Meibomian Gland Dysfunction Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

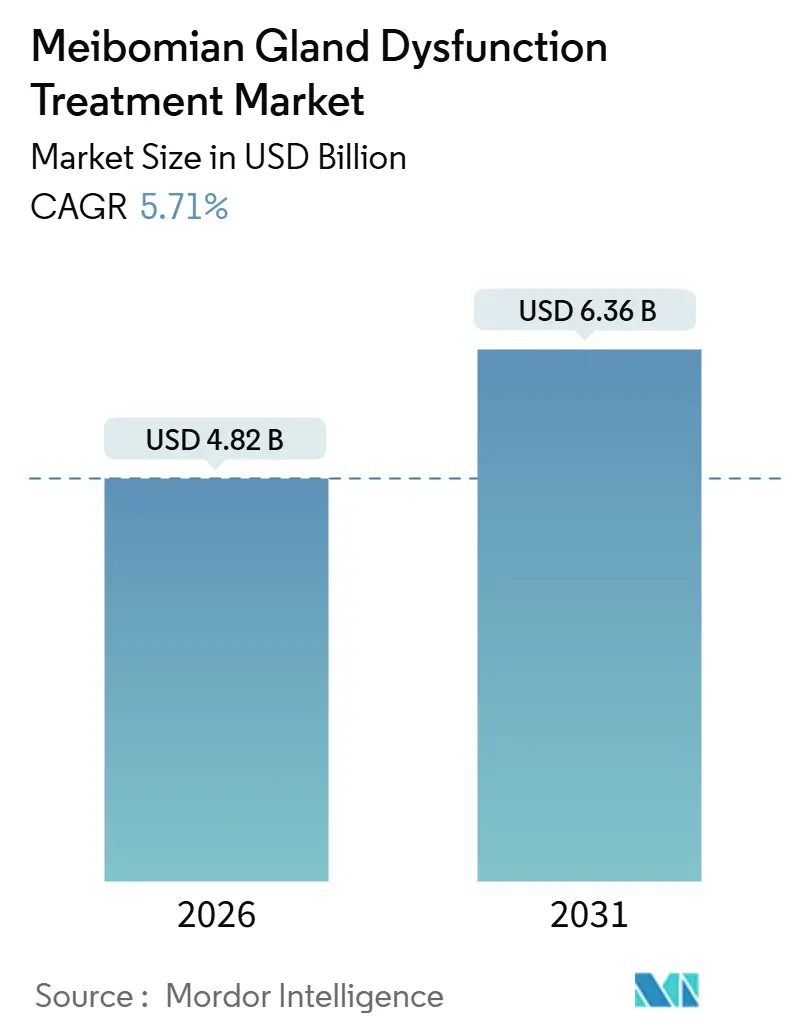

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

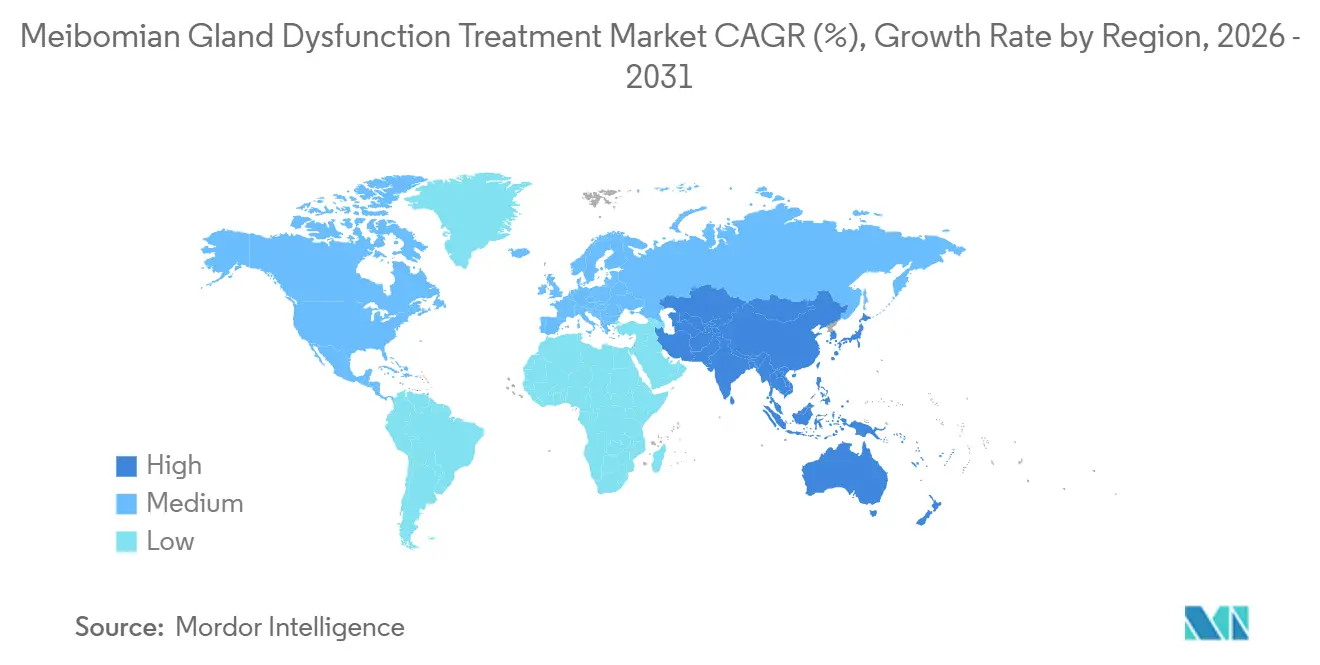

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

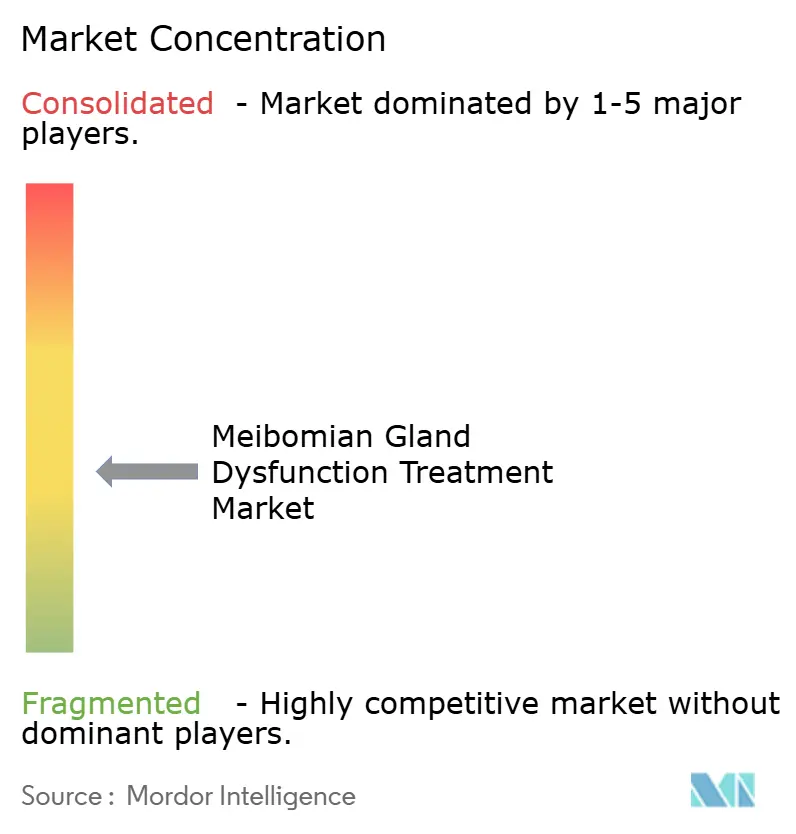

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Meibomian Gland Dysfunction Treatment Market Analysis by Mordor Intelligence

The Meibomian Gland Dysfunction Treatment Market size is estimated at USD 4.82 billion in 2026, and is expected to reach USD 6.36 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Demand is accelerating as clinicians acknowledge that evaporative dry eye represents most cases and now have targeted options such as perfluorohexyloctane eye drops and single-session thermal pulsation. In-office devices are winning share because a 12-minute procedure can deliver relief for up to a year while avoiding the adherence problems of twice-daily drops. Payer pressure is shifting volumes from lifetime prescriptions toward one-time interventions, yet rapid FDA approvals of Miebo, Vevye and TRYPTYR are widening the pharmaceutical armamentarium. Wearable heated masks and AI-enabled diagnostic apps are opening a consumer pathway that bypasses clinics, while capital-intensive device makers court U.S. self-insured employers seeking pharmacy-cost offsets.

Key Report Takeaways

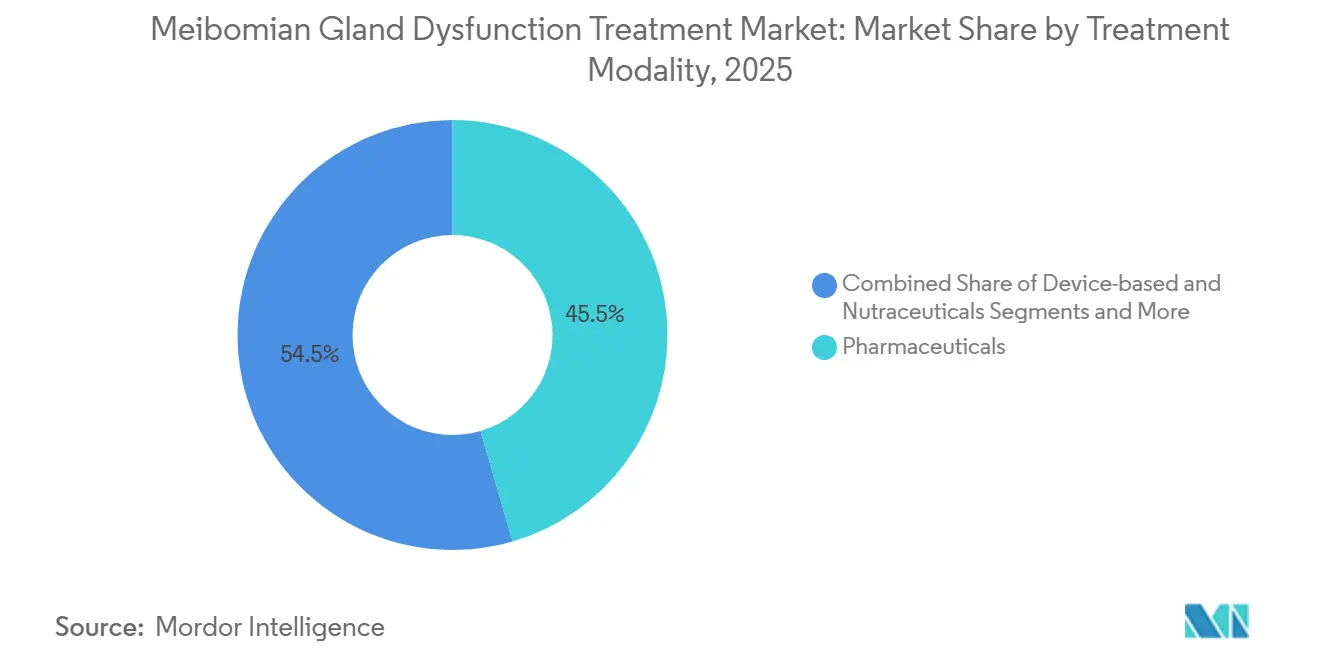

- By treatment modality, pharmaceuticals led with 45.55% of Meibomian Gland Dysfunction Treatment market share in 2025, whereas devices are advancing at a 10.25% CAGR to 2031.

- By end user, ophthalmology and optometry clinics accounted for 54.23% of the Meibomian Gland Dysfunction Treatment market size in 2025 and home-care solutions are expanding at an 8.15% CAGR through 2031.

- By geography, North America captured 38.15% revenue in 2025, while Asia-Pacific is forecast to grow at an 8.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meibomian Gland Dysfunction Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of in-office thermal pulsation systems | +1.2% | North America, Europe (private clinics), Asia-Pacific (tier-1 cities) | Medium term (2-4 years) |

| Growing clinical evidence and guideline endorsements for IPL therapy | +0.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Rising prevalence of screen-induced evaporative dry eye | +1.5% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing FDA approvals of novel cyclosporine and SFA formulations | +1.0% | North America with spill-over to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Emergence of AI-enabled home-use devices for gland diagnostics | +0.6% | Urban centers worldwide | Long term (≥ 4 years) |

| Employer self-insurance push for one-time procedures | +0.5% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of In-Office Thermal Pulsation Systems

Thermal pulsation platforms such as TearCare, LipiFlow and iLux are displacing warm compresses because they hold the tarsal conjunctiva at 41 °C to 43 °C, fully liquefying meibum and restoring gland patency. The 24-month SAHARA RCT reported that 76% of TearCare-treated patients avoided retreatment for two years, with median time to first retreatment of seven months among the remainder[1]Sight Sciences, “SAHARA 24-Month Results,” investors.sightsciences.com. U.S. self-insured employers see economic logic in a USD 600–900 procedure versus yearly drug spend above USD 6,000. Adoption remains highest in North America, moderate in self-pay European clinics and emergent in Chinese tier-1 cities, where device cost still limits public hospital uptake.

Growing Clinical Evidence and Guideline Endorsements for IPL Therapy

Meta-analyses of randomized trials from 2024-2025 confirm significant gains in meibomian secretion quality and tear-break-up time after three to four IPL sessions. The American Academy of Ophthalmology lists typical U.S. pricing near USD 400 per session, yet major payers like Kaiser Permanente label IPL investigational, throttling reimbursement[2]American Academy of Ophthalmology, “Devices for Dry Eye,” aao.org. Shared dermatology-ophthalmology systems boost adoption in Australia and parts of Europe where capital is already deployed, but Fitzpatrick IV-VI skin-type contraindications cap addressable prevalence in South Asia and sub-Saharan Africa.

Rising Prevalence of Screen-Induced Evaporative Dry Eye

Average blink rates drop from 15-20 to about five per minute during sustained screen use, promoting lipid stagnation. China’s 2023 consensus notes evaporative pathology in 69-86% of dry eye cases and daily screen time exceeding eight hours among urban adults. Similar behavior in North America ties into hybrid work patterns, driving earlier onset of gland dropout and enlarging the Meibomian Gland Dysfunction Treatment market.

Increasing FDA Approvals of Novel Cyclosporine and SFA Formulations

Between 2023 and 2025 the FDA cleared Miebo, Vevye and TRYPTYR, each addressing unique mechanisms—evaporation barrier, nanomicellar immunomodulation and TRPM8 agonism respectively. Phase 4 data show perfluorohexyloctane cuts symptom severity by 46% within one week, while TRYPTYR delivers tear stimulation in a single day, supporting combination regimens for mixed-etiology patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of capital equipment and consumables | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited reimbursement outside North America and Japan | -1.1% | Europe, Asia-Pacific ex-Japan, LATAM, MEA | Medium term (2-4 years) |

| Long-term durability of single-session treatments unproven | -0.5% | Global | Long term (≥ 4 years) |

| Preservative toxicity from chronic glaucoma drops | -0.4% | Aging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Capital Equipment and Consumables

Thermal consoles list for USD 35,000-50,000 and each disposable adds USD 200-350, pricing out rural practices where an average consultation costs under USD 30. IPL platforms cost even more and require four sessions yearly, pushing cash-pay burden past USD 1,600—prohibitive in India and Brazil.

Limited Reimbursement Outside North America and Japan

The UK NHS, German G-BA and France’s HAS provide no codes for thermal pulsation or IPL, leaving patients to self-fund procedures priced up to USD 900 per eye. China’s insurance catalog and India’s Ayushman Bharat do not list MGD devices, constricting uptake to private chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Devices Outpace Drugs on Durability Promise

Devices captured a smaller share yet are growing at 10.25% CAGR, more than twice pharmaceuticals, as clinics market a single session that postpones symptoms for six to twelve months. Pharmaceuticals still held 45.55% of Meibomian Gland Dysfunction Treatment market share in 2025 thanks to legacy cyclosporine and lifitegrast prescriptions, but dissatisfaction rates near 87% signal vulnerability. Perfluorohexyloctane is the fastest-rising drug, supported by rapid symptom relief documented in Phase 4 studies[3]Bausch + Lomb, “Phase 4 Miebo Data,” ir.bausch.com. TRYPTYR’s 24-hour onset introduces neuromodulation and may combine with evaporation-barrier drops for mixed disease.

Thermal pulsation dominates in-office devices; TearCare’s durability data underpin premium pricing. IPL adoption hinges on payer recognition. Home wearables, including iFlo and Meiboleyes, are spreading through e-commerce at USD 300-400, appealing to tech-savvy users and feeding future AI-diagnostic ecosystems. FDA 510(k) exemptions for low-risk heaters shorten time-to-market, fostering a crowded field.

By End User: Home-Care Surges as Wearables Mature

Specialty ophthalmology and optometry clinics generated 54.23% of 2025 revenue, leveraging trained staff and imaging tools. High-volume centers amortize console cost in 12-18 months, whereas general optometrists defer investment. Hospitals remain minor because procedures are outpatient.

Home-care is projected to rise 8.15% CAGR, the fastest among end users, driven by connected masks and handheld debridement kits validated in 2025 trials. Tele-optometry platforms ship devices after video evaluation, reserving onsite visits for refractory cases. Growth is capped until AI meibography receives regulatory clearance and payers craft benefit pathways for consumer hardware.

Geography Analysis

North America represents the largest slice, holding 38.15% of 2025 revenue. High per-capita spend, FDA’s quick approvals of Miebo and TRYPTYR, and employer funding of one-time procedures underpin leadership. U.S. reimbursement remains patchy; Medicare lacks a national decision on thermal pulsation and major integrated insurers deem IPL investigational, curbing reach. Canada’s single-payer model and Mexico’s fragmented coverage slow device rollout.

Asia-Pacific is the growth engine at 8.51% CAGR. China’s July 2025 clearance of Heng Qin introduced the first local MGD drug in a country where evaporative disease dominates, expanding the Meibomian Gland Dysfunction Treatment market size. Smartphone over-use accelerates pathology, and premium urban clinics invest in TearCare and IPL despite no public reimbursement. India lacks Class C approvals for thermal systems, confining adoption to metro centers. Japan’s Senju-Novaliq pact awaits pricing resolution, yet pent-up demand among 5 million diagnosed patients signals upside once launch occurs. Australia posts high self-pay tolerance, while South Korea’s approval of preservative-free glaucoma drops may indirectly enlarge the candidate pool.

Europe trails because national health systems demand cost-effectiveness proof before funding devices. NICE acknowledges thermal pulsation but offers no NHS reimbursement. EMA authorization of cyclosporine Vevizye in 2024 enriches drug choice, though 12-24-month pricing talks delay uptake. Private pay dominates in the GCC, South Africa and wealthier Latin American metros, but regulatory back-logs and absent reimbursement restrain scale.

Competitive Landscape

Competition is moderately fragmented: no supplier exceeds a double-digit global share. Pharmaceutical incumbents—Bausch + Lomb, AbbVie/Allergan, Alcon, Santen—compete on onset speed and mechanism while facing looming generics. Device specialists—Sight Sciences, Johnson & Johnson Vision, Alcon, Lumenis—sell capital gear into high-volume clinics but confront a USD 35,000-plus entry hurdle in price-sensitive regions.

Consolidation is active. Bausch + Lomb’s 2023 purchase of Xiidra for up to USD 2.5 billion combined anti-inflammatory and evaporation-barrier franchises, seeking prescriber lock-in. Merck’s 2024 EyeBio buy added an undisclosed MGD-focused pipeline. Technology differentiation continues: Alcon’s 2025 TRYPTYR brought first-in-class TRPM8 agonism; Sight Sciences’ 24-month durability data underpin premium TearCare positioning. Chinese entrants push low-cost wearables, but lack FDA-cleared AI diagnostics, making global expansion contingent on SaMD approvals. White space includes smartphone-based gland-imaging apps and preservative-free glaucoma generics, both capable of enlarging addressable demand and reinforcing device efficacy.

Meibomian Gland Dysfunction Treatment Industry Leaders

Alcon

Bausch + Lomb

Johnson & Johnson Vision

AbbVie (Allergan)

Sight Sciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Azura Ophthalmics received positive FDA feedback that its clinical dossier for AZR-MD-001 is adequate for NDA filing, positioning a first-in-class keratolytic for MGD approval.

- July 2025: Hengrui secured NMPA approval for Heng Qin perfluorohexyloctane eye drops, the first China-exclusive MGD drug, after Phase 3 trials showed symptom improvement from week 2.

Global Meibomian Gland Dysfunction Treatment Market Report Scope

As per the scope of the report, meibomian gland dysfunction (MGD) treatment refers to the various methods and procedures used to manage and alleviate the symptoms caused by the malfunction of the meibomian glands. These glands, located in the eyelids, produce oils that are essential for a healthy tear film and eye comfort. When these glands become blocked or their secretions become abnormal, it leads to dry eye symptoms and ocular surface inflammation.

The segmentation of the Meibomian Gland Dysfunction Treatment Market by treatment modality includes pharmaceuticals, such as cyclosporine formulations, lifitegrast, perfluorohexyloctane (SFA), and others. Device-based treatments include thermal pulsation systems, intense pulsed light (IPL) systems, thermoelectric masks & RF/LLLT, and others. Additionally, nutraceuticals and other treatment options are also considered. By end user, the market is segmented into ophthalmology & optometry clinics, hospitals, ambulatory surgical centers, and home-care. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Pharmaceuticals | Cyclosporine Formulations |

| Lifitegrast | |

| Perfluorohexyloctane (SFA) | |

| Others | |

| Device-based | Thermal Pulsation Systems |

| Intense Pulsed Light (IPL) Systems | |

| Thermoelectric Masks & RF/LLLT | |

| Others | |

| Nutraceuticals & Others |

| Ophthalmology & Optometry Clinics |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Pharmaceuticals | Cyclosporine Formulations |

| Lifitegrast | ||

| Perfluorohexyloctane (SFA) | ||

| Others | ||

| Device-based | Thermal Pulsation Systems | |

| Intense Pulsed Light (IPL) Systems | ||

| Thermoelectric Masks & RF/LLLT | ||

| Others | ||

| Nutraceuticals & Others | ||

| By End User | Ophthalmology & Optometry Clinics | |

| Hospitals | ||

| Ambulatory Surgical Centers | ||

| Home-care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the Meibomian Gland Dysfunction Treatment market?

The market was valued at USD 4.82 billion in 2026.

How fast is the segment of in-office devices growing?

Device revenues are advancing at a 10.25% CAGR through 2031.

Which region offers the highest growth outlook?

Asia-Pacific is projected to register an 8.51% CAGR, the fastest worldwide.

Why are employers paying for thermal pulsation procedures?

One-time procedures can offset annual prescription costs that exceed USD 6,000 per employee.

Which new drug acts via TRPM8 agonism?

Alcon's TRYPTYR stimulates natural tear production within one day of dosing.

Page last updated on: