Monkeypox Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

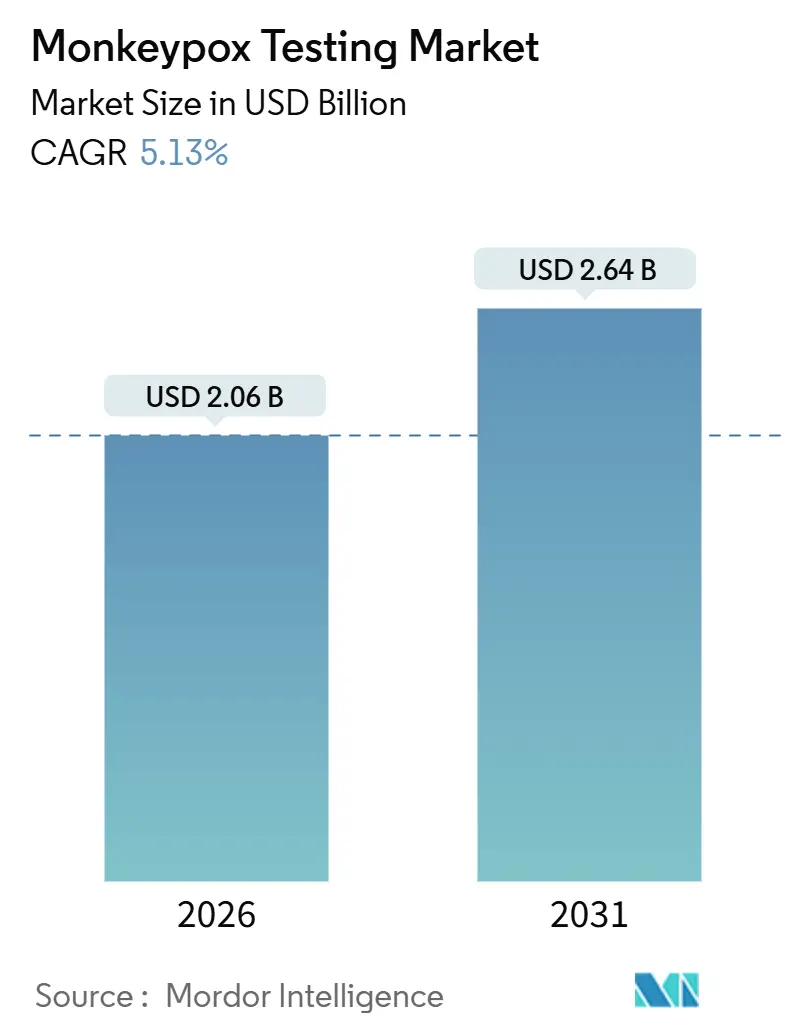

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

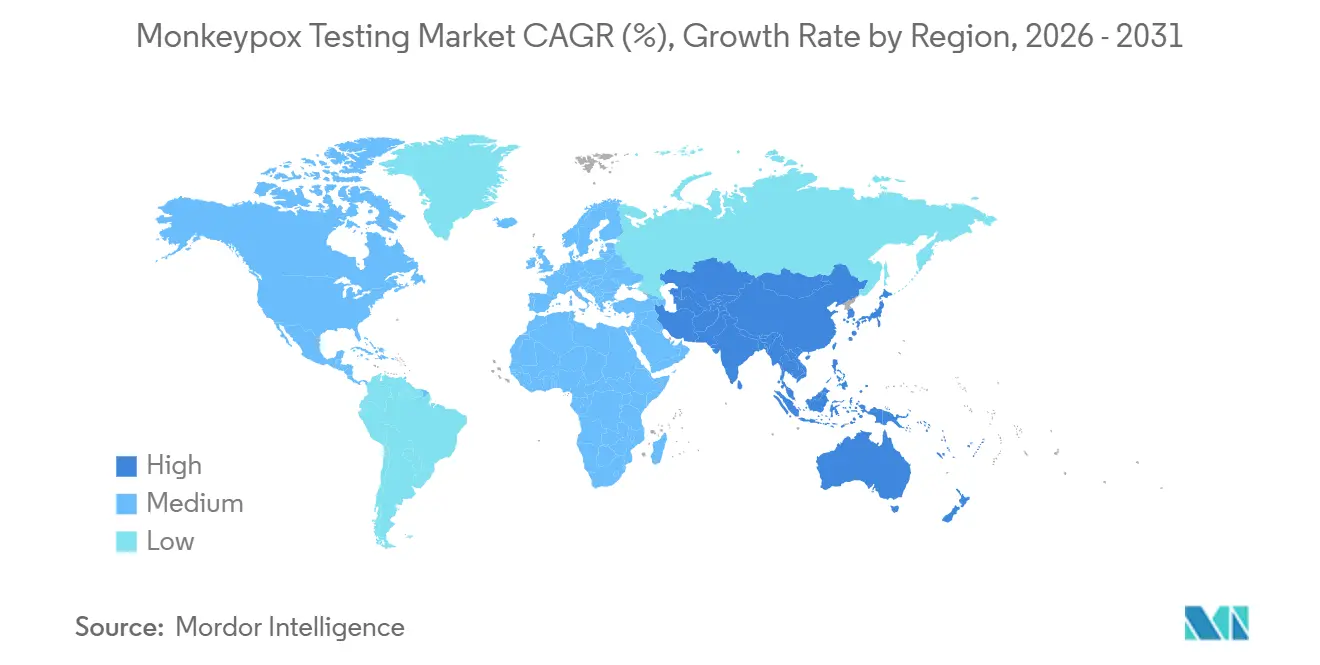

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

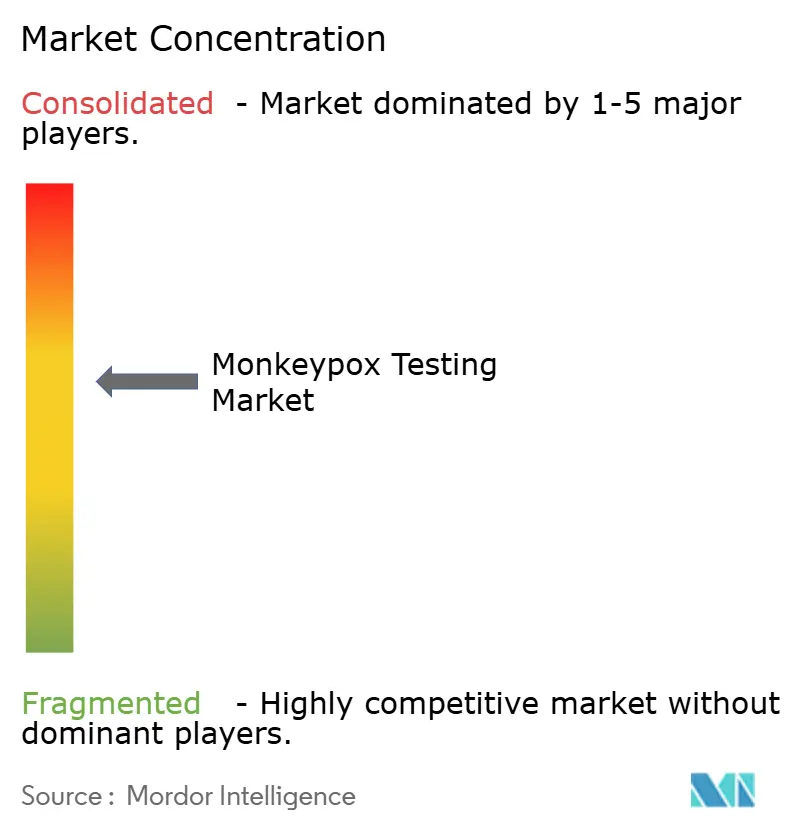

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Monkeypox Testing Market Analysis by Mordor Intelligence

The Monkeypox Testing Market size is estimated at USD 2.06 billion in 2026, and is expected to reach USD 2.64 billion by 2031, at a CAGR of 5.13% during the forecast period (2026-2031).

Resilient demand is shifting from emergency-driven spikes to steadier surveillance buying, while periodic flare-ups still create short-term volume peaks. PCR platforms now anchor country protocols following the World Health Organization’s Emergency Use Listings of Abbott, Roche, and Cepheid assays, yet rapid antigen formats remain sidelined after a CDC field study documented sensitivities below 16%. Vendor strategies increasingly center on multiplex menus that offset fixed costs, digital reporting add-ons that reduce manual data entry, and micro-fluidic cartridges that suit low-resource sites. Geographically, reimbursement frameworks in North America and proactive funding in Asia-Pacific sustain growth, whereas coverage gaps in parts of Africa and Latin America restrain volumes despite donor support.

Key Report Takeaways

- By test type, PCR assays captured 48.55% of monkeypox testing market share in 2025, while lateral-flow–based formats are forecast to advance at an 8.25% CAGR through 2031.

- By end user, hospitals and clinics held 36.53% of the monkeypox testing market size in 2025; diagnostic laboratories are projected to post the fastest 9.55% CAGR to 2031.

- By sample type, lesion swabs accounted for 54.23% share of the monkeypox testing market size in 2025 and oropharyngeal swabs are on track to expand at a 9.85% CAGR to 2031.

- By geography, North America led with 39.55% revenue share in 2025, whereas Asia-Pacific is set to register the highest 10.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Monkeypox Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of PCR-based approvals in private reference labs | +1.2% | Global focus on North America, Europe, APAC metros | Medium term (2-4 years) |

| G-7 funding surge for orthopoxvirus surveillance | +0.9% | North America, Europe, spillovers to Africa and Latin America | Short term (≤2 years) |

| WHO Target Product Profiles for POC kits | +0.8% | Sub-Saharan Africa, South Asia, Pacific islands | Long term (≥4 years) |

| Multiplex race bundling mpox + HSV + VZV | +0.7% | North America, Europe, APAC tertiary centers | Medium term (2-4 years) |

| Digital connectivity APIs for real-time reporting | +0.5% | Early adopters in Scandinavia, Singapore, select African pilots | Medium term (2-4 years) |

| Micro-fluidic cartridges cutting consumable cost | +0.6% | APAC manufacturing hubs, LMIC public-health systems | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of PCR-Based Test Approvals Across Private Reference Labs

Private reference laboratories now process a growing share of monkeypox specimens as streamlined FDA EUAs and WHO listings shrink regulatory hurdles. Quest Diagnostics received nationwide clearance in November 2024, enabling centralized throughput across coastal hubs[1]U.S. Food and Drug Administration, “FDA Authorizes First Home Collection Kit for Monkeypox Testing,” fda.gov. Labcorp scaled from 500 to 25,000 weekly tests after its April 2024 home-collection EUA, leveraging COVID-era logistics. Cepheid’s Xpert Mpox gained WHO listing in October 2024, allowing procurement by UNICEF and the Global Fund. Price dispersion—USD 75 in U.S. insurance versus USD 12 in donor programs—pushes labs to juggle premium and budget kits, complicating inventory planning.

Funding Surges for Orthopoxvirus Surveillance in G-7 Public-Health Budgets

Aggregate allocations of roughly USD 450 million between 2024 and 2026 triple pre-2022 baselines, with the U.S. committing USD 180 million for diagnostics and stockpiles. The Pandemic Fund added USD 129 million for ten African and Asian labs, and the EU earmarked EUR 9.4 million to bolster Africa CDC networks. Multi-year contracts emerging from these budgets encourage manufacturers to open regional distribution hubs and invest in local cold-chain nodes.

WHO Target Product Profiles Accelerating POC Kit Development

Revised 2024 profiles require 60-minute time-to-result, ambient stability, and ≥95% sensitivity at 1 000 copies/mL. Start-ups respond with 15-minute recombinase polymerase amplification lateral-flow formats achieving 95.47% sensitivity. Dragonfly’s 1.2 kg battery unit removes thermocycler needs, fitting outreach clinics. Despite progress, WHO still advises against pure antigen devices after Congo trials showed ≤15.8% sensitivity.

Vendor Race to Multiplex Assays Bundling Mpox + HSV + VZV

QIAGEN’s Viral Vesicle panel runs on GeneXpert, detecting four viruses in 90 minutes and letting emergency rooms rule out alternatives without batching. A 2024 study showed multiplex serology improved diagnostic accuracy by 18 percentage points relative to sequential testing. Roche leverages its cobas 6800/8800 installed base to add mpox with minimal new capital, illustrating the reagent-lock model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-outbreak demand volatility | -0.8% | Global, acute in Sub-Saharan Africa, Latin America | Short term (≤2 years) |

| High primer validation costs under FDA EUA | -0.5% | North America, spilling into export markets | Medium term (2-4 years) |

| Cross-reactivity lowering LFA uptake | -0.4% | Populations with recent smallpox vaccination | Medium term (2-4 years) |

| Cold-chain dependence in tropical LMICs | -0.6% | Sub-Saharan Africa, South Asia, Pacific islands, Amazon basin | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Post-Outbreak Demand Volatility Hurting Capacity-Planning ROI

The Democratic Republic of Congo tested only 37% of suspected cases in 2024 versus an 80% target, showing how stockpiled reagents can idle once incidence falls[2]Africa Centres for Disease Control and Prevention, “Unified Mpox Surveillance Protocol,” africacdc.org. Labcorp’s utilization dropped below 10% three months after its April 2024 EUA despite 25 000-test capacity. Laboratories therefore prefer multiplex PCR or HSV bundles that backfill volume when mpox ebbs.

High Validation Costs for Clade-Specific Primers Under Evolving FDA EUA

A 2024 medRxiv preprint linked primer mismatches to missed positives in California and South Kivu isolates, prompting redesign expenses exceeding USD 500 000 per EUA filing[3]medRxiv, “Diagnostic Failures Due to Genomic Deletions in Monkeypox Virus,” medrxiv.org. Smaller firms lacking bioinformatics teams face barriers, reinforcing scale advantages for Abbott and Roche.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Precision Anchors Market, Isothermal Platforms Gain Share

PCR assays held 48.55% of monkeypox testing market share in 2025 on the strength of eight FDA-cleared platforms and WHO listings that guarantee global procurement. Lateral-flow categories, boosted by emerging isothermal hybrids, are forecast for an 8.25% CAGR to 2031, the fastest among modalities. The recombinase polymerase amplification lateral-flow device serves as a bridge, reaching PCR-level sensitivity in 15 minutes. Serology remains niche due to vaccinia cross-reactivity, while CRISPR prototypes promise single-nucleotide differentiation but remain pre-commercial.

Growing adoption of multiplex viral rash panels further entrenches molecular platforms. Vendors with large analyzer fleets benefit from reagent lock-in, whereas open-platform entrants court volume by undercutting cartridge prices. As WHO Target Product Profiles emphasize 60-minute turnaround and ambient stability, isothermal formats should capture incremental share from centralized PCR without displacing it entirely, supporting steady expansion of the monkeypox testing market.

By End User: Diagnostic Laboratories Scale Fastest, Hospitals Retain Volume Share

Hospitals and clinics generated 36.53% of 2025 revenue, propelled by immediate patient access and bundled reimbursement. Diagnostic laboratories are on pace for a 9.55% CAGR through 2031, reflecting surge contracts during outbreaks and their use of broad test menus to preserve utilization. Public-health labs contribute vital genomic surveillance yet face budget ceilings, while research institutions remain small buyers focused on assay validation.

Home and community point-of-care testing will advance as Dragonfly-type devices win approvals, but centralized labs retain advantages during high-volume waves. Digital connectivity APIs that auto-report results into national databases strengthen the value proposition of reference labs that can integrate seamlessly, reinforcing their role within the monkeypox testing industry.

By Sample Type: Lesion Swabs Dominate, Respiratory Specimens Gain Traction

Lesion swabs delivered 54.23% of volume in 2025 due to viral loads 256-fold higher than respiratory sites, yielding earlier detection. Collection protocols mandate synthetic swabs to avoid inhibitors, with dual sampling from multiple lesions for redundancy. Oropharyngeal swabs should post a 9.85% CAGR, driven by asymptomatic contact tracing in Southeast Asia.

Scab material, although stable at room temperature for 30 days, suffers lower sensitivity late in the disease course. Blood and serum support seroprevalence studies but offer limited diagnostic utility. Vendors optimizing sample kits that pair lesion and throat swabs and include nucleic-acid stabilizers can improve result reliability, supporting the broader monkeypox testing market.

Geography Analysis

North America led revenue with a 39.55% stake in 2025 as FDA EUAs accelerated eight molecular launches and insurers reimbursed USD 75–150 per test. The United States sequenced 11% of confirmed cases, integrating diagnostics with genomic surveillance. Canada follows similar patterns, while Mexico blends public reference capacity with private outsourcing.

Asia-Pacific will expand at a 10.51% CAGR, the quickest globally, propelled by India’s Priority 2 designation for mpox and growing sequencing networks across ASEAN. Median genomic turnaround still sits at 18 days, signaling infrastructure gaps yet to be bridged. The region benefits from domestic cartridge production that lowers landed costs and from donor funds that smooth procurement cycles.

European demand stabilizes as outbreaks wane, though Spain’s cumulative 7,520 cases sustain baseline testing. EU4Health financing directs surplus capacity toward Africa CDC labs, diffusing European kit volumes into Sub-Saharan Africa. The Middle East showcases contrasting readiness: Saudi Arabia mandates 24-hour digital reporting while infrastructure-constrained neighbors depend on donor kits. Latin America’s need remains high after Brazil recorded 11,000 plus infections, but inconsistent reimbursement slows uptake. These contrasts shape a patchwork of opportunity for players in the monkeypox testing market.

Competitive Landscape

Abbott, Roche, and Cepheid collectively secured the only three WHO Emergency Use Listings as of late 2024, establishing a moderate powerhouse tier. Yet regional challengers like Morocco’s Moldiag and open-platform developments from academic centers fragment the field, keeping competitive intensity high. Multiplex panels from QIAGEN amplify differentiation by adding HSV and VZV in single cartridges, while micro-fluidic start-ups chase low-resource niches.

CRISPR-based assays under development promise clade-level discrimination without sequencing, responding to public-health calls after documented primer failures. Installed analyzer fleets create high switching costs, and reagent lock-in underpins recurring revenue. At the same time, the FDA–CDC surge testing memorandum enables reference labs to absorb overflow, further centralizing U.S. capacity. Collectively, these forces sustain innovation, price competition, and regional specialization across the monkeypox testing industry.

Monkeypox Testing Industry Leaders

Thermo Fisher Scientific

Roche Diagnostics

Quest Diagnostics

Labcorp

Sonic Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Global Health Innovative Technology Fund invested JPY 70 million (USD 460 000) to advance a prototype mpox detection assay.

- May 2025: South African Health Products Regulatory Authority listed the first mpox in-vitro diagnostic via WHO reliance pathway.

Global Monkeypox Testing Market Report Scope

As per the scope of the report, monkeypox testing refers to the procedures and methods used to detect and confirm the presence of the monkeypox virus in individuals. It typically involves laboratory tests such as PCR (polymerase chain reaction) to identify viral DNA from samples collected from skin lesions, blood, or other bodily fluids.

The segmentation for the monkeypox testing market is categorized by test type, end user, sample type, and geography. By test type, it includes PCR, lateral flow assay/rapid antigen, serology/antibody ELISA, and other test types. By end user, it covers hospitals and clinics, diagnostic laboratories, public-health/reference labs, research and academic institutes, and home and community POC settings. By sample type, it comprises lesion swab/exudate, scab/crust, blood/serum, and oropharyngeal/nasopharyngeal swab. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| PCR |

| Lateral Flow Assay / Rapid Antigen |

| Serology / Antibody ELISA |

| Other Test Types |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Public-Health / Reference Labs |

| Research & Academic Institutes |

| Home & Community POC Settings |

| Lesion Swab / Exudate |

| Scab / Crust |

| Blood / Serum |

| Oropharyngeal / Nasopharyngeal Swab |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | PCR | |

| Lateral Flow Assay / Rapid Antigen | ||

| Serology / Antibody ELISA | ||

| Other Test Types | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Public-Health / Reference Labs | ||

| Research & Academic Institutes | ||

| Home & Community POC Settings | ||

| By Sample Type | Lesion Swab / Exudate | |

| Scab / Crust | ||

| Blood / Serum | ||

| Oropharyngeal / Nasopharyngeal Swab | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the monkeypox testing market in 2031?

The market is forecast to reach USD 2.64 billion by 2031.

Which region shows the fastest growth in monkeypox diagnostics to 2031?

Asia-Pacific is projected to post the highest 10.51% CAGR through 2031.

Which test category commands the largest share today?

PCR assays hold the lead with 48.55% revenue share in 2025.

Why are isothermal-lateral flow hybrids gaining traction?

They deliver PCR-level sensitivity in about 15 minutes without the need for thermocyclers, suiting decentralized sites.

How does demand volatility affect laboratories?

Outbreak-driven spikes often leave labs with idle capacity once case counts drop, undermining return on recent expansions.

What impedes kit uptake in tropical LMICs?

Cold-chain requirements for many PCR reagents raise costs and risk spoilage where refrigerated transport is limited.

Page last updated on: