Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.84 Billion |

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

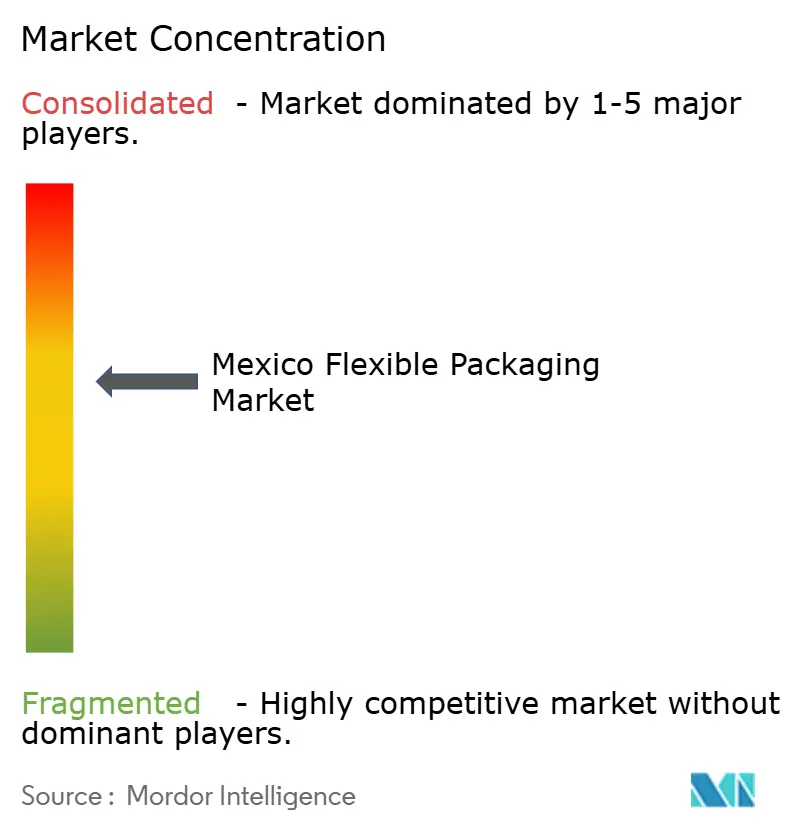

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Flexible Packaging Market Analysis by Mordor Intelligence

The Mexico flexible packaging market size is expected to grow from USD 3.84 billion in 2025 to USD 4.02 billion in 2026 and is forecast to reach USD 5.06 billion by 2031 at 4.69% CAGR over 2026-2031. Robust near-shoring of fast-moving consumer-goods (FMCG) lines from Asia, e-commerce parcel growth that demands impact-resistant formats, and rising disposable incomes in major cities collectively propel the Mexico flexible packaging market. Investors gain additional certainty from the United States-Mexico-Canada Agreement (USMCA), which secures duty-free access to North America’s integrated supply chain and encourages capital allocation toward high-barrier co-extrusion, retort laminates, and mono-material innovations. Migration of domestic brewers toward export-oriented models also enlarges demand for oxygen- and light-barrier films that protect cerveza shipped to the United States and Europe, while premium pet-food processors push stand-up-pouch lines that deliver portion convenience and brand visibility. Growing sustainability mandates, particularly in Mexico City and other Tier-1 municipalities, accelerate investments in post-consumer resin (PCR) incorporation and recyclable paper-based structures as brand owners attempt to curb future packaging levies.

Key Report Takeaways

- By material type, plastics captured 47.10% of Mexico flexible packaging market share in 2025, while paper is projected to register the fastest 5.62% CAGR to 2031.

- By product type, pouches accounted for 35.10% share of the Mexico flexible packaging market size in 2025; bags and sachets are expected to expand at a 5.38% CAGR through 2031.

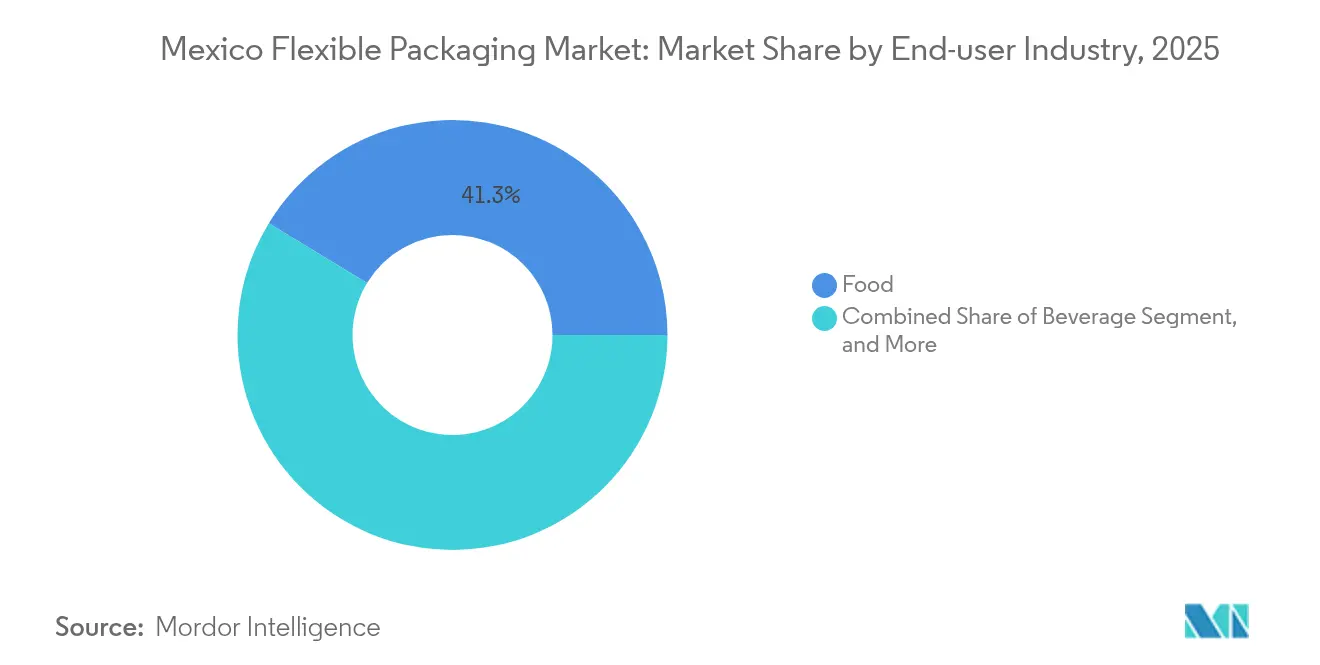

- By end-user industry, food dominated with 41.30% revenue share in 2025, whereas beverage applications are forecast to grow at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for packaged convenience food supported by the 13% rise in national food output recorded by INEGI in 2024 | +1.2% | Urban centers including Mexico City, Guadalajara, and Monterrey | Medium term (2-4 years) |

| Surge in e-commerce-ready primary packaging as parcel volume tops 700 million annual shipments | +0.8% | Nationwide, with pilot testing in Mexico City’s last-mile networks | Short term (≤ 2 years) |

| Growth of pet-food premiumization fueling stand-up pouches amid ADM’s USD 39 million wet food plant commissioning | +0.6% | Large metropolitan areas with high pet ownership | Medium term (2-4 years) |

| Near-shoring of FMCG production to Mexico under USMCA-linked tax incentives | +1.1% | Border states and central industrial corridors | Long term (≥ 4 years) |

| Cerveza exports requiring high-barrier retort laminates for trans-oceanic shipping | +0.4% | Brewer-dense regions such as Nuevo León and Jalisco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Packaged Convenience Food

Urban lifestyles shorten meal-preparation time and boost sales of ready-to-eat noodles, sauces, and single-serve dairy, directly lifting film-consumption volumes across the Mexico flexible packaging market.[2]Instituto Nacional de Estadística y Geografía, “Food Production Index 2024,” inegi.org.mx Processors specify multilayer polyethylene (PE)/ethylene-vinyl-alcohol (EVOH)/PE structures that combine moisture, oxygen, and aromatic barriers, thereby extending shelf life without cold-chain additions. Equipment suppliers report double-digit order growth for form-fill-seal lines adapted to 75-micron asymmetric laminates that withstand retort sterilization. Converter preference for solvent-free lamination reduces migration risk and accelerates line speeds, improving uptime in high-throughput snack plants. Brand owners simultaneously roll out 90-gram portion packs that meet calorie-control guidelines and support take-along convenience for commuting consumers.

Surge in E-commerce-Ready Primary Packaging

Rapid expansion of e-commerce fueled by omnichannel grocery adoption and food-delivery apps intensifies performance standards for flexible pouches shipped via third-party couriers. Converters integrate puncture-resistant nylon layers and reinforce gusset seals to survive conveyor sorters and urban motorcycle delivery. Optical-character-recognition-ready print surfaces enable precise package tracking, reducing lost parcels and customer complaints. Single-material polyethylene mailers with easy-open laser scoring replace mixed-material poly mailers banned in Mexico City’s single-use plastics ordinance.[3]Secretaria del Medio Ambiente (SEDEMA), “Plastic Ban Enforcement Report 2024,” sedema.cdmx.gob.mx Sustainability is addressed through PCR-containing co-extrusions that hit 30% recycled content, a threshold aligned with retailer procurement policies. As platforms refuse shipments that lack end-of-life labeling, demand swings sharply toward pouches carrying How2Recycle-equivalent marks.

Growth of Pet-Food Premiumization Fueling Stand-Up Pouches

Households continue humanization of pets, shifting toward formulations that include human-grade chicken, grain-free recipes, and functional additives, each requiring high oxygen-barrier packaging. ADM’s wet pet-food plant in Morelos sources 3-layer retortable structures that reduce cook cycle time and preserve nutrient integrity. Brand managers embrace transparent windows to showcase texture, but antioxidants in meat broths still demand EVOH layers for peroxide suppression. Mono-material polypropylene (PP) pouches with peelable seals are piloting in premium cat treats, promising recyclability without sacrificing shelf stability. Coupon-enabled QR codes printed in high-definition rotogravure drive consumer engagement and build loyalty. Pet-store chains report that stand-up formats occupy 15% less shelf depth than cans, allowing broader SKU assortments in constrained urban retail.

Near-Shoring of FMCG Production to Mexico

The proportion of U.S. consumer-goods imports sourced from Mexico climbed to 15.8% in 2024 as brand owners replaced Asian suppliers to cut freight time, mitigate geopolitical risk, and qualify for USMCA origin rules. Relocated factories typically demand bilingual artwork, FDA-compliant resin declarations, and color standards that match U.S. planogram guidelines, stimulating orders for digital-printing presses with rapid changeover. The federal Plan Mexico decree grants accelerated depreciation of up to 91% for capital expenditure on converting equipment, improving payback periods for new solvent-less laminators. Cluster development in Nuevo León’s Lithium Valley accelerates supply of high-barrier films needed for snack exports, while Guadalajara’s electronics assembly zone increases consumption of static-shielding flexible laminates. Logistics savings—five days faster than trans-Pacific routes underscore the value proposition for multinational packaging buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited municipal collection of flexible films, with recycling rates still at 24% of plastic waste despite 97% overall collection | -0.7% | National shortfall, starkest in municipalities under 100,000 inhabitants | Long term (≥ 4 years) |

| Volatile polymer-resin pricing linked to U.S. Gulf Coast (USGC) feedstocks and a 25% U.S. tariff on resin imports | -0.9% | Country-wide exposure, highest among PE-dependent snack-film extruders | Short term (≤ 2 years) |

| Circular-economy taxes proposed in Congress that would levy MXN 1.50/kg on virgin resin packaging | -0.3% | Nationwide, pending senate vote | Medium term (2-4 years) |

| Brand-owner shift to refill formats in premium cosmetics, reducing demand for single-use sachets | -0.2% | Tier-1 cities with boutique retail channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Municipal Collection of Flexible Films

Mexico’s legacy waste network prioritizes rigid PET bottle capture, leaving thin-film recovery markedly under-invested. Municipal material-recovery facilities often lack optical sorters and air-classification decks capable of isolating LDPE and PP films, forcing converters to downcycle trim scrap rather than harvest PCR from curbside streams. Although SEDEMA reports that plastic recycling businesses in Mexico City almost tripled between 2022 and 2024, none process multi-layer films at commercial scale. Brands risk missing 2025 voluntary recyclability goals, prompting contingency evaluations of paper solutions for dry snacks. Absent infrastructure, state governments defer landfill-tax incentives that could underwrite closed-loop investments. Retailers respond by piloting in-store take-back bins, but volumes remain insufficient to justify dedicated wash-lines.

Volatile Polymer Resin Pricing Linked to USGC Feedstocks

Ethylene and propylene spot prices on the USGC spiked 17% quarter-on-quarter in early 2025 following weather-related cracker outages. Simultaneously, a 25% U.S. tariff on North American resin imports compressed converter margins on export-linked film grades. Smaller film plants without financial hedging options postpone resin purchases, leading to intermittent production stoppages and extended lead times for food processors. Currency volatility MXN appreciating 6% against USD during 2025 exacerbates raw-material planning complexities. Compounders attempt cost pass-through, yet snack-brands lock annual bids, forcing operational-efficiency drives to offset resin hikes. Larger multinationals leverage forward-buy programs and integration with resin suppliers to stabilize input costs

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Retain Command Despite Accelerating Paper Adoption

Plastics remained dominant in 2025, when polyethylene, polypropylene, and specialized EVOH accounted for 47.10% of Mexico flexible packaging market share, primarily because multilayer structures provide unrivaled moisture and aroma barriers for snack and dairy exports. Paper substrates are posting the swiftest progress, growing at a 5.62% CAGR as retailers react to urban plastic-bag bans and as quick-service chains test grease-resistant, fluorine-free wraps. Mexico flexible packaging market size for paper-based formats is projected to rise steadily as converters install curtain-coating lines that apply water-based dispersions, allowing paper to handle frozen-food moisture without delamination. Aluminum foil remains indispensable for pharmaceutical blister overwraps and premium confectionery, but sustainability scrutiny spurs metallized-oxide PET adoption that mimics foil brightness while easing material separation at recyclers.

Heightened demand for mono-material solutions also influences resin selection, pushing converters toward high-density polyethylene (HDPE) that meets retailer recyclability targets without sacrificing seal integrity. Meanwhile, biaxially-oriented polypropylene (BOPP) continues to dominate salty-snack front panels for its clarity and gloss, with specialty matte finishes gaining favor among premium tortilla chip brands. Paper’s rise is aided by Mexico’s mature pulp infrastructure in Veracruz and Sonora, which supplies FSC-certified kraft for carrier-bag and flour-sack applications. The Mexico flexible packaging industry simultaneously experiments with bio-based PE derived from sugarcane ethanol, yet high feedstock premiums limit immediate scale versus fossil-based polymers. Material decisions increasingly hinge on life-cycle-assessment metrics embedded in retailer scorecards, amplifying demand for third-party certified PCR content across both plastic and paper substrates.

By Product Type: Pouches Lead While Bags and Sachets Accelerate

Pouches secured 35.10% of the Mexico flexible packaging market in 2025 as stand-up structures with laser-scored easy-open tops became standard in pet treats, infant purées, and functional beverages. Zipper and slider closures enhance resealability, supporting on-the-go usage and food-waste reduction. Flat-bottom pouches gain traction in premium coffee, where elevated shelf-presentation commands higher retail margins. Bags and sachets, though traditionally seen as entry-level formats, exhibit a 5.38% CAGR thanks to portion-control packs that introduce national brands into rural tiendas. Sachet proliferation also addresses affordability constraints by allowing shampoo and seasoning brands to offer MXN-5 price points.

Shrink sleeves and stretch labels form a specialized but influential sub-segment. Breweries adopt full-body sleeves to accommodate rapid SKU proliferation while maintaining supply-chain efficiency, although recyclability challenges persist because PET bottles require sleeve removal. High-barrier films for liquid concentrates integrate spout fitments compatible with at-home dispensers, supporting the emerging refill economy. Machinery investments prioritize high-speed pouch-making lines with servo-driven web tension control that handle thinner gauges without deformation. Mexico flexible packaging market size linked to e-commerce mailers grows as 50-micron co-extruded PE films replace bubble envelopes, improving cube utilization and cutting freight costs for fashion retailers.

By End-User Industry: Food Dominant yet Beverage Delivers the Fastest Upside

Food processors consumed 41.30% of all flexible packs in 2025, driven by robust frozen-snack exports and rising domestic demand for chilled ready-meals among dual-income households. High-barrier vacuum films extend shelf life for meat and seafood, lowering retail shrink and reinforcing plastic’s value proposition amid environmental scrutiny. Dairy brands adopt 5-layer yogurt lids that balance oxygen permeability and aluminum-free recyclability. Mexico flexible packaging market size dedicated to beverage applications is expanding at a 5.12% CAGR, energized by craft-brew concentrate pouches and electrolyte beverage sachets that travel efficiently through cross-border e-commerce channels.

Beer exporters, pressured by U.S. aluminum-can tariffs, innovate with bag-in-box beer syrup destined for U.S. microbreweries, creating niche demand for 5-gallon barrier liners. Pharmaceutical demand remains stable, with medical-device sterilization pouches requiring Tyvek-film laminates that withstand ethylene-oxide cycles. Household and personal-care brands embrace film-based refill bags for detergents and liquid hand soaps, capturing consumer loyalty through reduced unit-cost economics. The Mexico flexible packaging industry also supplies the electronics sector with static-dissipative pouches as near-shoring of assembly plants accelerates in border states, underscoring the market’s cross-industry diversification.

Geography Analysis

Northern border states Baja California, Sonora, and Nuevo León anchor 41.60% of the Mexico flexible packaging market value because maquiladora clusters funnel millions of snack and beverage units into U.S. supermarkets with 48-hour trucking lead times. Central highlands, led by Mexico City and the Bajío, contribute 38.30%, reflecting dense domestic consumption and omnichannel fulfillment centers. The Interoceanic Corridor aims to cut coast-to-coast logistics by 40%; converters eye Oaxaca and Veracruz for future plant sites to serve emerging seafood-processing zones. Regulatory heterogeneity shapes demand patterns: Mexico City’s strict single-use bans push paper trials, whereas Chihuahua’s permissive stance favors cost-oriented LDPE bags. Climate variation also dictates barrier specs; humid Gulf Coast facilities demand low-WVTR films, while arid northern exporters prioritize oxygen barriers for long-haul shipments.

Regulatory Landscape

Flexible packaging placed on the Mexican market is governed by mandatory Normas Oficiales Mexicanas (NOMs) covering safety, technical specifications, and labeling, with food-contact oversight linked to COFEPRIS. A core compliance anchor for brand owners and converters is NOM-051-SCFI/SSA1-2010 for pre-packaged food and non-alcoholic beverage labeling, which shapes artwork, warnings, and information placement across flexible formats used in food and beverage.

In 2026, the General Law of Circular Economy (Ley General de Economia Circular) introduced a federal framework around circularity, including extended producer responsibility, and triggered a harmonization process for state and municipal rules that already vary (for example, stricter single-use controls in Mexico City). With implementing regulations and related standards still developing, converters and importers must maintain NOM conformity at the pack level while tracking how new circular-economy requirements affect recyclability claims, traceability expectations, and material-selection decisions, such as mono-material designs and PCR incorporation.

Value Chain Analysis

The Mexico flexible packaging value chain starts with resin and substrate supply (PE, PP, specialty barrier resins such as EVOH, paper, and limited foil use), followed by film extrusion and orientation, adhesive or coating and lamination (increasingly solvent-free), printing (flexo, gravure, and growing digital for short runs), pouch and bag converting, and distribution to food, beverage, personal care, pharmaceutical, and industrial users. Downstream, the recovery loop remains uneven for flexible films. Established collection and recycling economics are stronger for materials such as PET, aluminum, and cardboard than for multi-layer flexible structures, which constrains both the volume and consistency of post-consumer feedstock for high-spec flexible applications.

Industry bodies such as ANIPAC, AMEE, and Inboplast support training, technical alignment, and compliance readiness as circularity requirements tighten. Converters and brand owners coordinate on qualification, testing, and certification to meet retailer and export specifications. The January 2026 General Law on Circular Economy shifts the chain toward design-for-recycling, EPR-linked documentation, and more explicit traceability, increasing the role of certified recyclers, take-back pilots, and waste-management partners alongside traditional raw-material suppliers and converters.

Competitive Landscape

Top five suppliers Amcor, Sealed Air, Huhtamaki, Constantia Flexibles, and SigmaQ command roughly 48% of Mexico flexible packaging market revenue, leaving mid-tier converters to compete on agility and localized service. Amcor’s merger with Berry Global targets USD 650 million in synergies and elevates its ability to supply retort pouches and medical barrier films.[1]Amcor plc, “Amcor Completes Combination with Berry Global,” amcor.comSigmaQ invests in digital printing to service craft-beer exporters seeking small-batch runs, while Grupo Gondi leverages integrated paper mills to capture rising demand for paper-based barrier bags. Technology investments focus on solvent-less laminators and 9-color CI-flexo presses that cut setup waste by 30%. Sustainability differentiation intensifies: Huhtamaki’s mono-material PP pouch launched in 2024 now contains 35% PCR and meets Mexico City’s recycling labeling standards. Meanwhile, niche entrants experiment with blockchain-enabled track-and-trace to document recycled-content provenance.

Mexico Flexible Packaging Industry Leaders

Amcor PLC

Sealed Air Corporation

Innovia Films

Constantia Flexibles Holding GmbH

Uflex Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An actionable opportunity is scalable, recyclable flexible structures that still meet barrier performance and e-commerce durability needs. Mexico's limited municipal recovery for multi-layer films creates a practical gap for applications where food, pet food, and export-oriented beverage demand high barrier performance.

The 2026 General Law on Circular Economy anchors a move toward EPR and circular design, which pushes brand owners and converters to redesign packs, document material flows, and qualify recycled or recyclable alternatives for defensible claims across jurisdictions such as Mexico City and export channels under USMCA-linked requirements. Investment and capability opportunities are clustering around three areas already visible in current market actions: (i) capacity and localization tied to North American packaging demand, illustrated by SIGs announced expansion of its Querétaro plant to scale output for packaged products; (ii) automation and smarter converting and printing that support near-shored FMCG production, shorter lead times, and rapid SKU changeovers, highlighted by the strong industry focus at EXPO PACK Mexico 2026; and (iii) circular-economy enabling services and materials, including PCR qualification, mono-material retortable structures, and labeling or traceability compliance, which help close the gap between performance requirements and end-of-life constraints for flexible formats.

Recent Industry Developments

- June 2026: SIG announced an expansion plan for its Querétaro plant to increase output capacity, with project phases starting in 2026 and a longer-term ramp to higher volumes. The move strengthens local supply for packaged-product formats and supports faster replenishment for North American demand served from Mexico.

- April 2025: Amcor completed its all-stock combination with Berry Global, targeting USD 650 million in synergies. The integration broadens Amcor's scale across flexible packaging capabilities, improving its ability to serve high-barrier and specialty applications for food, beverage, and healthcare customers operating in Mexico.

- June 2024: Huhtamaki advanced its mono-material PP pouch platform launched in 2024, positioning it for customers prioritizing recyclability-aligned designs in urban markets such as Mexico City. The product shift reinforces competitive differentiation around material simplification while maintaining performance requirements for pouch-led applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated in Mexico from flexible packaging that uses nonrigid materials, sold as finished packaging formats for consumer and industrial packing needs. It covers common flexible formats such as films, wraps, bags, and pouches, used across food, personal care, and pharma packing needs.

Scope exclusions: Excludes rigid packaging formats such as bottles, jars, and cans, and any non-packaging flexible materials that are not sold as packaging.

Segmentation Overview

- By Material Type

- Plastics

- Polyethylene (PE)

- Biaxially-Oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Polyvinyl Chloride (PVC)

- Ethylene-Vinyl Alcohol (EVOH)

- Paper

- Aluminum Foil

- Plastics

- By Product Type

- Pouches

- Bags and Sachets

- Films and Wraps

- Shrink Sleeves and Labels

- Other Formats

- By End-user Industry

- Food

- Frozen Food

- Dairy Products

- Fruits and Vegetables

- Meat, Poultry and Seafood

- Baked Goods and Snacks

- Confectionery

- Other Food

- Beverage

- Pharmaceutical and Medical

- Household and Personal Care

- Industrial and Chemical

- Food

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand base and pricing direction before the model was built, because flexible packaging spans many end uses and material chains in Mexico. We referenced public sources such as Mexico trade and customs statistics, INEGI industrial output series, central bank macro indicators, and environment and waste-management publications that discuss packaging and recycling rules.

To anchor supply and cost signals, we also reviewed material and packaging updates from industry associations, peer-reviewed papers on flexible structures and barrier performance, and public company filings and investor presentations from packaging and resin-linked participants operating in Mexico. Where needed, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export views were used to cross-check capacity moves and trade flows. These examples are not exhaustive, and many other public and paid sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what desk research could not show clearly, especially mix shifts across formats, end uses, and material structures, and the pace of price pass-through in Mexico. We spoke with a spread of converters, raw material participants, distributors, and large buyers across food, personal care, and pharma, and then rechecked key assumptions when responses showed wide variance across the country.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | |

| Mid tier: 47% | Functional/Unit leaders: 40% | |

| Smaller Players: 14% | Managers: 48% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where Mexico packaging demand indicators are converted into a flexible-pack share using format adoption signals, end-use packaging intensity, and observed shifts toward pouches, bags, and flexible films. To keep the totals realistic, the output is corroborated with selective bottom-up checks, such as sampled converter revenue ranges, implied volumes multiplied by observed average selling prices, and channel checks on high-rotation flexible formats.

Key model inputs include flexible packaging penetration in food and beverage categories, pouch and sachet usage trends, resin and aluminum foil price direction that affects pricing, trade flow changes for packaging films and laminates, and near-shoring linked manufacturing growth that increases packaged-goods output. For forecasting, scenario analysis was used around price pass-through and mix, supported by interview-based expectations on sustainability-linked structure changes and the timing of downgauging or mono-material moves. When bottom-up evidence was incomplete for smaller informal activity, the gap was handled through conservative scaling based on demand-side consumption signals rather than assuming full reporting coverage.

Data Validation & Update Cycle

Outputs are checked using multiple steps so that unusual jumps in implied volume, pricing, or share are caught early and corrected. We compare the modeled totals against independent signals like packaging output trends, trade balance shifts for key flexible inputs, and material price movements, and then variances are discussed in an internal review before sign-off.

If primary inputs disagree by respondent type or by end-use exposure, follow-up calls are triggered and the assumptions are tightened until the spread is explainable. The report is refreshed annually, and interim updates are made when major events materially change demand or pricing in Mexico. Before delivery, a final update pass is completed so clients receive the most current view based on the latest available inputs.

Mordor Intelligence's Mexico Flexible Packaging Market Size Versus Other Published Estimates

Published market numbers for Mexico flexible packaging can look far apart because each publisher sets its own rules on what counts as flexible packaging revenue and which years are treated as the current base. Differences also show up when one model leans more on material shipments and another leans more on end-use demand, which changes how mix and pricing are carried forward.

The main gap comes from how multilayer and structure-specific packaging is treated, where Mordor Intelligence counts flexible packaging only when it is sold as finished flexible formats in Mexico (films, wraps, bags, and pouches) and avoids mixing in broader multilayer-only lenses that can overlap with adjacent packaging value pools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.02 B (2026) | |

| Industry Research Publisher A | USD 4.52 B (2025) | Uses a different base year and a longer forecast window, and its scope description suggests broader inclusion of flexible structures and material buckets, which can lift the starting value versus a format-led count. |

| Specialty Packaging Portal B | USD 10.00 B (2024) | Tracks the multilayer flexible packaging segment, which is a narrower structure definition but is often measured with different value boundaries and can overlap with other packaging pools, making it not directly comparable to a finished-format flexible packaging market total. |

When the year and scope are aligned, most of the spread becomes explainable through what is included, how pricing is rolled forward, and whether the estimate is format-led or structure-led. By keeping the demand pool tied to finished flexible formats and then cross-checking with supply and trade signals, the estimate stays traceable to inputs that can be repeated and revalidated during updates.

Key Questions Answered in the Report

How large is the Mexico flexible packaging market in 2026?

The market stands at USD 4.02 billion and is projected to reach USD 5.06 billion by 2031.

What is the forecast CAGR for flexible packaging demand in Mexico?

An annual growth rate of 4.69% is expected from 2026 to 2031.

Which product format dominates sales?

Stand-up and flat-bottom pouches account for 35.10% of 2025 revenue thanks to convenience and visual appeal.

Which material is growing fastest?

Paper-based flexible packs are expanding at a 5.62% CAGR as brands seek recyclable solutions.

What region of Mexico consumes the most flexible packaging?

Northern border states lead with 41.60% value share because maquiladora plants serve U.S. retailers.

How will near-shoring affect local converters?

Relocated FMCG lines under USMCA rules will lift demand for high-barrier films that comply with both Mexican and U.S. regulations, supporting steady capacity additions through 2031.

Page last updated on: