Italy SLI Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

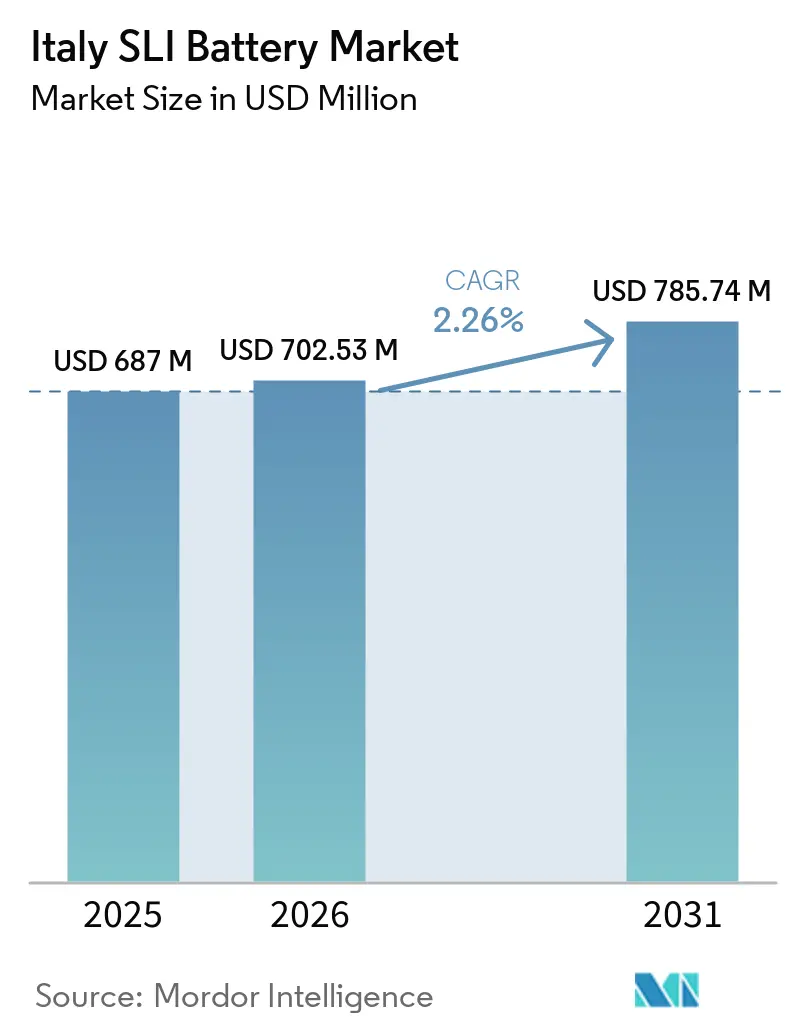

| Base Year Market Size (2025) | USD 687 Million |

| Market Size (2026) | USD 702.53 Million |

| Market Size (2031) | USD 785.74 Million |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

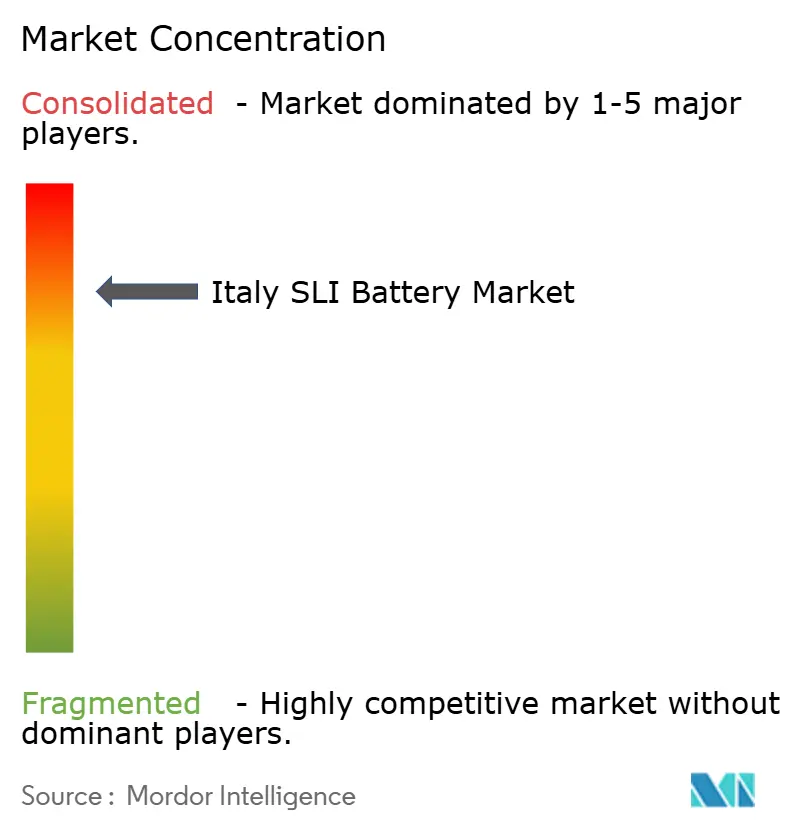

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy SLI Battery Market Analysis by Mordor Intelligence

The Italy SLI Battery Market size is expected to grow from USD 687 million in 2025 to USD 702.53 million in 2026 and is forecast to reach USD 785.74 million by 2031 at 2.26% CAGR over 2026-2031.

Modest topline growth conceals a shift toward advanced chemistries, tighter circular-economy rules, and regional manufacturing advantages. Italy’s 41 million-unit vehicle parc is aging, so replacement demand remains resilient even as new-car sales slow. AGM batteries are gaining momentum because start-stop systems surpassed 68% penetration in European light vehicles by 2024, and distributors are recalibrating SKU assortments to match that trend. Meanwhile, carbon-footprint labeling under EU Regulation 2023/1542 is tilting procurement in favor of domestic suppliers that can document lower Scope 3 emissions, a point that Italian producers such as FIAMM and Midac are already marketing. At the same time, lithium-ion auxiliary batteries, battery-passport compliance costs, and volatile lead prices weigh on margins, producing a bifurcated market in which well-capitalized manufacturers expand, but smaller distributors feel pressure.

Key Report Takeaways

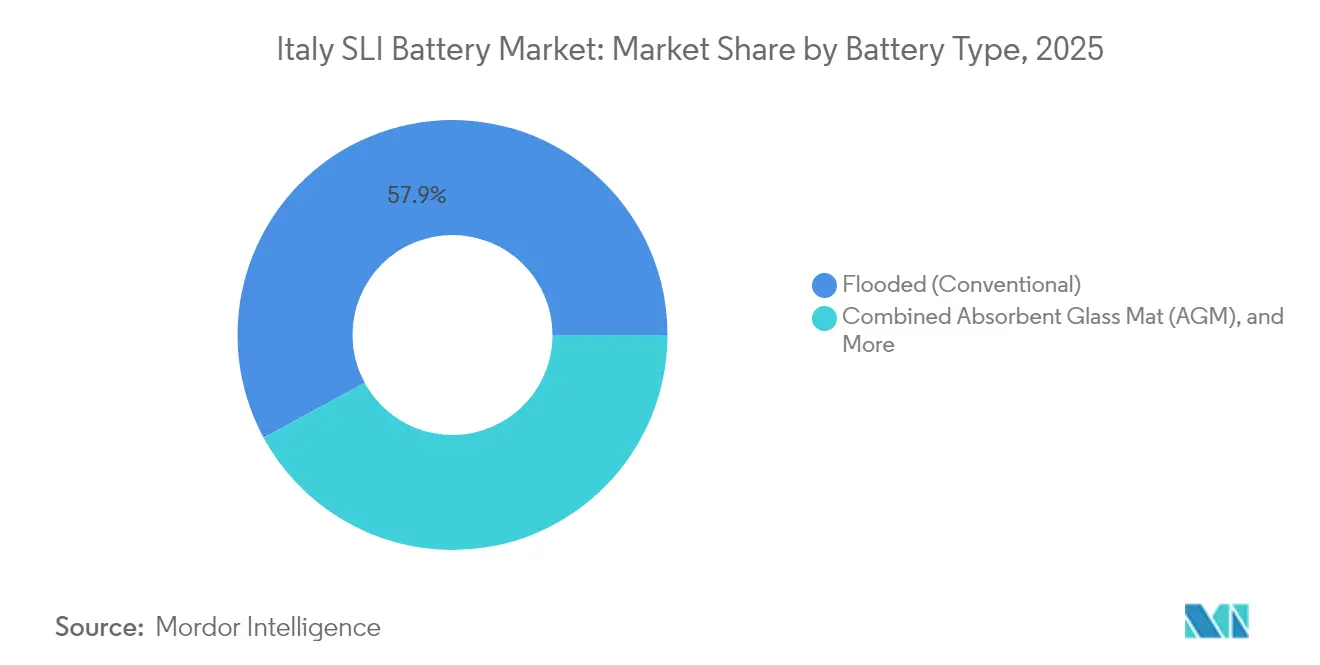

- By battery type, flooded designs held 57.92% share of the Italy SLI battery market in 2025, while AGM technology is advancing at a 6.31% CAGR through 2031.

- By voltage, 12-volt units dominated with 69.65% share in 2025; above-60-volt systems are on track for a 6.85% CAGR over the forecast horizon.

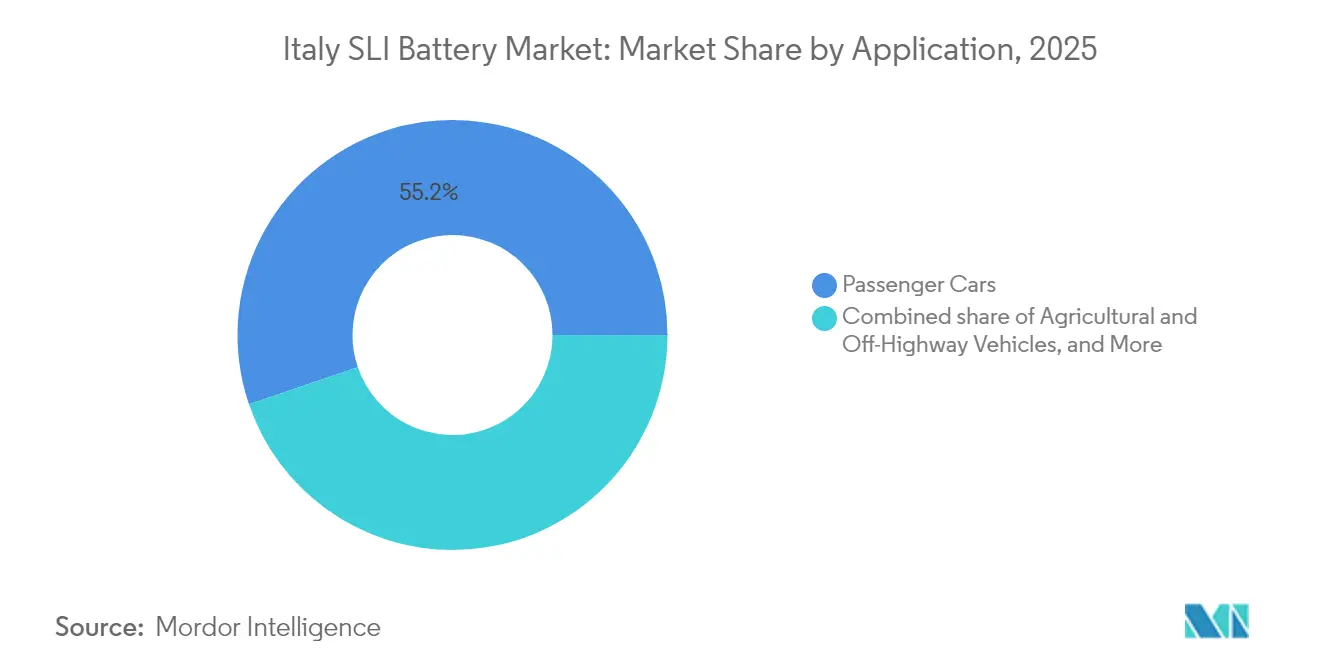

- By application, passenger cars accounted for 55.22% of demand in 2025, whereas agricultural and off-highway vehicles are forecast to post a 5.78% CAGR to 2031.

- Lombardy led national revenues in 2025, and Sardinia is expected to show the fastest growth thanks to new recycling and battery manufacturing investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Italy contributing to the overall trajectory. The outlook on worldwide sli battery market reflects how these are expected to evolve collectively.

Italy SLI Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vehicle-parc & replacement demand | +0.6% | National, concentrated in Lombardy, Lazio, Piedmont | Medium term (2-4 years) |

| Rising AGM/EFB adoption in start-stop cars | +0.8% | National, with OEM-driven uptake in Turin, Milan assembly clusters | Short term (≤ 2 years) |

| Micro-hybrid retrofit boom in urban fleets | +0.4% | Urban centers (Milan, Rome, Turin, Naples) | Medium term (2-4 years) |

| EU circular-economy push for lead recycling | +0.3% | EU-wide, with Italian recycling hubs in Portovesme, Brescia | Long term (≥ 4 years) |

| Carbon-footprint labelling favours local supply | +0.2% | National, benefiting Veneto and Lombardy manufacturing sites | Medium term (2-4 years) |

| Expansion of automotive aftermarket e-commerce | +0.3% | National, accelerating in Northern and Central regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing vehicle-parc & replacement demand

Italy’s 41 million-unit parc, averaging 13 years in age, generates a deep pool of batteries nearing end-of-life. Slow fleet turnover, new registrations equal only 3-4% of total parc, means flooded batteries installed before 2015 are now cycling through second or third replacements. The stability of this demand segment shields the Italy SLI battery market from abrupt volume declines even as EV adoption lags Northern Europe. Winter cold-cranking failures rise sharply in batteries older than five years, prompting retailers to promote diagnostic checks and seasonal discounts.[1]FIAMM, “Corporate Presentation 2025,” fiamm.com

Rising AGM/EFB adoption in start-stop cars

Start-stop systems topped 68% penetration in Europe by 2024, and Italian OEMs mandate AGM or EFB fitment on new micro-hybrid platforms. As these vehicles age, aftermarket replacements are set to accelerate, favoring AGM chemistry that tolerates deep cycling. Exide’s dual-terminal AGM B24 series widened fitment coverage by up to 1 million units, underscoring the priority manufacturers place on versatility. Distributors must therefore invest in AGM stocking, new racking, and staff training to capture the revenue upswing.

Micro-hybrid retrofit boom in urban fleets

Low-emission zones in Milan, Rome, and Turin are prompting fleet operators to retrofit vans with micro-hybrid kits that demand high-cycle AGM batteries. Frequent engine restarts and regenerative braking stress conventional flooded designs, so AGM remains the chemistry of choice. While the retrofit market is fragmented, contract awards hinge on warranty length and downtime-savings calculations. Suppliers that bundle batteries with mobile installation win share among last-mile operators looking to optimize the total cost of ownership.[2]Clarios, “Start-Stop Battery Adoption Report,” clarios.com

EU circular-economy push for lead recycling

EU Regulation 2023/1542 sets recycled-content thresholds of 6% lead by 2031 and 12% by 2036. Because lead-acid batteries already achieve more than 90% recycling rates, Italian recyclers in Portovesme and Brescia enjoy a head start. Clarios’ acquisition of Ecobat plants in Germany and Austria extends a vertically integrated model that mitigates lead-price volatility and ensures secure feedstock. Ongoing R&D into bipolar plates and carbon-enhanced grids will further raise energy density and broaden lead-acid applicability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Li-ion 12V auxiliaries gaining share | -0.5% | National, with early adoption in premium and EV segments | Medium term (2-4 years) |

| Shrinking ICE production under 2030 targets | -0.4% | National, concentrated in Turin and surrounding OEM clusters | Long term (≥ 4 years) |

| Battery-passport compliance cost for SMEs | -0.2% | National, disproportionately affecting SME distributors and recyclers | Short term (≤ 2 years) |

| Lead-scrap price volatility & export curbs | -0.3% | EU-wide, with acute impact on Italian recyclers in Portovesme, Brescia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Li-ion 12 V auxiliaries gaining share

EUROBAT projects a 50/50 split between lead-acid and lithium-ion in 12 V auxiliary batteries by 2030 as ADAS and infotainment loads soar. Lithium-ion offers faster recharge and lighter weight, but lead-acid holds a 60-70% cost edge and better cold-cranking at sub-zero temperatures. Italian manufacturers are racing to introduce Thin-Plate Pure Lead and carbon-enhanced variants to hold ground in this critical niche.

Shrinking ICE production under 2030 targets

EU rules demand 55% lower CO₂ emissions by 2030 and a full ICE phase-out by 2035. Stellantis’ Turin production already fell 63% in H1 2024, reducing OEM demand for SLI batteries. Heavy commercial vehicles and agricultural equipment remain ICE-centric, so suppliers are tilting product roadmaps toward those segments to offset lost passenger-car volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: AGM Outpaces Flooded in Start-Stop Wave

AGM already serves the majority of start-stop cars and is forecast to expand at a 6.31% CAGR, compared with the Italy SLI battery market’s overall 2.26% growth. Flooded batteries still dominate replacement sales for vehicles built before 2015, but their share will erode as the AGM replacement wave matures. EFB provides a mid-price option for fleet operators who need higher cycle life than flooded units can provide, yet balk at full-AGM pricing.

The Italy SLI battery market size for AGM units is projected to rise from USD 227 million in 2025 to nearly USD 327.7 million by 2031 as start-stop penetration deepens. Exide’s M3-rated AGM B24 launch shows how manufacturers are broadening terminal options to trim SKU counts for distributors. Meanwhile, flooded designs will persist in cost-pressured Southern regions but decline nationally as consumer education on AGM benefits increases.

By Battery Voltage: 12 V Dominates, 48 V and Above-60 V Accelerate

Twelve-volt batteries captured 69.65% of Italy's SLI battery market share in 2025, reflecting universal SLI architecture. Above-60-V segments, however, will post a 6.85% CAGR through 2031 as data-center UPS, industrial trucks, and telecom towers migrate toward higher-voltage strings to cut cabling losses.

Italy SLI battery market size attributed to 48-V modules is poised to climb from USD 34 million in 2025 to USD 50.5 million by 2031, buoyed by mild-hybrid commercial vehicles. Clarios' EUR 200 million EMEA investment includes tooling for 48-V assemblies, indicating confidence that lead-acid can compete on cost and safety versus lithium-ion in this voltage band. Above-60-V systems will leverage Italian logistics growth, where electric forklifts favor rugged lead-acid traction blocks for round-the-clock operations.

By Application: Passenger Cars Lead, Agricultural Vehicles Surge

Passenger cars delivered 55.22% of 2025 revenues, yet their share will inch downward as tractors, harvesters, and construction machinery experience faster growth. Agricultural and off-highway units are forecast to record a 5.78% CAGR thanks to electrification pilots and replacement of aging starter batteries, especially in Lombardy and Emilia-Romagna.

Italy SLI battery market size for agricultural equipment is expected to advance from USD 56 million in 2025 to USD 78.4 million by 2031. Commercial light-vehicle fleets also contribute, as last-mile delivery vans in Milan and Rome retrofit micro-hybrid systems. Industrial motive power and stand-by uses round out demand, offering suppliers a hedge against cyclical swings in automotive registrations.

Geography Analysis

Northern regions dominate production because battery plants cluster near Turin, Milan, and Verona. Access to skilled labor and Europe-wide rail corridors allows FIAMM, Midac, and Clarios to export efficiently to Spain, France, and North Africa, reinforcing economies of scale. Lombardy alone accounted for roughly one-quarter of 2025 national turnover, making it the keystone of the Italy SLI battery market.

Central and Southern regions, especially Lazio and Campania, drive aftermarket consumption thanks to dense vehicle populations and warmer climates that shorten the service life of starter batteries. These areas rely on logistics pipelines from Northern warehouses, so same-day delivery promises from e-commerce platforms are reshaping stock-holding policies. Sardinia moves from laggard to hotspot as the Portovesme Hub joint venture between Li-Cycle and Glencore paves the way for a 50,000-70,000 tonne black-mass facility, giving the island a recycling anchor that could rebalance national supply chains.

Export opportunities remain critical. Under EU carbon-footprint rules, “Made in Italy” batteries shipped to Spain or Greece carry lower embedded emissions versus Asian imports, a differentiator Italian brands highlight in bids for municipal bus and rail contracts. This geographic blend, Northern production, Central-Southern consumption, and Mediterranean exports, adds complexity but also strategic resilience to the Italy SLI battery market.

Analysis of the sli battery market by Mordor Intelligence spans multiple other regional evaluations across Europe and Middle East and Africa, supported by country-level insights for France, United Kingdom, China, United States, India, and Germany, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Italy SLI Battery Market is higly concentrated. FIAMM’s sale to AURELIUS in August 2025 signals private-equity confidence that rationalizing Italian operations can unlock value, especially under EU rules favoring local sourcing. Clarios’ 50% EMEA AGM capacity expansion by 2026 will intensify price competition, forcing rivals to sharpen value propositions around warranty terms and service uptime.

Exide is hedging with lithium-ion know-how acquired via BE-Power, anticipating future share shifts in 12-V auxiliaries. Midac, though smaller, leverages proximity to Verona’s metal-processing cluster to secure raw materials and runs R&D with Enel X on recycling flows that can meet recycled-content mandates. Vertical integration through recycling is emerging as a key moat; Clarios’ Ecobat asset purchases tighten its feedstock loop and reduce exposure to lead-price spikes.

Scale also matters for regulatory compliance. Battery-passport IT systems cost six-figure sums; large players amortize them, but SMEs may exit or sell. Consequently, the Italy SLI battery industry is likely to consolidate further between 2026 and 2028 as the February 2027 passport deadline approaches. Niche opportunities persist in UPS and telecom backup, where Italian suppliers’ fast response and customization offset volume disadvantages.

Italy SLI Battery Industry Leaders

FIAMM Energy Technology S.p.A.

Clarios

Exide Technologies

Midac SpA

EnerSys

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Haiki has acquired Ecobat's battery and polypropylene recycling operations in Italy, encompassing facilities in Marcianise, Paderno Dugnano, and Bologna. This move holds significant implications for Italy's lead and secondary-lead supply chain.

- May 2025: ALBA, the annual advanced lead battery workshop, took place in Turin, featuring technical sessions on AGM and lead-acid R&D, alongside networking opportunities for Italian stakeholders.

- March 2024: Ahlstrom unveiled its cutting-edge Absorbent Glass Mat (AGM) battery separator platform, now locally produced in Turin, Italy.

- July 2024: Ferrari, renowned for its luxury sports cars, introduced two novel warranty extension programs. Under the 'Warranty Extension Hybrid' and 'Power Hybrid' initiatives, Ferrari offers owners the opportunity to replace the high-voltage SLI battery packs (HVB) in the eighth and 16th year of their vehicle's lifespan.

Italy SLI Battery Market Report Scope

SLI (starting, lighting, and ignition) batteries are lead-acid batteries used in vehicles to start the engine and power the lighting and ignition systems. They provide a high burst of current needed to start the engine, after which the alternator takes over. SLI batteries are known for delivering quick, strong bursts of energy but are not meant for deep discharge or prolonged power delivery.

The Italy SLI battery market is segmented by battery type, battery voltage, and application. By battery type, the market is segmented into flooded, enhanced flooded, absorbent glass mat (AGM), and gel cell VRLA. By battery voltage, the market is segmented into up to 12V, 12V, 48V, and above 60V. By application, the market is segment into passenger cars, light commercial vehicles, heavy commercial vehicles, two-/three-wheelers, agricultural & off-highway vehicles, industrial motive power (forklifts, material-handling), and stand-by/backup (telecom, UPS). For each segment, market sizing and forecasts are presented on a value (USD) basis.

| Flooded (Conventional) |

| Enhanced Flooded (EFB) |

| Absorbent Glass Mat (AGM) |

| Gel Cell VRLA |

| Up to 12 V |

| 12 V |

| 48 V |

| Above 60 V |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-/Three-Wheelers |

| Agricultural and Off-Highway Vehicles |

| Industrial Motive Power (Forklifts, Material-Handling) |

| Stand-by/Backup (Telecom, UPS) |

| By Battery Type | Flooded (Conventional) |

| Enhanced Flooded (EFB) | |

| Absorbent Glass Mat (AGM) | |

| Gel Cell VRLA | |

| By Battery Voltage | Up to 12 V |

| 12 V | |

| 48 V | |

| Above 60 V | |

| By Application | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Two-/Three-Wheelers | |

| Agricultural and Off-Highway Vehicles | |

| Industrial Motive Power (Forklifts, Material-Handling) | |

| Stand-by/Backup (Telecom, UPS) |

Key Questions Answered in the Report

How large is the Italy SLI battery market in 2026?

The Italy SLI battery market size is USD 702.53 million in 2026, with a forecast to reach USD 785.74 million by 2031.

Which battery chemistry is growing fastest in Italy?

AGM units are expanding at 6.31% CAGR because of widespread start-stop adoption in passenger and light-commercial vehicles.

Why are above-60-volt SLI systems important for Italy?

Higher-voltage lead-acid strings support industrial trucks, telecom towers, and data-center UPS platforms that demand modular, safe, and cost-effective backup.

How will EU battery-passport rules affect small distributors?

SMEs must invest EUR 50,000–200,000 in digital tracking systems, which may prompt consolidation or alliances with larger logistics partners.

What is driving SLI battery demand in agriculture?

Aging tractors and electrification pilots in farming regions are pushing annual growth of 5.78% in agricultural starter-battery sales through 2031.

Which regions host most Italian battery manufacturing?

Lombardy, Veneto, and Piedmont host the bulk of production thanks to proximity to automotive OEMs and established metallurgical supply chains.

Page last updated on: