Military Aircraft MRO Market Size

Market Overview

| Study Period | 2019 - 2030 |

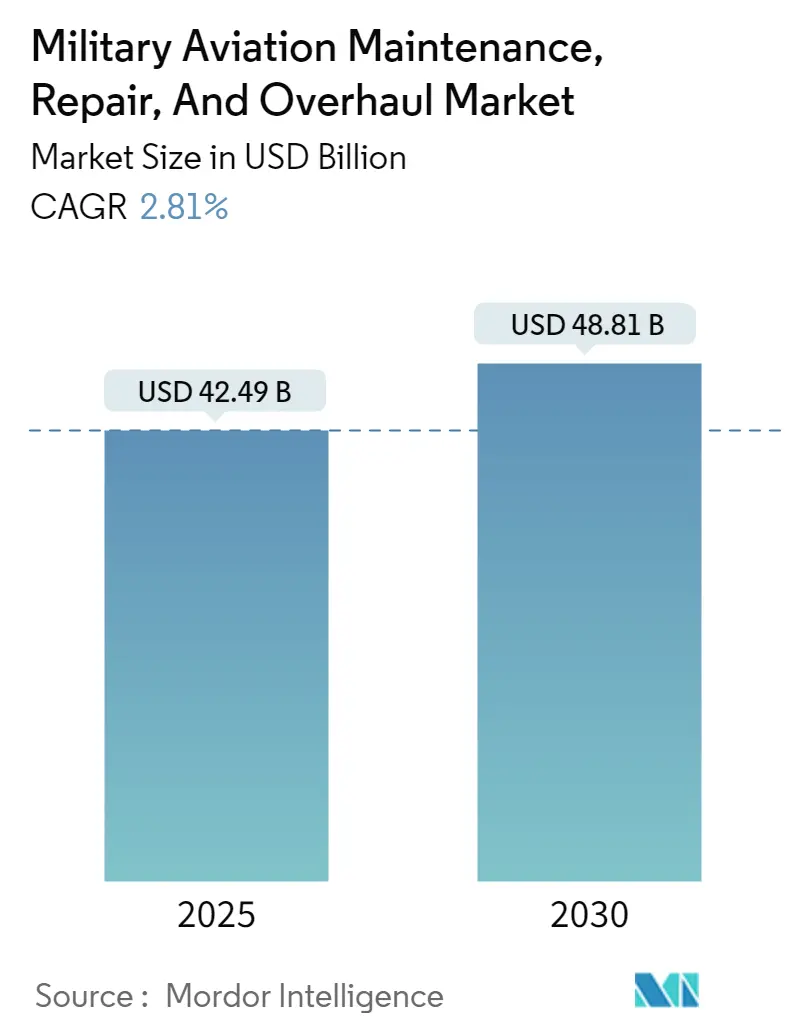

| Market Size (2025) | USD 42.49 Billion |

| Market Size (2030) | USD 48.81 Billion |

| Growth Rate (2025 - 2030) | 2.81% CAGR |

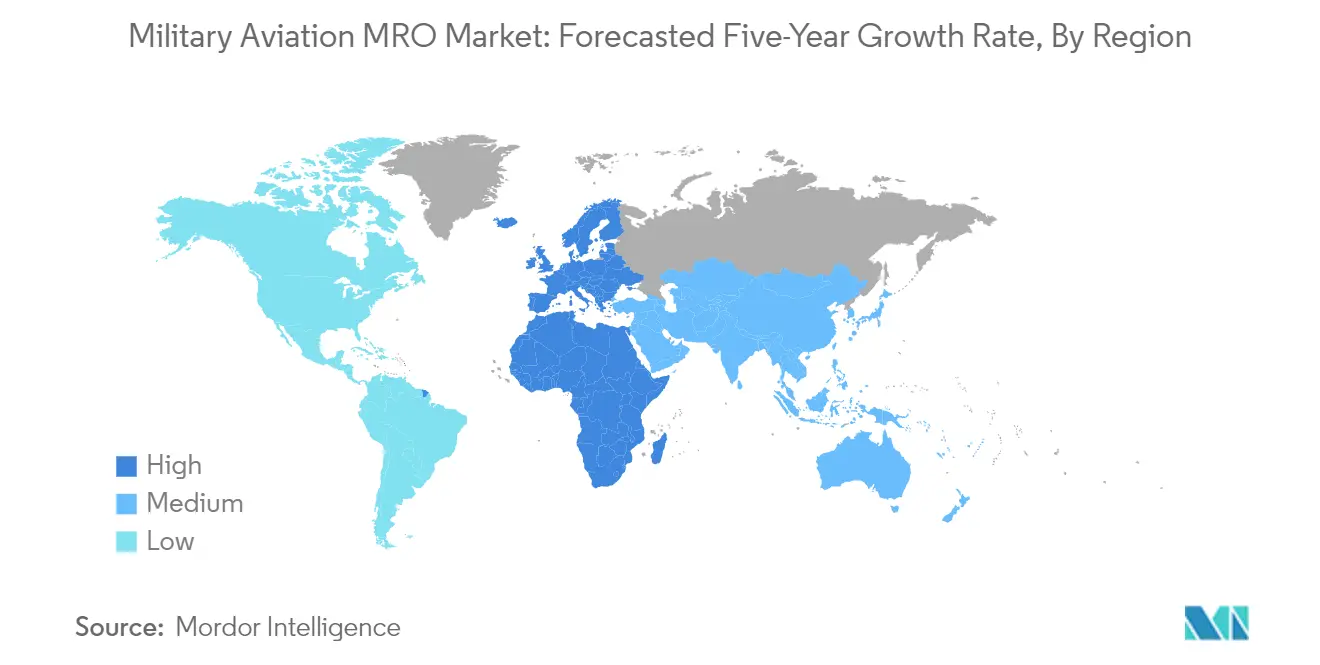

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Military Aircraft MRO Market Analysis

The Military Aviation Maintenance, Repair, And Overhaul Market size is estimated at USD 42.49 billion in 2025, and is expected to reach USD 48.81 billion by 2030, at a CAGR of 2.81% during the forecast period (2025-2030).

The military aviation MRO market landscape is experiencing significant transformation amid escalating global defense expenditures, with the United States and China leading military spending at USD 877 billion and USD 292 billion respectively in 2022. This substantial investment reflects the growing emphasis on maintaining operational readiness and modernizing existing military aircraft fleets. The aerospace and defense MRO market operates under increasingly stringent regulations enforced by various national and international bodies, including the ICAO, which sets global standards for flight safety. These comprehensive regulations encompass everything from component manufacturing to maintenance procedures, ensuring the highest levels of operational safety while simultaneously creating complex compliance requirements for MRO service providers.

The evolution of military aircraft fleet composition has created diverse maintenance requirements across different aircraft categories. As of 2023, the global military aircraft fleet comprises 45.9% combat aircraft, 6.2% special mission aircraft, 2.6% tanker aircraft, 13.4% transport aircraft, and 31.8% training aircraft, each requiring specialized maintenance protocols and expertise. This diversity in fleet composition has led to the development of specialized military MRO capabilities and the establishment of dedicated maintenance facilities equipped with advanced diagnostic tools and skilled technicians capable of handling various aircraft types.

The integration of stealth technology in military aircraft has introduced new complexities in maintenance requirements, with the United States leading the stealth aircraft fleet with 636 units, followed by China with 150 units as of 2023. These advanced aircraft require specialized maintenance procedures, particularly for their radar-absorbent materials and sophisticated electronic systems. The maintenance intensity is exemplified by the F-35 fighter jets, which require between 41.75 to 50.1 man-hours of maintenance per flight hour, highlighting the resource-intensive nature of maintaining advanced military aircraft MRO.

The industry is witnessing a significant shift toward digital transformation and predictive maintenance technologies. MRO providers are increasingly adopting artificial intelligence, machine learning, and Internet of Things (IoT) solutions to enhance maintenance efficiency and reduce aircraft downtime. This technological evolution is particularly evident in recent developments, such as the Chinese People's Liberation Army Air Force's introduction of mixed reality technology for aircraft maintenance in December 2023, enabling maintenance crews to gain comprehensive insights into aircraft capabilities without hands-on interaction with actual equipment. These advancements are revolutionizing traditional military aircraft maintenance approaches, improving efficiency, and enabling more proactive maintenance strategies.

Military Aircraft MRO Market Trends

Increasing Demand for Technologically Advanced Fighter Aircraft

The global military aviation sector has witnessed a significant surge in the procurement of technologically advanced fighter aircraft, particularly stealth aircraft, driving the demand for specialized military aircraft maintenance, repair, and overhaul services. As of 2023, the United States leads with 636 stealth aircraft, followed by China with 150 units, while countries like Australia, Norway, and Israel maintain fleets of 44, 34, and 33 stealth aircraft, respectively. These advanced aircraft require meticulous maintenance protocols, with the F-35 fighters necessitating between 41.75 and 50.1 man-hours of maintenance per flight hour, according to the Naval Air Systems Command. The maintenance demands increase substantially during combat operations, evasive maneuvers, and sustained high-speed flights, requiring dedicated maintenance crews trained specifically by manufacturers.

Recent developments highlight the growing focus on advanced fighter aircraft acquisition and maintenance. In March 2024, India's Defence Research & Development Organization (DRDO) received approval for the design and development of the Advanced Medium Combat Aircraft (AMCA), a fifth-generation stealth fighter jet, with an allocated budget of USD 1.81 billion. Similarly, in July 2023, Israel approved a USD 3 billion deal to purchase 25 F-35 stealth fighter jets, which included agreements with Lockheed Martin and Pratt & Whitney for local defense companies' involvement in aircraft component production. The maintenance of stealth aircraft presents unique challenges, particularly in maintaining the stealth coating that must be re-applied after each flight, requiring specialized military MRO services and infrastructure.

Aircraft Upgradation and Service Extension Programs

The military aviation sector is experiencing a significant push toward aircraft upgradation and life extension programs, driven by the need to maintain the operational relevance of existing fleets while managing budget constraints. A prime example is the US Air Force's initiative to extend the service life of approximately 608 Block 40 and Block 50 F-16 aircraft through the Post-Block Integration Team (PoBIT) project until 2048. This comprehensive program encompasses 22 modifications to enhance lethality and operational effectiveness, including major structural upgrades to extend flight hours from 8,000 to 12,000. Similarly, Turkey, which operates the third-largest F-16 fleet globally, has initiated a service-life extension program for its fleet that has been in service for nearly three decades, with work being performed by Turkish Aerospace.

Recent developments in 2024 underscore the growing emphasis on fleet modernization and upgradation programs. In February 2024, Boeing Defense Australia secured a contract worth AUD 600 million to upgrade the F/A-18F Super Hornet and EA-18G Growler fleet for the Royal Australian Air Force. Additionally, in March 2024, the Indian defense ministry approved a significant upgrade program worth approximately USD 7.2 billion for Hindustan Aeronautics Limited to enhance the Su-30MKI fighter jet fleet's capabilities, including the integration of new mission control systems, radars, electronic warfare capabilities, and weapon systems. These programs demonstrate the increasing focus on extending the operational life of existing aircraft while incorporating modern technologies and capabilities, contributing to the broader military aviation MRO market.

Segment Analysis: By Aircraft Type

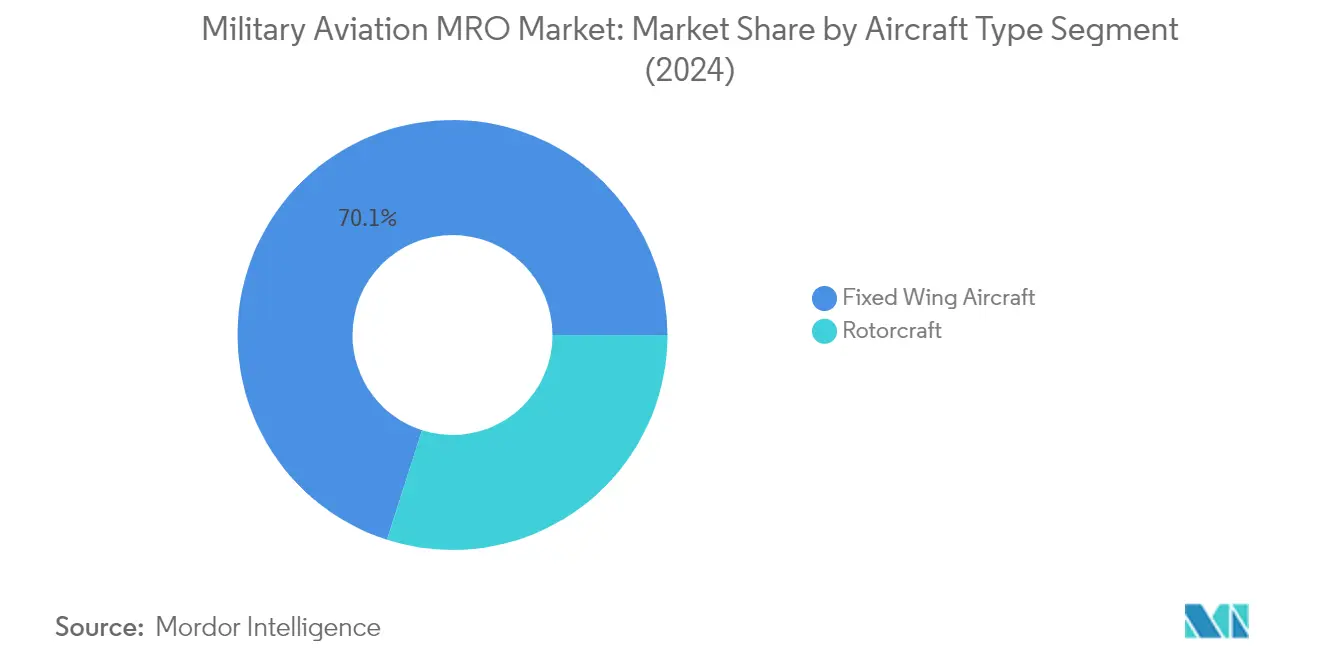

Fixed-Wing Aircraft Segment in Military Aviation MRO Market

The fixed-wing aircraft segment dominates the military aviation MRO market, commanding approximately 70% of the market share in 2024. This substantial market position is attributed to the growing procurement of fighter jets and rising expenditure on military aircraft modernization programs worldwide. The segment's prominence is further reinforced by the extensive maintenance requirements of various platforms, including fighter jets, bombers, transport planes, and surveillance aircraft. Fixed-wing military aircraft play crucial roles in modern warfare, providing essential capabilities such as air superiority, reconnaissance, surveillance, intelligence gathering, and close air support. The segment is also experiencing the fastest growth in the market, driven by increasing investments in next-generation fighter aircraft, the need for regular maintenance of aging fleets, and the integration of advanced technologies in existing platforms. The growth is particularly notable in regions with large military aircraft fleets, such as North America and Europe, where significant portions of defense budgets are allocated to aircraft maintenance and modernization initiatives.

Rotorcraft Segment in Military Aviation MRO Market

The rotorcraft segment represents a vital component of the military helicopter MRO market, encompassing maintenance services for military helicopters and tilt-rotor aircraft. These platforms serve diverse missions ranging from combat and reconnaissance to troop transport and search and rescue operations. The segment's maintenance requirements are influenced by the unique operational demands placed on rotorcraft, including extreme environmental conditions, high-altitude operations, and corrosive environments. Military helicopters like the AH-64 Apache and UH-60 Black Hawk require comprehensive servicing of rotor blades, engines, avionics systems, and dynamic components to maintain safety and mission readiness. The MRO services for this segment focus on ensuring reliability, quick turnaround times, and adherence to stringent safety standards, particularly given the critical nature of rotorcraft missions in military operations.

Segment Analysis: By MRO Type

Engine MRO Segment in Military Aviation MRO Market

The Engine MRO segment dominates the military aircraft MRO market, accounting for approximately 31% market share in 2024, while also demonstrating the strongest growth trajectory with a projected growth rate of around 2% from 2024-2029. This segment encompasses comprehensive maintenance activities for military aircraft engines, including inspections, repairs, and overhauls aimed at maintaining propulsion systems' reliability, efficiency, and safety. The segment's prominence is driven by the increasing complexity of modern military aircraft engines, stringent regulatory requirements, and the critical nature of engine performance in military operations. Major engine manufacturers like General Electric, Rolls Royce, Pratt & Whitney, and MTU Aero Engines significantly contribute to this segment through maintenance support contracts typically included in product purchase agreements. The integration of advanced technologies like predictive maintenance and real-time monitoring systems has further enhanced the segment's capabilities in ensuring optimal engine performance and reliability.

Remaining Segments in Military Aviation MRO Market

The military aircraft MRO market encompasses several other crucial segments, including Components and Modifications MRO, Field Maintenance, and Airframe MRO. The Components and Modifications segment focuses on maintaining and upgrading various aircraft systems, including actuators, landing gear, weapon systems, and avionics, playing a vital role in ensuring mission readiness. Field Maintenance services provide crucial on-site support through diagnostic operations, cleaning procedures, and component replacements, enabling rapid response to maintenance needs. The Airframe MRO segment specializes in structural maintenance and repairs, including fuselage maintenance and corrosion prevention, which are essential for extending aircraft service life. Each of these segments contributes uniquely to the overall market ecosystem, with their services being essential for maintaining the operational effectiveness of military aircraft fleets worldwide.

Military Aviation Maintenance, Repair, And Overhaul Market Geography Segment Analysis

Military Aviation MRO Market in North America

North America represents a dominant force in the global military aviation MRO market, driven by the presence of major defense contractors and the world's largest military aircraft fleet. The region's market is characterized by sophisticated MRO infrastructure, advanced technological capabilities, and substantial defense budgets. Both the United States and Canada maintain significant military aviation assets, with the US leading in terms of fleet size and operational requirements. The region's focus on aircraft modernization programs, coupled with the need to maintain aging aircraft fleets, continues to drive demand for comprehensive military MRO services.

Military Aviation MRO Market in the United States

The United States dominates the North American military aviation MRO market, commanding approximately 95% of the regional market share in 2024. This dominance stems from housing the world's largest military aircraft fleet, including 2,757 combat aircraft, 731 special mission aircraft, and substantial numbers of transport and training aircraft. The US Air Force's commitment to maintaining operational readiness across its diverse fleet drives continuous demand for military MRO services. The country's robust defense infrastructure, supported by major contractors and specialized MRO facilities, enables comprehensive maintenance capabilities for both legacy platforms and next-generation aircraft. The size of US military fleet significantly influences the demand for MRO services.

Military Aviation MRO Market in Canada

Canada's military aviation MRO market demonstrates steady growth, supported by the country's strategic focus on modernizing its military aircraft fleet and enhancing its defense capabilities. The Canadian Armed Forces' diverse fleet, comprising combat aircraft, special mission aircraft, and helicopters, necessitates comprehensive MRO services. The country's emphasis on developing domestic MRO capabilities, coupled with strategic partnerships with international defense contractors, positions it for sustained growth. Canada's investment in new aircraft acquisitions and fleet modernization programs, including the procurement of F-35 fighters and maintenance contracts for existing platforms, underscores its commitment to maintaining a capable and well-maintained military aviation fleet.

Military Aviation MRO Market in Europe

Europe represents a significant market for military aviation MRO services, characterized by diverse requirements across multiple countries and a strong focus on technological advancement. The region's market is driven by ongoing modernization programs, increasing defense budgets, and the need to maintain operational readiness in response to evolving security challenges. Countries like the United Kingdom, France, Germany, and Russia maintain substantial military aircraft fleets, each with unique MRO requirements and capabilities. The region's emphasis on developing domestic MRO capabilities and fostering international collaboration continues to shape market dynamics.

Military Aviation MRO Market in Russia

Russia emerges as the largest military aviation MRO market in Europe, accounting for approximately 25% of the regional market share in 2024. The country maintains an extensive fleet of military aircraft, including 1,539 combat aircraft, 1,547 combat helicopters, and various transport and special mission aircraft. Russia's commitment to military modernization and the need to maintain its large fleet drives substantial demand for MRO services. The country's robust domestic aerospace industry and comprehensive MRO infrastructure support its position as a regional leader.

Military Aviation MRO Market in Germany

Germany demonstrates the highest growth potential in Europe's military aviation MRO market, with a projected growth rate of approximately 3% from 2024 to 2029. The country's strategic focus on modernizing its military aircraft fleet and enhancing its maintenance capabilities drives this growth. Germany's commitment to NATO obligations and increasing defense spending supports ongoing investments in MRO infrastructure. The country's emphasis on developing advanced maintenance capabilities and adopting innovative technologies positions it as a key growth market in the region.

Military Aviation MRO Market in Asia-Pacific

The Asia-Pacific region represents a dynamic and rapidly evolving market for military aviation MRO services, driven by increasing defense budgets, growing military modernization programs, and rising regional security concerns. Countries like China, India, Japan, and South Korea maintain significant military aircraft fleets, each with comprehensive MRO requirements. The region's focus on developing indigenous MRO capabilities and reducing dependence on foreign providers shapes market dynamics. Increasing military tensions and the need to maintain operational readiness drive sustained demand for MRO services across the region.

Military Aviation MRO Market in China

China stands as the dominant force in the Asia-Pacific military aviation MRO market, supported by its extensive military aircraft fleet and robust domestic aerospace industry. The country's commitment to military modernization and the development of advanced maintenance capabilities drives market growth. China's strategic focus on enhancing its military aviation capabilities, coupled with significant investments in MRO infrastructure and technology, reinforces its position as the regional market leader.

Military Aviation MRO Market in India

India emerges as the fastest-growing market for military aviation MRO services in the Asia-Pacific region, driven by its ambitious military modernization programs and increasing focus on developing domestic MRO capabilities. The country's strategic partnerships with international aerospace companies and investments in MRO infrastructure support this growth trajectory. India's emphasis on self-reliance in defense maintenance and the expansion of its military aircraft fleet contribute to its dynamic market growth. The India military size and its modernization efforts are pivotal in shaping the MRO landscape.

Military Aviation MRO Market in Latin America

The Latin American military aviation MRO market is characterized by varying levels of capability and demand across different countries, with Brazil emerging as both the largest and fastest-growing market in the region. The region's market is driven by the need to maintain aging aircraft fleets and modernize military aviation capabilities. Countries across Latin America are increasingly focusing on developing domestic MRO capabilities to reduce dependence on foreign providers. The market is shaped by defense budget constraints, fleet modernization initiatives, and the need to maintain operational readiness of existing aircraft.

Military Aviation MRO Market in Middle East & Africa

The Middle East & Africa region demonstrates significant potential in the military aviation MRO market, driven by substantial defense spending and ongoing military modernization programs. Saudi Arabia emerges as the largest market in the region, supported by its extensive military aircraft fleet and significant defense budget. The United Arab Emirates shows the fastest growth potential, driven by its strategic focus on developing advanced MRO capabilities. The region's market is characterized by increasing investments in domestic MRO infrastructure, strategic partnerships with international providers, and the need to maintain growing military aircraft fleets. Countries like Qatar and Egypt also contribute significantly to regional market dynamics through their military modernization initiatives and growing focus on developing local MRO capabilities.

Military Aircraft MRO Industry Overview

Top Companies in Military Aviation MRO Market

The military aviation MRO market features prominent players like Boeing, RTX Corporation, Lockheed Martin, BAE Systems, and Safran leading the industry through continuous innovation and strategic developments. These military MRO companies are investing heavily in advanced technologies like predictive maintenance, augmented reality, and additive manufacturing to enhance their service capabilities and operational efficiency. The industry is witnessing a significant shift towards digitalization and automation of MRO processes, with companies developing integrated solutions that combine traditional maintenance practices with data analytics and artificial intelligence. Market leaders are expanding their global footprint through strategic partnerships and establishing regional MRO facilities to better serve local military customers. There is also an increasing focus on developing sustainable MRO practices and green initiatives to reduce environmental impact while maintaining high service standards.

Market Dominated by Defense Industry Giants

The military aviation MRO market structure is characterized by the dominance of large defense contractors and aerospace conglomerates that possess extensive technical expertise and established relationships with military organizations worldwide. These major players benefit from their integrated capabilities across the aerospace and defense value chain, combining aircraft manufacturing expertise with comprehensive MRO services. The market shows high consolidation levels, particularly in regions with significant military presence like North America and Europe, where established players have built strong barriers to entry through their specialized capabilities and long-term service contracts with defense departments.

The industry landscape is shaped by strategic mergers and acquisitions, as larger companies seek to expand their service portfolios and geographical reach through targeted acquisitions of specialized MRO providers and technology companies. Market participants are increasingly focusing on vertical integration strategies to strengthen their position in the value chain, while also pursuing horizontal expansion through partnerships and joint ventures with regional players to access new markets and customer bases. The competitive dynamics are further influenced by the growing trend of OEMs expanding their aftermarket services, creating a more complex and interconnected market structure.

Innovation and Adaptability Drive Future Success

Success in the military aviation MRO market increasingly depends on companies' ability to adapt to evolving technological requirements and changing military operational needs. Incumbent players must focus on developing comprehensive service solutions that integrate advanced diagnostics, predictive maintenance capabilities, and digital platforms to maintain their market position. Companies need to invest in building robust supply chain networks, developing specialized expertise in emerging technologies, and creating flexible service models that can accommodate various aircraft types and military requirements. The ability to offer customized solutions while maintaining cost efficiency and service quality will be crucial for market success.

For new entrants and growing players, the path to market share growth lies in identifying and exploiting niche segments, developing specialized capabilities in emerging technologies, and building strong relationships with military customers. Companies must navigate complex regulatory requirements while maintaining high security and quality standards essential for military aircraft maintenance. The future competitive landscape will be shaped by factors such as the increasing focus on operational readiness, the growing importance of cybersecurity in MRO operations, and the need for sustainable maintenance practices. Success will depend on companies' ability to balance innovation with reliability, cost-effectiveness with service quality, and global reach with local presence.

Military Aircraft MRO Market Leaders

-

Lockheed Martin Corporation

-

The Boeing Company

-

Safran

-

RTX Corporation

-

Rolls-Royce plc

- *Disclaimer: Major Players sorted in no particular order

Military Aircraft MRO Market News

April 2023: The Brazilian Air Force designated the responsibility of providing comprehensive maintenance, repair, and overhaul (MRO) services for the Rolls-Royce AE 3007 engines to StandardAero. These engines power the Brazilian Air Force’s fleet of Embraer ERJ-145 aircraft. Under the exclusive multi-year agreement, StandardAero will provide MRO services for FAB's AE 3007A equipped fleet from its facility in Maryville, the US, an OEM-approved authorized maintenance center (AMC) for the AE 3007 family of engines.

March 2023: GE Aerospace granted ITP Aero a service contract extension to conduct maintenance, repair, and overhaul services for CT7 engines at its facility in Albacete, Spain. The CT7-8 is a powerful engine designed to meet the demanding mission needs of commercial heavy-lift helicopters and modern military medium helicopters worldwide.

Military Aircraft MRO Industry Segmentation

Aircraft MRO includes tasks performed to ensure the airworthiness of an aircraft and its parts. MRO service providers perform overhaul, inspection, replacement, defect rectification, and the embodiment of modifications in compliance with airworthiness directives and repair.

The military aviation MRO market is segmented by aircraft type, MRO type, and geography. By aircraft type, the market is segmented into fixed-wing and rotary-wing. By MRO type, the market is segmented into engine MRO, components and modifications MRO, airframe MRO, and field maintenance. The report also covers the market size and forecast for the military aviation MRO market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Aircraft Type | Fixed-wing | ||

| Rotary-wing | |||

| By MRO Type | Engine MRO | ||

| Components and Modifications MRO | |||

| Airframe MRO | |||

| Field Maintenance | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

| Fixed-wing |

| Rotary-wing |

| Engine MRO |

| Components and Modifications MRO |

| Airframe MRO |

| Field Maintenance |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| France | |

| Germany | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Rest of Middle East and Africa |

Military Aircraft MRO Market Research FAQs

How big is the Military Aviation Maintenance, Repair, And Overhaul Market?

The Military Aviation Maintenance, Repair, And Overhaul Market size is expected to reach USD 42.49 billion in 2025 and grow at a CAGR of 2.81% to reach USD 48.81 billion by 2030.

What is the current Military Aviation Maintenance, Repair, And Overhaul Market size?

In 2025, the Military Aviation Maintenance, Repair, And Overhaul Market size is expected to reach USD 42.49 billion.

Who are the key players in Military Aviation Maintenance, Repair, And Overhaul Market?

Lockheed Martin Corporation, The Boeing Company, Safran, RTX Corporation and Rolls-Royce plc are the major companies operating in the Military Aviation Maintenance, Repair, And Overhaul Market.

Which is the fastest growing region in Military Aviation Maintenance, Repair, And Overhaul Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Military Aviation Maintenance, Repair, And Overhaul Market?

In 2025, the North America accounts for the largest market share in Military Aviation Maintenance, Repair, And Overhaul Market.

What years does this Military Aviation Maintenance, Repair, And Overhaul Market cover, and what was the market size in 2024?

In 2024, the Military Aviation Maintenance, Repair, And Overhaul Market size was estimated at USD 41.30 billion. The report covers the Military Aviation Maintenance, Repair, And Overhaul Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Military Aviation Maintenance, Repair, And Overhaul Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: June 16, 2024