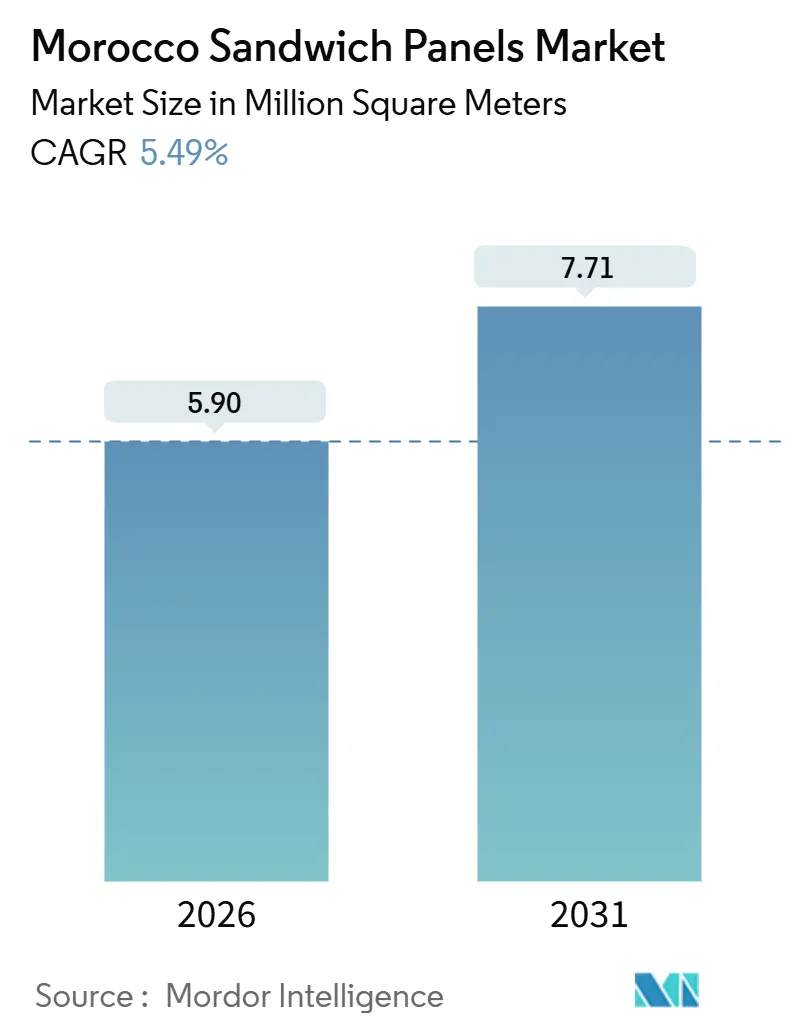

| Market Volume (2026) | 5.90 Million square meters |

| Market Volume (2031) | 7.71 Million square meters |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

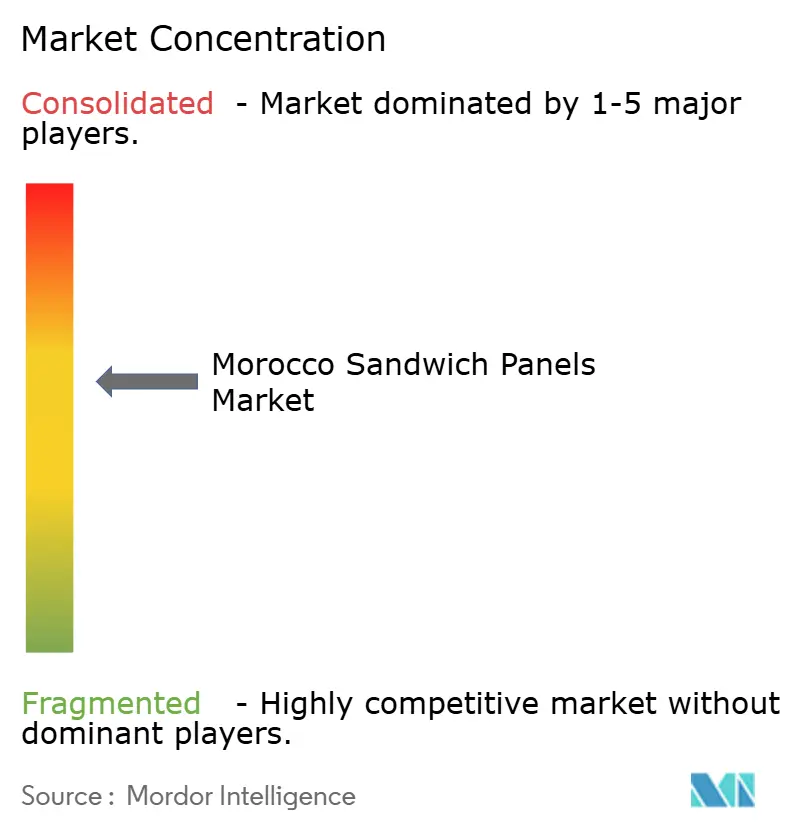

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Sandwich Panels Market Analysis by Mordor Intelligence

The Morocco Sandwich Panels Market size is estimated at 5.90 million square meters in 2026, and is expected to reach 7.71 million square meters by 2031, at a CAGR of 5.49% during the forecast period (2026-2031). This headline trajectory confirms that the Morocco Sandwich Panels market is expanding faster than the wider non-combustible enclosure category as foreign direct investment, tourism, and logistics megaprojects converge on the kingdom. Morocco’s policymakers keep construction activity buoyant through airport, rail, and stadium upgrades, while Stellantis and other automotive suppliers pull a steady pipeline of tier-1 and tier-2 plants that specify insulated wall and roof systems. Cold-chain developers expedite warehouse completions to protect perishable exports that travel to Europe within forty-eight hours by road, which sustains volume for low-temperature panels and fast-fit fastening kits. Demand also flows from retrofit programs that pursue energy-code compliance in hotels, malls, and public buildings, supported by concessional debt under the MorSEFF credit line. Competitive intensity revolves around lead times, integrated envelope packages, and verified environmental product declarations that win LEED or HQE points, with local fabricators narrowing the gap with multinationals in recycled-steel facings and renewable-energy sourcing.

Key Report Takeaways

- By product type, polyurethane captured 37.42% of the Morocco Sandwich Panels market share in 2025, while polyisocyanurate is forecast to expand at a 6.72% CAGR through 2031.

- By end-user segment, industrial facilities held 35.98% of the Morocco Sandwich Panels market size in 2025, whereas logistics facilities registered the highest projected CAGR at 7.50% between 2026 and 2031.

- By application category, wall systems commanded 56.20% of the Morocco Sandwich Panels market size in 2025, and roof systems are growing at a 6.00% CAGR to 2031.

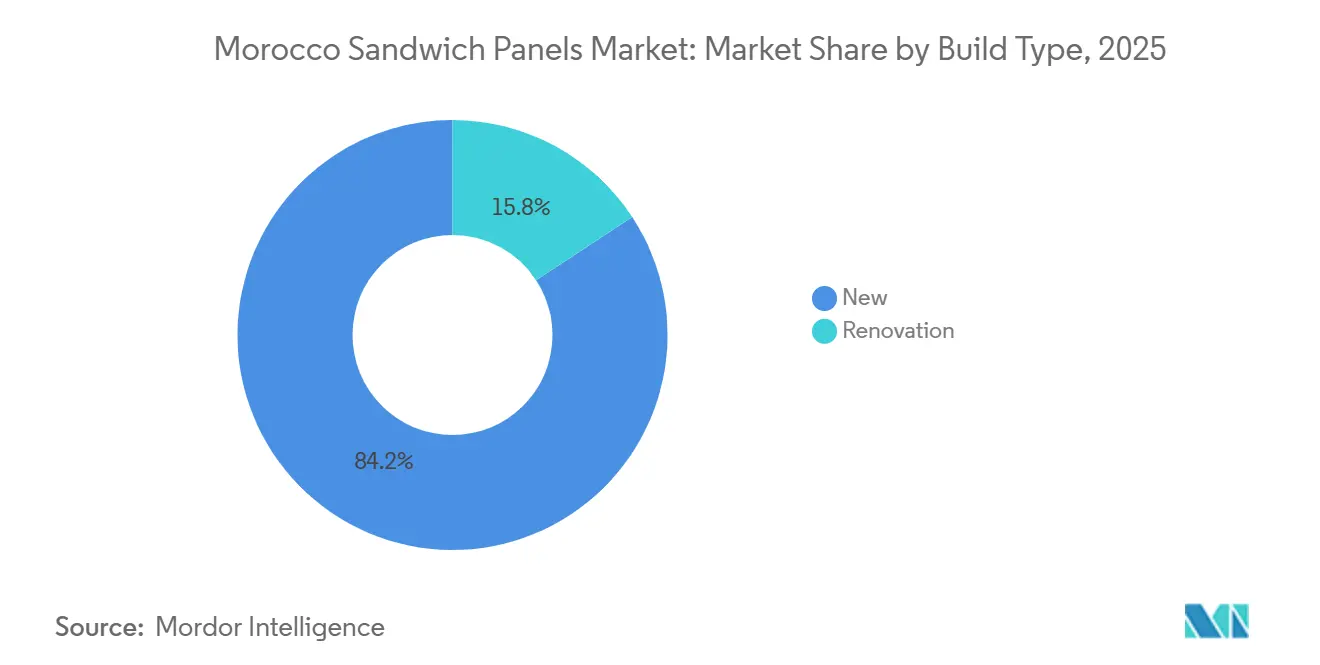

- By build type, new construction accounted for 84.24% volume in 2025 and is advancing at a 5.79% CAGR through 2031.

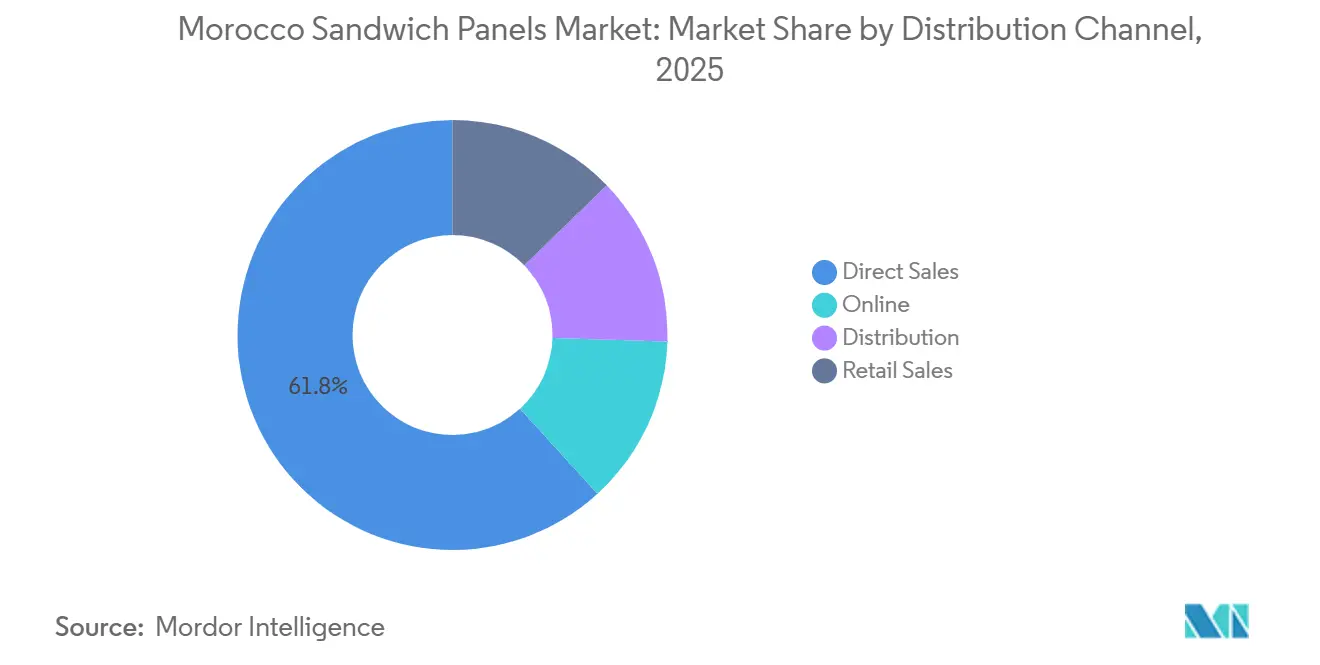

- By distribution channel, direct sales controlled 61.78% volume in 2025; online procurement will rise at a 9.50% CAGR across the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Morocco representing one among them. The global report on sandwich panels market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Morocco Sandwich Panels Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction in tourism and hospitality corridors | +1.2% | Marrakech, Agadir, Tangier, Casablanca | Medium term (2-4 years) |

| Expansion of cold-chain logistics and agro-industrial facilities | +1.5% | Casablanca-Settat, Souss-Massa, Oriental | Short term (≤ 2 years) |

| Government subsidy roll-out for energy-efficient building envelopes | +0.8% | National, pilot cities Rabat-Salé-Kénitra, Fès-Meknès | Long term (≥ 4 years) |

| Africa-Europe automotive supply-chain near-shoring into Morocco | +1.3% | Tanger-Tétouan-Al Hoceïma, Casablanca-Settat | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Construction in Tourism and Hospitality Corridors

In 2024, Morocco welcomed a significant number of tourists. A major airport-capacity program, set to run until 2030, is fueling the development of hotels and resorts in Marrakech, Agadir, Tangier, and Casablanca. New terminals are anchoring mixed-use clusters, necessitating insulated façades that meet international fire ratings. This demand has boosted order volumes for Euroclass B-rated walls. Global brands, like Hilton with its announced properties and Royal Mansour Tamuda Bay, which is set to open in 2024, are turning to sandwich panels to achieve desired thermal and acoustic standards[1]Hilton, “Hilton Announces Nine New Properties in Morocco,” hilton.com. As Morocco prepares for the 2030 FIFA World Cup, efforts span numerous stadium projects, including a flagship venue near Casablanca with a seating capacity exceeding 115,000. This brings heightened demand for press boxes, fan zones, and hospitality suites, with a preference for pre-engineered envelopes to adhere to tight timelines. Panel vendors offering rapid-install roofing profiles are in high demand, as general contractors risk liquidated damages for delays. Additionally, the Ministry of Tourism's push for eco-certification is steering specifications towards products with environmental declarations and low-embodied-carbon credentials.

Expansion of Cold-Chain Logistics and Agro-Industrial Facilities

Morocco is banking on temperature-controlled infrastructure to bolster its export strategy for berries, citrus, and seafood. In 2025, the UNDP and IFRIA unveiled the nation's largest cold-storage facility, strategically located near Casablanca[2]UNDP, “IFRIA Opens Morocco’s Largest Cold Storage,” undp.org. That same year, the U.S. Development Finance Corporation backed an Ifria warehouse in Oulad Teima. Looking ahead, the World Bank, through its agri-food systems program, is set to finance twelve wholesale markets by 2030. Each market will be equipped with insulated chambers tailored for perishables. In December 2025, Logintek inaugurated its integrated zone in Settat, boasting logistics space, all clad in high-density PIR panels. Meanwhile, Tanger Med is pushing boundaries with an expansion of its truck terminal, ramping up capacity to 1 million units annually. This move amplifies the demand for cross-docking warehouses, now a necessity, and fitted with advanced low-temperature wall and roof systems. As exporters hustle to align with stringent EU traceability mandates, they've turned to factory-bonded panels. These panels not only meet hygiene and temperature standards but also facilitate quicker shipments, especially during the bustling tomato and citrus export seasons.

Government Subsidy Roll-Out for Energy-Efficient Building Envelopes

MorSEFF, backed by multiple development banks, provides concessional loans. These loans help cover the added costs of high-performance panels compared to traditional masonry, benefiting both new constructions and retrofits. The GIZ PEEM program aims to enhance energy-management systems and building envelopes in non-residential buildings by 2026. While Morocco’s RTCM thermal regulation sets U-value thresholds for six climate zones, the slow uptake due to voluntary compliance is mitigated by subsidy programs, especially in hotels and malls. Public-sector investors are increasingly pursuing the AMEE Eco-Binyate label, which aligns with ISO 50001, making panel solutions appealing for building envelope upgrades. The PEEB Med initiative, introduced at COP 27, goes beyond flagship commercial projects by offering technical assistance and concessional finance for social housing, schools, and clinics, thereby raising awareness.

Africa-Europe Automotive Supply-Chain Near-Shoring into Morocco

In July 2025, Stellantis pledged a commitment to boost the output of its Kenitra facility to double its current capacity. This move has spurred the construction of tier-1 component plants and logistics yards, featuring insulated panels. Morocco hosts a significant number of automotive suppliers and has a strong export market for vehicles and parts. As the demand for electric vehicles surges, Gotion commenced work on a gigafactory in May 2025, while BTR unveiled plans for a cathode plant in 2024. Both facilities necessitate thermally stable assembly halls and battery rooms. Additionally, ONCF's rolling-stock procurement emphasizes local industrial content, paving the way for pre-engineered buildings in rail manufacturing. Automotive companies are leaning towards single-source envelope packages, which can reduce erection time. This trend favors panel firms that can seamlessly integrate flashing, fixings, and sealants.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic sandwich-panel production capacity | -0.5% | National, with import dependency on Europe and Middle East | Short term (≤ 2 years) |

| Inconsistent enforcement of energy-efficiency codes | -0.3% | National, more pronounced in secondary cities and rural areas | Long term (≥ 4 years) |

| Petro-chemical feedstock price volatility feeding into PIR/PUR costs | -0.5% | National, affecting all polyurethane and polyisocyanurate panel manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Sandwich-Panel Production Capacity

Morocco's reliance on imported polyurethane and PIR foam ingredients makes its panel costs vulnerable to fluctuations in crude oil prices and shipping delays from the Red Sea. Local fabricators, including Maghreb Steel, HIANSA Panel, and SOFAFER, assemble panels using imported cores and steel coils. However, without in-house foam plants, they find it challenging to customize densities for ultra-low-temperature rooms. In recent years, Morocco raised MFN tariffs on construction inputs. While specific taxes on cement and rebar exert indirect pressure on project budgets, sandwich panels have managed to avoid the steepest duties. During peak building seasons, lead times can extend to six weeks. This delay has led some contractors to revert to using single-skin sheeting with on-site insulation, a shift that is projected to dampen demand growth through the forecast period.

Inconsistent Enforcement of Energy-Efficiency Codes

Morocco's RTCM delineates six climate zones with U-value caps, but private developers often escape penalties for non-compliance, especially outside major metropolitan areas. A 2019 study by PEEB revealed a significant knowledge gap, with many builders unaware of code specifics. Further underscoring the issue, a 2023 case study in Ifrane found a staggering majority of residential properties failing to meet thermal standards. While adhering to these standards can inflate upfront costs, this financial hurdle has stymied adoption, particularly in speculative warehouses and budget hotels. Although Law No. 24-09 oversees product safety, it notably omits sandwich panels. Consequently, claims related to fire reaction and thermal properties often rely on self-certification. This lack of stringent inspection diminishes the allure of high-performance panels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PIR Gains on Fire-Safety Mandates

Polyurethane retained 37.42% volume in 2025, but polyisocyanurate (PIR) will outrun overall Morocco Sandwich Panels market growth with a 6.72% CAGR as hotel chains and cold-store operators favor Euroclass B-rated cores. This surge is largely driven by hotel chains and cold-store operators opting for Euroclass B-rated cores. While PIR commands a cost premium over PUR, this gap narrows for projects targeting LEED or HQE certification points. Maghreb Steel's MAGREEN line, launched in May 2025, emphasizes greener standards, utilizing electric-arc furnaces powered by renewable energy sources. Mineral-wool panels lead in specialized fire-wall applications, whereas EPS serves as the budget-friendly choice for light commercial roofing, especially when thermal requirements surpass fire safety standards. Kingspan's QuadCore and PowerPanel technologies are setting a precedent, potentially squeezing margins for standard PUR cores.

Simultaneously, there's a noticeable shift towards thicker panels, driven by tightening cooling-load calculations under RTCM. In Casablanca, cold-store constructions are now opting for 200 mm PIR cores, an increase from the 150 mm standard in 2022, ensuring they can maintain minus-25 °C temperatures even during peak summer. In light of the EU's refrigerant phase-downs, developers are channeling investments into higher-insulation envelopes. This strategy not only curtails compressor runtime but also bolsters the upward trajectory of PIR volume in comparison to PUR.

By End-User Segment: Logistics Overtakes Industrial

Industrial parks consumed 35.98% of volume in 2025, yet the logistics slice of the Morocco Sandwich Panels market is expanding at a 7.50% CAGR to 2031. The logistics share of the Morocco Sandwich Panels market is projected to grow substantially by 2031. The expansion of Tanger Med’s truck terminal and Logintek’s initiatives in the Settat zone are driving demand for fulfillment hubs, cross-docks, and temperature-controlled platforms. While automotive suppliers continue to place orders for wide-span workshops with 12-meter clear heights, logistics developers are leaning towards faster-erect panel envelopes to minimize financing carry costs. Cold-chain investors are opting for PIR panels to meet EU food hygiene standards, and e-commerce players are choosing panel roofs that come pre-wired for photovoltaic modules, helping to mitigate HVAC loads.

Commercial buildings are increasingly using panels for façade renovations. A prime example is Tour Mohammed VI in Rabat, which integrated BIPV cladding, highlighting the aesthetic potential. Despite Morocco's horticulture exports necessitating more controlled environments, agricultural adoption of these panels remains subdued. While residential uptake is limited due to price sensitivity, GIZ-funded demonstration homes in Fès have showcased a reduction in energy bills within just one cooling season, hinting at a significant latent demand.

By Application Category: Roof Systems Gain Retrofit Traction

Wall systems held a 56.20% share in 2025, but roof panels grew faster at a 6.00% CAGR. This surge is largely driven by operators retrofitting 1990s-era sheds, which have been notorious for leaking conditioned air. The market for roof applications in Morocco is poised to expand significantly in the coming years. Kingspan is set to make waves in 2026 with its regional launch of the PowerPanel®, a product that marries 60 mm PIR insulation with a PV laminate. This innovation is particularly enticing for warehouses eager to counteract rising grid-tariff costs. Meanwhile, architects are increasingly favoring façade panels with metallic coatings, known for their resistance to coastal corrosion. These panels are gaining traction in hospitality projects, where branded aesthetics and swift completion are paramount.

When retrofits are combined with rooftop solar installations, they significantly shorten payback durations. Further bolstering this trend, government subsidy programs are stepping in to reimburse a portion of the envelope costs. This financial incentive has spurred a notable increase in roof-panel adoption, especially in the industrial zones of Casablanca and Tangier. Additionally, on-site pull-out tests have validated the load-bearing capacity, instilling confidence in lenders to promptly release construction draws without any hitches.

By Build Type: New Construction Dominates, Renovation Emerges

New builds represented 84.24% of 2025 demand and will keep command through 2031 with a 5.79% CAGR. While new builds dominate, renovation demand is gaining traction, buoyed by PEEM-funded upgrades and heightened energy-price sensitivity in older malls. The share of Morocco's Sandwich Panels market in renovations is set to rise. To minimize downtime, retrofits at airport buildings, public hospitals, and ministry offices are opting for night-shift installations, favoring panel systems that can be easily craned into place in two-meter widths.

As case studies emerge, tenant awareness heightens, notably with HVAC bills in Tanger logistics sheds dropping post-installation of 100 mm roof panels. Recognizing their demountable nature and resale value, financial institutions are increasingly accepting panel envelopes as collateral. This shift not only enhances loan conditions for SMEs pursuing energy upgrades but also underscores the growing financial recognition of these panels.

By Distribution Channel: Online Procurement Surges

Direct sales still rule at 61.78% volume in 2025, reflecting project-specific negotiations. Yet online marketplaces for construction inputs expand at a 9.50% CAGR, bringing the Morocco Sandwich Panels market to digital platforms where buyers compare insulation values and fire ratings in real time. For public projects exceeding MAD 5 million, e-procurement is mandatory, funneling traffic through certified portals. Tools like Holcim’s Batipro allow contractors to configure panel thickness, color, and fastening within web forms, cutting quoting cycles to hours. Smaller renovation crews source stock sizes via online distributors that offer next-day delivery from Casablanca depots. Inventory visibility shortens lead times, although bulk custom orders still require six-week shipping for imported cores.

Geography Analysis

Casablanca-Settat and Tanger-Tétouan-Al Hoceïma lead in volume, clustering automotive assembly, port operations, and cold-chain hubs. Casablanca is home to Stellantis Kenitra, Logintek Settat, and Morocco’s largest cold store, collectively handling a significant portion of the nation's panel orders. Meanwhile, Tanger reaps the benefits of the expanded Tanger Med port, spurring the construction of logistics parks and feeder factories that produce harnesses and seat frames for European OEMs. In Souss-Massa, near Agadir, the U.S. DFC-funded cold store in Oulad Teima, along with fruit-packing sheds, amplifies the region's agro-industrial demand.

Marrakech-Safi and Fès-Meknès capitalize on tourism, unveiling new resorts and conference centers that incorporate PIR façades for enhanced fire safety. The Oriental region is on the rise, thanks to the Nador West Med industrial zones, backed by EBRD funding in 2024, featuring panel-clad warehouses catering to Sub-Saharan trade. High-altitude towns like Ifrane, facing annual heating loads, require thicker panels, while coastal areas opt for coated facings to counter saline air.

With infrastructure investments slated for 2025, including rail extensions, Casablanca solidifies its central role. Yet, these projects also extend southward to Marrakech and Essaouira, enhancing regional freight capabilities. Despite this, the enforcement of RTCM codes lags in remote prefectures, hindering the adoption of premium panels. As World Cup stadiums rise, they spur a surge in panel demand across Rabat, Meknès, and Oujda. However, the legacy use rates will ultimately determine how many facilities maintain high-spec panels in active service beyond 2030.

Competitive Landscape

The Morocco sandwich panels market is moderately consolidated. Competition centers on three levers: lead time, technical certification, and integrated supply packages that include fasteners, flashing, and sealant. Local fabricators respond by installing coil-coating and foam-blowing capabilities to cushion exchange-rate risk and cut turnaround to three weeks. Environmental credentials matter more in public tenders; projects quoting Maghreb Steel’s MAGREEN claim of embodied-carbon savings over imported steel. White-space opportunities lie in residential and controlled-environment agriculture. Price sensitivity curbs uptake in low-cost housing, but demonstration homes in Fès cut cooling bills, widening the total addressable market once subsidy coverage expands. Horticulture investors eye climate-controlled greenhouses to feed European supermarket contracts, offering a new revenue vertical for panel suppliers able to deliver high-humidity, corrosion-resistant systems.

Morocco Sandwich Panels Industry Leaders

Maghreb Steel

Kingspan Group

HIANSA Panel

SOFAFER

Profilacier

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Maghreb Steel published an Environmental Product Declaration for its MAGREEN sandwich-panel line, highlighting PIR, PUR, and rock-wool cores manufactured with 100% recycled steel facings and renewable-energy-powered electric-arc furnaces, positioning the firm to capture green-building specifications.

- January 2025: Maghreb Steel commissioned a next-generation continuous line with 2 million square meters annual capacity, injecting scale that reduces dependence on imported panels and shortens lead times for Moroccan projects.

Morocco Sandwich Panels Market Report Scope

Sandwich panels are pre-engineered, energy-efficient building components consisting of a rigid insulating core—such as PUR, PIR, Mineral Wool, or EPS—encased between two durable outer metal sheets, typically steel or aluminum. They are designed to provide superior thermal insulation, high structural strength, and lightweight, rapid construction for walls, roofs, and cold storage applications.

The market is segmented by product type, end-user segment, application category, build type, and distribution channel. By product type, the market is segmented into Polyurethane (PUR), Polyisocyanurate (PIR), Mineral Wool, and Expanded Polystyrene (EPS). By end-user segment, the market is segmented into Logistics, Industrial, Commercial, Agricultural, and Residential. By application category, the market is segmented into Wall, Roof, and Façade. By build type, the market is segmented into New and Renovation. By distribution channel, the market is segmented into Direct Sales, Online, Distribution, and Retail Sales. For each segment, the market sizing and forecasts have been done on the basis of volume (Square Meters).

| Polyurethane (PUR) |

| Polyisocyanurate (PIR) |

| Mineral Wool |

| Expanded Polystyrene (EPS) |

| Logistics |

| Industrial |

| Commercial |

| Agricultural |

| Residential |

| Wall |

| Roof |

| Façade |

| New |

| Renovation |

| Direct Sales |

| Online |

| Distribution |

| Retail Sales |

| By Product Type | Polyurethane (PUR) |

| Polyisocyanurate (PIR) | |

| Mineral Wool | |

| Expanded Polystyrene (EPS) | |

| By End-user Segment | Logistics |

| Industrial | |

| Commercial | |

| Agricultural | |

| Residential | |

| By Application Category | Wall |

| Roof | |

| Façade | |

| By Build Type | New |

| Renovation | |

| By Distribution Channel | Direct Sales |

| Online | |

| Distribution | |

| Retail Sales |

Key Questions Answered in the Report

What drives the current demand for Moroccan sandwich Panels?

Tourism infrastructure, automotive supplier parks, and cold-chain warehouses are the primary demand engines, pushing the Morocco Sandwich Panels market toward 7.71 million square meters by 2031 from 5.90 million square meters, registering a CAGR of 5.49% in the period.

How fast is logistics construction growing?

Logistics facilities will register a 7.50% CAGR through 2031, overtaking industrial buildings in annual volume.

Why is PIR gaining share over PUR?

PIR offers Euroclass B fire ratings and better thermal efficiency, which satisfy hotel brands and cold-room operators despite its cost premium.

What role do subsidies play in panel retrofits?

MorSEFF concessional loans and the GIZ PEEM program offset extra envelope costs, making high-performance panels financially viable for hotel, mall, and public-building upgrades.

Which regions consume the most panels?

Casablanca-Settat and Tanger-Tétouan-Al Hoceïma together account for the majority of demand thanks to port, automotive, and logistics megaprojects.

What is the current market size of Morocco Sandwich Panels Market?

The Morocco Sandwich Panels Market size is estimated at 5.90 million square meters in 2026, and is expected to reach 7.71 million square meters by 2031, at a CAGR of 5.49% during the forecast period (2026-2031).

Page last updated on: