Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.32 Billion |

| Market Size (2026) | USD 31.3 Billion |

| Market Size (2031) | USD 36.64 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

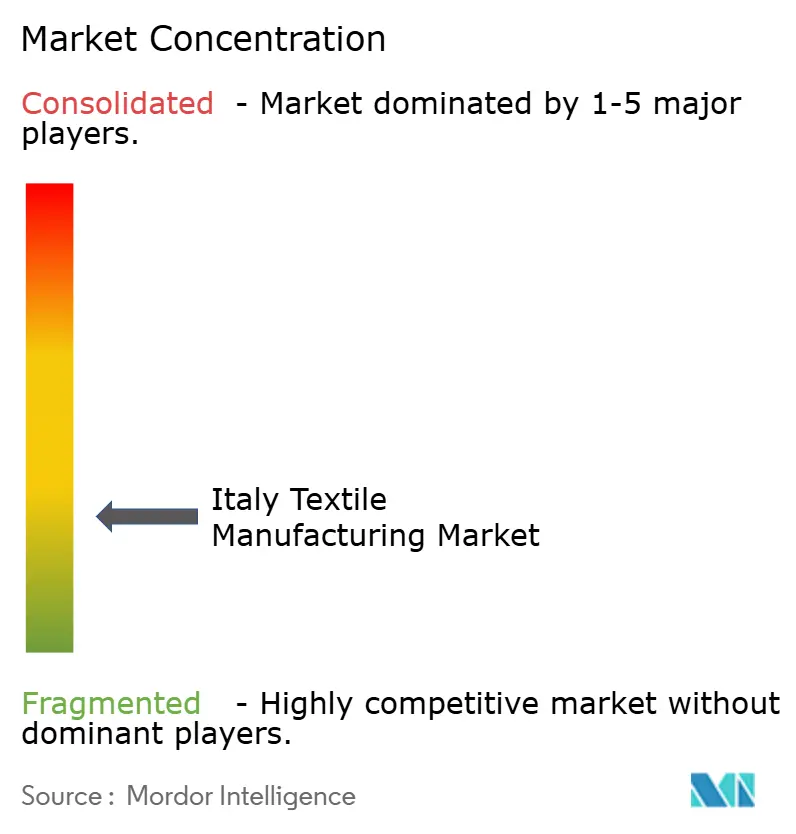

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Textile Manufacturing Market Analysis by Mordor Intelligence

The Italy Textile Manufacturing Market size was valued at USD 30.32 billion in 2025 and estimated to grow from USD 31.3 billion in 2026 to reach USD 36.64 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031).

This growth trajectory is underpinned by a strategic shift from volume‐based manufacturing toward premium fabrics, technical textiles, and circular economy solutions, which collectively insulate producers from global demand swings. Clustered industrial districts Biella for wool, Como for silk, and Prato for recycling, enable vertical integration that safeguards margins, while EU Green Deal regulations accelerate machinery upgrades and traceability investments. Forward-looking companies are pairing mycelium fibers and recycled polyester with digital passports to meet sustainability mandates and to provide a line-of-sight from raw material to store shelf. On the demand side, automotive lightweighting, medical disposables, and protective gear are creating fresh pull for non-woven and specialty fabrics, helping offset the plateau in fast fashion exports[1]Observatory of Economic Complexity, "Boot Without Borders: New Trade Data Reveal A Mosaic Of Micro-Economies In Italy," oec.world.

Key Report Takeaways

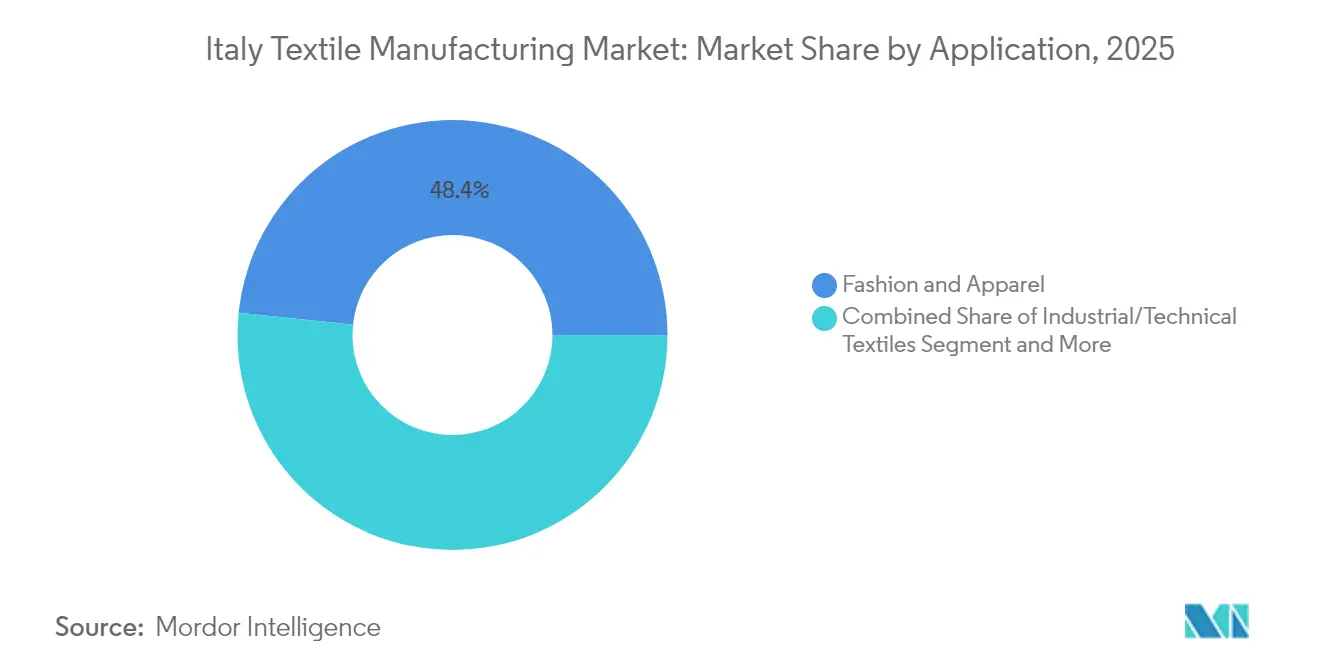

- By application, Fashion & Apparel led with 48.35% of Italy's textile market share in 2025, while Industrial/Technical Textiles is forecast to expand at a 4.66% CAGR through 2031.

- By raw material, synthetic fibers commanded 42.12% of the Italy textiles market size in 2025; recycled polyester is projected to grow at a 5.02% CAGR between 2026-2031.

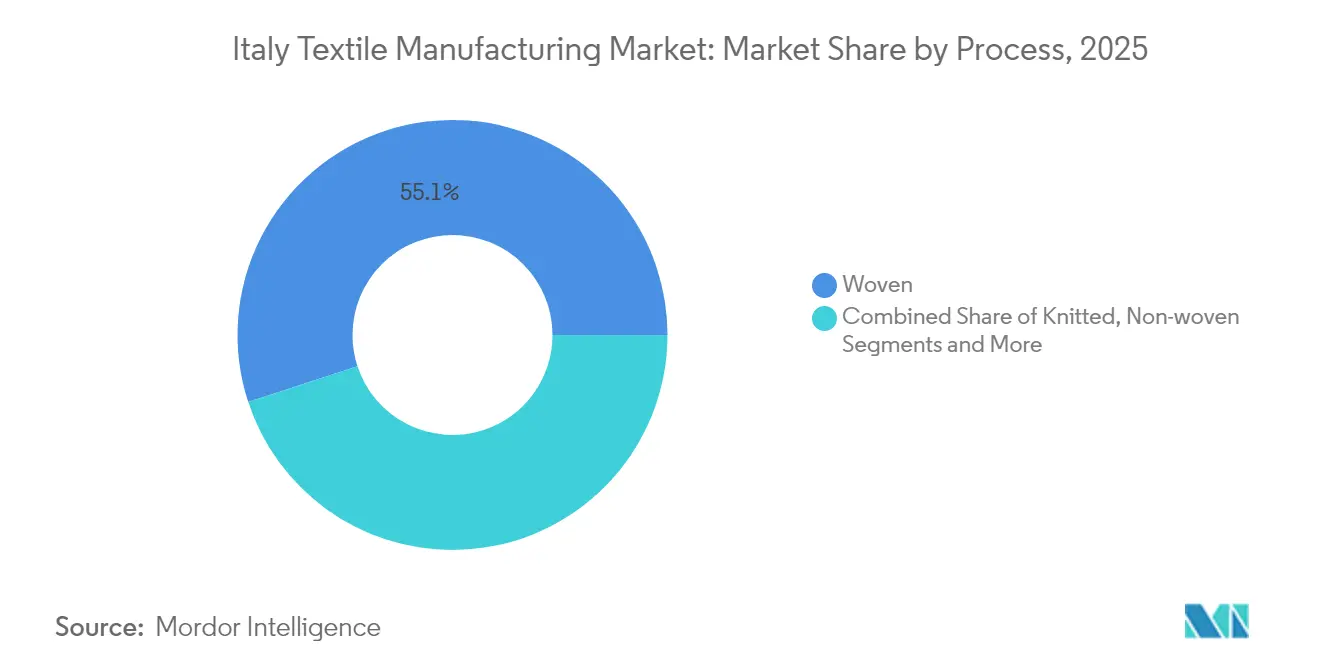

- By process, woven fabrics accounted for 55.05% of the Italy textiles market size in 2025, and non-woven technologies are advancing at a 4.52% CAGR through 2031.

- By geography, the North-East held 34.30% revenue share of the Italy textiles market in 2025, whereas the South & Islands region is set to post a 4.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Textile Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid scale-up of technical/industrial textiles capacity | +1.2% | Lombardy, Veneto; Global end-markets | Long term (≥ 4 years) |

| Export-led rebound in premium wool & silk fabrics | +0.8% | North-West (Biella, Como), North-East | Medium term (2-4 years) |

| EU Green Deal & Ecodesign regulations accelerating retooling | +0.7% | National, EU-wide compliance | Medium term (2-4 years) |

| National Recovery & Resilience Plan funds for circular hubs | +0.6% | Nationwide, early focus on Biella & Lombardy | Medium term (2-4 years) |

| Digital-ready textile machinery adoption | +0.5% | SME-focused, nationwide | Short term (≤ 2 years) |

| Mycelium & bio-based fiber pilots reaching commercial scale | +0.4% | North-West & Central Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-Up Of Technical/Industrial Textiles Capacity

Technical textiles already form 22% of domestic output and exceed USD 4 billion in turnover, placing Italy fourth worldwide. Protective fabric exports capture 6.5% global share as conflict-driven demand lifts shipments for military and emergency services. Growth is redoubled through M&A; Quadrivio’s Industry 4.0 Fund took over Soft N.W., a polypropylene spunbond specialist earning USD 36 million with 90% exports to Germany and CEE. Automotive OEMs are piloting mycelium composites for dashboards and seat backs under the MY-FI Horizon program, while filtration media fit into EU indoor-air directives. With ISO 14001 credentials now table stakes, Italian converters are winning long-cycle contracts where compliance and performance trump unit cost, extending their lead over low-wage rivals.

Export-Led Rebound In Premium Wool & Silk Fabrics

Selective recovery in formalwear is reviving order books for Biella’s wool mills and Como’s silk converters. Reda held USD 83 million in sales in 2024 despite a slowdown, and early-2025 invoices signal steadier North American demand as inventory rightsizing concludes. Marzotto Group, with a USD 398 million turnover, is leveraging fully integrated scouring-to-finishing chains across Europe and North Africa to protect quality and lead times. Heritage houses are complementing artisanal expertise with blockchain QR tags that document fiber origin, processing chemicals, and carbon footprint, thus meeting Digital Product Passport rules. Brewed Protein™ blends created with Spiber showcase how biotech fibers can be inserted into worsted lines without compromising drape, anchoring a premium tier that Asian mills struggle to replicate. Sustained differentiation on provenance and traceability is expected to keep export ASPs resilient even as global luxury consumption normalizes.

EU Green Deal & Ecodesign Regulations Accelerating Re-Tooling

The Ecodesign for Sustainable Products Regulation places textiles in the first wave of Digital Product Passports, phasing in from 2026 for footwear and 2027 for apparel. Italian mills are racing to retrofit looms with real-time resource meters that feed blockchain nodes run by Certilogo, which already authenticates 540 million items for 80+ brands. Save The Duck tags 99% of its outerwear with NFC chips that store repair guides and resale credits, capturing loyalty data in the process. Marzotto refreshed all wool dye houses to closed-loop water systems, cutting discharge by 45% and meeting zero-liquid-discharge zones under Lombardy rules. Firms that cross the DPP compliance line early win preferred-supplier status with EU retailers and unlock eco-modulated EPR fees, turning sunk investments into pricing leverage.

National Recovery & Resilience Plan Funds For Circular Textile Hubs

Italy’s PNRR funnels grant capital into industrial symbiosis, and MagnoLab secured USD 5.3 million to build a sorting-to-spinning pilot in Biella. Lombardy’s follow-on scheme added USD 7.6 million to seed a regional recycling hub that will service 1,200 SMEs. Tuscany channels a parallel tranche into reskilling programs for pattern-makers at risk from automation, embedding inclusivity objectives into the green transition. Early adopters such as Vesti Solidale show the scale advantage: its Rho facility diverts 20,000 tons of post-consumer apparel annually with 60% reuse rates, cutting landfill fees and virgin fiber imports. As extended-producer-responsibility fees enter force in 2025, brands that tap these hubs will realize cost parity with Asian recyclate, reinforcing domestic demand for reclaimed feedstock.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging energy & gas prices are impacting dyeing/finishing margins | -0.9% | Nationwide, concentrated in industrial districts | Short term (≤ 2 years) |

| Competitive pressure from low-cost Asian imports despite tariffs | -0.7% | National, mass-market segments | Medium term (2-4 years) |

| Shortage of green-skilled technicians & ageing workforce | -0.5% | National, acute in North-West and North-East districts | Long term (≥ 4 years) |

| Increasing water-abstraction limits in northern districts | -0.3% | North-West (Biella, Como), North-East (Veneto) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Energy & Gas Prices Impacting Dyeing/Finishing Margins

Gas and electricity costs spiked 28% year-on-year in 2024, throttling SMEs that lack cogeneration or PPA hedges. Dyeing and finishing lines, responsible for over half of textile GHG emissions, saw EBITDA compress by up to 300 bps, prompting 91% more redundancy hours in Veneto. Machinery suppliers report capacity utilization stuck at 61% in H1 2024, with only a modest rise forecast as power futures ease. Water-intensive effluent treatment, already facing stricter discharge caps, magnifies the energy hit. Larger players like Marchi & Fildi captured efficiency gains via heat-recovery and membrane filtration, but micro-finishers risk exit if subsidies lag. Short-term relief hinges on grid decarbonization grants and faster Industry 5.0 rollout[2]MDPI, "Sustainable Wet Processing Technologies For The Textile Industry: A Comprehensive Review," mdpi.com.

Competitive Pressure From Low-Cost Asian Imports Despite Tariffs

Average CIF prices of Chinese polyester fabrics undercut Italian output by 28% in 2024, widening to 34% for cotton blends after shipping rate normalization. Prometeia models show that a 10% U.S. tariff hike could shave USD 1.6 billion off total Italian fashion exports, with mid-tier brands most exposed. Foreign orders for Italian textile machinery slipped 4% in early 2024, indicating that downstream producers overseas are slowing capex in favor of cheap supply. Domestic mills counter by courting luxury houses that prize design provenance, but entry-level apparel is ceding shelf space to fast-fashion imports even with EU safeguard duties in place. The medium-term outlook demands relentless product differentiation and faster lead times to outrun price wars.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Fashion Dominance Meets Technical Innovation

Fashion & Apparel held 48.35% of Italy's textile manufacturing market share in 2025, underscoring the country’s heritage as a luxury production hub. Sales suffered in 2024 as LVMH flagged USD 1.6 billion lower revenues year-over-year, yet the segment retained pricing power via artisanal quality and certified traceability. Industrial/Technical Textiles is the sprinter, poised to log a 4.66% CAGR through 2031 as automakers crave lightweight composites and defense agencies requisition protective gear. Emerging cross-overs like mycelium-based bio-leathers for car interiors blur classical boundaries, enabling fashion mills to pivot into technical niches without abandoning core competencies.

High-strength aramid and UHMWPE fabrics for aerospace, filtration felts for HVAC retrofits, and non-woven medical disposables are expanding addressable markets beyond couture. Startups under the MY-FI consortium collaborate with Volkswagen and Stellantis, demonstrating how industrial textiles piggy-back on Italy’s design ethos to win high-margin contracts. Although mass-market apparel is squeezed by Asian imports, luxury and made-to-measure demand remains sticky, offering runway for dual-track growth once discretionary spending cycles recover.

By Raw Material: Synthetic Leadership Drives Polyester Growth

Synthetic fibers contributed 42.12% to Italy's textile manufacturing market share in 2025, reflecting performance, durability, and cost advantages. Polyester, boosted by bottle-grade recycling and in-house depolymerization tech, will grow at a 5.02% CAGR through 2031. Wool preserves a lucrative niche courtesy of Biella artisans who pair heritage with blockchain passports, ensuring cruelty-free and climate-positive claims. Silk from Como maintains high ASPs, but volume has drifted toward Asian sericulture; Italians compensate by focusing on creative jacquards and digital color management.

Regulations now nudge converters toward recycled content: Marchi & Fildi’s Ecotec yarn, spun from pre-consumer clippings, lowered resource intensity enough to win eco-modulated EPR bonuses. Specialty fibers like carbon, aramid, and bio-based PLA service aerospace and medical orders where Italian know-how beats cost disadvantages. The raw-material palette is thus diversifying, aligning elasticity, moisture-management, and circularity to different end-user imperatives while cushioning the Italy textiles market from monolithic dependency on any single polymer.

By Process: Woven Tradition Faces Non-woven Innovation

Woven fabrics represented 55.05% of the Italy textiles manufacturing market size in 2025 because heritage mills anchor luxury apparel supply chains. Jacquard looms in Como and worsted lines in Biella give Italian suiting its unmistakable hand. Nonetheless, non-woven processes are projected to grow 4.52% CAGR, commandeering filtration, hygiene, and automotive spaces where functionality trumps drape. Spunbond polypropylene from Soft N.W. aligns with Euro-7 cabin-air directives, while melt-blown media answer healthcare respirator demand.

Knitted goods ride athleisure and circular knitting trends; Italian vendors add AI-driven defect detection to minimize returns. Spacer fabrics and 3D weaving unlock lightweight sub-assemblies for aerospace seating. Even traditional weavers install multi-shuttle Jacroots that toggle patterns mid-run, enabling small-lot luxury orders. The competitive theater thus shifts toward flexible manufacturing, where process choice becomes a strategic lever rather than a legacy constraint.

Geography Analysis

The North-East captured 34.30% of 2025 revenue, powered by Veneto’s export apparatus that channels Italian fabrics to France, Switzerland, and Spain. Clusters near Vicenza deploy multi-generational skill sets and dense supplier networks, shrinking lead times and inventory risks. At the same time, the region invests in solar roofs and biomass boilers to dilute energy volatility.

South & Islands, historically peripheral, is forecast to post a 4.29% CAGR through 2031. Catalysts include OVS Group’s USD 36 million circular hub in Puglia, designed to recondition 15 million garments annually, and EU Just Transition funds earmarked for Sardinia’s depopulated mill towns. Lower real-estate costs lure start-ups testing regenerative dyeing and 3D knitting for on-demand collections. The pipeline of trained labor from regional fashion schools further counters northern wage escalation.

North-West regions such as Lombardy and Piedmont sustain high-value wool and machinery exports, while Milan’s fashion week keeps the global spotlight. Central Italy, led by Tuscany, doubles down on leather accessories but deploys PNRR grants to retrain redundant artisans in digital prototyping. The geographic spread indicates a recalibration rather than a zero-sum game; mature hubs refine premium volumes while emerging areas absorb greenfield projects, collectively broadening the footprint of the Italy textiles market.

Regulatory Landscape

Italy’s textile manufacturers work under EU-wide product and sustainability requirements, with additional national implementation measures. For core compliance, Regulation (EU) 1007/2011 on fiber naming and labeling is enforced through market-surveillance and inspection channels, including local Chambers of Commerce, which affects documentation practices for both domestic sales and exports.

Environmental and industrial-policy requirements are tightening around circularity and supply-chain transparency. Italy is advancing an Extended Producer Responsibility (EPR) framework for textiles, footwear, and accessories under the Ministry of Environment and Energy Security (MASE), while the Ministry of Enterprises and Made in Italy (MIMIT) has activated support measures for the sector’s ecological and digital transition. Key anchors include a ministerial decree dated 23 January 2025 reserving EUR 100 million for development programs tied to strategic textile and fashion supply chains, and MIMIT’s 26 February 2025 directive on applications for measures supporting natural and recycled textile fibers (and leather tanning), with an application window opening on 3 April 2025.

Value Chain Analysis

Italy’s textile value chain is structured around specialized industrial districts and a dense SME supplier base, with production moving from fibers and yarns into weaving, knitting, and non-wovens, then into dyeing, finishing, and conversion into apparel, home, and industrial end-uses. District-style integration supports short lead times for premium wool and silk (Biella and Como), and it also strengthens circular feedstock loops in recycling-centric hubs, including Prato, where downstream brands and converters increasingly require traceability tools and auditable process data to meet buyer compliance and authentication needs.

Constraints are most visible in energy-intensive wet processing, workforce availability, and the ability of smaller firms to fund digital upgrades. Sector-level initiatives are increasingly influencing how capabilities spread across tiers. In February 2025, Confindustria Moda and trade unions signed the Rome Declaration to prioritize innovation, sustainability, circularity, and training, and in June 2026 Confindustria Moda presented an AI adoption program with AI4I and academic partners to accelerate deployment across the fashion and textile supply chain. These initiatives, together with MIMIT incentives for eco-digital transition, shape supplier selection, technology procurement (automation, metering, and data capture), and consolidation dynamics as larger players and platform groups absorb specialist capacity to offer end-to-end compliance-ready supply.

Competitive Landscape

Roughly 45,000 firms populate the Italy textiles market, and 82% employ fewer than 10 people, creating a tapestry of micro-specialists. Yet consolidation is accelerating: Piacenza Group stitched together six wool mills, preserving heritage brands but pooling capex for automation. Such roll-ups seek scale to justify ESG audits and to bargain for renewable-energy PPAs.

Private equity is active; Glickman Capital bagged an 85% stake in cashmere label Malo, signaling foreign appetite for Italian IP even amid cost headwinds. Quadrivio’s Industry 4.0 Fund snapped up Soft N.W. to ride non-woven demand, while Elvaston formed Textile Solutions Group around ERP and CAD assets to service digitalization mandates. These moves reposition Italy from a mere contract-manufacturing base to a tech-enabled innovation corridor.

Start-ups target white spaces like bio-materials and recycling. SQIM scales mycelium composites; Vesti Solidale runs Europe’s largest textile-waste hub at 20,000 tons annual capacity; and Certilogo powers 540 million digital passports, monetizing data analytics for brands. The top five groups now control about 28% of national output, signaling moderate concentration but plenty of runway for niche disruptors.

Italy Textile Manufacturing Industry Leaders

-

Marzotto Group

-

Albini Group

-

Miroglio Group

-

RadiciGroup

-

Candiani Denim

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven investment creates room for Italian mills and converters that can package performance, traceability, and circularity into scalable offerings. The EU’s move toward product-level information, including Digital Product Passport rollouts referenced in the report context, and Italy’s textile EPR direction increase demand for verified fiber content, accurate labeling, and auditable supply-chain data. This strengthens the position of solution providers for digital authentication and tagging, as well as mills that can supply standardized datasets to brand customers. On the policy front, MIMIT’s measures for the transformation of natural and recycled textile fibers, including the application terms set in February 2025 and the application window opening on 3 April 2025, give SMEs a defined route to finance upgrades that improve recycled-content capability and waste reduction.

Technology modernization is another clear opportunity area for the market. In June 2026, Durst Group committed EUR 20 million to create “Durst Como,” an industrial and technology hub for digital textile printing in the Como district, which supports Italy’s emphasis on higher-value finishing and customization. Alongside this, trade-body coordination is also shaping supply-chain digitization: Confindustria Moda and AI4I launched an AI-integration program (presented in June 2026) focused on experimentation and training, while ACIMIT highlighted innovation and sustainable transition priorities in the 2026-2027 biennium as the machinery ecosystem prepares for ITMA 2027. Together, these efforts point to demand for energy-efficient processing, automated quality control, faster sampling, small-lot production, and circular sorting-to-spinning pathways already being piloted in Italian districts.

Recent Industry Developments

- July 2026: Ferraro S.p.A. completed the acquisition of the Finishing business unit from Cibitex, expanding its portfolio in textile finishing machinery. The deal strengthens Ferraro’s surface-treatment and finishing technology offering, supporting customers that are upgrading plants for efficiency and compliance-driven process control.

- June 2026: Durst Group launched the Durst Como project, a EUR 20 million investment to build a new industrial and technology hub in Como dedicated to digital textile printing. The project deepens advanced printing capacity in the Como silk district and supports shorter runs and customization, aligning with premium fashion supply-chain requirements.

- March 2025: OVS Group brought a new technology and circular-economy hub online in Puglia after investing EUR 33 million (USD 36.0 million) in a 15,000 square meter complex that can refresh up to 70,000 garments per day. The facility increases domestic capacity for reconditioning and resale-oriented workflows, reinforcing circular models that reduce virgin fiber demand and support EPR-era collection and reuse systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers textile manufacturing activity in Italy, starting from fiber and yarn processing through fabric production. It is measured in value terms for local industry output sold into end-use demand.

Scope exclusions: It does not include downstream apparel brand retailing, and it does not count pure trading of imported finished garments where no manufacturing value is added in Italy.

Segmentation Overview

-

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others (Protective, Sports Textiles, etc.)

-

By Raw Material

-

Natural Fibers

- Cotton

- Wool

- Silk

-

Synthetic Fibers

- Polyester

- Nylon

- Rayon / Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

-

Natural Fibers

-

By Process / Technology

- Woven

- Knitted

-

Non-woven

- Spunlaid (Spunbond / Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

-

By Geography

- North-West (Lombardy, Piedmont, Liguria, Aosta)

- North-East (Veneto, Trentino-AA, Friuli-VG, Emilia-Romagna)

- Central (Tuscany, Marche, Umbria, Lazio)

- South & Islands (Campania, Apulia, Sicily, Sardinia, Others)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the industry boundary, align definitions with standard industrial classifications, and build the first view of output and demand signals for textiles made in Italy. We mainly relied on public statistical series and policy releases to understand production direction, export exposure, and the cost items that move prices over time.

Sources referenced included, for example, Italian national statistics releases, Eurostat structural business statistics, UN Comtrade trade flows, OECD industry and price indicators, and trade association publications for textiles and fashion manufacturing. We then reviewed company annual reports, investor presentations, and reputable business press. Where useful, paid subscriptions for company financials and shipment-level trade databases were used to cross-check revenue pools and unit value ranges. These desk sources are not exhaustive, and we also reviewed additional public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on manufacturers, distributors, machinery and chemical input participants, and industry observers who track Italy-specific production clusters. In interviews and surveys, we tested volume drivers, utilization swings, and pricing behavior by fabric type, and we assessed how often the operational plan runs domestic shipments versus export-led output. The respondent input was then used to refine assumptions that desk sources could not fully explain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 28% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of Italy textile output using production and trade signals, then adjusts for import intensity and export share so the value ties back to what is produced within the country. In parallel, we corroborated totals with selective bottom-up checks, such as sampled manufacturer revenue ranges, channel checks on fabric shipments, and ASP times volume sanity tests for key fabric families, before final totals were locked.

Key model inputs included textile production indices, export and import values by textile category, and capacity utilization commentary gathered in primary discussions. We also tracked energy and key input cost movements that influence pricing, and we monitored shifts in end-use demand such as home textiles and technical applications. Forecasting used scenario analysis supported by trend smoothing, where price progression and volume recovery were treated separately, so the model did not overstate growth when only ASPs rise. Where bottom-up data was thin for small private firms, gaps were handled through consistent proxies based on output mix and typical price bands, and these were validated in interviews.

Data Validation & Update Cycle

Validation was done through multiple checks, including reconciling modeled value with trade balances, testing implied unit values against observed ranges, and reviewing year-on-year swings against known macro and sector signals. When results looked unusual, assumptions were reopened and targeted re-contacts were triggered to confirm what changed in volumes, pricing, or mix.

A second analyst review is completed before sign-off, and calculations are checked for currency consistency and timing alignment. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Italy Textile Manufacturing Industry Study Market Size Compared With Other Published Estimates

Published numbers for Italy textile manufacturing often do not match because they use different boundaries for what counts as textiles, they apply different currency timing, and they do not always separate volume change from price change in the same way. Differences also show up when a study mixes manufacturing value with downstream fashion and apparel revenues, which can inflate the apparent market.

In this study, the refresh cadence and the way annual average exchange rates and ASP movements are re-checked against trade unit values are major drivers of the final value. These controls are applied consistently in Mordor Intelligence to avoid overstating growth during price-led years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.32 B (2025) | |

| Industry Publisher A | USD 27.20 B (2025) | Uses a broader textile market framing that can blend manufacturing with downstream categories. The pricing build often assumes smoother ASP increases without checking implied unit values against trade data in the same year. |

| Research Publisher B | USD 7.87 B (2022) | Anchors to an earlier base year and a narrower definition that appears closer to a sub-scope of textile activity. The currency timing plus limited validation signals can compress the value versus a full fiber-to-fabric manufacturing view. |

Overall, the spread in published values is mainly explained by year selection, what activities are counted inside textiles, and how price progression is converted into USD. By tying the model to observable production and trade signals, and then stress-testing with interview-led checks, the resulting number stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the Italy textiles market in 2026?

The Italy textiles market size stands at USD 31.3 billion in 2026 with a 3.22% CAGR outlook to 2031.

Which application category is growing fastest?

Industrial/Technical Textiles is expected to log a 4.66% CAGR through 2031, outpacing fashion and home segments.

What region is expanding quickest inside Italy?

The South & Islands region shows the highest forecast CAGR at 4.29% because of new circular hubs and lower operating costs.

Why are non-wovens gaining share?

Non-woven fabrics meet demand for filtration, hygiene, and automotive components, driving a 4.52% CAGR that challenges woven dominance.

How is regulation shaping investment?

EU Ecodesign rules and Digital Product Passports push mills to adopt smart machinery and traceability systems, unlocking tax credits and premium contracts.

What is driving synthetic fiber growth?

Recycled polyester and bio-based alternatives align with circularity targets, helping synthetic fibers maintain 42.12% market share and 5.02% CAGR.

Page last updated on: