Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

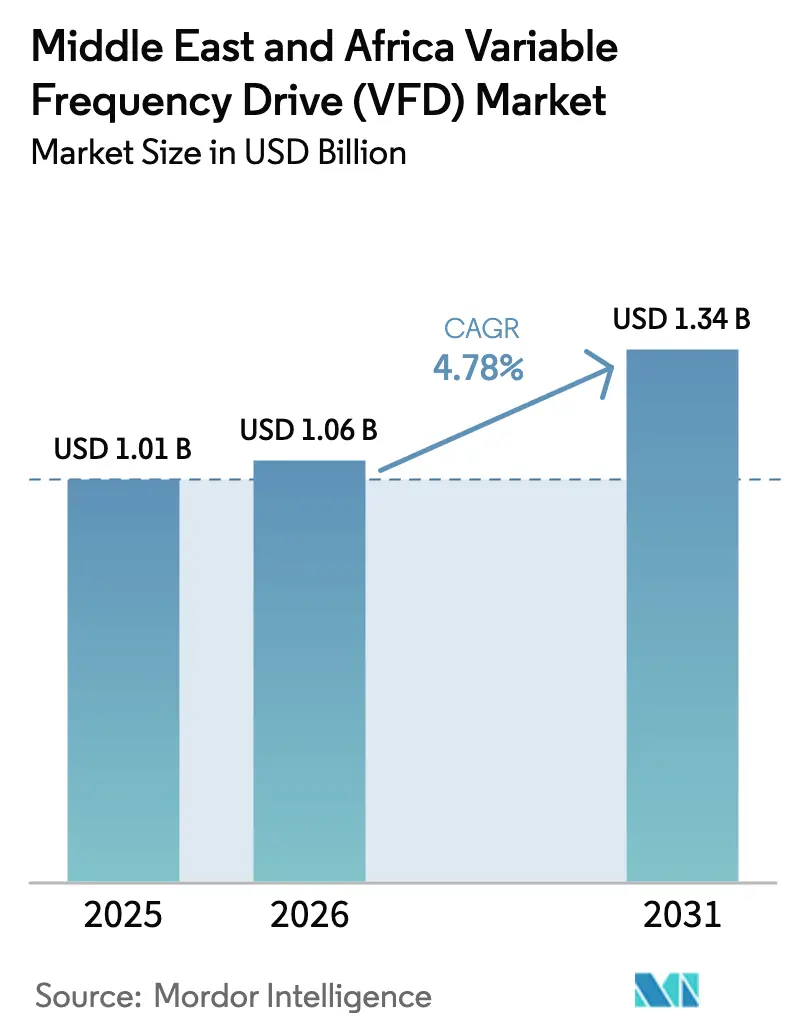

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Variable Frequency Drive (VFD) Market Analysis by Mordor Intelligence

The variable frequency drive market size in the Middle East and Africa is expected to grow from USD 1.01 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.34 billion by 2031 at 4.78% CAGR over 2026-2031. Rising efficiency mandates, widening desalination capacity, and rapid solar-PV rollout form the backbone of demand, while precision-centric applications such as servo-based solar trackers add incremental gains. Medium-voltage specifications tied to green-hydrogen and LNG mega-projects lift the value mix, even as low-voltage installations dominate in commercial HVAC retrofits. Competitive intensity sits at a moderate level, with European and Asian multinationals cementing share through technology depth, regional assembly, and lifecycle services, while local assemblers leverage public-sector localization incentives for entry points. Volatile oil-price-linked capex cycles and fragmented post-warranty service outside the GCC temper the variable frequency drive market growth outlook.

Key Report Takeaways

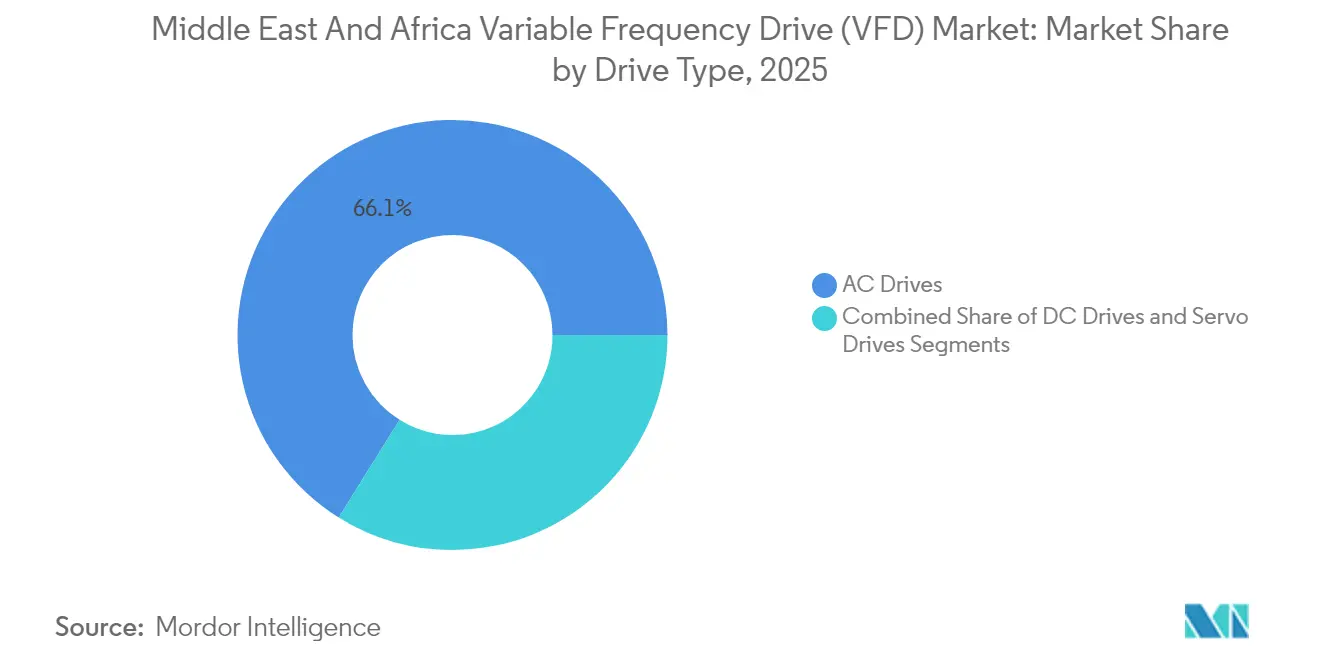

- By drive type, AC drives led with 66.12% revenue share of the Middle East and Africa variable frequency drive market in 2025, while servo drives are projected to grow at a 5.63% CAGR through 2031.

- By power rating, the 5-30 kW class held 38.35% of the 2025 value of the Middle East and Africa variable frequency drive market, whereas 31-75 kW systems are forecast to advance at a 5.78% CAGR to 2031.

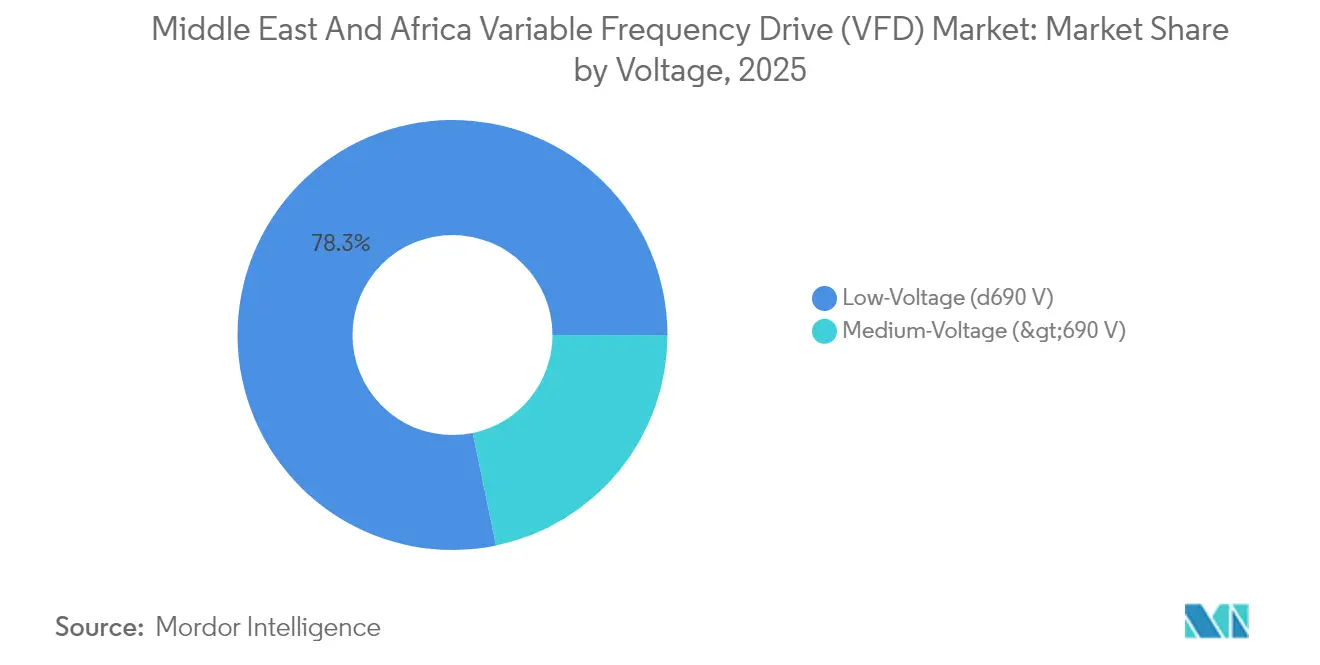

- By voltage, low-voltage units captured 78.25% of the 2025 revenue of the Middle East and Africa variable frequency drive market, while medium-voltage installations are set to post a 5.29% CAGR through 2031.

- By end-user, oil and gas accounted for 32.74% of the 2025 spending of the Middle East and Africa variable frequency drive market, yet water and wastewater treatment is expanding at a 6.24% CAGR to 2031.

- By application, pumps commanded a 39.55% share of the Middle East and Africa variable frequency drive market in 2025, while compressors are registering the fastest uptake at a 5.88% CAGR.

- By geography, the Middle East dominated with 69.62% market share of the Middle East and Africa variable frequency drive market in 2025, whereas Africa is anticipated to record a 5.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Variable Frequency Drive (VFD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying energy-efficiency mandates across Middle East and Africa | +1.2% | Global MEA, strongest in GCC states | Medium term (2-4 years) |

| Massive build-out of desalination and district-cooling infrastructure | +1.4% | Middle East core, UAE and Saudi Arabia | Long term (≥ 4 years) |

| Rapid solar-PV integration driving need for variable-speed motors | +0.9% | Middle East and North Africa | Medium term (2-4 years) |

| Shift toward electric submersible pumps in mature oilfields | +0.8% | GCC states, Algeria, Nigeria | Short term (≤ 2 years) |

| Government-funded localization of industrial automation manufacturing | +0.6% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Upcoming green-hydrogen mega-projects requiring medium-voltage VFDs | +0.7% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Energy-Efficiency Mandates Across Middle East and Africa

Governments across GCC states now specify IE3 and IE4 motor efficiency classes for new installations, prompting widespread adoption of inverter-driven systems to match the higher in-rush requirements of premium motors.[1]International Electrotechnical Commission, “IEC 61800-9-2,” IEC.ch Utility rebate programs in Saudi Arabia and the UAE cut payback periods for HVAC retrofits to under three years, accelerating replacement of fixed-speed starters with modern drives. Grid operators in Oman have begun applying power-factor penalties above 0.90, nudging industrial users toward drives equipped with active front-end rectifiers. Multilateral development banks have embedded efficiency targets into desalination and wastewater funding criteria, making variable speed control a prerequisite for loan approval. Together, these policies create a predictable baseline for the variable frequency drive market while fostering a services ecosystem around inspection and tuning of installed bases.

Massive Build-Out of Desalination and District-Cooling Infrastructure

Saudi Arabia’s National Water Strategy calls for 8.5 million m³/day of incremental desalination by 2030, translating into thousands of 5-75 kW pump drives for reverse-osmosis feed and brine recirculation circuits.[2]International Electrotechnical Commission, “Electric motors,” IEC.ch District-cooling operators in Dubai, Doha, and Abu Dhabi report 20-30% energy savings after migrating from throttling valves to speed control, bolstering payback narratives for financiers. Integration of rooftop solar and waste-heat recovery complicates load profiles, heightening the need for digital drives that track variable head pressures without cavitation. Specifications now routinely cite IEC 61800-9-2 efficiency classes, steering procurement toward higher-grade converter topologies. As chilled-water networks extend to mixed-use megaprojects like NEOM and Lusail, the variable frequency drive market gains high-volume orders linked to long-dated concession agreements that secure O&M revenues.

Rapid Solar-PV Integration Driving Need for Variable-Speed Motors

Utility-scale solar parks across Saudi Arabia, Egypt, and Morocco exceeded 24 GW of cumulative capacity in 2025, creating variable power conditions that favor inverters with ride-through and low-voltage support. Servo drives enable single-axis and dual-axis trackers to improve yield up to 17% versus fixed-tilt arrays, underpinning the 5.83% CAGR in the servo segment. In NEOM’s hydrogen complex, 2.2 GW of electrolyzers rely on medium-voltage drives to modulate compressor loads in sync with fluctuating solar output, demonstrating high-value niches for digitally networked units. Regional grid codes increasingly mandate active-harmonic mitigation, pushing suppliers to embed twelve-pulse or active-filter stages. As solar LCOE falls below USD 20 /MWh in Dubai tenders, operators focus on balancing OPEX, where efficient motor control is the fastest lever.

Government-Funded Localization of Industrial Automation Manufacturing

Saudi Arabia’s Vision 2030 sets 50% local-content thresholds for public-sector industrial projects, prompting OEMs to assemble drives in the kingdom and transfer test-bench know-how to domestic partners. The UAE’s In-Country Value program offers bid preference scoring, guiding global vendors to establish wiring-harness and PCB sub-assemblies in free zones. Egypt’s industrial zones provide ten-year tax holidays for automation firms, positioning Cairo as a re-export hub to North and West Africa. Local assembly slashes lead times from 14 weeks to 6 weeks for standard 30-kW units and improves spare-parts availability, directly addressing aftermarket constraints outside the GCC. Over time, localization also cultivates an indigenous technician base, raising service density and reinforcing pull-through for the variable frequency drive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile capex cycles tied to Brent-crude price swings | -1.1% | Oil-dependent economies: GCC, Algeria, Nigeria | Short term (≤ 2 years) |

| Fragmented aftermarket service networks outside GCC | -0.8% | Sub-Saharan Africa, North Africa excluding Egypt | Medium term (2-4 years) |

| Limited grid-power quality hindering high-frequency inverter adoption | -0.6% | Rural Africa, secondary cities | Long term (≥ 4 years) |

| Persistent import tariffs on power-electronic components in Africa | -0.5% | Sub-Saharan Africa excluding South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Capex Cycles Tied to Brent-Crude Price Swings

EIA projections place Brent at USD 74 /bbl in 2025 before sliding to USD 66 /bbl in 2026, narrowing fiscal buffers for oil-weighted economies and leading to deferred automation budgets.[3]U.S. Energy Information Administration, “Short-Term Energy Outlook,” Eia.gov Project cancellations ripple fastest through mid-stream debottlenecking and petrochemical expansions, directly denting medium-voltage drive orders. Suppliers prioritize frame-size consolidation to hedge inventory risk, yet long planning horizons for LNG trains make timing mismatches inevitable. Loan syndicates become cautious on dollar-denominated debt for utilities, further trimming near-term tender volumes. Consequently, the variable frequency drive market endures uneven quarterly demand despite compelling lifecycle savings.

Fragmented Aftermarket Service Networks Outside GCC

Mining hubs in Zambia and Mali often face six-week lead times for power-module replacements, compelling operators to stock spares worth 12-18 months of consumption, inflating carrying costs. The scarcity of certified technicians results in extended downtime for water utilities in Kenya and Tanzania, where a failed 15-kW inverter can halt municipal supply for days. OEMs attempt to bridge gaps via remote diagnostics, yet patchy connectivity limits real-world effectiveness. International financiers now weigh service coverage maps when appraising infrastructure loans, inadvertently penalizing projects in thinly served geographies. Until local distributor capability expands, the variable frequency drive market will see adoption throttled by perceived reliability risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: AC Dominance, Servo Upswing

AC drives retained 66.12% share of the 2025 variable frequency drive market size thanks to proven durability in desert heat and refinery duty cycles. Servo drives posted a 5.63% CAGR as solar trackers, robotic welders, and pick-and-place units demanded sub-1° positioning accuracy. DC drives linger in niche mining hoists where torque control is paramount. The drive-type mix also reflects evolving motor standards; IEC-certified IE3 and IE4 motors prompt design tweaks in AC inverters to manage higher magnetizing currents, keeping established suppliers in pole position.

Projected upgrades across district-cooling plants and potable-water boosters sustain AC volume through 2031, yet incremental revenue skews toward servo units embedded with edge analytics. Vendors unlock cross-sell potential via integrated packages. ABB’s IE3-ready line couples synchronous reluctance motors with tailored drive firmware, while WEG’s axial-flux motor plus CFW900 inverter packs tighten the footprint for rooftop solar trackers. Such packaging deepens ecosystem stickiness and elevates service attachment in the variable frequency drive market.

By Power Rating: Mid-Range Drives Propel Growth

Products spanning 5-30 kW met 38.35% of 2025 demand, mirroring pump sizes in district-cooling loops and municipal well fields. The 31-75 kW class lifts fastest at 5.78% CAGR, riding medium-scale industrial automation across food processing and textiles in Egypt and Morocco. Sub-5 kW units flourish in building management, while >75 kW frames anchor desalination high-pressure pumps and refinery blowers.

Hydrogen hubs like NEOM create outsized pull for multi-megawatt ratings, but complex EPC cycles temper volume swings. Conversely, SME factories chasing ISO 50001 energy targets adopt mid-range drives as quick wins, reinforcing steady expansion. Capacity investments by regional assemblers shorten delivery to four weeks for 37-kW skids, strengthening the variable frequency drive market’s mid-band momentum.

By Voltage: Low-Voltage Retains Majority, Medium-Voltage Builds Momentum

Low-voltage products ≤690 V captured 78.25% of the 2025 value on the back of HVAC retrofits and packaged booster sets. Medium-voltage units >690 V grow at 5.29% CAGR as seawater RO, LNG, and green-hydrogen plants specify 6-11 kV motors. Digital twins embedded in ABB’s ACS8080 platform monitor insulation stress, bolstering reliability credentials needed for critical desalination duty. IEC 61800-5-1 revisions extend safety mandates to 35 kV, nudging end-users toward certified suppliers for high-voltage skids.

Elevated copper prices encourage OEMs to shift to silicon-carbide switchgear, shaving cable cross-section and offsetting CAPEX premiums. The broader shift favors firms with power-electronics competencies, gradually tightening barriers to entry in the variable frequency drive market.

By End-User: Oil and Gas Leads, Water Sector Accelerates

Oil and gas facilities absorbed 32.74% of 2025 spending, spanning ESP lift pumps, flare compressors, and crude pipeline boosters. Water and wastewater projects edge forward with 6.24% CAGR, propelled by 8.5 million m³/day desalination targets in Saudi Arabia and the UAE’s slant toward district-cooling. Chemicals and petrochemicals enjoy diversification tailwinds as GCC economies move downstream, whereas metals and mining depend on commodity cycles but still demand ruggedized inverters for conveyors and crushers in South Africa’s iron-ore belt.

Municipal utilities now carve out O&M funding for predictive maintenance modules embedded in drive firmware, a shift that tightens vendor-customer linkages. Hybrid renewables plus battery farms in Egypt’s Benban complex add auxiliary load profiles, broadening the variable frequency drive market use-cases beyond legacy segments.

By Application: Pumps Hold Sway, Compressors Climb

Pumps commanded a 39.55% share in 2025 variable frequency drive market share calculations and remain volume workhorses from agriculture pivots to RO membranes. Compressors gain at a 5.88% CAGR as hydrogen, nitrogen, and CO₂ value chains scale. Fans keep steady traction in high-rise HVAC yet face saturation in core GCC cities; however, new African telecom data centers resurrect fan demand for precision cooling.

Power factor penalties push end-users toward VFD-driven air compressors that modulate draw, enhancing grid stability. Meanwhile, conveyor applications pivot to regenerative drives that recuperate downhill energy in South African platinum mines, subtly widening the variable frequency drive industry footprint.

Geography Analysis

The Middle East captured 69.62% of 2025 revenue, underpinned by Vision 2030 megaprojects and steady LNG investments. Saudi Arabia tops the leaderboard, funneling USD 8.4 billion into the NEOM hydrogen complex that alone requires thousands of medium-voltage drives. The UAE sustains growth through smart-city builds and solar roof mandates, while Qatar’s LNG expansion adds compressor duty-cycles that pull in high-power inverters.

Africa, though smaller, posts a 5.68% CAGR to 2031 as industrialization gains steam. South Africa remains the anchor with mining automation, such as Kumba Iron Ore’s USD 428 million digitization plan, dependent on regenerative conveyor drives. Egypt leverages canal toll receipts to bankroll textile and food-processing clusters, demanding 7.5-37 kW drives with quick-ship lead times. Nigeria, despite forex constraints, continues ESP drive upgrades to arrest production decline, keeping oil-linked demand afloat.

Infrastructure gaps shape divergent adoption curves. GCC grids deliver 99.9% reliability, enabling sophisticated active-front-end topologies, whereas Kenya and Ghana place higher emphasis on voltage-tolerant scalar drives. Localization moves ABB’s Dammam plant, Innomotics’ Midrand assembly hub with solar-backed power, and an Egyptian PCB cluster shorten chain lengths, gradually smoothing disparity across sub-regions and broadening the addressable variable frequency drive market.

Competitive Landscape

European and Asian incumbents hold a mid-70% combined share, reflecting decades of installed base and lifecycle contracts. ABB channels USD 100 million into regional manufacturing, pairing synchronous reluctance motors with drives for IE4 compliance. Siemens fortifies with cloud analytics layered on the SINAMICS series for desalination predictive maintenance. Schneider Electric rides EcoStruxure’s open-protocol stack, winning building-automation retrofits in Dubai.

Localization mandates spawn new alliances: WEG closed on Regal Rexnord’s motor line in February 2025, expanding horsepower coverage and enabling motor-drive bundles tailored to solar trackers. Bonfiglioli’s INR 3.2 billion Tamil Nadu site extends gearmotor capacity that feeds Middle Eastern OEMs seeking compact powertrains. Eaton refreshes its PowerXL line with IE4 motor support, capturing retrofit projects spurred by energy audits.

White-space entrants pitch integrated powertrain kits or SaaS-wrapped asset health dashboards, nibbling at service revenues. Fragmented post-warranty markets in sub-Saharan Africa attract regional distributors offering multi-brand repair under one roof. Compliance with IEC 61800 norms remains the non-negotiable barrier, channeling high-voltage volumes toward full-line multinationals and reinforcing moderate concentration in the variable frequency drive market.

Middle East And Africa Variable Frequency Drive (VFD) Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

Rockwell Automation, Inc.

Danfoss A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Delta EMEA added South African irrigation case studies featuring CP2000 drives.

- February 2025: WEG completed the acquisition of Regal Rexnord’s industrial motor and generator business, deepening global powertrain capabilities.

- January 2025: Eaton launched an enhanced PowerXL family compatible with IE4 motors and multiple rotor technologies.

- October 2024: Bonfiglioli committed INR 3.2 billion to expand Indian manufacturing and a technology hub serving export markets.

Middle East And Africa Variable Frequency Drive (VFD) Market Report Scope

A variable frequency drive (VFD) is a motor controller that drives an electric motor by varying the frequency and voltage of its power supply. The VFD can also control the motor's ramp-up and ramp-down during start or stop, respectively. Although the drive controls the voltage and frequency of power supplied to the motor, it is often called speed control since the result is a motor speed adjustment. Variable frequency drives (VFD) are used in combination with electric motors to monitor the speed of motors. The study includes all such motor controllers with different power ratings varying the frequency and voltage supplied to an electric motor. The market estimations cover the revenue accrued from the sales of VFDs.

The Middle East & Africa Variable Frequency Drive (VFD) Market is segmented by End-user Industry (Oil & Gas, Chemicals & Petrochemicals, Metals & Mining, Power Generation, Water & Wastewater, HVAC, Pulp & Paper), and country.

By Drive Type

| AC Drives |

| DC Drives |

| Servo Drives |

By Power Rating

| Below 5 kW |

| 5 – 30 kW |

| 31 – 75 kW |

| Above 75 kW |

By Voltage

| Low-Voltage (≤690 V) |

| Medium-Voltage (>690 V) |

By End-User

| Oil and Gas |

| Chemicals and Petrochemicals |

| Metals and Mining |

| Power Generation |

| Water and Wastewater |

| HVAC |

| Pulp and Paper |

| Other End-User Industries |

By Application

| Pumps |

| Fans |

| Compressors |

| Conveyors |

| HVAC Systems |

| Other Applications |

By Region

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Algeria | |

| Rest of Africa |

| By Drive Type | AC Drives | |

| DC Drives | ||

| Servo Drives | ||

| By Power Rating | Below 5 kW | |

| 5 – 30 kW | ||

| 31 – 75 kW | ||

| Above 75 kW | ||

| By Voltage | Low-Voltage (≤690 V) | |

| Medium-Voltage (>690 V) | ||

| By End-User | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Metals and Mining | ||

| Power Generation | ||

| Water and Wastewater | ||

| HVAC | ||

| Pulp and Paper | ||

| Other End-User Industries | ||

| By Application | Pumps | |

| Fans | ||

| Compressors | ||

| Conveyors | ||

| HVAC Systems | ||

| Other Applications | ||

| By Region | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Algeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa variable frequency drive market?

The variable frequency drive market size reached USD 1.06 billion in 2026 and is forecast to hit USD 1.34 billion by 2031.

Which segment is expanding fastest within regional demand?

Servo drives, used in precision applications such as solar trackers, are advancing at a 5.63% CAGR through 2031.

How dominant are low-voltage drives compared with medium-voltage models?

Low-voltage units accounted for 78.25% of 2025 revenue, while medium-voltage units are growing at 5.29% CAGR thanks to desalination and hydrogen projects.

Why are variable frequency drives critical in desalination plants?

VFD-controlled pumps optimize flow and pressure, cutting energy use by 20-30% and aligning with IEC 61800-9-2 efficiency requirements.

What hampers drive adoption in sub-Saharan Africa?

A fragmented service network causes long downtime for repairs, prompting end-users to defer purchases despite energy-savings potential.

Which policy trends most support market growth?

Mandatory IE3/IE4 motor standards and localization incentives in Saudi Arabia, UAE, and Egypt underpin stable, long-term demand for advanced drives.

Page last updated on: