Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

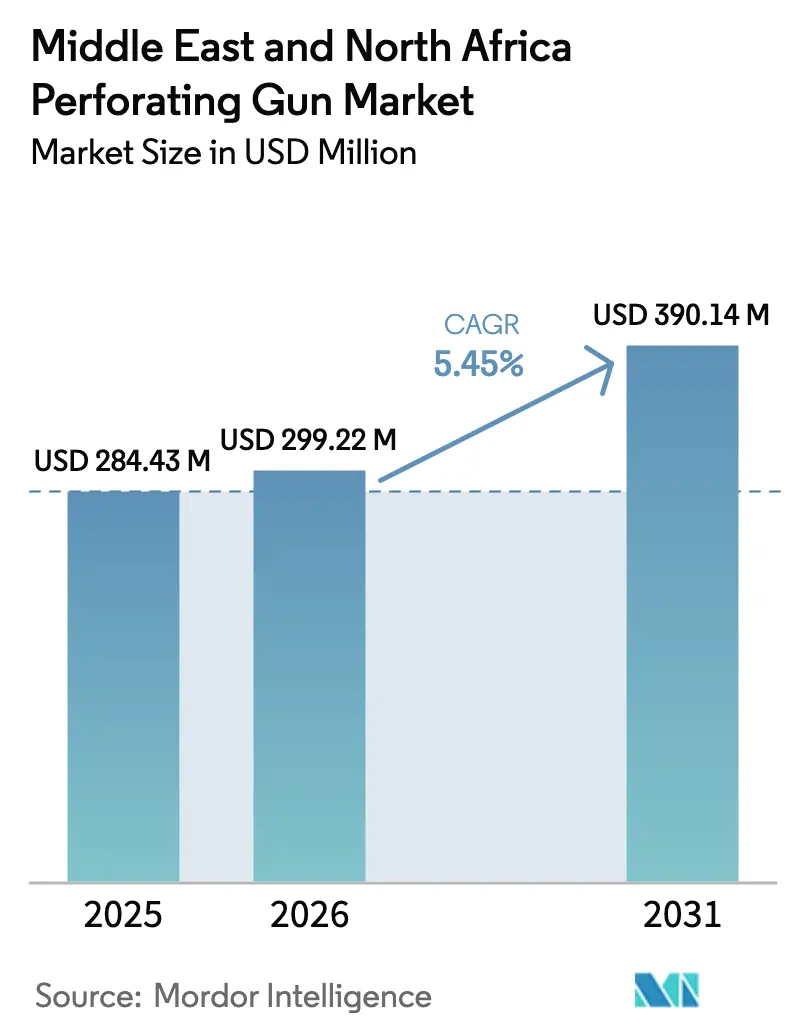

| Base Year Market Size (2025) | USD 284.43 Million |

| Market Size (2026) | USD 299.22 Million |

| Market Size (2031) | USD 390.14 Million |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And North Africa Perforating Gun Market Analysis by Mordor Intelligence

The Middle East And North Africa Perforating Gun Market size is projected to expand from USD 284.43 million in 2025 and USD 299.22 million in 2026 to USD 390.14 million by 2031, registering a CAGR of 5.45% between 2026 to 2031.

Several factors underpin this steady climb. Horizontal drilling campaigns in unconventional reservoirs demand higher shot densities than legacy vertical wells, multiplying perforating-gun intensity per completion. National oil companies (NOCs) are simultaneously directing sizable re-perforation budgets toward mature onshore fields to defer expensive infill drilling. Localization mandates such as Saudi Aramco’s iktva and ADNOC’s in-country value (ICV) framework shorten supply chains, support regional manufacturing of shaped charges, and stabilize lead times despite global logistics shocks. Operators are also embracing rig-less conveyance, coiled-tubing, and slickline to trim intervention costs, while offshore gas megaprojects in Qatar and Egypt accelerate demand for high-pressure tubing-conveyed systems. Against this backdrop, competitive dynamics are intensifying as integrated service majors defend share against regional specialists and state-owned Chinese contractors.

Key Report Takeaways

- By carrier type, retrievable tubing guns held a 30.2% share of the Middle East & North Africa perforating gun market size in 2025 and are expanding at an 8.1% CAGR through 2031.

- By well type, horizontal and deviated wells captured 64.9% of the Middle East & North Africa perforating gun market share in 2025.

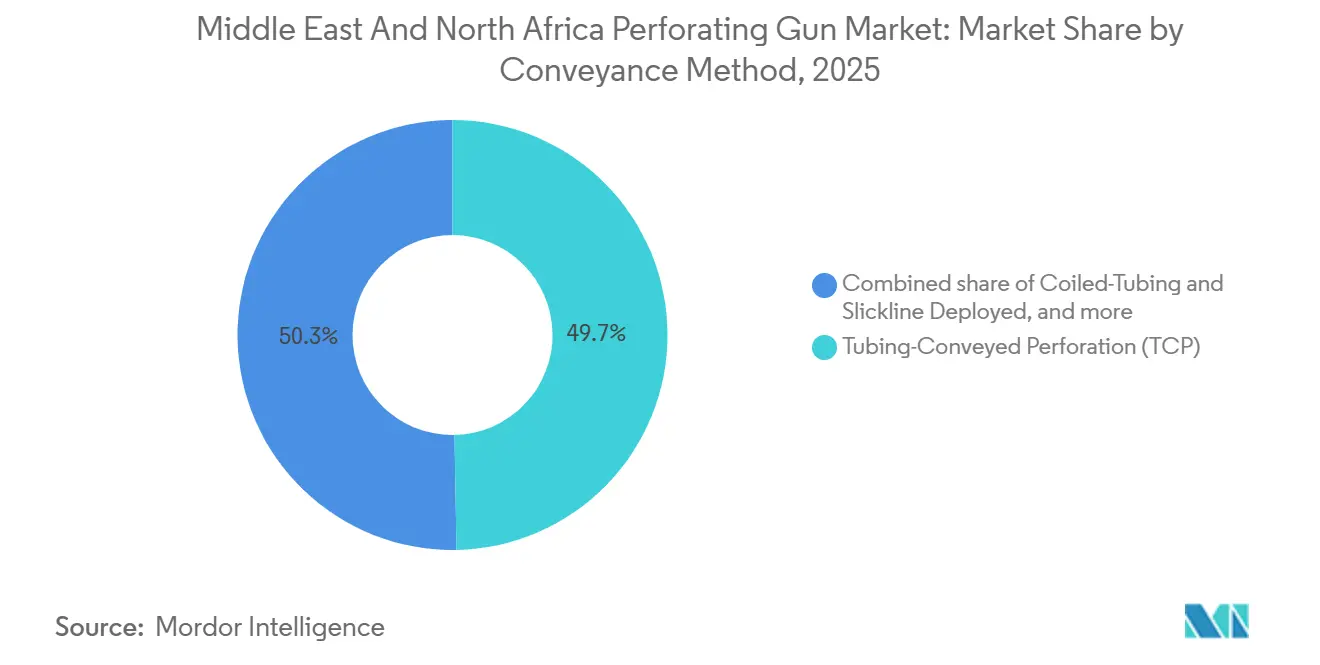

- By conveyance method, coiled-tubing is forecast to post a 7.3% CAGR through 2031, the fastest growth within the segment mix.

- By application, offshore projects accounted for 24.9% of the Middle East & North Africa perforating gun market size in 2025 and are advancing at a 7.8% CAGR to 2031.

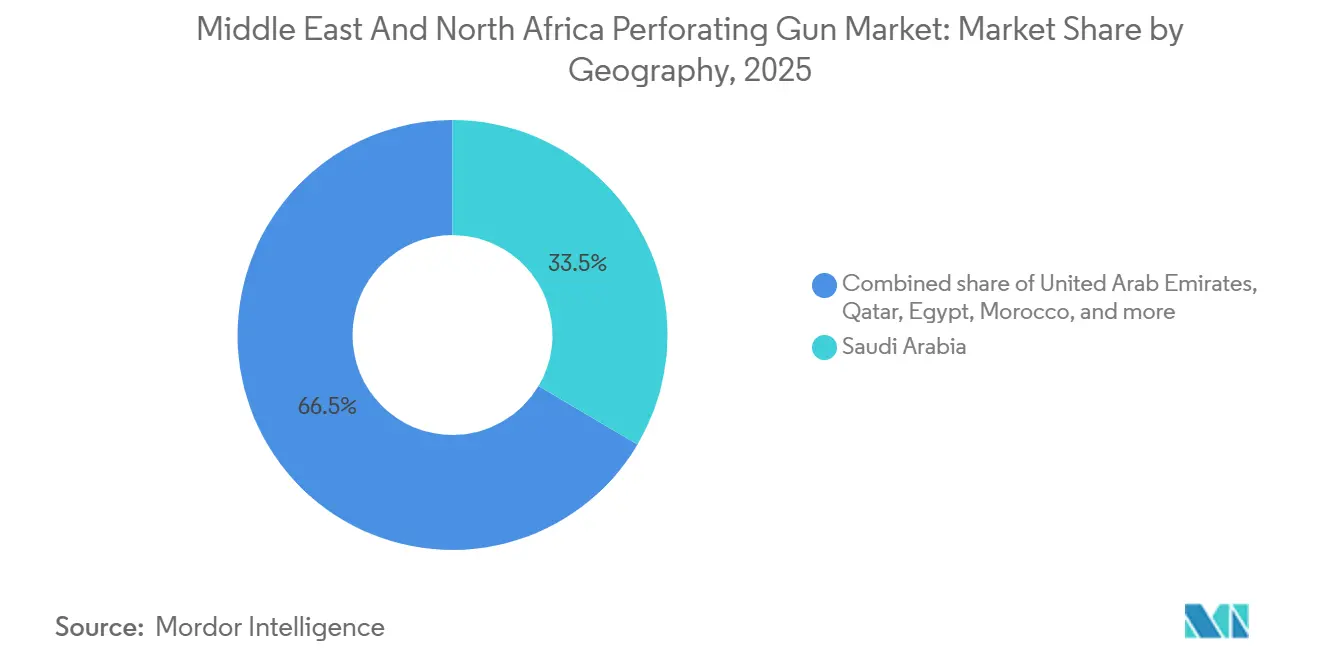

- By geography, Saudi Arabia, the largest geography, commanded 33.5% revenue share in 2025, while Morocco is projected to be the fastest-growing country at an 8.0% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East And North Africa Perforating Gun Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in unconventional horizontal drilling programs | +1.4% | Saudi Arabia (Jafurah, Tuwaiq), UAE (unconventional gas), Oman | Long term (≥ 4 years) |

| Accelerating re-perforation campaigns in mature MENA fields | +1.1% | Saudi Arabia (Ghawar, Safaniyah), UAE (onshore fields), Kuwait, Algeria | Medium term (2-4 years) |

| National oil-company push for in-country perforating manufacturing | +0.9% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Adoption of compact fragmenting guns to cut rigless P&A cost | +0.7% | Saudi Arabia, UAE, Qatar, Egypt | Short term (≤ 2 years) |

| Rising rig-less well-intervention budgets post-2024 oil-price rebound | +0.8% | Global MENA, with concentration in Saudi Arabia, UAE | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Unconventional Horizontal Drilling Programs

Commercial production from Saudi Arabia’s Jafurah shale in December 2025 marked a watershed for unconventional gas in the region, with 200 horizontal wells slated annually through 2031 and each well demanding 8–12 perforating stages.[1]Saudi Aramco, “Jafurah Gas Program Update,” aramco.com Similar tight-gas pilots in the UAE’s Diyab and Bab formations and Oman’s Mabrouk North East project reinforce the pull for high-shot-density gun strings. The switch to long laterals favors retrievable and fragmenting carriers that leave minimal debris and cut clean-out time. In parallel, local-content rules compel global vendors to co-manufacture shaped charges in the Gulf, reducing customs delays. Collectively, these trends lift per-well hardware intensity and anchor long-term demand across the Middle East & North Africa perforating gun market.

Accelerating Re-Perforation Campaigns in Mature MENA Fields

Selective re-perforation in Saudi Arabia’s Ghawar, Kuwait’s Burgan, and ADNOC’s onshore blocks is delivering 15%–25% production uplifts at one-tenth the cost of drilling new wells.[2]Schlumberger, “Kuwait Burgan Field Case Study,” slb.com Coiled-tubing conveyance enables live-well interventions, avoiding costly workovers. Algeria and Egypt apply similar tactics in thin pay zones, extending field life by up to 10 years. Rapid payback, often under six months, encourages NOCs to earmark rising portions of well-services budgets for re-perforation, reinforcing a resilient aftermarket for the Middle East & North Africa perforating gun market.

National Oil-Company Push for In-Country Perforating Manufacturing

Aramco’s iktva program certified 59 perforating-equipment suppliers by 2022 and redirected USD 11 billion into the Saudi supply chain. ADNOC’s ICV scheme has cycled AED 242 billion (USD 65.9 billion) into local vendors since 2018 and sets an AED 90 billion target by 2030. QatarEnergy follows suit with contract clauses mandating local assembly for North Field expansion hardware. Localization compresses lead times from 12–16 weeks to roughly six weeks, cushions freight volatility, and locks multiyear call-off agreements in favor of vendors that invest in regional plants, thereby fortifying the Middle East & North Africa perforating gun market.

Adoption of Compact Fragmenting Guns to Cut Rig-less P&A Cost

Fragmenting or capsule guns disintegrate upon detonation, eliminating retrieval trips and slashing plug-and-abandonment (P&A) timelines. Aramco recorded 35% cost savings across 15 Safaniyah wells in 2024 after adopting expendable capsule guns. ADNOC achieved similar efficiencies in offshore Umm Shaif, while UAE regulations encourage low-debris systems for environmental compliance.[3]UAE Government, “Federal Law No. 24 of 1999,” uae.gov.ae Offshore platforms facing decommissioning mandates now view fragmenting carriers as an economical route, opening a sizeable niche within the Middle East & North Africa perforating gun market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy CAPEX diversion by Gulf sovereign funds | -0.6% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Steel & RDX/HMX supply-chain volatility after Red Sea disruptions | -0.4% | Global MENA, import-dependent markets (Egypt, Morocco, Algeria) | Short term (≤ 2 years) |

| ESG-driven explosives-handling restrictions at onshore fields | -0.3% | Saudi Arabia, UAE, Algeria, Egypt (onshore-heavy markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy CAPEX Diversion by Gulf Sovereign Funds

Saudi Arabia’s Public Investment Fund now commits USD 10 billion annually to renewables, while the UAE targets USD 54 billion by 2030 through Masdar[4]Public Investment Fund, “Renewable Investment Strategy,” pif.gov.sa. Such commitments can cap upstream budgets, potentially trimming annual perforating-gun volumes by 8%–12% over a decade. Still, the projects that survive budget cuts often require higher-complexity completions, partly offsetting volume declines for the Middle East & North Africa perforating gun market.

Steel and RDX/HMX Supply-Chain Volatility After Red Sea Disruptions

Houthi attacks cut Suez Canal traffic in half during 2024, stretching freight times by two weeks and hiking rates threefold. Seamless tubing prices climbed 18%, and RDX shipments faced 6–8-week delays, forcing Egypt’s West Nile Delta project to postpone 12 perforating jobs. Operators with local manufacturing, such as Aramco and ADNOC, proved more resilient, highlighting the advantages of regional supply chains within the Middle East & North Africa perforating gun market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Carrier Type: Retrievable Guns Advance on Cost Efficiency

Retrievable tubing guns claimed 30.2% of the Middle East & North Africa perforating gun market size in 2025, thanks to their ability to be redeployed across multiple zones, driving an 8.1% CAGR outlook through 2031. Hollow-carrier systems, still dominant at 40.6%, remain indispensable in high-pressure carbonates where full debris retrieval safeguards well integrity. Fragmenting guns, though smaller in share, are gaining ground in offshore P&A campaigns where eliminating retrieval trips slashes rig days. Semi-expendable strip guns fill a niche for through-tubing work in tight-clearance casings. Over the forecast horizon, mature fields that require several interventions favor retrievable carriers for total-cost-of-ownership advantages, while single-shot unconventional wells continue to lean on expendable designs that compress completion time. Service firms are accordingly broadening portfolios: Halliburton opened a USD 45 million plant in Dammam in October 2025 to manufacture both hollow and retrievable carriers, achieving 72% local content and cementing preferred-vendor status with Aramco.

By Well Type: Horizontal Dominance Sustains Hardware Intensity

Horizontal and deviated wells accounted for 64.9% of the Middle East & North Africa perforating gun market demand in 2025 and are forecast to expand at 6.5% through 2031. Each Jafurah lateral needs 8–12 stages, quadrupling gun consumption over a conventional vertical well. QatarEnergy’s extended-reach offshore wells exceed 5,000 feet and rely on oriented shots to optimize fracture clusters. Vertical wells persist in Algeria and Egypt, where legacy infrastructure supports low-cost completions. Regulatory bodies such as the UAE Supreme Petroleum Council now encourage horizontal drilling to maximize reservoir contact, ensuring a sustained pull for high-shot-density systems. Consequently, tubing-conveyed and coiled-tubing conveyances outpace wireline in long laterals, reinforcing the lead of horizontal architecture within the Middle East & North Africa perforating gun market.

By Conveyance Method: Coiled-Tubing Captures Rig-Less Upside

Tubing-conveyed perforation (TCP) retained 49.7% revenue share in 2025, underpinned by high-pressure completions that demand robust well control. Yet coiled-tubing and slickline deployments, projected to grow 7.3% annually to 2031, thrive on rig-less economics. Schlumberger’s CoilFLEX cut intervention time in Kuwait’s Burgan field from four days to 1.5, freeing rigs for drilling new horizontals. Wireline’s share is slipping in torturous laterals where friction limits are reached. The conveyance mix is thus bifurcating: TCP stays dominant for new wells, while coiled-tubing rules re-perforation. This duality keeps the Middle East & North Africa perforating gun market competitive across equipment classes.

By Application: Offshore Share Rises on Gas Megaprojects

Onshore operations generated 75.1% of 2025 revenue, but offshore activity is gaining momentum with a 7.8% CAGR outlook through 2031. Qatar’s North Field, Egypt’s Zohr hub, and Morocco’s upcoming Anchois field drive demand for high-pressure, deep-water gun systems. Each subsea perforating job can cost USD 1.5 million, nearly quadruple the onshore average, magnifying revenue impact despite fewer wells. Operators increasingly specify fracturing carriers to cut offshore P&A expense, widening the adoption of expendable technology. If oil prices stay above USD 75/bbl, offshore’s contribution to the Middle East & North Africa perforating gun market will expand beyond the current one-quarter stake.

Geography Analysis

Saudi Arabia held 33.5% of the Middle East & North Africa perforating gun market revenue in 2025, underwritten by Aramco’s USD 50–60 billion annual upstream spend and the iktva program that channels purchases to 59 local suppliers. The Jafurah shale alone will require roughly 200 horizontal wells per year, each consuming 8–12 gun stages, ensuring robust demand through 2031. Concurrent re-perforation in giant maturing fields such as Ghawar and Khurais absorbs considerable volumes of through-tubing guns.

The United Arab Emirates follows as ADNOC’s ICV framework, targeting AED 90 billion in local spending by 2030, spurring regional manufacture of shaped charges and detonation cord. Qatar ranks third as its North Field LNG expansion schedules 120 offshore wells with high-pressure specifications that elevate average gun value per well.

Algeria and Egypt, characterized by vast inventories of aging wells, fund coiled-tubing re-perforations to extend field life. Sonatrach budgeted USD 2.1 billion for well interventions in 2024, assigning 35% to perforating services. Egypt’s joint ventures perforated 340 wells in 2024 using slim guns that pass through 2⅞-inch tubing, reducing rig time by 40%.

Morocco, though small today, is projected to grow at an 8.0% CAGR over 2026-2031 on the back of Chariot Energy’s Anchois development, which will introduce deep-water completion workflows and spur demand for specialized casing guns. Frontier license awards to TotalEnergies and Eni in 2024 could double prospective gas resources and prolong perforating demand into the next decade.

Elsewhere, Oman’s Mabrouk North East tight-gas project adds multi-stage fracturing work to the mix, while civil unrest continues to cap upside in Yemen and Libya. Overall, geographic dispersion balances the Middle East & North Africa perforating gun market, with Gulf incumbents pursuing localization and North African countries offering margin upside for agile entrants.

Competitive Landscape

The three global service majors, Schlumberger, Halliburton, and Baker Hughes, collectively control about 55%–60% of the Middle East & North Africa perforating gun market, bundling hardware with broader completion and intervention services. Regional challengers are closing gaps: ADNOC Drilling’s 2021 IPO funded 12 coiled-tubing units and eight wireline spreads, enabling turnkey packages priced 15%–20% below international competitors. Chinese contractors, led by Sinopec Oilfield Service, undercut bids by roughly 25% but face hurdles in meeting local-content thresholds that favor Gulf-based fabrication.

Technology differentiation concentrates on shaped-charge design and oriented-shot placement. DynaEnergetics’ DS Select copper-liner charges penetrated 15% deeper than standard alternatives and gained traction in Saudi tight-gas wells during 2025. Weatherford’s Centric system places shots on the low side of horizontal wellbores and raised initial production 16% in ADNOC’s Bab field. Fragmenting guns for offshore P&A remains under-penetrated at less than 20% of interventions, representing a potential USD 180–220 million opportunity through 2031.

Regulatory compliance, ISO 10426, API RP 19B, remains mandatory, yet NOC localization programs increasingly dictate vendor selection. Companies committing to Gulf manufacturing secure multi-year call-off contracts, while import-dependent players risk erosion of market share. Competitive intensity is therefore expected to rise, but high technical barriers and safety requirements continue to guard margins for established suppliers in the Middle East & North Africa perforating gun market.

Middle East And North Africa Perforating Gun Industry Leaders

Baker Hughes Company

Schlumberger Limited

Weatherford International PLC

Halliburton Company

Hunting plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Abu Dhabi National Oil Company (ADNOC) has unveiled bold plans for oil and gas production, coupled with a commitment to local procurement, backed by significant investments through 2027. Initiatives like "Make it in the Emirates" bolster local manufacturing of oilfield services and equipment, streamlining the regional supply and deployment of perforating systems.

- September 2025: Petroleum Development Oman (PDO) and Schlumberger (SLB) inked a deal to set up the Oman Perforation Technology Centre, marking the debut of a perforating charges manufacturing facility tailored for oil and gas operations in the Middle East and North Africa.

- September 2024: Today, GEODynamics, a global frontrunner in perforating and downhole solutions, unveiled its latest innovation: the EPIC Flex Orbit Perforating System. This new system enhances the already robust EPIC Flex suite of offerings.

- February 2024: GEODynamics patented the EPIC suite of perforation technologies. The EPIC collection includes EPIC Precision and EPIC Flex top-loading gun systems, which can withstand the harshest conditions to deliver greater safety, uptime, and operational efficiencies.

Middle East And North Africa Perforating Gun Market Report Scope

A perforating gun is used to make holes in oil and gas wells in preparation for production. For oil and gas to flow into the wellbore, perforations must be made, and this is accomplished by lowering the gun down the well.

The Middle East & North Africa perforating gun market is segmented by carrier type, well type, conveyance method, application, and geography. By carrier type, the market is segmented into hollow carrier, fragmenting/capsule, semi-expendable strip, and retrievable tubing guns. By well type, the market is segmented into horizontal and deviated wells, and vertical wells. By conveyance method, the market is segmented into wireline-conveyed casing guns, tubing-conveyed perforation, and coiled-tubing and slickline-deployed systems. By application, the market is segmented into onshore and offshore operations. By geography, the market is segmented into Saudi Arabia, the United Arab Emirates, Qatar, Algeria, Egypt, Morocco, and the rest of the Middle East & North Africa. For each segment, market sizing and forecasts are provided on the basis of value (USD).

By Carrier Type

| Hollow Carrier |

| Fragmenting/Capsule (Expendable) |

| Semi-Expendable Strip |

| Retrievable Tubing Guns |

By Well Type

| Horizontal and Deviated |

| Vertical |

By Conveyance Method

| Wireline-Conveyed Casing Guns |

| Tubing-Conveyed Perforation (TCP) |

| Coiled-Tubing and Slickline Deployed |

By Application

| Onshore |

| Offshore |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Algeria |

| Egypt |

| Morocco |

| Rest of Middle East and North Africa |

| By Carrier Type | Hollow Carrier |

| Fragmenting/Capsule (Expendable) | |

| Semi-Expendable Strip | |

| Retrievable Tubing Guns | |

| By Well Type | Horizontal and Deviated |

| Vertical | |

| By Conveyance Method | Wireline-Conveyed Casing Guns |

| Tubing-Conveyed Perforation (TCP) | |

| Coiled-Tubing and Slickline Deployed | |

| By Application | Onshore |

| Offshore | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Algeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and North Africa |

Key Questions Answered in the Report

How large is the Middle East & North Africa perforating gun market in 2026?

The market is valued at USD 299.22 million in 2026 and is forecast to grow at a 5.45% CAGR to USD 390.14 million by 2031.

Which well type dominates regional demand?

Horizontal and deviated wells account for 64.9% of 2025 demand and are expanding at a 6.5% CAGR as unconventional gas and extended-reach offshore projects multiply perforating stages per well.

Why are retrievable guns gaining share?

Retrievable tubing guns can be reused across multiple zones, lowering total-cost-of-ownership and driving an 8.1% CAGR outlook through 2031.

How will localization policies affect suppliers?

Programs such as iktva and ICV shorten lead times, lock in long-term contracts, and favor vendors that invest in Gulf manufacturing facilities.

What is the outlook for offshore applications?

Offshore perforating demand is forecast to rise at 7.8% through 2031, propelled by deep-water gas megaprojects in Qatar, Egypt, and Morocco that require high-pressure gun systems.

Page last updated on: