Market Overview

| Study Period | 2020 - 2030 |

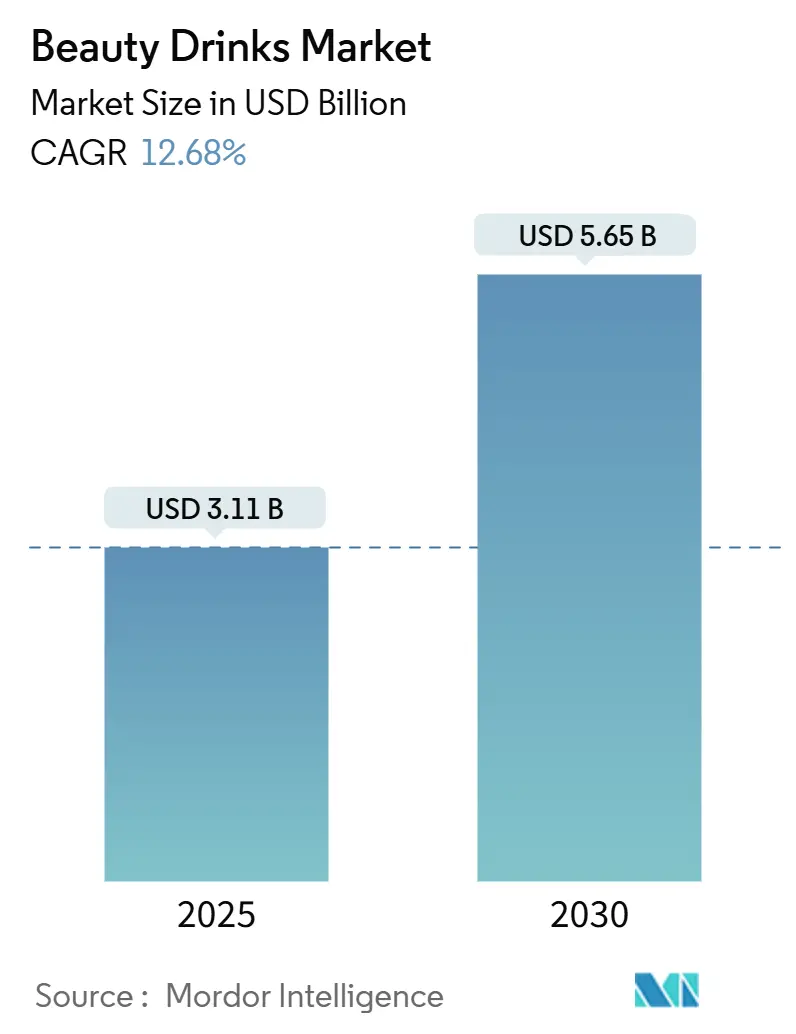

| Market Size (2025) | USD 3.11 Billion |

| Market Size (2030) | USD 5.65 Billion |

| Growth Rate (2025 - 2030) | 12.68% CAGR |

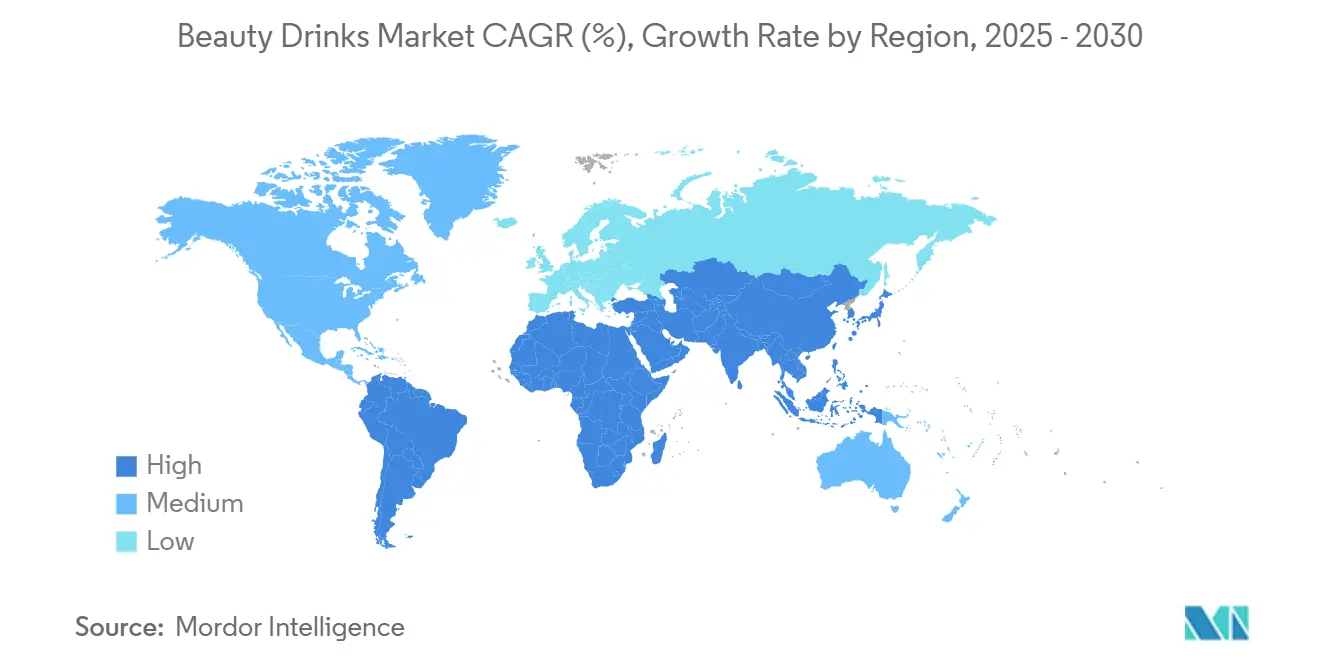

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beauty Drinks Market Analysis by Mordor Intelligence

The global beauty drinks market reached USD 3.11 billion in 2025 and is projected to grow to USD 5.65 billion by 2030, at a CAGR of 12.68% during the forecast period. The market growth is primarily driven by increasing consumer awareness of preventive healthcare measures and a shift from traditional topical applications to ingestible beauty products. The rising aging population in developed countries, coupled with growing concerns about lifestyle-related diseases, has accelerated the adoption of beauty drinks. Additionally, these products have gained significant traction among women seeking to reduce wrinkles and enhance their appearance, with celebrity endorsements further amplifying market growth. n addition to these, the surge of e-commerce platforms has broadened the reach of beauty drinks, allowing brands to engage consumers directly through targeted marketing. Furthermore, the rising inclination towards natural and organic ingredients, coupled with personalized formulations catering to specific health and beauty requirements, is intensifying the demand.

Key Report Takeaways

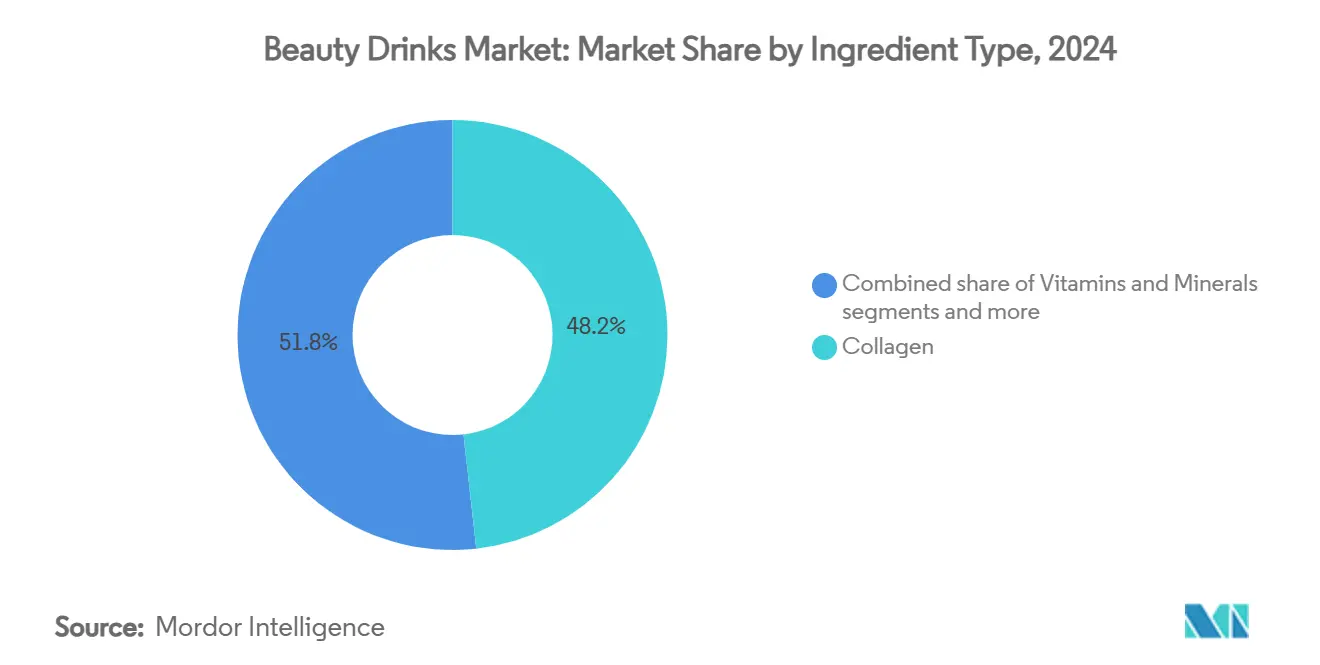

- By ingredient type, collagen held 48.23% of the market share in 2024, while vitamins and minerals are set to grow at a 14.55% CAGR through 2030.

- By functional benefit, anti-aging led with 42.04% revenue share in 2024, skin hydration is slated to expand at a 13.67% CAGR to 2030.

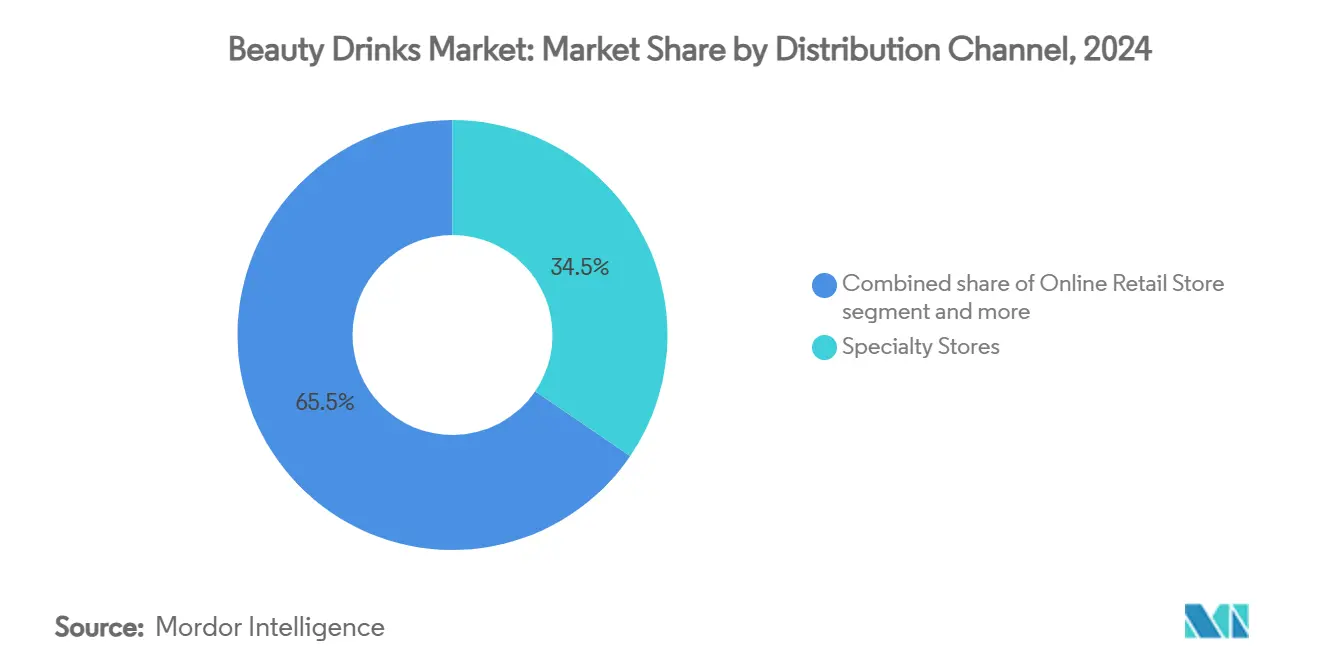

- By distribution channel, specialty stores commanded 34.52% of the beauty drinks market in 2024, and e-commerce channels are rising at a 12.76% CAGR through 2030.

- By geography, Asia-Pacific captured 41.02% of the market share in 2024, and the Middle East and Africa will register the fastest 13.83% CAGR to 2030.

Global Beauty Drinks Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer focus on anti-aging and inner wellness solutions | +2.1% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Rising demand for beverages supporting skin and hair health | +1.8% | Asia-Pacific core, spill-over to Middle East and Africa and Europe | Short term (≤2 years) |

| Expanding availability of collagen and vitamin-enriched beauty beverages | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Celebrity endorsements and influencer marketing boosting brand credibility | +1.2% | Global, highest in North America and Europe | Short term (≤2 years) |

| Shift toward preventive skincare over topical cosmetic applications | +2.3% | Global, strong in Asia-Pacific and North America | Long term (≥4 years) |

| Innovations in flavors and formulations improve consumer acceptance | +1.4% | Global, early adoption in developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Increasing Consumer Focus On Anti-Aging And Inner Wellness Solutions

As populations age and wield greater purchasing power, beauty drinks are witnessing a surge in adoption. Heightened awareness about aging's impact on appearance has spurred demand for functional beverages that promise anti-aging benefits and bolster skin health. The "beauty from within" trend, gaining traction especially among millennials and Gen X, has led to a spike in the consumption of beauty drinks rich in collagen and antioxidants. Consumers' growing preference for holistic wellness is evident in the rising popularity of beauty drinks infused with bioactive ingredients like hyaluronic acid, vitamins, and peptides. According to the World Health Organization, the number of people aged 60 and older worldwide is projected to increase from 1.1 billion in 2023 to 1.4 billion by 2030, further strengthening the market growth potential [1]Source: World Health Organization, “Population Ageing Q&A,” who.int. This demographic evolution not only broadens the consumer base but also pushes brands to craft innovative formulations targeting specific age-related skin issues. Moreover, with older adults enjoying increased disposable incomes, premium pricing strategies become viable, positioning beauty drinks as a profitable niche in the expansive health and wellness sector.

Expanding Availability of Collagen And Vitamin-Enriched Beauty Beverages

Consumers are increasingly drawn to beauty drinks due to growing evidence supporting their efficacy in improving skin health. According to the National Library of Medicine, collagen supplements can enhance skin properties, including hydration, elasticity, and reduce the visibility of wrinkles [2]Source: Liquet-López C. et al., “Collagen Supplementation and Skin Health,” National Library of Medicine, ncbi.nlm.nih.gov.Manufacturers, spurred by scientific validation, are now crafting innovative formulations that blend collagen peptides with vital vitamins, minerals, and bioactive compounds. Market growth is buoyed by notable product launches, including Crushed Tonic's premium marine collagen-infused Korean Broth Beverage, debuting in February 2025. Consumers are increasingly drawn to the convenience of ingesting beauty-boosting nutrients in beverage form, sidestepping traditional supplements or topical applications. This shift resonates especially with those seeking straightforward skincare solutions. Furthermore, as personalized nutrition gains traction, brands are rolling out customizable beauty drinks, fine-tuned to individual skin types and concerns, fostering deeper consumer engagement. The trend also sees a push for natural flavors and transparent, clean-label ingredients, mirroring the beauty and wellness sector's growing emphasis on health-conscious choices and transparency.

Celebrity Endorsements And Influencer Marketing Boosting Brand Credibility

Social media platforms, especially TikTok, are reshaping consumer purchasing decisions in the beauty drinks market, underscoring the power of celebrity endorsements and influencer marketing. Testimonials and before-and-after results from trusted personalities lend authenticity to product claims, driving adoption, especially among younger demographics attuned to lifestyle and beauty influencers. TikTok's algorithm allows niche beauty drink brands to achieve viral success without hefty advertising budgets, leveling the playing field for emerging competitors through user-generated content. A testament to this trend, in December 2024, American podcaster Alex Cooper unveiled 'Unwell Hydration', a drink line packed with electrolytes, B-complex vitamins, and green coffee extract. Brands like Glow Recipe have also tapped into influencer partnerships and trending TikTok challenges, propelling their collagen-infused beauty drinks. Such digital marketing maneuvers are fueling rapid growth in the global beauty drinks market, emphasizing the pivotal role of social media endorsements in market penetration and trust-building.

Shift Toward Preventive Skincare Over Topical Cosmetic Applications

Cosmetic products can trigger adverse reactions ranging from mild irritation to severe health issues, with studies published in Clinical Epidemiology and Global Health reporting high prevalence of problems including conjunctivitis, acne, contact dermatitis, pigmentation issues, and itching among users [3]Source: Adityan S. et al., “Cosmetic Product Adverse Effects: A Cross-Sectional Study,” Clinical Epidemiology and Global Health, cegh.net .This awareness has sparked a significant shift in consumer behavior moving from reactive cosmetic treatments to proactive nutritional interventions. Consumers now understand that skin health is rooted in internal cellular processes, not just external applications. The beauty drinks market is witnessing significant growth, especially among Generation Z and Millennials. These consumers are prioritizing long-term skin health and preventive skincare over corrective treatments. They're increasingly opting for beauty drinks enriched with collagen, vitamins, antioxidants, and other bioactive compounds. These ingredients, known for their cellular benefits, are driving a consistent demand for daily beauty drinks, overshadowing sporadic cosmetic interventions. This shift is in harmony with broader wellness trends, emphasizing internal nourishment for skin health. Additionally, the rising demand for clean beauty and product transparency has led brands to eliminate harmful chemicals from their formulations. This move not only aligns with consumer preferences but also bolsters trust in ingestible beauty solutions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product costs limit access for price-sensitive consumers | -1.9% | Global, impactful in developing economies | Short term (≤2 years) |

| Lack of clinical evidence for long-term beauty benefit claims | -1.3% | Global, high in regulated markets | Medium term (2-4 years) |

| Consumer skepticism regarding effectiveness of ingestible beauty solutions | -1.1% | Primarily North America and Europe | Short term (≤2 years) |

| Limited awareness in developing economies about beauty drinks | -0.8% | Middle East and Africa, South America, parts of Asia-Pacific | Long term (≥4 years) |

Source: Mordor Intelligence

High Product Costs Limit Access For Price-Sensitive Consumers

Beauty drinks face a significant market restraint due to their high costs, especially in price-sensitive regions and developing economies. Premium ingredients such as marine collagen, vitamins, antioxidants, and bioactive compounds are pricier than traditional protein sources. Moreover, specialized extraction and processing technologies complicate manufacturing. These heightened production costs lead to steeper retail prices, making beauty drinks a luxury for budget-conscious consumers. This economic sensitivity is especially evident in developing markets, where limited disposable incomes curtail adoption, even amidst a rising interest in wellness products. As a result, many consumers turn to traditional beverages, basic nutritional supplements, or topical products as more affordable alternatives. This creates a tension between the allure of premium ingredient quality and the reality of market accessibility. Furthermore, a lack of widespread consumer education on the long-term benefits of beauty drinks dampens the enthusiasm to invest in these premium products. To navigate these challenges, brands might need to consider cost-effective formulations and tailored pricing strategies to broaden their appeal in emerging markets.

Lack of Clinical Evidence For Long-Term Beauty Benefit Claims

In markets under stringent regulatory scrutiny, beauty drink manufacturers grapple with the challenge of aligning marketing messages with scientifically validated claims. Regulatory bodies, like the FDA and Australia's Therapeutic Goods Administration, are tightening their grip, demanding robust clinical evidence for health claims on dietary supplements and beauty products. This push for evidence is underscored by a notable scarcity of comprehensive studies backing the long-term beauty benefits of these products. Such a void in evidence is especially pronounced for newer ingredients, such as glutathione and certain vitamin formulations, which haven't yet garnered the clinical validation that established ingredients, like collagen peptides. This lack of scientific backing not only hampers manufacturers in securing regulatory approvals for health claims but also casts a shadow on market growth and erodes consumer trust. In response, companies are ramping up investments in clinical trials and forging alliances with research institutions to bolster their evidence base. Furthermore, there's a concerted effort towards heightened transparency and educational initiatives, targeting both consumers and regulatory entities, to cultivate trust and ease market entry.

Segment Analysis

By Ingredient Type: Collagen Dominance Faces Vitamin Innovation

Collagen commands a dominant 48.23% share in 2024, bolstered by clinical validations that highlight its hydrolyzed peptides' efficacy in enhancing skin hydration and elasticity. Glutathione, recognized for its antioxidant benefits in promoting cellular health and skin brightness, lacks the extensive clinical backing that collagen enjoys. Nevertheless, glutathione's potential in countering oxidative stress and fostering a luminous complexion has spurred its rising popularity, leading to heightened interest and investment in its scientific exploration. With a growing consumer appetite for natural and effective beauty solutions, both collagen and glutathione are poised to play synergistic roles in the burgeoning beauty drinks market.

The vitamins and minerals segment shows the highest growth potential with a 14.55% CAGR through 2030, driven by consumers seeking comprehensive nutritional solutions. This growth particularly stems from vitamin C's role in collagen synthesis and bioavailability enhancement, while biotin addresses specific hair and nail health requirements, indicating a shift toward more sophisticated, targeted nutritional interventions.

Note: Segment shares of all individual segments available upon report purchase

By Functional Benefit: Anti-Aging Leadership Yields to Hydration Growth

Anti-aging applications command a dominant 42.04% market share in 2024, underscoring consumers' focus on staving off visible aging signs. Yet, the skin hydration segment is outpacing others, boasting a robust 13.67% CAGR growth rate projected through 2030. This surge signals a notable pivot towards prioritizing foundational skin health, especially among younger consumers who lean towards preventive care rather than reactive solutions. Heightened awareness about skin moisture's role in bolstering the skin barrier and postponing aging signs fuels this trend. Furthermore, the allure of beauty drinks, which meld hydrating agents with antioxidants and vitamins, is captivating health-savvy consumers eager for holistic internal skincare remedies..

The market demonstrates strong cross-category appeal through segments like detoxification, which attracts wellness-conscious consumers seeking holistic health benefits, and specialized hair and nail health applications that address specific concerns. This multi-functional approach enables beauty drinks that target multiple benefits to command premium pricing and foster stronger consumer loyalty compared to single-benefit alternatives.

By Distribution Channel: Specialty Stores Lead as E-commerce Accelerates

Specialty stores command a leading position with a 34.52% market share in 2024, capitalizing on expert consultations and product education to justify the premium pricing of their scientifically validated beauty drinks. Online retail stores, buoyed by the allure of convenience and an expansive product selection, are projected to expand at a robust 12.76% CAGR through 2030. Meanwhile, drug stores and pharmacies bolster the credibility of their offerings, especially those making health claims, by aligning with recognized healthcare associations. The rising trend of subscription models in online channels dovetails seamlessly with the daily consumption habits of beauty drinks, paving the way for consistent revenue streams for brands. This subscription approach not only fosters direct engagement with consumers but also empowers brands to customize their offerings based on individual purchase behaviors and preferences, significantly boosting customer retention and lifetime value.

Supermarkets and direct-to-consumer platforms are catering to price-sensitive consumers who prioritize convenience and cost savings. Supermarkets, with their one-stop shopping advantage, make beauty drinks readily accessible to a wide audience. In contrast, direct-to-consumer platforms allow brands to sidestep traditional retail markups, presenting competitive prices and tailored shopping experiences. These platforms also frequently offer subscription services and exclusive online promotions, boosting affordability and nurturing long-term loyalty among budget-conscious shoppers.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific holds the largest market share at 41.02% in 2024, benefiting from deep-rooted cultural acceptance of functional beverages and well-developed regulatory frameworks. Japan and South Korea stand out as premium market leaders, where consumers readily invest in scientifically validated products. The region's demographic profile, combining an aging population seeking anti-aging solutions with younger consumers adopting preventive beauty approaches, creates a robust market for daily-use beauty drinks.

The Middle East and Africa region demonstrates the highest growth potential with a projected CAGR of 13.83% through 2030. This growth is supported by developing wellness tourism infrastructure and increasing urbanization. South Africa leads the sub-Saharan market with USD 56.9 million in cosmetics imports, showing particular demand for organic and natural beauty drinks. Rising consumer spending power across the region creates new consumer segments seeking convenient wellness solutions.

North America and Europe maintain strong market positions through established nutraceutical awareness and comprehensive regulatory frameworks. These mature markets emphasize transparency in ingredient sourcing and manufacturing processes, particularly favoring clean-label products and sustainable practices. Marine collagen products with environmental credentials receive particular attention, reflecting these regions' focus on both personal wellness and environmental responsibility.

Competitive Landscape

The beauty drinks market is moderately fragmented, presenting strategic opportunities for both established companies like SAPPE Public Company Limited, Shiseido Co. Ltd, Lacka Foods Limited, and Nestle SA, as well as emerging players. The competitive environment increasingly favors companies that can provide robust clinical evidence to support their efficacy claims, as regulatory frameworks and consumer sophistication demand scientific validation rather than marketing promises.

New market entrants are leveraging direct-to-consumer channels and social media marketing, particularly through user-generated content on platforms like TikTok, to connect with younger consumers seeking beauty-from-within solutions. The market presents opportunities in specialized formulations targeting specific demographic groups and functional benefits. In April 2024, Shiseido demonstrated this trend by launching new drink format supplements, which gained significant traction in Japan and China, marking its expansion in the ingestible beauty sector.

Technology adoption in the beauty drinks market enables personalized nutrition approaches and subscription-based business models that increase customer lifetime value. Companies are implementing omnichannel retail strategies that combine physical expertise with digital accessibility, creating competitive advantages against pure online competitors. These technological integrations help manufacturers better serve consumer needs while establishing stronger market positions.

Beauty Drinks Industry Leaders

-

Shiseido Co. Ltd

-

Kinohimitsu

-

Nestlé SA

-

Sappe Public Company Ltd

-

Lacka Foods Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: In May 2025, the MAR Advantage team unveiled its ready-to-drink (RTD) Athena's Glow Drink, a blend of natural ingredients tailored for women aged 45 and above. Athena's Glow Drink makes its entrance in four invigorating flavors.

- August 2024: Collagen Café introduced Advanced Collagen Liquid, a sugar-free supplement sweetened with Stevia.

- April 2024: Bizzi launched ready-to-drink coffee-plus-collagen blends in three flavor variants. Health-conscious consumers seeking convenient wellness options are the target audience for three new blends: Coffee + Collagen Signature Blend, Matcha + Collagen Signature Blend, and Coffee + Collagen Vanilla & Turmeric.

- January 2024: Pretty Tasty, a beverage brand focused on beauty innovations, has unveiled its inaugural ready-to-drink collagen tea line, aptly named Pretty Tasty Collagen Tea.

Global Beauty Drinks Market Report Scope

Beauty drinks are a new concept among a growing trend of 'nutri-cosmetics,' which include foods, drinks, and supplements that provide beauty benefits from within.

The beauty drinks market is segmented by type (vitamins and minerals, collagen, carotenoids, and other types), distribution channel (grocery retailers, beauty specialty stores, drug stores and pharmacies, and other distribution channels), and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers market size and forecasts in value (USD million) for the above segments.

| By Ingredient Type | Vitamins and Minerals | ||

| Collagen | |||

| Glutathione | |||

| Other Types | |||

| By Functional Benefit | Anti-Ageing | ||

| Detoxification | |||

| Skin Hydration | |||

| Hair and Nail Health | |||

| Others Functional Benefits | |||

| By Distribution Channel | Specialty Stores | ||

| Drug Stores and Pharmacies | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Spain | |||

| Netherlands | |||

| Italy | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Indonesia | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Nigeria | |||

| Saudi Arabia | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

By Ingredient Type

| Vitamins and Minerals |

| Collagen |

| Glutathione |

| Other Types |

By Functional Benefit

| Anti-Ageing |

| Detoxification |

| Skin Hydration |

| Hair and Nail Health |

| Others Functional Benefits |

By Distribution Channel

| Specialty Stores |

| Drug Stores and Pharmacies |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the beauty drinks market and how fast is it growing?

The beauty drinks market was valued at USD 3.11 billion in 2025 and is projected to expand to USD 5.65 billion by 2030 at a 12.68% CAGR.

Which ingredient type holds the largest share in the beauty drinks market?

Collagen beverages captured 48.23% of global revenue in 2024, making them the dominant ingredient segment.

What functional benefit segment is growing the fastest?

Skin hydration formulations are forecast to rise at a 13.67% CAGR through 2030, outpacing anti-aging and detox categories.

Which region leads the beauty drinks market in revenue terms?

Asia-Pacific held 41.02% of global sales in 2024, driven by strong demand in Japan, South Korea, and China.

Page last updated on: July 7, 2025