Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

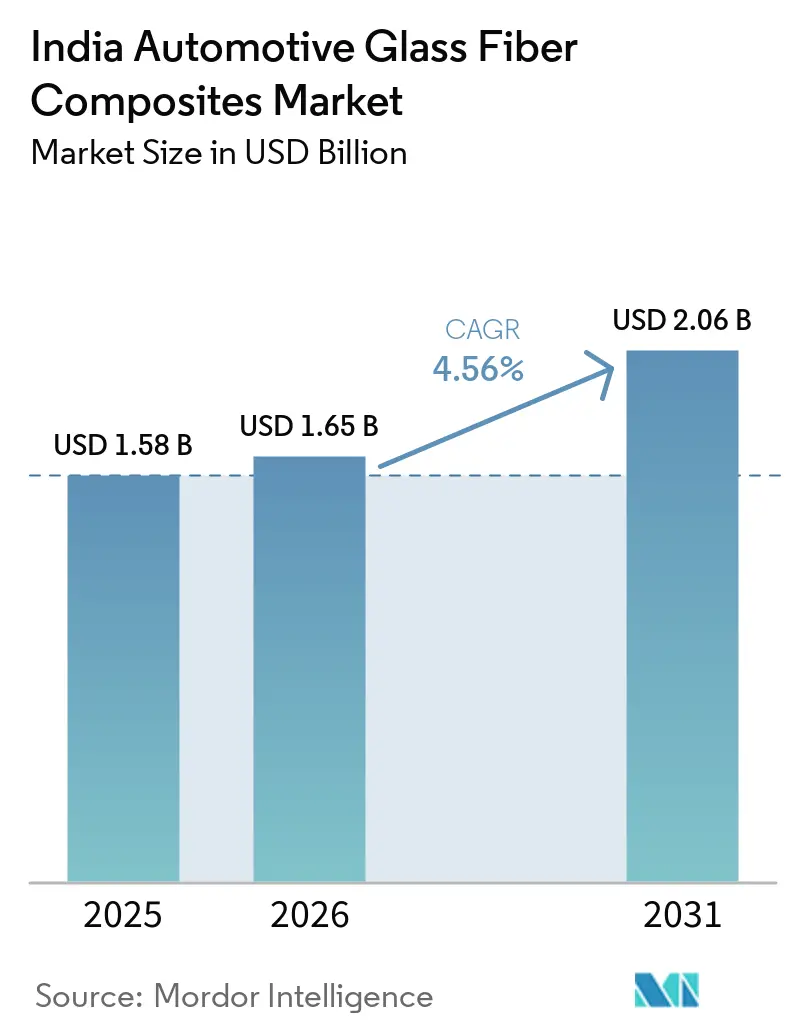

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.06 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Glass Fiber Composites Market Analysis by Mordor Intelligence

The India Automotive Glass Fiber Composites Market size is projected to expand from USD 1.58 billion in 2025 and USD 1.65 billion in 2026 to USD 2.06 billion by 2031, registering a CAGR of 4.56% between 2026 to 2031. Electric-vehicle programs funded by FAME-II subsidies, the PLI-ACC battery scheme, and state EV incentives are amplifying lightweighting demand, and glass fiber remains the preferred reinforcement because it delivers competitive tensile strength at a fraction of carbon fiber’s energy intensity. Domestic Tier-1 and Tier-2 moulders are scaling rapidly, yet India still imports about 250 kilotonnes of roving each year, exposing the supply chain to freight and geopolitical volatility. OEM weight-reduction targets dovetail with new Extended Producer Responsibility rules that favor recyclable thermoplastic matrices. Together, these factors position glass-fiber composites as a cost-effective pathway to protect driving range, lower lifecycle CO₂, and safeguard CAFE compliance.

Key Report Takeaways

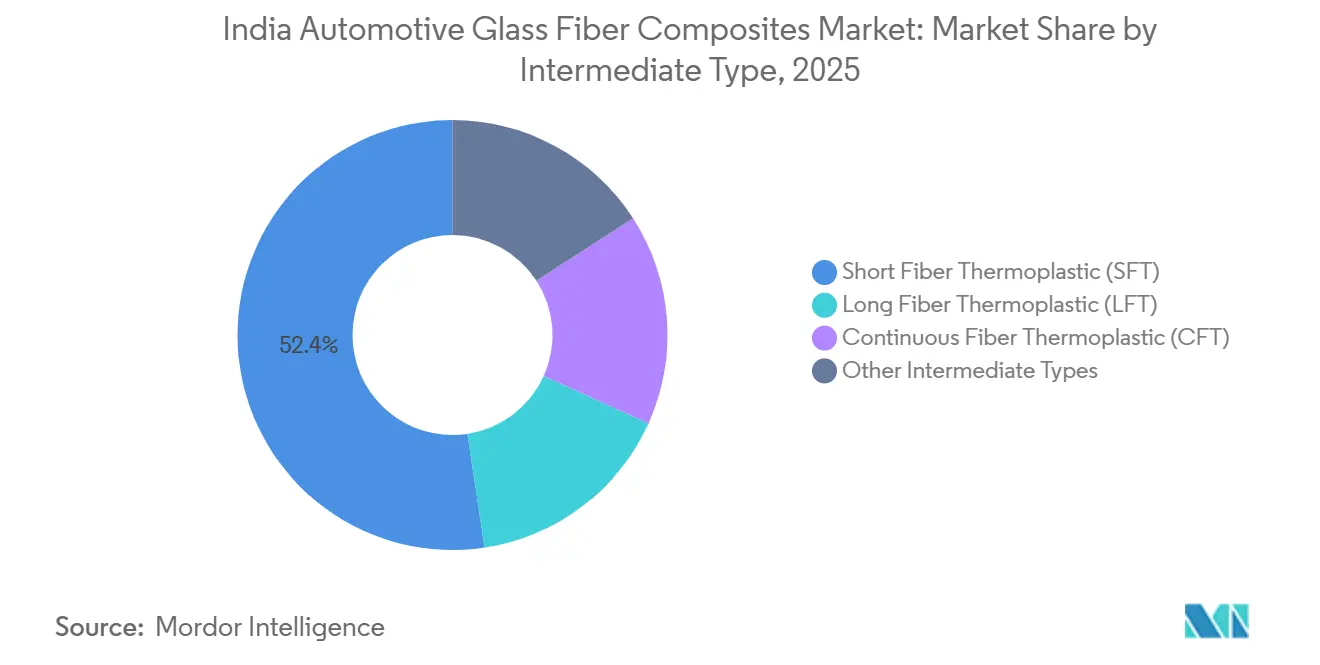

- By intermediate type, the short fiber thermoplastic (SFT) held a market share of 52.38% in 2025, and long fiber thermoplastic (LFT)'s share is expected to grow with a CAGR of 5.84% during the forecast period (2026-2031).

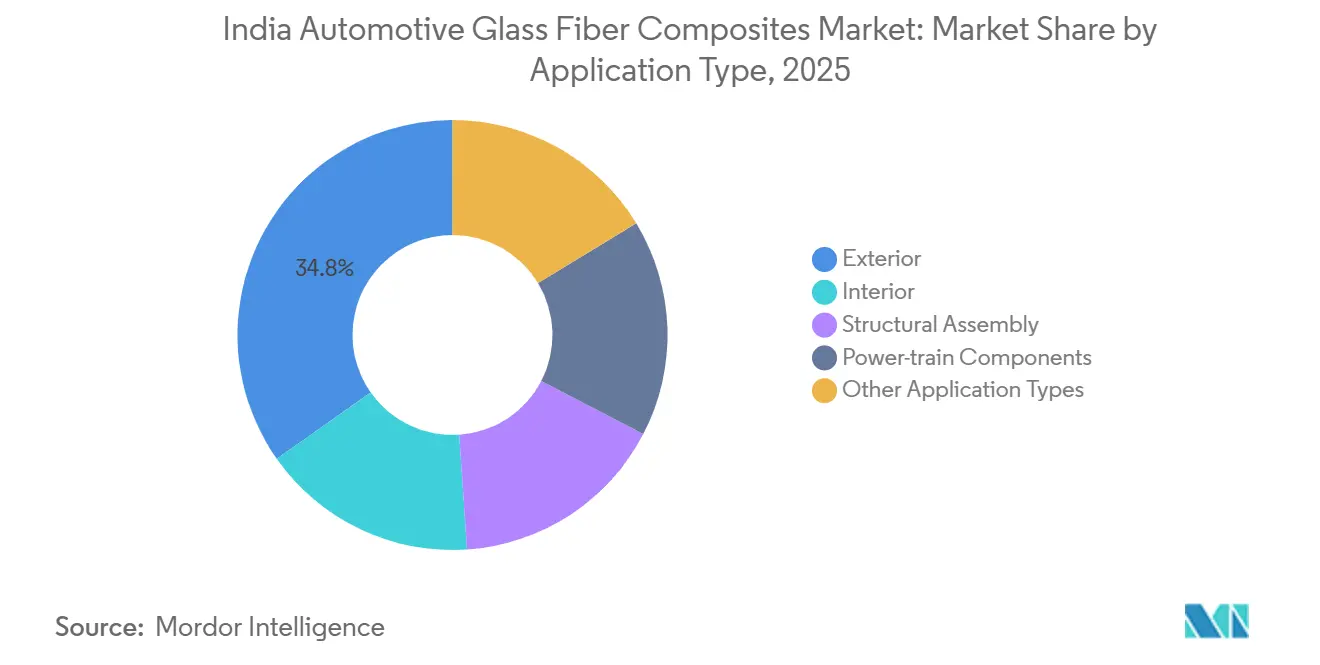

- By application type, exterior held a share of 34.76% in 2025, and the structural assembly application is expected to witness a growth of 6.12% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Automotive Glass Fiber Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV production under FAME-II incentives | +1.2% | Maharashtra, Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Cost-performance edge of glass vs. carbon | +0.8% | National | Long term (≥4 years) |

| Domestic Tier-1/2 moulding capacity expansion | +1.0% | Tamil Nadu, Gujarat, Maharashtra | Medium term (2-4 years) |

| PLI-ACC scheme boosting high-strength thermoplastics | +0.9% | Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Shift to recyclable thermoplastic composites | +0.7% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising EV Production Under FAME-II Incentives

FAME-II subsidies supported 1.61 million electric vehicles through 2025, and the successor PM E-DRIVE program will extend funding to 2028[1]Press Information Bureau, “Government approves Production-Linked Incentive Scheme for ACC Battery Storage,” pib.gov.in. Battery-electric cars weigh roughly 1.5 times their ICE peers, so OEMs rely on glass-fiber battery enclosures and underbody shields to offset the added mass. Tata Motors, Hyundai, and Suzuki have each adopted glass-fiber parts in next-generation platforms, demonstrating that composites help protect range without eroding price competitiveness. Tier-1 suppliers are responding with rapid-cycle moulding lines near EV hubs, trimming logistics time and cost. As electrification scales nationwide, lightweight composites become integral rather than optional.

Cost-Performance Edge of Glass vs. Carbon Fiber

Glass fiber represents close to 92% of automotive composite volume because it provides 350 MPa tensile strength at one-tenth the embodied energy of virgin carbon fiber[2]Royal Society of Chemistry, “Energy consumption and environmental impact in carbon-fiber production,” rsc.org. Mass-market vehicles priced below USD 15,000 cannot absorb carbon-fiber premiums, making glass-fiber-reinforced polymers the pragmatic choice for exterior panels, seat structures, and battery covers. Trinseo and CSP have launched long-fiber grades that cut enclosure weight by more than 25% versus steel, proving that performance thresholds can be met at competitive cost. As CAFE limits tighten, the balance of strength, price, and sustainability keeps glass ahead of rival materials.

Domestic Tier-1/2 Moulding Capacity Expansion

Saint-Gobain invested INR 3,400 crore (USD 39 billion) to add a 1,000-tonne-per-day float line in Chennai, and 3B Fibreglass is scaling to 120 kilotonnes of capacity by mid-2025. OPmobility’s new Maharashtra plant and Exel Composites’ Goa pultrusion facility improve local availability of structural beams, cross-car members, and battery trays. Expanded domestic supply shortens lead times, stabilizes prices, and encourages OEMs to specify glass-fiber composites in high-volume models. Regional clusters also create jobs and upskill the workforce.

PLI-ACC Scheme Boosting High-Strength Thermoplastics

The PLI-ACC program awarded 40 GWh of battery capacity under an INR 18,100 crore (USD 207.8 billion) budget, prompting demand for continuous-fiber thermoplastic laminates that meet cell-to-pack structural loads. Avient’s Nymax REC 6000 recycled nylon, launched in 2026, supplies up to 30% glass fiber while satisfying impact and dimensional targets for battery covers. Coupled PLI-Auto incentives for advanced components, the scheme accelerates investment in recyclable, high-stiffness grades that expand the application envelope of glass-fiber composites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling and end-of-life hurdles for thermosets | -0.40% | National, with acute impact in states lacking advanced recycling infrastructure | Medium term (2–4 years) |

| Intermittent roving and PA resin supply shortages | -0.30% | National, with acute impact in Gujarat, Tamil Nadu, Maharashtra manufacturing clusters | Short term (≤ 2 years) |

| Limited OEM design-for-composite skill base | -0.30% | National, with concentration in Tier-2 and Tier-3 supplier networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recycling and End-of-Life Hurdles for Thermosets

Conventional pyrolysis removes nearly all resin, but cuts recovered glass-fiber strength by up to 50%, confining reuse to low-value fillers. Chemical routes retain more properties but remain pilot-scale and costly. India’s 82 Registered Vehicle Scrapping Facilities, therefore, struggle to capture value from thermoset scrap, discouraging OEMs from specifying epoxy or polyester parts. Without standardized testing or digital passports for recovered fiber, tier suppliers fear warranty liabilities, slowing market penetration of thermoset glass-fiber composites.

Intermittent Roving and PA Resin Shortages

India imports around 250 kilotonnes of glass roving each year from Chinese suppliers, and freight volatility can extend lead times to 12 weeks. Polyamide feedstocks face similar constraints, exposing moulders to price spikes and forcing 60-day safety stocks that tie up working capital. Local players such as Goa Glass Fibre and U.P. Twiga Fiberglass remain capital-constrained, limiting rapid capacity additions. Material insecurity raises production costs and can delay new-model launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Intermediate Type: SFT Dominance Masks LFT’s Structural Upswing

In 2025, Short Fiber Thermoplastic accounted for 52.38% of the India Automotive Glass Fiber composites market, reflecting the fast-cycle economics of injection moulding for door modules, instrument panels, and non-load-bearing exterior trims. Long Fiber Thermoplastic is set to grow at 5.84% CAGR during the forecast period (2026-2031) as OEMs adopt it for battery enclosures, cross-car beams, and underbody shields that demand higher stiffness-to-weight ratios. Continuous-fiber tapes remain niche but are gaining momentum through new pultrusion lines in Goa and research partnerships aimed at hydrogen fuel-cell bipolar plates. The India Automotive Glass Fiber Composites market size for LFT components is projected to expand steadily as Tier-1 suppliers validate multi-material architectures with up to 40% part-count reduction. SFT will keep its volume edge, but LFT’s share of structural assemblies will climb in tandem with EV production.

Röchling’s hybrid metal-plastic cross-car beam cuts weight 40% versus steel while integrating attachment points, showing how LFT reduces assembly complexity. LANXESS Tepex sheets combine continuous glass layers with polypropylene cores to deliver gravel-impact resistance for SUV underbody shields. Maruti Suzuki’s lightweight initiative already removed 80 kilograms from a small-car platform, proving that incremental composite substitution contributes 3-4% fuel-economy gains. As local converters scale compression and injection presses beyond 4,000 kN, LFT and hybrid laminates will move deeper into semi-structural domains.

By Application Type: Exterior Still Leads, Structural Assembly Accelerates

Exterior parts held 34.76% revenue share in 2025 owing to paintable, corrosion-resistant fenders, grilles, and tailgates. Structural assembly is forecast to log a 6.12% CAGR during the forecast period (2026-2031) as battery trays, underbody shields, and crash beams migrate to glass-fiber thermoplastics that safeguard range and crashworthiness. Interior modules and power-train covers retain healthy demand for SFT, while high-temperature polyamide grades support oil sumps and cam covers. The India Automotive Glass Fiber Composites market size for structural components is poised to climb as EV platforms require large, integrated enclosure systems. Exterior volumes will stay robust, but their share gradually declines as structural use cases multiply.

OPmobility’s quick-turn bumper program shows local moulders can outpace metal stampers on tooling lead times, a key edge in India’s cost-sensitive market. Hyundai’s paintless composite spoilers achieve 25% weight savings, and Mahindra is testing composite oil sumps that shave 15 kilograms per vehicle. Trinseo’s long-fiber polycarbonate enclosures drop carbon footprint 30% relative to aluminum, highlighting the sustainability dividend that resonates with EPR regulations.

Geography Analysis

Tamil Nadu accounts for most of the national EV output, buoyed by full road-tax waivers and battery incentives that attract OEMs such as Hyundai, Nissan-Renault, and Tata Motors. Maharashtra’s INR 1,993 crore (USD 22.87 billion) EV policy targets 30% penetration by 2030 and anchors composite demand around Pune and Talegaon, where OPmobility and Jushi plan new capacity. Karnataka offers 25% capex subsidies and hosts Kia’s 3.7-megawatt rooftop-solar plant; its three mobility clusters house moulders feeding both passenger cars and two-wheelers. Gujarat’s Sanand hub supports Suzuki’s e VITARA production and NTF India’s new facility, reinforcing demand for battery enclosures and fuel-cell components. These four states collectively form the nucleus of the India Automotive Glass Fiber Composites market, supplying most national vehicle volumes and fostering just-in-time composite delivery networks.

Regional incentive arbitrage shapes plant locations. Uttar Pradesh grants 100% road-tax waivers, stimulating e-rickshaw adoption and lightweight roof-canopy demand, while Madhya Pradesh’s truck-focused policy fuels composite fairings for heavy vehicles. Saint-Gobain’s INR 3,400 crore (USD 39 billion) Oragadam investment cements Tamil Nadu’s status as a raw-material node, and Exel’s Goa pultrusion line offers coastal export access. Despite localized strengths, national schemes such as FAME-II and PLI-ACC provide uniform fiscal underpinnings that mitigate state-level policy gaps. Consequently, the India automotive glass fiber composites market share of southern and western clusters remains dominant through 2031, even as northern and central zones gain capacity.

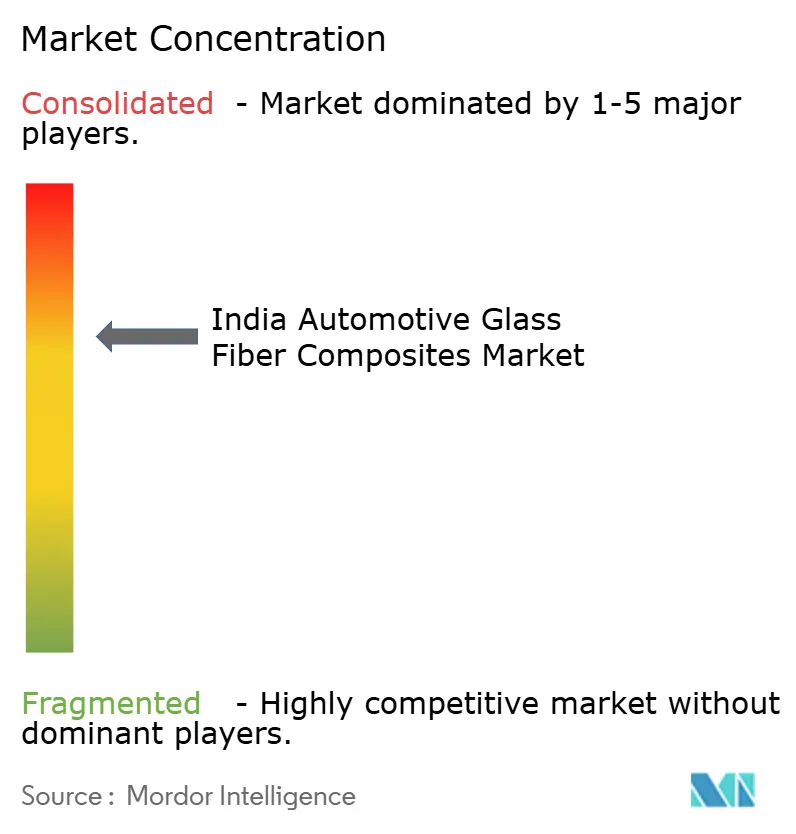

Competitive Landscape

The India Automotive Glass Fiber Composites market is moderately consolidated. Strategic moves cluster around capacity additions, recycled-grade launches, and lightweighting collaborations with OEMs. Hexcel leverages aerospace know-how to supply fast-curing prepregs and tape for Indian mobility projects, opening the door to continuous-fiber chassis components. Barriers persist: inconsistent roving supply, limited sizing-chemistry know-how, and scarce design-for-composite skills within OEM engineering teams.

India Automotive Glass Fiber Composites Industry Leaders

Owens Corning

Jushi India Fiberglass Pvt. Ltd.

3B - the fibreglass company

Saint-Gobain India

Veplas d.d.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Owens Corning completed the sale of its glass reinforcements business to Mumbai-based Praana Group. This development is expected to impact the automotive glass fiber composites market in India by driving localized production and strengthening the domestic supply chain.

- September 2025: Triumph Composites Pvt. Ltd. and Quartz Fibre Private Limited received approval from the Competition Commission of India to acquire a stake in Owens-Corning (India) Pvt. Ltd. Through a Master Share Purchase Agreement (MSPA), the involved parties agreed to sell Owens-Corning’s global glass fibre reinforcement business, including its operations in India.

India Automotive Glass Fiber Composites Market Report Scope

Automotive glass fiber composites (GFRP) are high-strength, lightweight materials composed of glass fibers embedded in a polymer resin matrix, widely used to replace metals, reduce vehicle weight, and lower emissions.

The India Automotive Glass Fiber Composites market report is segmented by intermediate type and application type. By intermediate type, the market is segmented into short fiber thermoplastic (SFT), long fiber thermoplastic (LFT), continuous fiber thermoplastic (CFT), and other intermediate types. By application type, the market is segmented into interior, exterior, structural assembly, power-train components, and other application types. The market sizes and forecasts are provided in terms of value (USD).

By Intermediate Type

| Short Fiber Thermoplastic (SFT) |

| Long Fiber Thermoplastic (LFT) |

| Continuous Fiber Thermoplastic (CFT) |

| Other Intermediate Types |

By Application Type

| Interior |

| Exterior |

| Structural Assembly |

| Power-train Components |

| Other Application Types |

| By Intermediate Type | Short Fiber Thermoplastic (SFT) |

| Long Fiber Thermoplastic (LFT) | |

| Continuous Fiber Thermoplastic (CFT) | |

| Other Intermediate Types | |

| By Application Type | Interior |

| Exterior | |

| Structural Assembly | |

| Power-train Components | |

| Other Application Types |

Key Questions Answered in the Report

What is the forecast size of the India automotive glass fiber composites market in 2031?

India Automotive Glass Fiber Composites market is projected to reach USD 2.06 billion by 2031.

How fast is the market expected to grow after 2026?

India Automotive Glass Fiber Composites Market is forecast to expand at a 4.56% CAGR between 2026 and 2031.

Which intermediate type is growing the quickest?

Long Fiber Thermoplastic is projected to post the fastest growth at a 5.84% CAGR to 2031.

Why are OEMs favoring glass fiber over carbon fiber in India?

Glass fiber offers similar strength at far lower energy and cost, fitting mass-market price points and sustainability mandates.

Which Indian states drive the highest composite demand?

Tamil Nadu, Maharashtra, Karnataka, and Gujarat lead due to concentrated EV production and supportive incentives.

Page last updated on: