Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

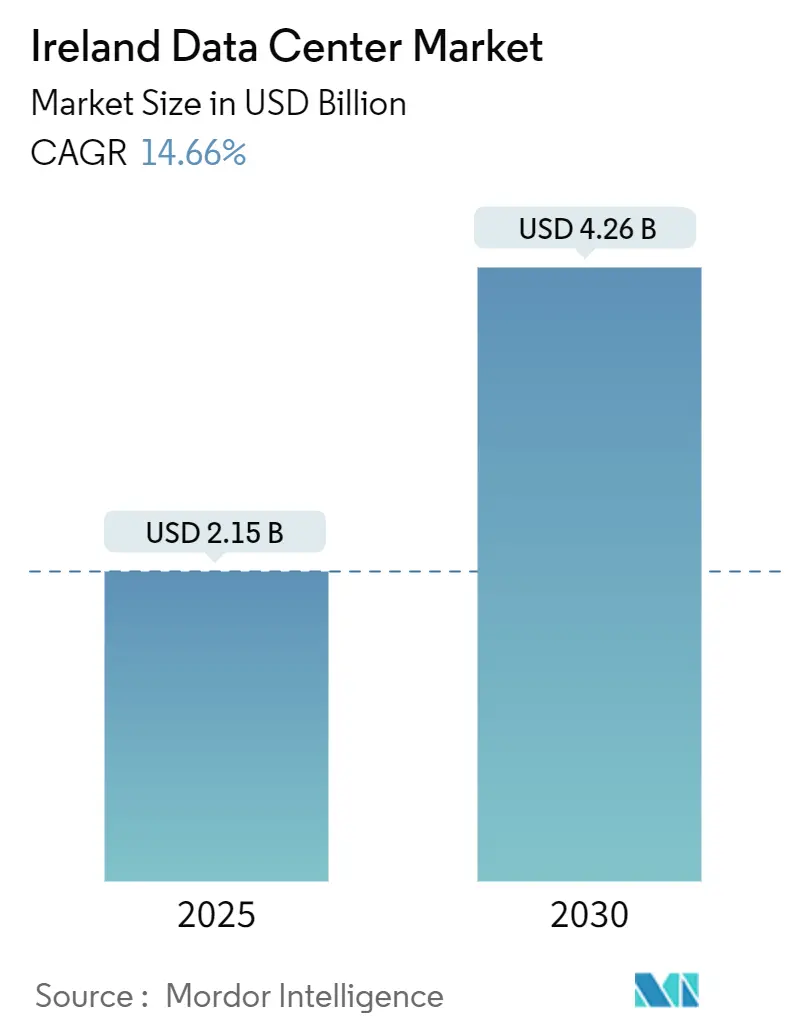

| Market Size (2025) | USD 2.15 Billion |

| Market Size (2030) | USD 4.26 Billion |

| Growth Rate (2025 - 2030) | 14.66% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ireland Data Center Market Analysis by Mordor Intelligence

The Ireland data center market size stands at USD 2.15 billion in 2025 and is forecast to reach USD 4.26 billion by 2030, expanding at a 14.66% CAGR over the period. The IT load capacity is expected to increase from 2.88 thousand MV in 2025 to 5.24 thousand MV in 2030, growing at a CAGR of 12.7%. The market segment shares and estimates are calculated and reported in terms of MW. Rapid hyperscale build-outs, deep subsea connectivity, and corporate tax advantages reinforce Ireland’s position as Europe’s third-largest hyperscale hub. Yet, electricity consumption already equals 21% of national demand, drawing regulatory scrutiny.[1]Sean Murray, “Report criticises Ireland’s ‘struggle to implement necessary systems’ to collate data centre information,” Irish Examiner, irishexaminer.com EirGrid’s moratorium on new Dublin grid connections until 2028 forces operators to evaluate regional sites even as latency-sensitive workloads still favour Dublin. Growth is further propelled by renewable power purchase agreements, liquid cooling adoption for AI workloads, and emerging edge deployments in Cork, Galway, and Limerick. Competitive dynamics pivot on sustainability credentials, with operators integrating waste-heat reuse, energy storage, and demand-response participation to secure planning approvals.

Key Report Takeaways

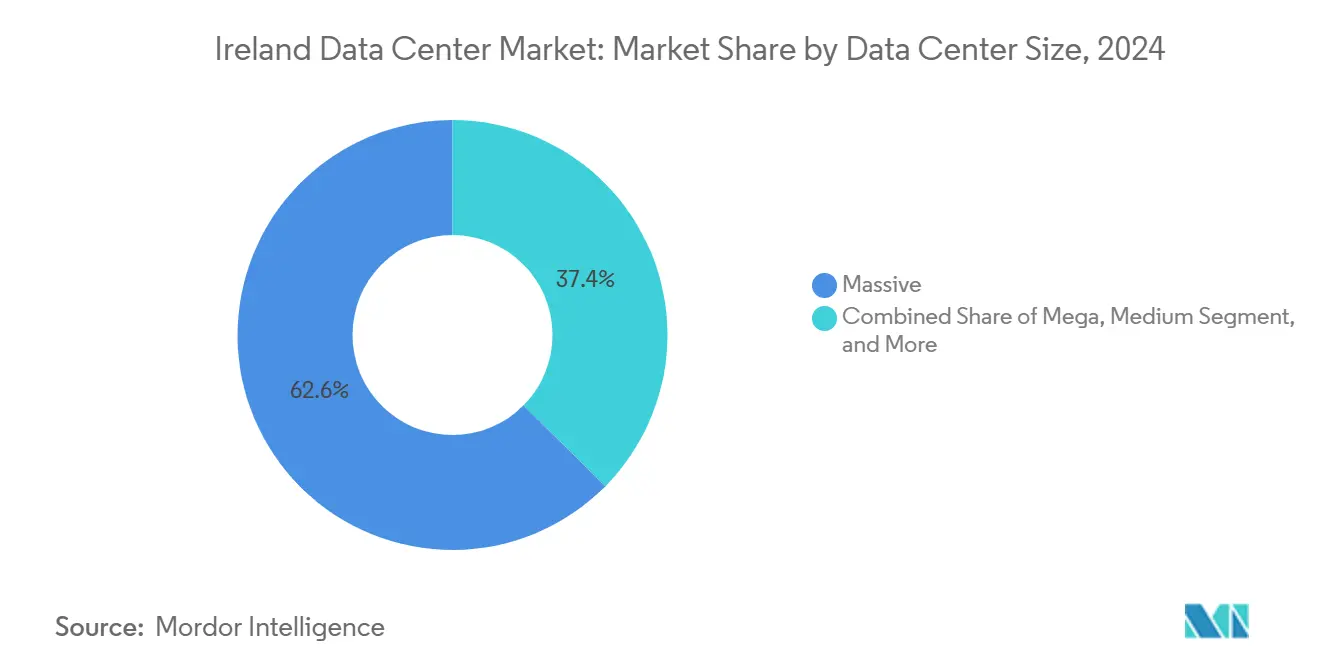

- By data center size, massive facilities led with 62.59% of Ireland data center market share in 2024, while edge deployments are projected to grow at a 13.30% CAGR through 2030.

- By tier type, Tier 4 infrastructures accounted for 82.53% of Ireland data center market size in 2024 and are advancing at a 14.10% CAGR to 2030.

- By data center type, hyperscale and self-built projects held 76.77% of Ireland data center market share in 2024; edge facilities recorded the fastest CAGR at 12.90% over the forecast horizon.

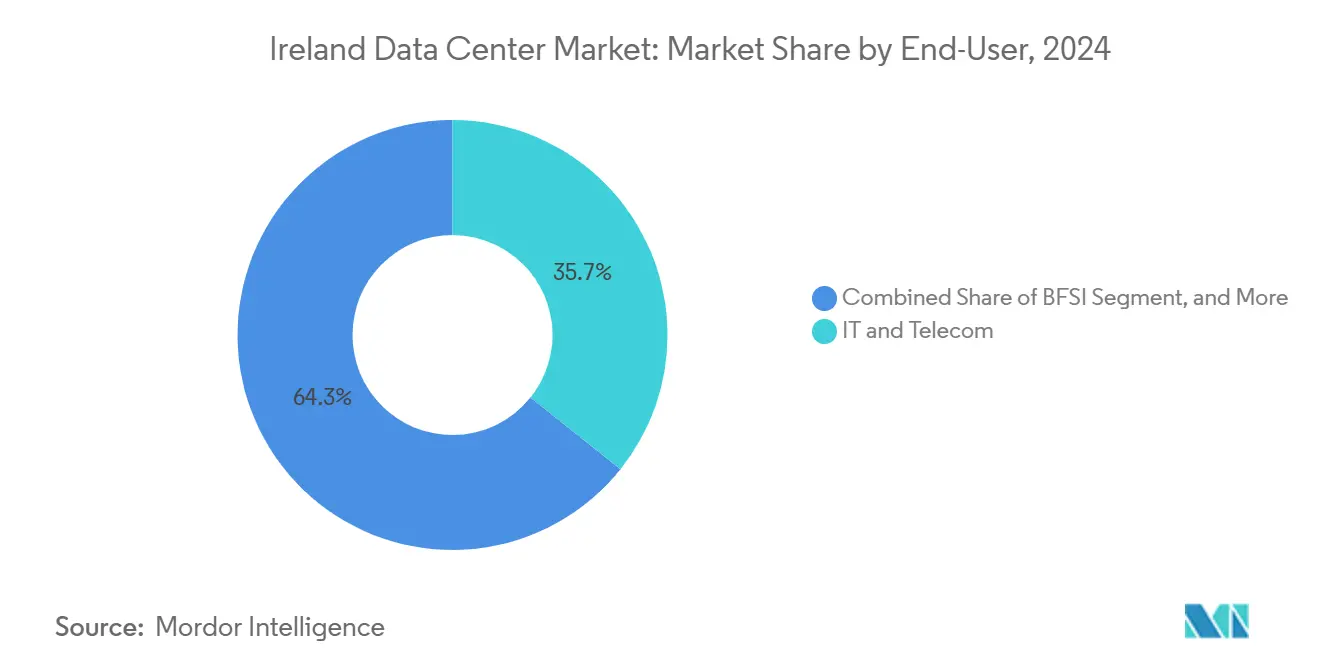

- By end user, IT and telecom captured 35.74% of the Ireland data center market in 2024, whereas BFSI is forecast to expand at a 13.18% CAGR to 2030.

- By geography, Dublin commanded 93.93% share of the Ireland data center market size in 2024, but the rest of Ireland is on track for a 14.21% CAGR through 2030.

Ireland Data Center Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate-tax incentives sustaining hyperscaler inflows | +2.80% | National, concentrated in Dublin | Long term (≥ 4 years) |

| Robust subsea-fiber ecosystem enabling ultra-low-latency routes | +2.10% | National, with Dublin as primary landing hub | Medium term (2-4 years) |

| Hyperscaler campus pipeline exceeding 1 GW by 2030 | +3.20% | Dublin region, expanding to midlands | Medium term (2-4 years) |

| Renewable-energy PPAs enhancing sustainability credentials | +1.90% | National, with focus on wind-rich western regions | Long term (≥ 4 years) |

| 5G-driven edge compute demand around Irish metros | +1.40% | Dublin, Cork, Galway metropolitan areas | Short term (≤ 2 years) |

| Waste-heat reuse mandates unlocking district-heating revenues | +0.90% | Dublin urban areas, expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Corporate-Tax Incentives Sustaining Hyperscaler Inflows

Ireland’s 15% effective corporate tax rate continues to attract cloud giants despite the 2024 increase from 12.5%.[2]European Commission, “Economic forecast for Ireland,” europa.eu Coupled with English-speaking talent and EU market access, the regime underpins long-term commitments such as Microsoft’s USD 500 million expansion at Grange Castle. Embedded capital investments create high switching costs, insulating operators from near-term policy shifts. Even potential U.S. protectionist measures are unlikely to trigger wholesale exits given latency constraints and sovereign data requirements. As a result, fiscal stability remains a cornerstone driver for the Ireland data center market.

Robust Subsea-Fiber Ecosystem Enabling Ultra-Low-Latency Routes

Eleven transatlantic cables land in Ireland, offering direct 60-millisecond round-trip latency to New York and resilient paths to mainland Europe. The 2024 Aqua Comms-Ciena 1.3 Tbps trial increased spectral efficiency by 15% and reduced power per bit by half, thereby extending capacity headroom.[3]Winston Qiu, “Aqua Comms and Ciena Trial 1.3 Tbps Wavelength,” Submarine Networks, submarinenetworks.com This deep connectivity enables U.S. cloud platforms to meet European General Data Protection Regulation compliance requirements without compromising performance. However, the United Nations flagged Irish waters as a strategic choke point, prompting government investment in cable-landing hardening. Sustained bandwidth upgrades cement Ireland’s role as a gateway node, reinforcing market expansion.

Hyperscaler Campus Pipeline Exceeding 1 GW by 2030

Pipeline projects clustered near Dublin’s Grange Castle exceed 1 GW of planned IT load, with Google seeking an additional 72,400 square meters adjacent to existing sites. Campus models deliver scale economies, shared utilities, and rapid capacity scaling. Yet local authorities rejected multiple applications in 2024-2025 over climate consistency concerns, illustrating the tension between growth and sustainability goals. The moratorium has redirected some builds to Offaly and Wicklow, but latency-sensitive workloads still demand Dublin adjacency. Resolution of planning bottlenecks will largely shape the Ireland data center market trajectory through 2030.

Renewable-Energy PPAs Enhancing Sustainability Credentials

Operators have signed more than 1 GW of wind and solar PPAs since 2022, led by Microsoft’s 900 MW and Amazon’s 115 MW deals. These PPAs unlock additional renewable builds in resource-rich western counties and help data centers maintain carbon-neutral pledges. A Friends of the Earth analysis noted that incremental wind generation since 2017 was wholly absorbed by data center demand, thereby limiting the displacement of fossil fuels. Regulators now propose on-site storage obligations to ensure grid-positive operation, pushing operators toward battery and hydrogen solutions that can further differentiate sustainability leadership.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electricity-grid capacity moratorium in Dublin corridor | -4.20% | Dublin metropolitan area | Medium term (2-4 years) |

| Escalating power prices and carbon-tax exposure | -1.80% | National, with higher impact on energy-intensive facilities | Short term (≤ 2 years) |

| Lengthy local-planning appeals delaying new builds | -2.10% | National, concentrated in Dublin and urban areas | Medium term (2-4 years) |

| Shortage of specialist contractors inflating project CAPEX | -1.30% | National, with acute impacts on complex builds | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electricity-Grid Capacity Moratorium in Dublin Corridor

EirGrid froze new high-density connections around Dublin through 2028 to safeguard grid stability. The halt strands committed capital, evident in Digital Realty’s idle halls awaiting power clearance. Hyperscalers tied to Dublin for latency and ecosystem benefits now consider hybrid builds in Offaly or Westmeath, adding network complexity and cost. Political support for AI competitiveness has sparked discussions on conditional exemptions that include large-scale battery storage, yet implementation timing remains uncertain. Until resolution, the moratorium is the single largest drag on the Ireland data center market.

Escalating Power Prices and Carbon-Tax Exposure

The Central Statistics Office reported a 20% rise in data center consumption to 6,334 GWh in 2024, tightening wholesale supply and pushing spot prices upward. Carbon taxes on backup diesel and gas generation reached EUR 120 per ton in 2025 (USD 135), inflating operating expenditure. Public backlash over parallel household tariff hikes raises policy risks that could impose further levies on large users. Operators turning to islanded gas turbines face higher carbon exposure, while grid-connected sites grapple with volatility that complicates long-term cost predictability. Together, rising energy costs compress margins and may defer non-critical expansions.

Segment Analysis

By Data Center Size: Massive Facilities Anchor Capacity While Edge Gains Momentum

Massive facilities captured 62.59% of Ireland data center market share in 2024, reflecting hyperscale clustering around Dublin. Edge deployments, however, exhibit a 13.30% CAGR that outstrips all other categories as telcos roll out 5G and enterprises pursue low-latency analytics. The Ireland data center market size for massive builds is projected to exceed USD 2.6 billion by 2030.

Edge nodes typically range from 1 MW to 5 MW and are surfacing in Cork, Galway, and Limerick, where local content caching reduces backbone traffic. Massive builds embrace liquid cooling to hit 120 kW rack densities, with KPMG estimating EUR 400,000 (USD 452,000) to EUR 600,000 (USD 678,000) premiums per MW for densified designs. The hybrid landscape reinforces Ireland data center market resilience by balancing centralized efficiency with distributed responsiveness.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Tier Type: Tier 4 Pre-eminence Reflects Uptime Imperatives

Tier 4 commanded 82.53% of Ireland data center market share in 2024, underscoring financial-grade expectations for 99.995% availability. The Ireland data center market size attributed to Tier 4 capacity is set to double by 2030 while sustaining a 14.10% CAGR.

Microsoft’s DB3 facility achieved a 1.13 power usage effectiveness, demonstrating that extreme resilience need not compromise efficiency. Regulatory moves to mandate grid-balancing will likely favour Tier 4 players already equipped with redundant power and storage systems, widening the performance and compliance gap with lower-tier competitors.

By Data Center Type: Hyperscale Supremacy Faces Proximity-Driven Edge Demand

Hyperscale and self-built projects held 76.77% share in 2024, translating to the majority of Ireland data center market capacity. The edge category posts a 12.90% CAGR, creating incremental opportunities for modular and containerized solutions.

Amazon’s dual-sized Dublin builds illustrate adaptive scaling where a 12,875 square meter hall handles core cloud services while a 1,445 square meter pod addresses latency-critical workloads. The co-existence of mega campuses and near-customer micro sites signals a maturing architecture and diversifies revenue streams across the Ireland data center industry.

By End User: IT and Telecom Dominate but BFSI Accelerates

IT and telecom contributed 35.74% of 2024 demand, anchored by multinational headquarters leveraging favourable tax regimes and connectivity. BFSI demonstrates the fastest 13.18% CAGR, buoyed by fintech growth and post-Brexit data residency requirements.

Equinix commissioned research indicating a proposed south Dublin build could yield EUR 200 million (USD 226 million) in economic value, largely from financial services interconnection. As regulatory frameworks around Open Banking tighten, BFSI workloads will intensify demand for low-latency, sovereign-compliant infrastructure, reinforcing the sector’s upward trajectory within the Ireland data center market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Hotspot: Dublin Dominance Meets Regional Catch-Up

Dublin accounted for 93.93% of Ireland data center market share in 2024, underscoring its entrenched role as the country’s digital capital. The city’s appeal stems from eleven transatlantic cable landings that deliver sub-70 millisecond round-trip latency to New York, dense interconnection campuses at Grange Castle, and a skilled technology workforce clustered around major cloud providers. This critical mass translates into network effects that lower peering costs and elevate service reliability, keeping hyperscalers and colocation firms firmly anchored near the capital. However, the 2021-2028 moratorium on new high-density grid connections has frozen fresh megawatt allocations, forcing operators like Digital Realty to idle built space until power is available. As a result, the Ireland data center market size tied exclusively to Dublin is approaching saturation even as demand for AI-ready capacity accelerates.

Yest of Ireland emerges as the fastest-growing hotspot with a projected 14.21% CAGR to 2030, supported by land availability, lower operating costs, and proximity to onshore wind resources that simplify renewable energy procurement. Counties Offaly and Wicklow lead this surge, where partnerships with utilities such as Bord na Móna bundle data center campuses with adjacent wind projects, helping new entrants satisfy grid-positive requirements proposed by regulators. Edge deployments in Cork, Galway, and Limerick further diversify geographic risk while enhancing user experience for latency-sensitive 5G applications. Nonetheless, regional builds must overcome fiber backhaul gaps and limited specialist labor pools, challenges that could temper near-term capacity rollouts if unaddressed. Balancing these headwinds, the Ireland data center market size allocated outside Dublin is poised to more than double by 2030, gradually reshaping an ecosystem long defined by a single metropolitan stronghold.

Geography Analysis

Dublin’s concentration remains unparalleled, controlling 93.93% of 2024 installed capacity thanks to eleven transatlantic cables, deep hyperscale clustering, and a specialized workforce. The moratorium complicates expansion yet also spurs innovations such as 30 MWh battery farms that provide grid services while safeguarding latency-critical workloads.

The rest of Ireland, led by Offaly and Wicklow, is projected for a 14.21% CAGR through 2030 as operators exploit land availability and renewable proximity. Statkraft’s wind farm paired with Microsoft’s PPA exemplifies symbiotic regional models that tackle both capacity and sustainability targets. However, gaps in dark fiber and skilled labour remain hurdles.

Secondary metros Cork, Galway, and Limerick attract edge deployments aligned with 5G rollouts, improving service quality for regional consumers and diversifying the Ireland data center market footprint. Continued public-private collaboration on fiber backbones and training programs will determine the pace at which non-Dublin nodes mature into self-sustaining ecosystems.

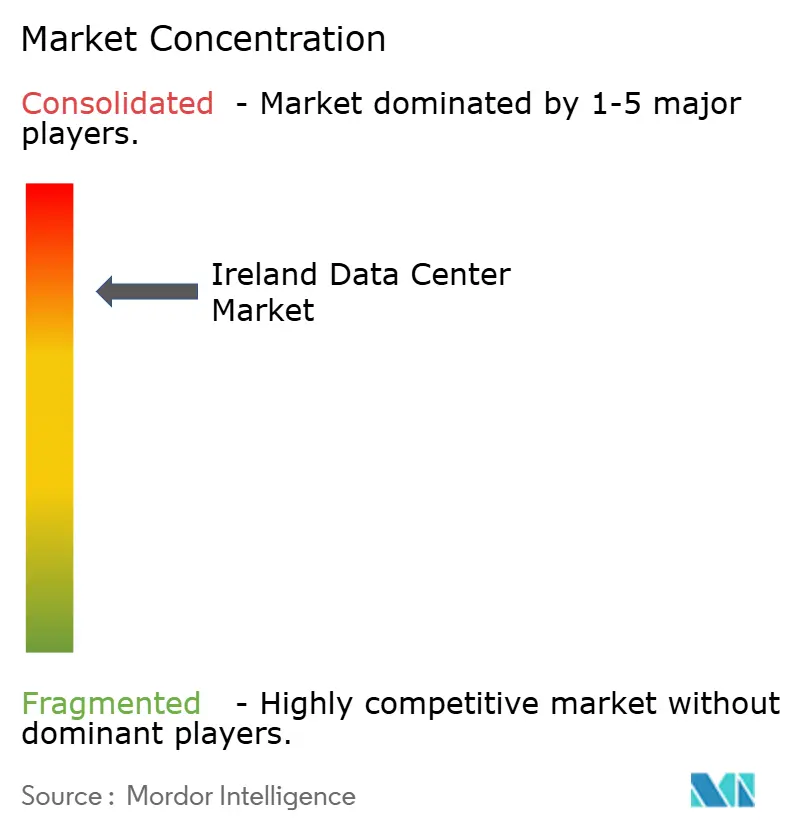

Competitive Landscape

The market exhibits moderate concentration; the top five providers hold roughly 75% of installed capacity. Digital Realty, Equinix, Microsoft, Amazon, and Google maintain flagship campuses in Dublin, leveraging first-mover scale and interconnection density. Vantage Data Centers’ 52 MW campus signals fresh capital inflows, while Echelon’s 200 MW Wicklow project targets spillover demand from the Dublin moratorium.

Strategic differentiation now revolves around energy innovation. Digital Realty piloted a 2.5 MWh lithium-ion battery system providing 15-minute ride-through and grid frequency response, unlocking potential revenue streams while meeting forthcoming regulatory obligations. Equinix expanded its xScale joint venture, integrating 10 MW of rooftop solar to offset Scope 2 emissions.

Regional challengers partner with utilities to bundle renewable generation and data center loads; Bord na Móna’s collaboration with Amazon exemplifies land-plus-power propositions that lower project risk. In edge markets, EdgeConneX and Cloudflare deploy micro-modules linked to national fiber rings, serving CDN and telecom customers seeking sub-10 millisecond latency. Competitive intensity is expected to rise as grid-positive mandates reward innovators able to combine digital and energy infrastructure expertise.[4]Rich Miller, “Microsoft Confirms Dublin Data Center Plans,” datacenterknowledge.com

Ireland Data Center Industry Leaders

-

BT Communications Limited (BT Group PLC)

-

Digital Realty Trust Inc.

-

EdgeConneX Inc.

-

Equinix Inc.

-

K2 Strategic Pte Ltd (Kuok Group)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Red Admiral DC Limited advanced pre-application planning for a large-scale facility in Westmeath with projected completion in 2028.

- June 2025: Taoiseach Micheál Martin endorsed continued data center growth to maintain AI competitiveness amid Dublin grid constraints.

- May 2025: European Commission Spring forecast highlighted Ireland’s vulnerability to U.S. trade policy shifts yet affirmed 3.4% GDP growth supported by tech exports.

- April 2025: EUR 1.5 billion Ennis data center project experienced delays attributed to bureaucratic inertia.

Ireland Data Center Market Report Scope

Dublin are covered as segments by Hotspot. Large, Massive, Medium, Mega, Small are covered as segments by Data Center Size. Tier 1 and 2, Tier 3, Tier 4 are covered as segments by Tier Type. Non-Utilized, Utilized are covered as segments by Absorption.

By Data Center Size

| Large |

| Massive |

| Medium |

| Mega |

| Small |

By Tier Type

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

By Data Center Type

| Hyperscale/Self-built | ||

| Enterprise/Edge | ||

| Colocation | Non-Utilized | |

| Utilized | Retail Colocation | |

| Wholesale Colocation | ||

By End User

| BFSI |

| IT and ITES |

| E-Commerce |

| Government |

| Manufacturing |

| Media and Entertainment |

| Telecom |

| Other End Users |

By Hotspot

| Dublin |

| Rest of Ireland |

| By Data Center Size | Large | ||

| Massive | |||

| Medium | |||

| Mega | |||

| Small | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Type | Hyperscale/Self-built | ||

| Enterprise/Edge | |||

| Colocation | Non-Utilized | ||

| Utilized | Retail Colocation | ||

| Wholesale Colocation | |||

| By End User | BFSI | ||

| IT and ITES | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

| By Hotspot | Dublin | ||

| Rest of Ireland | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- IT LOAD CAPACITY - The IT load capacity or installed capacity, refers to the amount of energy consumed by servers and network equipments placed in a rack installed. It is measured in megawatt (MW).

- ABSORPTION RATE - It denotes the extend to which the data center capacity has been leased out. For instance, a 100 MW DC has leased out 75 MW, then absorption rate would be 75%. It is also referred as utilization rate and leased-out capacity.

- RAISED FLOOR SPACE - It is an elevated space build over the floor. This gap between the original floor and the elevated floor is used to accommodate wiring, cooling, and other data center equipment. This arrangement assist in having proper wiring and cooling infrastructure. It is measured in square feet (ft^2).

- DATA CENTER SIZE - Data Center Size is segmented based on the raised floor space allocated to the data center facilities. Mega DC - # of Racks must be more than 9000 or RFS (raised floor space) must be more than 225001 Sq. ft; Massive DC - # of Racks must be in between 9000 and 3001 or RFS must be in between 225000 Sq. ft and 75001 Sq. ft; Large DC - # of Racks must be in between 3000 and 801 or RFS must be in between 75000 Sq. ft and 20001 Sq. ft; Medium DC # of Racks must be in between 800 and 201 or RFS must be in between 20000 Sq. ft and 5001 Sq. ft; Small DC - # of Racks must be less than 200 or RFS must be less than 5000 Sq. ft.

- TIER TYPE - According to Uptime Institute the data centers are classified into four tiers based on the proficiencies of redundant equipment of the data center infrastructure. In this segment the data center are segmented as Tier 1,Tier 2, Tier 3 and Tier 4.

- COLOCATION TYPE - The segment is segregated into 3 categories namely Retail, Wholesale and Hyperscale Colocation service. The categorization is done based on the amount of IT load leased out to potential customers. Retail colocation service has leased capacity less than 250 kW; Wholesale colocation services has leased capacity between 251 kW and 4 MW and Hyperscale colocation services has leased capacity more than 4 MW.

- END CONSUMERS - The Data Center Market operates on a B2B basis. BFSI, Government, Cloud Operators, Media and Entertainment, E-Commerce, Telecom and Manufacturing are the major end-consumers in the market studied. The scope only includes colocation service operators catering to the increasing digitalization of the end-user industries.

| Keyword | Definition |

|---|---|

| Rack Unit | Generally referred as U or RU, it is the unit of measurement for the server unit housed in the racks in the data center. 1U is equal to 1.75 inches. |

| Rack Density | It defines the amount of power consumed by the equipment and server housed in a rack. It is measured in kilowatt (kW). This factor plays a critical role in data center design and, cooling and power planning. |

| IT Load Capacity | The IT load capacity or installed capacity, refers to the amount of energy consumed by servers and network equipment placed in a rack installed. It is measured in megawatt (MW). |

| Absorption Rate | It denotes how much of the data center capacity has been leased out. For instance, if a 100 MW DC has leased out 75 MW, then the absorption rate would be 75%. It is also referred to as utilization rate and leased-out capacity. |

| Raised Floor Space | It is an elevated space built over the floor. This gap between the original floor and the elevated floor is used to accommodate wiring, cooling, and other data center equipment. This arrangement assists in having proper wiring and cooling infrastructure. It is measured in square feet/meter. |

| Computer Room Air Conditioner (CRAC) | It is a device used to monitor and maintain the temperature, air circulation, and humidity inside the server room in the data center. |

| Aisle | It is the open space between the rows of racks. This open space is critical for maintaining the optimal temperature (20-25 °C) in the server room. There are primarily two aisles inside the server room, a hot aisle and a cold aisle. |

| Cold Aisle | It is the aisle wherein the front of the rack faces the aisle. Here, chilled air is directed into the aisle so that it can enter the front of the racks and maintain the temperature. |

| Hot Aisle | It is the aisle where the back of the racks faces the aisle. Here, the heat dissipated from the equipment’s in the rack is directed to the outlet vent of the CRAC. |

| Critical Load | It includes the servers and other computer equipment whose uptime is critical for data center operation. |

| Power Usage Effectiveness (PUE) | It is a metric which defines the efficiency of a data center. It is calculated by: (𝑇𝑜𝑡𝑎𝑙 𝐷𝑎𝑡𝑎 𝐶𝑒𝑛𝑡𝑒𝑟 𝐸𝑛𝑒𝑟𝑔𝑦 𝐶𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛)/(𝑇𝑜𝑡𝑎𝑙 𝐼𝑇 𝐸𝑞𝑢𝑖𝑝𝑚𝑒𝑛𝑡 𝐸𝑛𝑒𝑟𝑔𝑦 𝐶𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛). Further, a data center with a PUE of 1.2-1.5 is considered highly efficient, whereas, a data center with a PUE >2 is considered highly inefficient. |

| Redundancy | It is defined as a system design wherein additional component (UPS, generators, CRAC) is added so that in case of power outage, equipment failure, the IT equipment should not be affected. |

| Uninterruptible Power Supply (UPS) | It is a device that is connected in series with the utility power supply, storing energy in batteries such that the supply from UPS is continuous to IT equipment even during utility power is snapped. The UPS primarily supports the IT equipment only. |

| Generators | Just like UPS, generators are placed in the data center to ensure an uninterrupted power supply, avoiding downtime. Data center facilities have diesel generators and commonly, 48-hour diesel is stored in the facility to prevent disruption. |

| N | It denotes the tools and equipment required for a data center to function at full load. Only "N" indicates that there is no backup to the equipment in the event of any failure. |

| N+1 | Referred to as 'Need plus one', it denotes the additional equipment setup available to avoid downtime in case of failure. A data center is considered N+1 when there is one additional unit for every 4 components. For instance, if a data center has 4 UPS systems, then for to achieve N+1, an additional UPS system would be required. |

| 2N | It refers to fully redundant design wherein two independent power distribution system is deployed. Therefore, in the event of a complete failure of one distribution system, the other system will still supply power to the data center. |

| In-Row Cooling | It is the cooling design system installed between racks in a row where it draws warm air from the hot aisle and supplies cool air to the cold aisle, thereby maintaining the temperature. |

| Tier 1 | Tier classification determines the preparedness of a data center facility to sustain data center operation. A data center is classified as Tier 1 data center when it has a non-redundant (N) power component (UPS, generators), cooling components, and power distribution system (from utility power grids). The Tier 1 data center has an uptime of 99.67% and an annual downtime of <28.8 hours. |

| Tier 2 | A data center is classified as Tier 2 data center when it has a redundant power and cooling components (N+1) and a single non-redundant distribution system. Redundant components include extra generators, UPS, chillers, heat rejection equipment, and fuel tanks. The Tier 2 data center has an uptime of 99.74% and an annual downtime of <22 hours. |

| Tier 3 | A data center having redundant power and cooling components and multiple power distribution systems is referred to as a Tier 3 data center. The facility is resistant to planned (facility maintenance) and unplanned (power outage, cooling failure) disruption. The Tier 3 data center has an uptime of 99.98% and an annual downtime of <1.6 hours. |

| Tier 4 | It is the most tolerant type of data center. A Tier 4 data center has multiple, independent redundant power and cooling components and multiple power distribution paths. All IT equipment are dual powered, making them fault tolerant in case of any disruption, thereby ensuring interrupted operation. The Tier 4 data center has an uptime of 99.74% and an annual downtime of <26.3 minutes. |

| Small Data Center | Data center that has floor space area of ≤ 5,000 Sq. ft or the number of racks that can be installed is ≤ 200 is classified as a small data center. |

| Medium Data Center | Data center which has floor space area between 5,001-20,000 Sq. ft, or the number of racks that can be installed is between 201-800, is classified as a medium data center. |

| Large Data Center | Data center which has floor space area between 20,001-75,000 Sq. ft, or the number of racks that can be installed is between 801-3,000, is classified as a large data center. |

| Massive Data Center | Data center which has floor space area between 75,001-225,000 Sq. ft, or the number of racks that can be installed is between 3001-9,000, is classified as a massive data center. |

| Mega Data Center | Data center that has a floor space area of ≥ 225,001 Sq. ft or the number of racks that can be installed is ≥ 9001 is classified as a mega data center. |

| Retail Colocation | It refers to those customers who have a capacity requirement of 250 kW or less. These services are majorly opted by small and medium enterprises (SMEs). |

| Wholesale Colocation | It refers to those customers who have a capacity requirement between 250 kW to 4 MW. These services are majorly opted by medium to large enterprises. |

| Hyperscale Colocation | It refers to those customers who have a capacity requirement greater than 4 MW. The hyperscale demand primarily originates from large-scale cloud players, IT companies, BFSI, and OTT players (like Netflix, Hulu, and HBO+). |

| Mobile Data Speed | It is the mobile internet speed a user experiences via their smartphones. This speed is primarily dependent on the carrier technology being used in the smartphone. The carrier technologies available in the market are 2G, 3G, 4G, and 5G, where 2G provides the slowest speed while 5G is the fastest. |

| Fiber Connectivity Network | It is a network of optical fiber cables deployed across the country, connecting rural and urban regions with high-speed internet connection. It is measured in kilometer (km). |

| Data Traffic per Smartphone | It is a measure of average data consumption by a smartphone user in a month. It is measured in gigabyte (GB). |

| Broadband Data Speed | It is the internet speed that is supplied over the fixed cable connection. Commonly, copper cable and optic fiber cable are used in both residential and commercial use. Here, optic cable fiber provides faster internet speed than copper cable. |

| Submarine Cable | A submarine cable is a fiber optic cable laid down at two or more landing points. Through this cable, communication and internet connectivity between countries across the globe is established. These cables can transmit 100-200 terabits per second (Tbps) from one point to another. |

| Carbon Footprint | It is the measure of carbon dioxide generated during the regular operation of a data center. Since, coal, and oil & gas are the primary source of power generation, consumption of this power contributes to carbon emissions. Data center operators are incorporating renewable energy sources to curb the carbon footprint emerging in their facilities. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF