Morocco Non-Alcoholic Beverages Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

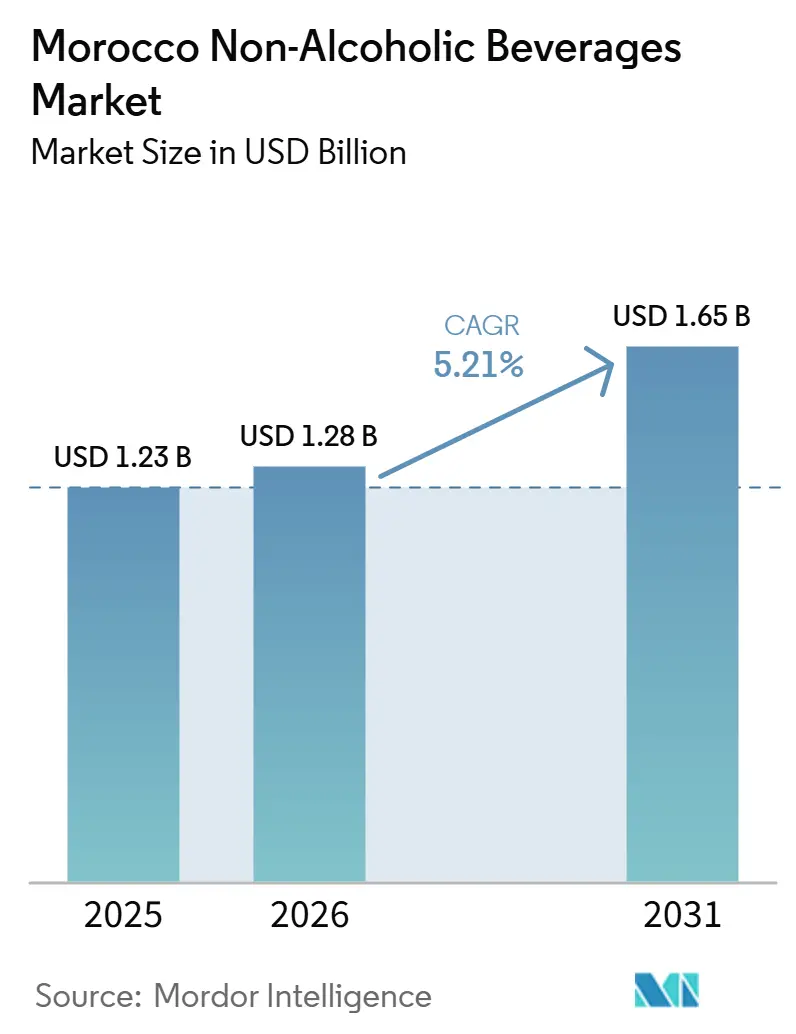

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Non-Alcoholic Beverages Market Analysis by Mordor Intelligence

The Morocco non-alcoholic beverages market size is projected to grow from USD 1.23 billion in 2025 and USD 1.28 billion in 2026 to USD 1.65 billion by 2031, registering a CAGR of 5.2% between 2026 and 2031. Strong tourism demand, rising adoption of packaged beverages in urban areas, and growing hydration needs linked to drought conditions and water stress support the Morocco non-alcoholic beverages market. The market also benefits from a gradual shift away from informal and unbranded drinks, as modern retail formats expand product access and improve the visibility of branded portfolios. Pressure on household spending continues to limit the pace of premiumization among some consumer groups. However, branded consumption continues to strengthen as buyers prioritize safety, consistency, and convenience. A parallel supply-side shift is also shaping the Morocco non-alcoholic beverages market, with producers placing greater emphasis on functional extensions, efficient packaging, and stronger control over sourcing and distribution. As a result, competitive activity is moving beyond price, with local leaders and multinational bottlers investing in capacity, innovation, and route-to-market reach to secure long-term positions in the Morocco non-alcoholic beverages market.

Key Report Takeaways

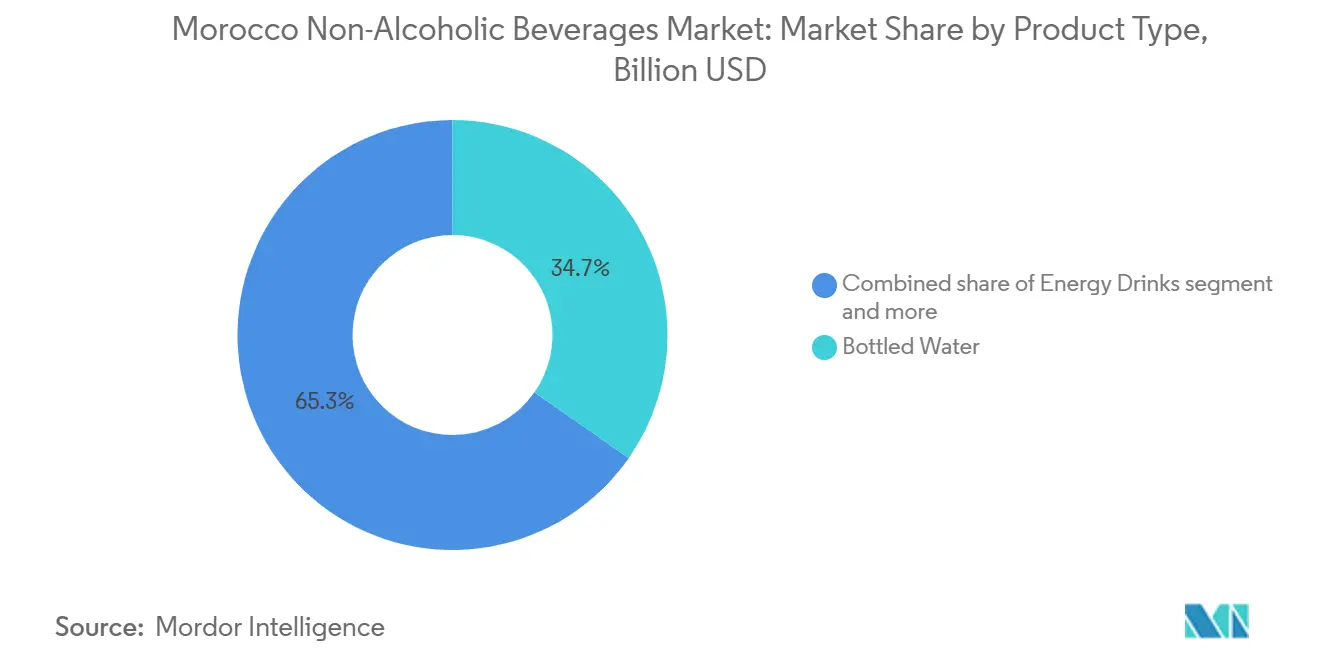

- By product type, bottled water led with 34.71% share in 2025, while energy drinks are forecast to expand at a 6.96% CAGR through 2031.

- By packaging type, PET and glass bottles accounted for 72.62% share in 2025, while Tetra Pak is forecast to grow at a 7.0% CAGR through 2031.

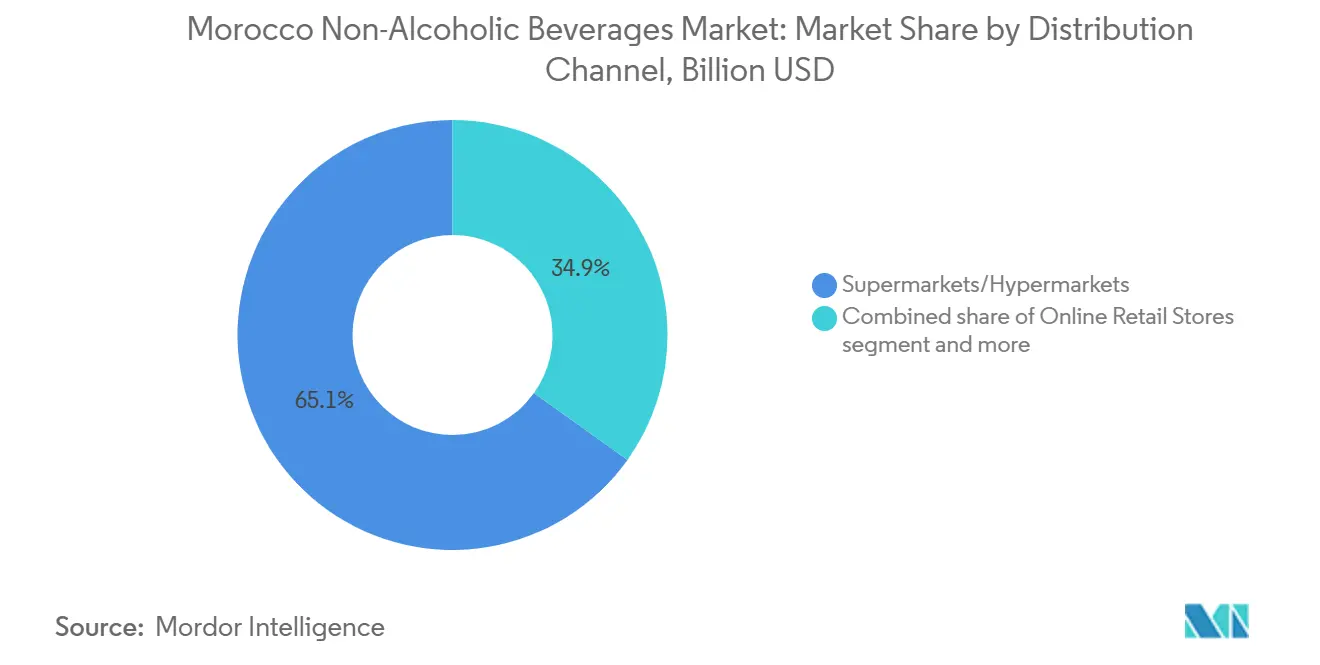

- By distribution channel, supermarkets and hypermarkets held 65.13% of Morocco non-alcoholic beverages market share in 2025, while online retail stores are projected to record the fastest CAGR at 7.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco Non-Alcoholic Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and sugar reduction | +1.1% | Urban Morocco (Casablanca, Rabat, Marrakech, Fez) | Medium term (2-4 years) |

| Tourism, hospitality, and on-the-go consumption | +0.9% | Atlantic coastal corridor, Marrakech, Agadir, Fez, national hotel network | Short term (≤ 2 years) |

| Modern trade and convenience channel expansion | +0.8% | Casablanca, Rabat-Salé-Kénitra, expanding secondary cities | Medium term (2-4 years) |

| Hot-climate hydration demand and safe packaged water preference | +0.7% | National, peaked in the southern, central, and interior regions | Short term (≤ 2 years) |

| Returnable-pack economics in value channels | +0.4% | National; concentrated in high-volume urban distribution zones | Long term (≥ 4 years) |

| Localized sourcing and water stewardship differentiation | +0.4% | Fez-Meknès (Oulmès springs), national supply chain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and sugar reduction

Health awareness is becoming a decisive driver of product innovation across the Morocco non-alcoholic beverages market, rather than remaining a gradual consumer trend. Demand for low-sugar and sugar-free carbonates registered measurable growth in 2025, even as the broader carbonates category remained flat in volume terms. Worldpanel by Numerator's 2025 Brand Footprint report confirmed that Danone's Double Zéro 00% product, a zero-fat, zero-added-sugar dairy drink, reached approximately one-third of Moroccan households within its first year. This performance indicates that consumer demand for functional, cleaner-label formats extends well beyond premium urban niches. This shift is converging with Morocco's subsidy reform agenda, which is gradually exposing artificially low sugar prices to market-rate pressures and encouraging both producers and consumers to move toward reduced-sugar alternatives. As a result, manufacturers are reformulating existing product lines and launching functional extensions faster than the typical 18-24 month innovation cycle. For large incumbents, this capability creates a competitive moat; for smaller players with limited research and development capabilities, it creates a growing barrier.

Tourism, hospitality, and on-the-go consumption

Morocco’s hospitality sector is expected to remain one of the market’s most effective demand-generation engines, with measurable spillover effects across retail channels. According to the Morocco Ministry of Tourism, the country is projected to welcome 18.2 million international tourists in 2025, representing a 14% increase, while tourism revenue in foreign currency is expected to reach MAD 145 billion[1]Source: Morocco Ministry of Tourism and ONMT, “May 2026 Tourism Update,” Morocco Ministry of Tourism, tourisme.gov.ma. This would mark the first year in which tourism revenues surpass non-resident transfers. Momentum is expected to continue into 2026, with arrivals projected to reach 7.7 million through May 2026, up 7% year-on-year, and tourism revenues anticipated to grow 24% in Q1 2026. On-trade channels, including hotels, airport lounges, restaurants, and stadium concessions during AFCON 2025, are expected to expose visiting consumers to both premium international brands and local labels under favorable margin conditions, with some consumers likely converting to repeat off-trade purchasers. SBM’s (Société des Boissons du Maroc) Q4 2025 revenues are projected to reach MAD 930 million (USD 93 million), up 12.6% year-on-year, with company disclosures attributing this growth to tourism inflows and AFCON-driven hospitality consumption[2]Source: Société des Boissons du Maroc, “Q4 2025 Financial Press Release,” Société des Boissons du Maroc, boissons-maroc.com. Structurally, tourism growth is expected to lift both the premium tier and on-trade volumes, creating a two-speed market in which hospitality-oriented and convenience-led formats outperform standard retail metrics.

Modern trade and convenience channel expansion

Organized retail’s rapid expansion is reshaping beverage distribution economics beyond headline store-count growth. Modern retail stores in Morocco are expected to surpass 1,580 points of sale by early 2026, driven primarily by discount formats such as BIM, Supeco, and Kazyon. Together, these retailers are projected to operate more than 1,300 outlets, with BIM approaching 1,000 stores after opening 144 new locations in 2025. LabelVie Group is expected to open 141 new stores in 2025, increase annual revenue by 12.9% to MAD 18.5 billion (USD 1.85 billion), and expand into four new cities, with Q1 2026 retail sales projected to rise 15.6% year-on-year. For beverage brands, the key implication is the concentration of channel power. As discount formats capture a larger share of FMCG sales, branded beverage manufacturers are likely to face stronger shelf-placement negotiation pressure and narrower promotional margins. Brands that invest in discount-channel-specific pack sizes and pricing architectures are expected to gain incrementally in this environment. Meanwhile, modern trade’s geographic expansion into secondary and tertiary cities, including Khénifra, Béni Mellal, and inland corridors, is broadening the addressable market for branded beverages beyond the traditional Casablanca-Rabat-Marrakech triangle.

Hot-climate hydration demand and safe packaged water preference

Morocco's climate profile remains one of the market's most durable demand drivers, and its influence is expected to strengthen rather than stabilize. The UNCCD's 2025 drought assessment is expected to identify Morocco as a global hotspot, where worsening aridity could reduce per-capita freshwater availability to below 500 cubic meters annually by mid-century. In 2025, bottled water is expected to record strong off-trade volume growth, supported by hot weather, drought conditions, and concerns over tap water safety. Affordability pressures are likely to steer lower-income households toward large-format, low-cost purified water packs, while urban and wealthier consumers are expected to favor premium glass-bottled mineral water and flavored variants. This bifurcation is creating two structurally distinct demand profiles within the same category: a high-volume, price-sensitive tier driven by necessity and a premium tier driven by aspiration. LEMO's Vitalya functional water line, which is expected to see strong brand-level growth through Q3 2025, illustrates how the premium tier is monetizing hydration anxiety through added-value positioning rather than price competition. The key insight is that temperature extremes and water anxiety are not cyclical headwinds for the beverage industry; they are permanent structural demand accelerators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and promotion dependence | -0.90% | National; most acute in rural and peri-urban markets | Short term (≤ 2 years) |

| Pet and packaging cost volatility | -0.60% | National; amplified by import-dependent supply chains | Medium term (2-4 years) |

| Water scarcity and source access constraints | -0.70% | National, concentrated in interior and southern basins | Long term (≥ 4 years) |

| Rural distribution inefficiencies and cold-chain gaps | -0.50% | Rural Morocco (Atlas and Souss hinterlands, coastal periphery) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price sensitivity and promotion dependence

Despite rising health awareness, a significant share of beverage consumers in Morocco remains highly price-sensitive, which moderates the pace at which premium and functional formats can scale. Traditional grocery stores, or hanouts, still account for roughly 80% of FMCG distribution, according to some industry estimates, and operate on thin margins that favor promotional pricing and private-label alternatives. Inflationary pressures from 2022 to 2024 compressed household budgets, while the recovery in real spending power through 2025 has remained uneven and concentrated among urban middle-income households. Brands that rely on frequent promotions to sustain volumes in mass channels face a structural challenge: the promotional depth needed to maintain shelf presence in discount outlets erodes the gross margins required to fund the product innovation that health-driven premiumization demands. This restraint does not reflect market maturity alone; it also reflects an income distribution structure in which the aspirational consumer base for functional and premium beverages remains relatively narrow. Producers that address this tension by developing mid-tier functional SKUs at accessible price points, rather than defaulting to full-premium positioning, are likely to achieve faster and more sustainable penetration.

Water scarcity and source access constraints

On the input side, beverage manufacturers in Morocco face two major cost pressures: water sourcing constraints and raw material packaging volatility. Morocco has experienced six consecutive years of drought since 2018, and the World Bank estimates the country’s per capita freshwater resources at approximately 620 cubic meters per year. This level places Morocco under permanent structural water stress and increases operating costs for producers that depend on groundwater extraction. Agricultural water competition further intensifies this pressure, as irrigation demand from export-oriented farming directly competes with beverage production sourcing in basins such as Souss-Massa. At the same time, global PET resin prices, the primary packaging input, are projected to record a 19.7% price range in 2025, with domestic and export benchmarks declining year-on-year but remaining exposed to renewed volatility as upstream petrochemical feedstock prices respond to energy market uncertainty. Producers with vertically integrated PET preform manufacturing or long-term supply contracts have partially protected themselves from spot-market risk. However, smaller regional brands lack this buffer. The combined input-cost exposure from water and packaging disproportionately affects mid-tier producers, limiting their ability to compete on price in discount channels while investing in product development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bottled Water Anchors Share While Energy Formats Drive Growth

Bottled water is expected to hold a 34.71% share of the product type segmentation in 2025, driven by necessity and lifestyle preferences across Morocco's urban and peri-urban population. LEMO is expected to remain the dominant manufacturer, generating approximately MAD 3.3 billion (USD 330 million) in revenue in 2025, an 11.2% year-on-year increase, supported by its spring-water network and functional water lines such as Vitalya Boost[3]Source: Les Eaux Minérales d’Oulmès, “FY2025 Financial Results,” Les Eaux Minérales d’Oulmès, eauxmineralesoulmes.ma. Energy drinks are forecast to grow at a CAGR of 6.96% through 2031, the fastest rate across the product type segmentation, as demand expands into convenience and sports-lifestyle occasions. Red Bull leads the category, while PepsiCo gains ground with value-positioned energy SKUs through modern trade channels. Sports drinks, juices, RTD tea and coffee, and dairy-based and dairy alternative beverages form the long tail of Morocco's diversified non-alcoholic beverage portfolio. Carbonated soft drinks retain a significant base, with Coca-Cola Morocco leading as low-sugar and sugar-free variants outpace regular formats.

The category's key structural shift is the split in bottled water between necessity-driven volume and premiumized functional formats. This split favors incumbents with broad brand portfolios over mono-brand specialists. LEMO's MAD 35 million (USD 3.5 million) allocation to product innovation, including flavored and functional water lines, within its 2025 capital plan signals the direction of category value growth. Dairy alternative drinks remain nascent but are growing, driven by lactose intolerance awareness and plant-based diet adoption among younger urban consumers. These segments are likely to attract investment from global players seeking first-mover advantages. For dairy-based and dairy alternative segments, scale depends on competitive pricing and distribution breadth rather than product novelty alone, given the established household penetration of brands such as Centrale Danone across Morocco's retail network.

By Packaging Type: PET/Glass Dominates as Aseptic Formats Gain Ground

PET/glass bottles are expected to account for 72.62% of the packaging type segmentation in 2025, reflecting Morocco's established beverage production base and consumer familiarity across beverage sub-categories. ECCBC's expanded COBOMI facility in Nouaceur, supported by a MAD 715 million (USD 77.6 million) investment in two new production lines, operates high-speed PET filling lines and ranks among North Africa's most efficient bottling operations. However, PET/glass formats face margin pressure from resin cost volatility, while glass bottles face weight and fragility challenges in last-mile rural logistics. These factors are gradually shifting incremental packaging investment toward alternatives. Cans remain attractive in energy drinks and carbonated beverages due to their portability and suitability for on-trade channels and tourism-driven consumption occasions, with steady uptake expected during the forecast period.

Tetra Pak is the fastest-growing packaging format and is forecast to register a CAGR of 7.01% through 2031, driven by structural factors. In November 2024, Tetra Pak partnered with Moroccan dairy cooperative COPAG to launch a school milk program distributing Tetra Brik Aseptic packages to about 4,000 children across 41 schools in the Maghreb region. This government-backed initiative supports aseptic packaging adoption in institutional distribution channels and creates long-term demand for Tetra Pak infrastructure among dairy and juice producers. Aseptic cartons also eliminate cold-chain dependency for dairy and juice products in inland and rural markets with inconsistent refrigeration, making Tetra Pak more practical for geographic expansion than chilled PET or glass alternatives. The others packaging segment, mainly aluminum foil pouches and bag-in-box formats, remains marginal but is gaining niche traction in out-of-home and food-service contexts.

By Distribution Channel: Supermarkets Lead as Online Retail Resets the Growth Curve

Supermarkets and hypermarkets are expected to account for 65.13% of the distribution channel segmentation in 2025, driven by broad assortments and rapid format expansion. Morocco’s modern food retail is expected to grow by 4.7% in 2024, the fastest rate in MENA, with momentum continuing into 2025 and 2026. LabelVie’s network is projected to reach 411 stores across 37 cities by end-2025, supported by 141 new openings, including three Carrefour hypermarkets in Casablanca. Under Vision 2028, the group targets MAD 28 billion in revenue and about 950 outlets. For beverage brands, these stores remain the highest-volume sales channel but face rising competition from private-label beverages and imported discount brands. Convenience and grocery stores are expected to lose relative share as modern trade expands but remain important for impulse purchases, especially single-serve and chilled formats in high-footfall urban areas.

Online retail stores are forecast to grow at a 7.51% CAGR through 2031, the fastest among distribution channels, despite a small current share of beverage sales. Morocco’s food delivery and grocery e-commerce segment is expected to grow by 40% in 2025, while active online buyers are projected to reach 6.8 million, or 24% of Moroccan adults. Marjane.ma, Jumia, and Glovo are expanding beverage assortments, with multi-pack deals and subscriptions gaining early traction in urban households. Varun Beverages Morocco’s MAD 120 million (USD 12 million) investment in a 31,000 sq. m logistics hub in Lakhyayta, reportedly Morocco’s largest FMCG warehousing contract, reflects the need for dedicated last-mile infrastructure for e-commerce and quick commerce. Experts project e-grocery will account for 5-7% of Morocco’s total food retail by 2030, with beverage categories positioned as early volume contributors.

Geography Analysis

The Morocco non-alcoholic beverages market remains geographically concentrated, with the strongest demand centered along the Atlantic urban corridor and in major tourism cities. Casablanca, Rabat, and Kénitra continue to anchor modern retail traffic, organized distribution, and branded beverage visibility. This core geography gives larger producers a clear advantage, as they can build marketing scale, distribution density, and retail execution more efficiently in concentrated urban zones. ECCBC’s Nouaceur production base reinforces Casablanca’s role as a national supply hub, while LabelVie continued to add stores in key urban areas through 2025 and into 2026. These conditions help explain why branded and premium-ready formats hold a stronger share in these cities than in the country’s interior. Urban concentration also supports faster testing of functional products, new packaging formats, and channel-specific promotions.

Tourism-heavy cities create a distinct demand layer within the Morocco non-alcoholic beverages market. Marrakech and Agadir benefit from visitor spending, which supports premium bottled water, imported energy drinks, and ready-to-drink products across hotels, restaurants, and leisure venues. Morocco recorded 78.6 million hotel overnight stays in 2025, underscoring the scale of hospitality-linked beverage demand. This effect extends beyond direct on-trade sales, as hospitality often serves as a discovery channel for brands that later gain off-trade traction. Société des Boissons du Maroc tied part of its late-2025 revenue expansion to tourism flows in these cities, confirming that travel demand creates a meaningful commercial spillover. As tourism activity remains strong in 2026, the Morocco non-alcoholic beverages market is likely to continue seeing above-average demand from locations closely tied to international arrivals and hotel concentration.

Interior and secondary markets still offer room for wider penetration in the Morocco non-alcoholic beverages market. Fez, Meknès, Béni Mellal, and the Souss-Massa hinterland remain less fully served by branded portfolios than the main coastal corridor. Demand exists, but the commercial model remains more challenging because ambient value-tier products move more easily than chilled, fragile, or premium formats. Last-mile distribution constraints and lower retail formalization continue to limit the conversion of available demand into consistent branded sales. This dynamic leaves the Morocco non-alcoholic beverages market with a clear core-periphery pattern, where national growth will increasingly depend on producers’ ability to serve interior demand with the right mix of pack size, shelf stability, and affordable price points.

Competitive Landscape

The Morocco non-alcoholic beverages market is semi-consolidated, with Les Eaux Minérales d’Oulmès leading in bottled water and ECCBC holding a strong position in carbonated soft drinks and related bottling operations. Large players benefit from extensive distribution, sourcing control, and investment capacity across core and premium products. However, the market is not fully concentrated, as categories such as juices, ready-to-drink tea, coffee, and selected functional beverages remain more open to competition. Centrale Danone remains important in dairy beverages, while Red Bull maintains a premium energy drinks position through strong visibility and broad channel presence. This structure sustains competition across pricing, innovation, channel management, and occasion-based branding.

Les Eaux Minérales d’Oulmès is expected to make a key strategic move in 2025 through MAD 551 million, or USD 55.1 million, in CAPEX and a proposed MAD 350 million, or USD 35 million, bond-to-equity offering for innovation and capacity expansion. ECCBC also strengthened its position through the USD 77.6 million expansion of its Nouaceur plant, which increased national production capacity by 40%. These moves show that scale competitors are defending existing volumes while preparing for more segmented demand across health, convenience, and premium occasions. Société des Boissons du Maroc also notified Morocco’s Competition Council of its acquisition of a 33.3% stake in Africa Retail Market for MAD 50 million, or USD 5 million, giving it joint control over a retail network and stronger route-to-market influence.

Growth opportunities remain strongest where demand is expanding faster than category leadership has solidified. Mid-tier functional beverages, sports drinks, fortified juices, and selected ready-to-drink products still offer room for differentiation. Danone’s partnership with CAF in 2025 is expected to connect brand presence with health, sport, and mass visibility, while Red Bull shows how premium branding can pair with wide availability across hospitality and convenience channels. ONSSA certification and labeling standards are raising barriers for smaller or import-dependent niche brands. Competitive advantage in the Morocco non-alcoholic beverages market increasingly depends on capacity, regulatory readiness, channel control, and careful premiumization rather than headline volume growth alone.

Morocco Non-Alcoholic Beverages Industry Leaders

Les Eaux Minérales d'Oulmès SA

Equatorial Coca-Cola Bottling Company Morocco

Société des Boissons du Maroc SA

Nestlé S.A.

The Coca-Cola Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Société des Boissons du Maroc (SBM) acquired a 33.3% stake in Africa Retail Market (ARM) for MAD 50 million (approximately USD 5 million), securing joint control of a retail chain that operated eight stores under the Hyper U, Super U, and U Express banners. The investment aimed to integrate SBM’s beverage supply directly into organized retail and reduce distribution-chain intermediaries along the Casablanca-Rabat corridor.

- November 2025: Equatorial Coca-Cola Bottling Company (ECCBC) inaugurated two new high-speed production lines at its COBOMI factory in the Technopole Mohammed V industrial zone in Nouaceur, representing an investment of MAD 715 million (USD 77.6 million). The expansion increased national production capacity by 40% and created over 400 direct jobs. It formed part of the company’s broader MAD 3.2 billion (USD 320 million) capital commitment for 2020-2025.

- July 2025: Centrale Danone signed an official partnership with the Confederation of African Football (CAF) to serve as the nutrition partner of the TotalEnergies CAF Africa Cup of Nations Morocco 2025. Under the agreement, the company distributed dairy products to more than 10,000 volunteers, 5,000 journalists, and players at tournament venues across Morocco.

Morocco Non-Alcoholic Beverages Market Report Scope

Non-alcoholic beverages are drinks containing either no alcohol or less than 0.5% Alcohol by Volume (ABV). The Morocco non-alcoholic beverages market is segmented by product type, packaging type, and distribution channel. By product type, the market is segmented into energy drinks, sports drinks, bottled water, juices, carbonated soft drinks, RTD tea and coffee, dairy alternative and dairy-based beverages, and others. By Packaging Type, the market is segmented into PET/glass bottles, cans, Tetra Pak, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail, and others. Market Forecasts in Value (USD).

| Energy Drinks |

| Sports Drinks |

| Juices |

| Bottled Water |

| Carbonated Soft Drinks |

| RTD Tea and Coffee |

| Dairy Alternative Drinks |

| Dairy Based Beverages |

| Other Product Types |

| PET/Glass Bottles |

| Cans |

| Tetra Pak |

| Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Product Type | Energy Drinks |

| Sports Drinks | |

| Juices | |

| Bottled Water | |

| Carbonated Soft Drinks | |

| RTD Tea and Coffee | |

| Dairy Alternative Drinks | |

| Dairy Based Beverages | |

| Other Product Types | |

| Packaging Type | PET/Glass Bottles |

| Cans | |

| Tetra Pak | |

| Others | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2031 outlook for Morocco non-alcoholic beverages demand?

The sector is forecast to reach USD 1.65 billion by 2031 from USD 1.28 billion in 2026, growing at a 5.21% CAGR over 2026-2031.

Which product category leads beverage sales in Morocco?

Bottled water is the largest product type, with 34.71% share in 2025, supported by hydration demand, water safety concerns, and broad household usage.

Which beverage category is growing the fastest in Morocco?

Energy drinks are forecast to expand at a 6.96% CAGR through 2031, driven by urban youth demand and wider convenience-led consumption.

Why is tourism important for beverage companies in Morocco?

Tourism lifts demand across hotels, restaurants, airports, and leisure venues, and Morocco recorded 18.2 million arrivals in 2025 with strong momentum continuing in 2026.

Page last updated on: