Microneedle Patches Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

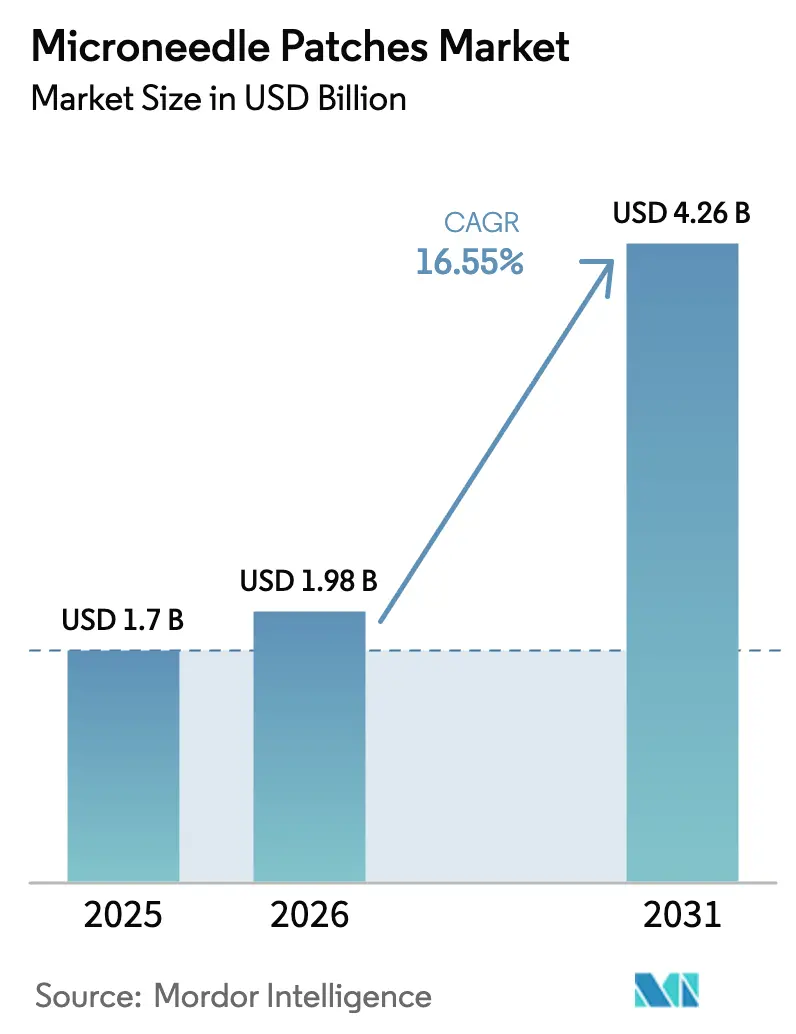

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 16.55% CAGR |

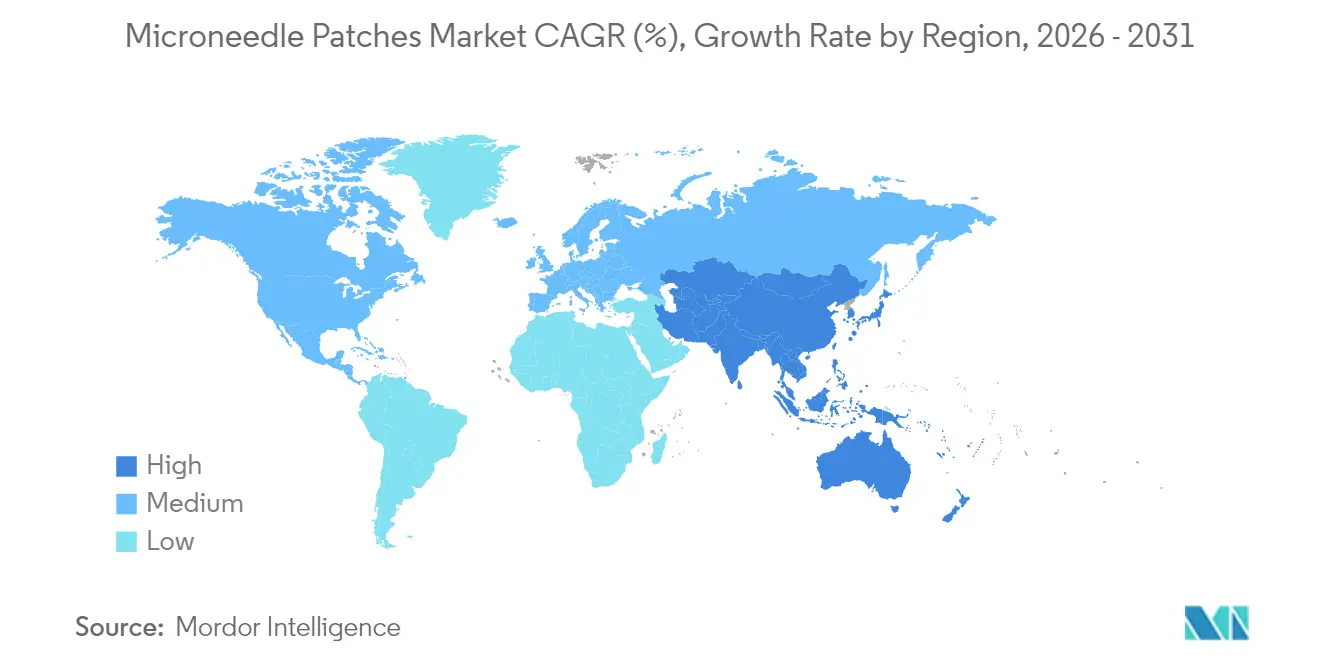

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

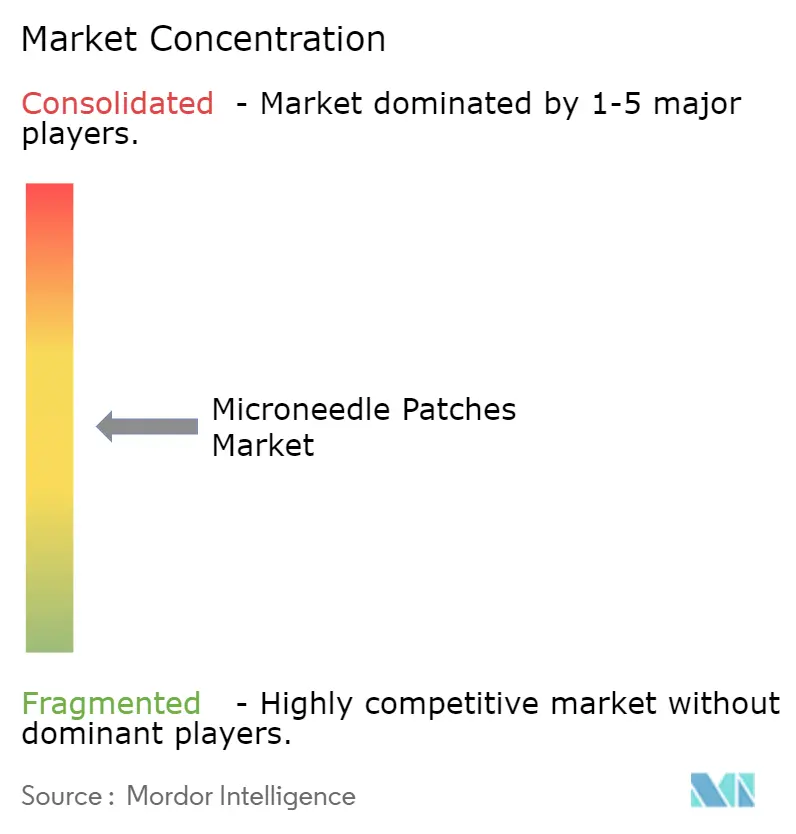

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microneedle Patches Market Analysis by Mordor Intelligence

Market Analysis

The Microneedle Patches Market size was valued at USD 1.7 billion in 2025 and estimated to grow from USD 1.98 billion in 2026 to reach USD 4.26 billion by 2031, at a CAGR of 16.55% during the forecast period (2026-2031). Rapid adoption stems from painless administration, reducing of cold-chain costs, and rising pharma partnerships that redirect injectable-biologic budgets toward transdermal delivery. Investors validated the shift when Micron Biomedical raised USD 33 million in January 2025 and Vaxxas secured AUD 90 million (~USD 61 million) in August 2025 to install semi-automated production lines, signaling growing confidence in microneedle scale-up.[1]Source: Vaxxas Pty Ltd., “Vaxxas secures ~A$90 million in funding to commercialise needle-free vaccination delivery technology,” GlobeNewswire, globenewswire.com Dissolvable platforms are gaining traction because they remove sharps waste, while vaccine developers view thermostable dried formulations as the answer to inequitable COVID-19 distribution. Policy catalysts include FDA combination-product guidance, BARDA’s USD 50 million Patch Forward Prize, and Asia-Pacific regulators that are fast-tracking software-integrated devices. Together, these forces sharpen competitive urgency among patch developers and pharma industris that aim to lock in early regulatory precedents before biosimilar entrants scale manufacturing.

Key Report Takeaways

- By product type, solid microneedles led with 52.85% microneedle patches market share in 2025; dissolvable patches are projected to expand at an 18.1% CAGR through 2031.

- By application, drug delivery accounted for 60.55% of the microneedle patches market size in 2025, while vaccine delivery is forecast to grow at a 19.25% CAGR to 2031.

- By end user, hospitals captured 43.10% revenue share in 2025; homecare settings are expected to post an 18% CAGR through 2031.

- By material, polymer-based arrays held 46.65% of 2025 revenue; hybrid composites will rise at a 16.85% CAGR to 2031.

- By geography, North America commanded 34.95% microneedle patches market share in 2025, whereas Asia-Pacific is predicted to register an 18.3% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microneedle Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for painless vaccine delivery | +3.2% | Global, with concentration in CEPI-supported low-resource regions (Sub-Saharan Africa, South Asia) | Medium term (2-4 years) |

| Diabetes prevalence boosting needle-free insulin adoption | +2.8% | North America, Europe, Asia-Pacific (China, India leading prevalence growth) | Long term (≥ 4 years) |

| Advances in dissolvable & biodegradable microneedle tech | +3.5% | Global, with R&D hubs in North America, Europe, and East Asia (Japan, South Korea) | Short term (≤ 2 years) |

| Pharma funding & partnerships accelerating commercialization | +2.6% | North America and Europe, spill-over to Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Cold-chain cost avoidance for vaccines in low-resource regions | +2.4% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Integration with on-patch biosensors enabling closed-loop therapy | +2.1% | North America, Europe, early adoption in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Painless Vaccine Delivery

Needle anxiety inhibits immunization uptake, particularly among children, a gap that microneedle patches close by offering virtually painless administration. Vaxxas’ high-density microarray patch showed that a one-sixth influenza dose elicited equivalent immunity to full intramuscular injection in more than 750 participants, validating dose-sparing potential. CEPI’s USD 4.3 million investment in thermostable mRNA patches aims to bypass freezers that hinder vaccine outreach in low-resource geographies.[2]Source: Marianne Chang, “Microneedle vaccine patches to the rescue,” Korea Biomedical Review, koreabiomed.com Public-health agencies foresee mail-delivered patches that eliminate clinic scheduling, while developers expect stronger demand curves as needle-averse populations convert into compliant users.

Diabetes Prevalence Boosting Needle-Free Insulin Adoption

According to World Heart Foundation, global diabetes will affect more than 780 million by 2045, yet adherence to daily injections remains poor. Glucose-responsive microneedle patches kept mice normoglycemic for up to 20 hours, suggesting a once-daily human regimen that removes both finger-pricks and manual dosing. Weekly GLP-1 patches featuring liraglutide achieved seven-day release in preclinical studies, hinting at relief from daily pens that currently dominate therapy. FDA combination-product review adds 18-24 months, but payers anticipate lower long-term costs by reducing hypoglycemia-related admissions.

Advances in Dissolvable & Biodegradable Microneedle Tech

Polyvinyl alcohol and sucrose matrices now deliver biologics without leaving sharps waste, cutting production costs by around 35% relative to metal arrays. Direct 3D-printing of vaccine antigens onto microneedle tips preserves potency at room temperature for 12 months, halving logistics budgets in tropical regions. Bio-inspired geometries modeled after mosquito proboscis reduce insertion force and improve self-administration among older adults.

Pharma Funding & Partnerships Accelerating Commercialization

Vaxxas, Micron Biomedical, and LTS Lohmann drew more than USD 140 million in fresh capital during 2024-2025, a sum earmarked for semi-automated production lines that leap from 5-10 million to 100 million patches a year. BARDA’s Patch Forward Prize aligned U.S. funding behind platforms that combine thermostability with rapid scale-up. Smaller firms lacking capital must therefore seek strategic alliances to avoid being out-paced in clinical evidence and factory throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain combination-product regulatory pathways | -1.8% | Global, most acute in Asia-Pacific and Latin America lacking FDA/EMA equivalents | Medium term (2-4 years) |

| High manufacturing scale-up costs & yield losses | -1.4% | Global, with highest impact in North America and Europe due to GMP requirements | Short term (≤ 2 years) |

| Moisture-driven shelf-life limits in tropical climates | -0.9% | Sub-Saharan Africa, South Asia, Southeast Asia, Latin America | Medium term (2-4 years) |

| Low drug-loading capacity for high-dose biologics | -0.7% | Global, affecting oncology and autoimmune applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uncertain Combination-Product Regulatory Pathways

FDA demands coordination between drug and device centers, adding 18-36 months to review cycles, and Europe’s evolving frameworks trigger pathway ambiguity that pushes many developers to prioritize U.S. filings first. Asia-Pacific regulators are only now drafting equivalent rules, prolonging market entry where demand is growing fastest.

High Manufacturing Scale-Up Costs & Yield Losses

Commercial plants require USD 50-100 million in capital, mainly for precision molding and lyophilization. Vaxxas earmarked most of its August 2025 raise for semi-automated lines, underscoring how manual assembly remains the sector’s bottleneck. Yield losses from needle breakage and demolding further inflate cost of goods, challenging new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dissolvable Patches Narrow the Gap

Solid microneedles captured 52.85% microneedle patches market share in 2025 on the back of mature stainless-steel tooling that ensures consistent 500-800 µm penetration depths. Dissolvable arrays are set for 18.1% CAGR until 2031 as polyvinyl alcohol and sucrose matrices remove sharps disposal, a decisive benefit in community health settings. Hollow formats deliver up to 200 µL-suitable for biologics-with clogging risks that keep them niche. Hydrogel-forming needles enable 24-48 hour analgesic release, adding chronic-pain appeal.

Across 2026-2031, dissolvable technologies should erode metal incumbency as 3D-printed arrays match drug-loading of hollow needles while cutting costs by roughly 35%. Cosmetic offshoots, such as Nissha’s lavender-scented skincare patches debuted at Cosme Tech Tokyo in January 2025, demonstrate adjacent revenue channels. [3]Source: Nissha Co., Ltd., “Nissha to Exhibit Dissolving Microneedle Patches for Cosmetics,” nissha.com . Personalized geometry-print-to-order within 48 hours-may become a differentiator for high-dose oncology applications.

By Application: Vaccines Sprint Ahead

Drug delivery retained 60.55% of 2025 revenue, supported by insulin, hormone, and pain therapies. Vaccine delivery, however, is primed for 19.25% CAGR to 2031, driven by dried formulations that travel without freezers and the public-health goal of postal self-administration. Micron Biomedical’s infant polio-rotavirus patch entered Phase 2 with Gates Foundation backing, spotlighting pediatric demand in low-resource regions.

Oncology programs explore localized microneedle chemotherapy where paclitaxel or doxorubicin is deposited directly over tumor margins, reducing systemic toxicity while exploiting microneedle precision. Diagnostics also surface as a growth lane: silicon electrodes embedded in patches have already measured interstitial glucose with sub-millimolar accuracy, foreshadowing biomarker panels that could displace conventional blood draws.

By End User: Homecare Moves Center Stage

Hospitals represented 43.10% of 2025 unit demand because physicians controlled oncology and pediatric vaccinations. Homecare adoption will accelerate at 18% CAGR through 2031 as user-friendly applicators gain approval and OTC regulation matures. Survey data show patient acceptance climbs sharply when patches come pre-loaded and require no activation steps, alleviating dexterity concerns among older adults. Health-system economics further propel the shift: each self-administered patch avoids USD 50-100 clinic costs and releases capacity for higher acuity services.

Specialty clinics still drive dermatology and chronic-pain prescriptions, but their share should shrink as e-commerce pharmacy channels distribute patches directly to consumers under pharmacist guidance. To succeed, manufacturers must validate human-factors usability that 95% of intended users can correctly apply on first attempt, a requirement that adds 12-18 months to FDA timelines.

By Material: Hybrid Composites Bridge Performance and Waste

Polymer arrays held 46.65% revenue in 2025 on cost advantages and biodegradability. Composite matrices that embed ceramic or graphene nanoparticles will expand at a 16.85% CAGR, offering metal-like strength while dissolving in tissue. Metal needles retain an edge for precise dermal targeting and deeper penetration but face regulatory glare over sharps disposal. Silicon remains indispensable for biosensor integration, despite brittleness that limits reusability.

R&D efforts target hybrid polymer-ceramic systems delivering double the fracture resistance of pure polymers yet dissolving within hours to sidestep biohazard disposal. Alginate and chitosan hydrogels, now around 12% of material demand, illustrate growth in cosmetic and wound-healing lines where moisture absorption enhances delivery.

Geography Analysis

North America dominated the microneedle patches market with 34.95% share in 2025, underpinned by clear FDA guidance and BARDA grants that derisked manufacturing investments. U.S. demand benefits from 37 million diabetes patients and reimbursement codes that already cover transdermal systems. Canada aligns regulatory pathways with FDA, trimming launches by up to a year, while Mexico’s expanding medtech assembly sector entices contract manufacturing though domestic uptake lags due to limited coverage.

Asia-Pacific will post the fastest 18.3% CAGR through 2031 as China fast-tracks NMPA reviews, Japan’s PMDA issues transdermal guidelines, and South Korea’s 2024 Digital Medical Products Act streamlines software-integrated devices. China’s 140 million diabetics create the world’s largest insulin-patch addressable population, and tariff incentives for local production tilt competitiveness toward domestic suppliers. Japan’s super-aged society values devices that cut clinic visits, and expedited pathways reduce approval lead times to roughly 15 months. South Korea’s regulator eliminates duplicate software tests for ISO-13485-compliant code, shortening cycles for biosensor patches. Europe’s EMA convergence is reducing approval uncertainty; Germany, the United Kingdom, and France collectively contribute 60% of regional demand. Germany’s sickness funds reimburse patches when studies demonstrate non-inferiority or better than injectables, a hurdle that early vaccine patches already meet. UK post-Brexit alignment remains steady but diverging device codes after 2027 could fragment market entry. Middle East and Africa face humidity that degrades polymer arrays, capping growth until more moisture-resistant composites emerge. South America’s expansion clusters in Brazil and Argentina, but 20-30% device import duties inflate patch prices 40-60% above U.S. levels, constraining public-sector tenders.

Competitive Landscape

The microneedle patches market is moderately fragmented: the top five players—Vaxxas, Micron Biomedical, LTS Lohmann, Zosano Pharma, and Kindeva—controlled a sizable revenue pool in 2024. Competitive thrust centers on first-in-class regulatory wins and factory scale. LTS Lohmann secured the first FDA nod for a dissolvable biologic patch (UDENYCA OBI) in December 2024, setting a benchmark likely to slow biosimilar rivals by 18-24 months. Vaxxas’ USD 61 million raise earmarks 100 million-patch annual capacity, a tenfold leap that reinforces its moat.

Partnership dynamics intensify as SK biosciences, CEPI, and Wellcome fund rapid trial execution, effectively aligning vaccine IP with patch hardware. Emerging disruptors include ArrayPatch, whose 3D-printed DerMap aims at onychomycosis where topical creams underperform, and Raphas, which cut electroporation voltage from 90 V to 25-50 V to improve DNA-vaccine tolerability. Universities exploit print-to-order flexibility to demonstrate personalized oncology arrays within 48 hours, hinting at bespoke therapies that incumbents may struggle to match quickly.

Strategic positioning now revolves around three levers: thermostability (critical for global vaccine bids), biosensor integration (necessary for closed-loop diabetes and cardiovascular devices), and fully automated production that slashes cost per patch. Players that master two of the three will likely command premium pricing and partnership attention; laggards risk commoditization once regulatory guidance stabilizes and contract manufacturers enter.

Microneedle Patches Industry Leaders

LTS Lohmann Therapie-Systeme AG

Micron Biomedical, Inc.

Kindeva

VAXXAS

Zosano Pharma Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vaxxas secured AUD 90 million (~USD 61 million) to build semi-automated lines targeting 100 million patches per year.

- January 2025: Micron Biomedical raised USD 33 million Series A to advance pediatric vaccine patches and scale manufacturing.

- January 2025: BARDA awarded USD 50 million Patch Forward Prize to LTS Lohmann and BioNet for mRNA vaccine patches.

- January 2025: University of Queensland and Vaxxas received USD 2 million to progress mRNA patch thermostability studies.

Global Microneedle Patches Market Report Scope

The Global Microneedle Patches Market Report is Segmented by Product Type (Solid, Hollow, Dissolving, Coated, Hydrogel-forming, Combination/Smart Platforms), Application (Drug Delivery, (Pain Management, Oncology Drugs, Insulin, Others), Vaccine Delivery, Cosmetic/Dermatology, Diagnostics), End User (Hospitals, Specialty Clinics, Homecare, Others), Material (Polymer, Metal, Silicon, Hybrid/Composite, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America).

| Solid Microneedles |

| Hollow Microneedles |

| Dissolving Microneedles |

| Coated Microneedles |

| Hydrogel-forming Microneedles |

| Combination / Smart Patch Platforms |

| Drug Delivery | Pain Management |

| Oncology Drugs | |

| Insulin Delivery | |

| Others | |

| Vaccine Delivery | |

| Cosmetic & Dermatology | |

| Diagnostics & Biosensing |

| Hospitals |

| Specialty Clinics |

| Home-care Settings |

| Others |

| Polymer-based |

| Metal-based |

| Silicon-based |

| Hybrid & Composite Materials |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Solid Microneedles | |

| Hollow Microneedles | ||

| Dissolving Microneedles | ||

| Coated Microneedles | ||

| Hydrogel-forming Microneedles | ||

| Combination / Smart Patch Platforms | ||

| By Application | Drug Delivery | Pain Management |

| Oncology Drugs | ||

| Insulin Delivery | ||

| Others | ||

| Vaccine Delivery | ||

| Cosmetic & Dermatology | ||

| Diagnostics & Biosensing | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home-care Settings | ||

| Others | ||

| By Material | Polymer-based | |

| Metal-based | ||

| Silicon-based | ||

| Hybrid & Composite Materials | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the microneedle patches market?

The microneedle patches market size is USD 1.98 billion in 2026

How fast the market is expected to grow?

The market is projected to expand at a 16.55% CAGR, reaching USD 4.26 billion by 2031.

Which region leads adoption of microneedle patches?

North America holds 34.95% market share due to early FDA clearances and reimbursement coverage

Which product type has the highest market share?

Solid microneedles captured 52.85% microneedle patches market share

Page last updated on: