Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

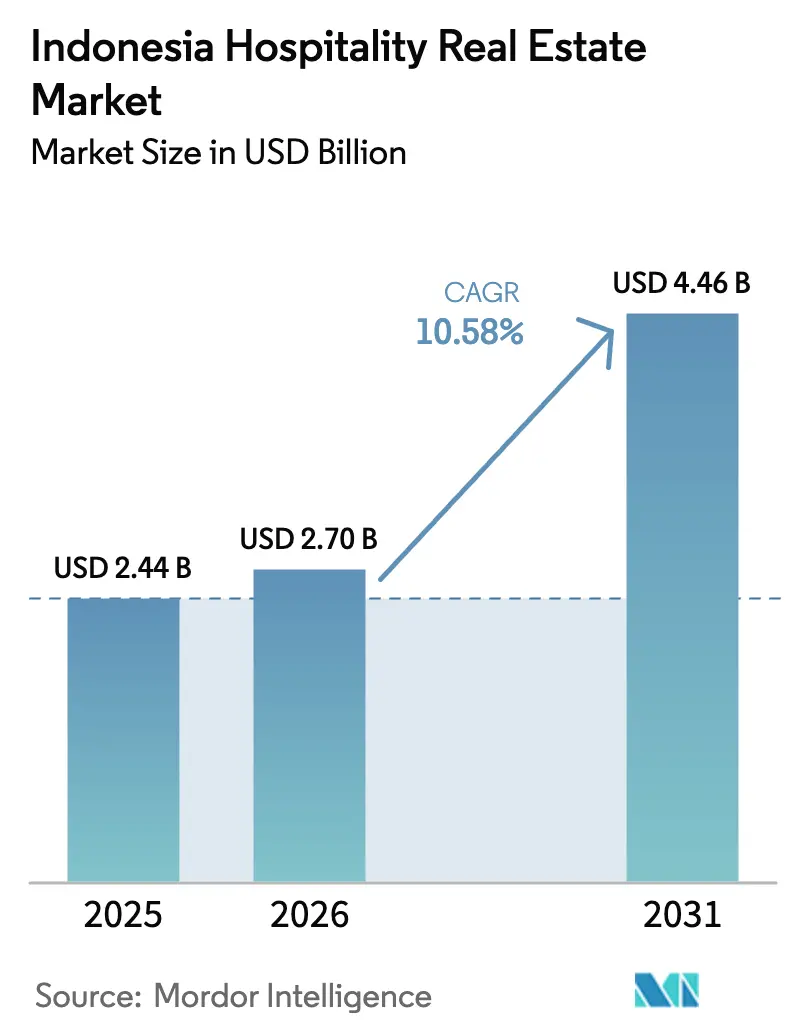

| Base Year Market Size (2025) | USD 2.44 Billion |

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

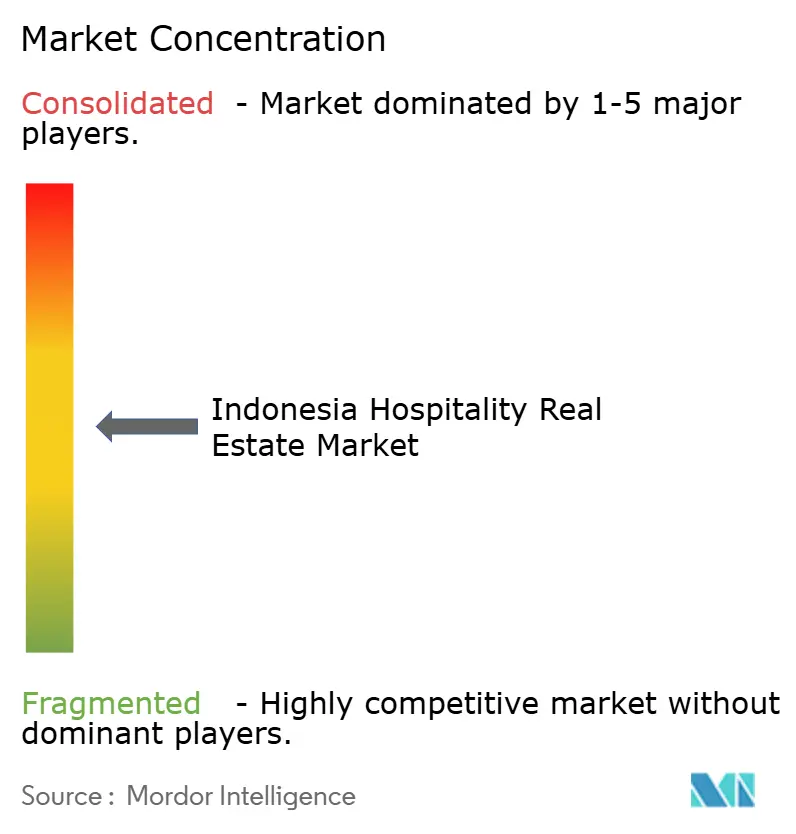

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Hospitality Real Estate Market Analysis by Mordor Intelligence

The Indonesia Hospitality Real Estate Market is expected to grow from USD 2.44 billion in 2025 to USD 2.7 billion in 2026 and is forecast to reach USD 4.46 billion by 2031 at 10.58% CAGR over 2026-2031. Government infrastructure spending of USD 25.5 billion in 2025, combined with the ongoing Nusantara Capital City program, anchors the sector’s long-run demand. Tourism’s USD 72.5 billion contribution to 2024 GDP demonstrates strong post-pandemic resilience. New air routes, tax-friendly Special Economic Zones, and visa-on-arrival expansions further stimulate pipeline activity, while cautious monetary conditions and complex land rules temper foreign investor appetite. Institutional capital continues to favor branded assets, yet locally owned independents retain pricing agility across secondary cities.

Key Report Takeaways

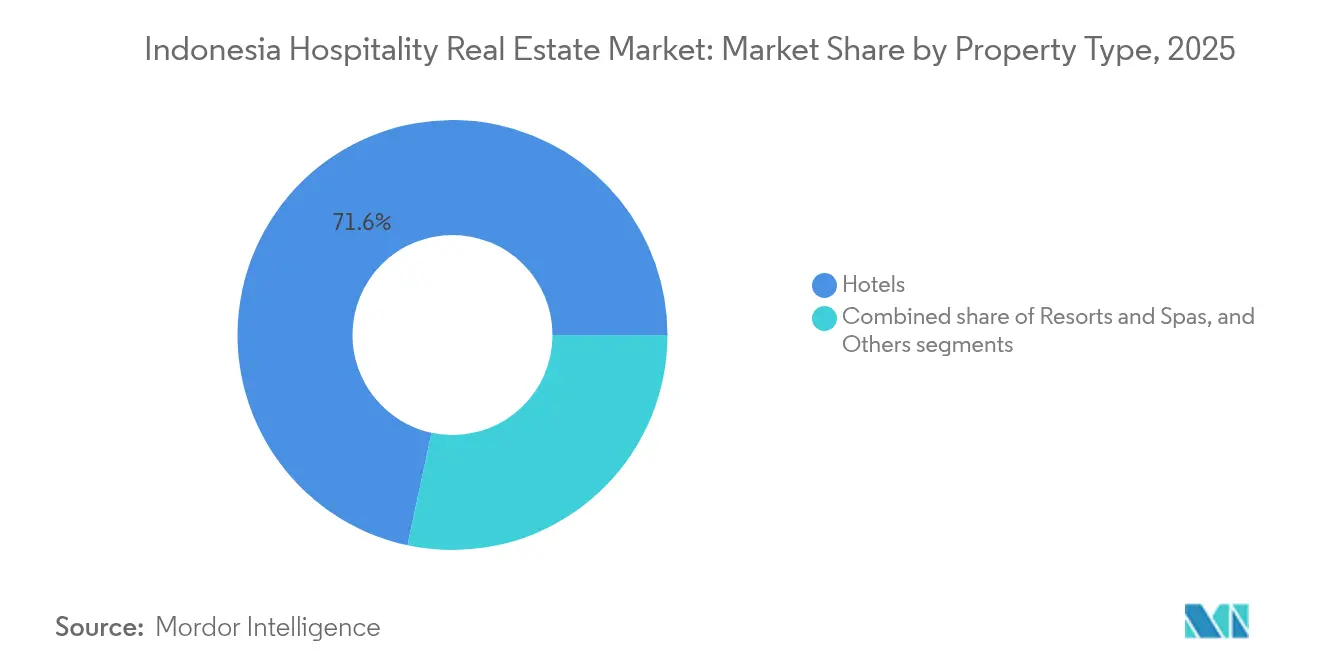

- By property type, hotels led with 71.64% revenue share of the Indonesia hospitality real estate market in 2025; resorts and spas are advancing at an 10.92% CAGR to 2031.

- By type, independent hotels held 62.85% of the Indonesia hospitality real estate market share in 2025, while chain hotels are projected to expand at an 11.14% CAGR through 2031.

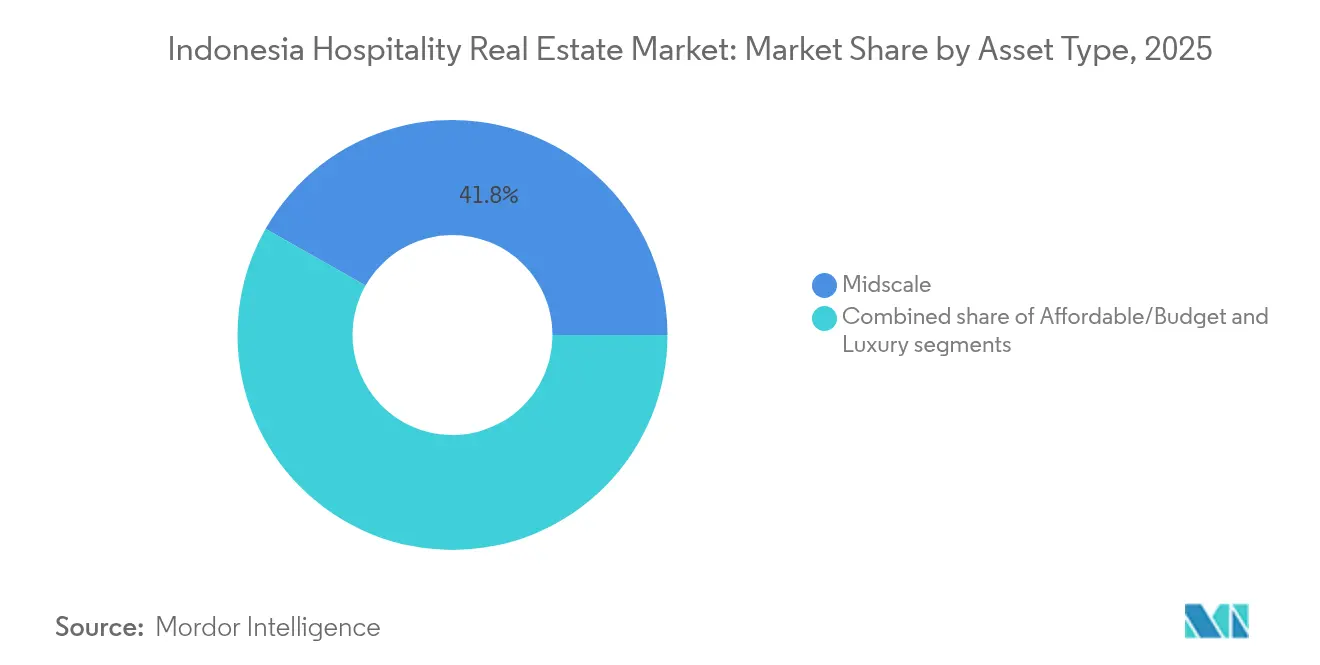

- By asset class, midscale properties accounted for a 41.78% share of the Indonesia hospitality real estate market size in 2025, whereas luxury developments are forecast to grow at an 11.46% CAGR to 2031.

- By geography, Jakarta captured a 27.14% share in 2025, and the Rest of Indonesia category is set to log the fastest 11.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Hospitality Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed destination development programs unlocking new hotel corridors | +3.1% | National, with priority focus on super-priority destinations and IKN | Long term (≥ 4 years) |

| Visa liberalization and streamlined arrivals procedures increasing international visitation | +2.4% | Gateway cities, major tourist destinations with international airports | Short term (≤ 2 years) |

| Large-scale public works creating sustained business/MICE room nights | +2.2% | IKN Nusantara, Jakarta, major industrial zones and government centers | Medium term (2-4 years) |

| Air connectivity upgrades improving access and RevPAR potential | +1.8% | Hub airports, secondary destinations with new route development | Medium term (2-4 years) |

| Investment incentives accelerating hospitality project viability | +1.2% | Special Economic Zones, designated tourism areas, priority regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Backed Destination Development Programs Unlocking New Hotel Corridors

Dedicated federal spending is opening new demand corridors beyond Bali and Jakarta. The USD 3.7 billion private hospitality commitments tied to Nusantara Capital City underscore investor confidence in the government’s long-horizon strategy. Super-priority sites spanning Lake Toba to Labuan Bajo receive direct budget allocations, creating predictable construction timelines and de-risked feasibility models. North Sulawesi’s USD 50.0 million influx into hotels and restaurants illustrates capital migration toward lesser-known islands. State guarantees under the National Strategic Projects framework streamline licensing, compress financing costs, and differentiate Indonesia from neighboring tourism markets that rely on ad-hoc growth[1]Bambang Susantono, “Nusantara Capital City Investor Guide 2025,” IKN Authority, ikn.go.id.

Visa Liberalization and Streamlined Arrivals Procedures Increasing International Visitation

Simplified entry rules produced 4.09 million foreign arrivals in the first four months of 2024, a 24.85% jump year-over-year. Malaysia, Australia, and China collectively represent 36% of total visitors, reducing single-market vulnerability. Occupancy of star-rated hotels reached 47.14% in April 2024, up 5.77 percentage points from 2023. Traffic spikes at Ngurah Rai and Soekarno Hatta airports confirm the immediate linkage between policy change and RevPAR gains. Streamlined screening minimizes arrival friction and positions the Indonesia hospitality real estate market for share gains against regional competitors still operating tight border controls[2]Ida Bagus Kade Subagia, “International Visitor Arrivals April 2024,” BPS-Statistics Indonesia, bps.go.id.

Large-Scale Public Works Creating Sustained Business/MICE Room Nights

Road, rail, and port upgrades underpin steady corporate travel flows. The relocation program for Nusantara Capital City guarantees a decade-long stream of contractors, officials, and consultants requiring extended-stay inventory. Jakarta properties initially absorbed a 10–20% dip in government bookings but quickly diversified into commercial events and transient business. Special Economic Zones, many attached to industrial estates, stimulate meetings demand that stabilizes occupancy during tourism shoulder months. The predictable MICE base helps hotel developers lock in debt at fixed rates, improving underwriting for new assets.

Air Connectivity Upgrades Improving Access and RevPAR Potential

Aviation expansion directly influences hotel metrics: Jakarta RevPAR rose 17.8% and Bali climbed 21.5% through August 2024 amid seat growth and LCC penetration. Major capex, such as the USD 3 billion Bali airport enhancement, enhances premium room pricing power by funneling higher-spend travelers into the island. Secondary hubs from Lombok to Makassar obtain first-time international links, creating first-mover advantages for early hotel projects. The correlation between flight frequency and pipeline velocity remains strongest in destinations previously hindered by limited lift capacity.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land/title structuring and foreign-ownership limits complicating acquisitions and timelines | -2.3% | National, acute in high-demand areas like Bali and Jakarta | Long term (≥ 4 years) |

| Regulatory unpredictability raising development risk | -1.9% | Variable by region, higher impact in tourism-dependent areas | Medium term (2-4 years) |

| Currency volatility and elevated financing costs lifting capex and return hurdles | -1.5% | National, with higher impact on foreign-funded projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land/Title Structuring and Foreign-Ownership Limits Complicating Acquisitions and Timelines

Equity structures must navigate the Building Use Rights framework that restricts outright foreign ownership to 85% in designated zones. Tenure uncertainty complicates 25-year management contracts typical for global flags. Protracted multilevel approvals can stretch land closing by up to two years, inflating interest carry and eroding IRRs. The Mandalika case, fraught with disputes, illustrated how unresolved titles derail marquee resort schemes despite federal support. Savvy sponsors now allocate greater contingency for land due diligence to keep the Indonesia hospitality real estate market timetable credible.

Regulatory Unpredictability Raising Development Risk

Regional autonomy means sudden moratoriums, zoning shifts, or density caps that disrupt pro-forma assumptions. New franchise rules introduced in 2024 demand a minimum three-year operating record and two-year profitability proof, tilting the playing field toward incumbents. Enforcement crackdowns on unlicensed villas in Bali elevate compliance costs but also remove unfairly priced competitors. Inconsistent environmental reviews push design revisions that add capex yet may preserve community goodwill when handled early[3]Prijandaru Effendi, “Government Regulation No. 35 of 2024 on Franchising,” Ministry of Law and Human Rights, kemenkumham.go.id.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Hotels Retain Core Dominance, Resorts Propel Growth

Hotels controlled 71.64% of the Indonesia hospitality real estate market size in 2025, supported by corporate contracts, government allotments, and stopover traffic in Jakarta and Surabaya. Full-service formats maintain baseline occupancy even during leisure slumps, shielding cash flows amid demand cycles. Resorts and spas, though holding a smaller base, deliver the fastest 10.92% CAGR as wellness and experiential travel accelerate. The segment benefits from upgraded island airports and the SEZ toolkit that offsets heavy upfront infrastructure spend. Developers leverage master-planned tourism zones to cluster resorts with retail and attractions, enhancing the average length of stay. Pipeline data indicates seven new five-star resorts scheduled in Bali by 2027, while North Sulawesi and Flores record their first international flag announcements. Rising domestic affluence sustains weekday resort occupancy, a notable shift from pre-2024 patterns dominated by weekend peaks. Regulatory clarity favoring eco-sensitive designs supports investor sentiment for resort assets positioned away from congested beaches.

The hotel sub-sector continues to attract institutional capital targeting stabilized yield, especially in transit-oriented developments near rail and toll-road junctions. Brands prioritize flexible room mixes that combine traditional keys with serviced-suite wings to capture extended-stay demand. Resorts, meanwhile, deploy asset-light management agreements allowing owner participation in F&B, spa, and activity revenues. Both categories underscore the Indonesia hospitality real estate market as a dual-track opportunity: steady urban income plays versus higher-beta leisure plays with stronger ADR upside.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Independents Lead Volumes, Chains Accelerate Professionalization

Independent operators accounted for 62.85% of the Indonesia hospitality real estate market share in 2025, reflecting local entrepreneurs’ ability to align product with nuanced consumer preferences and municipal regulations. Their lean cost base enables competitive pricing and quicker refurb cycles. Chain hotels, although smaller in number, grow at an 11.14% CAGR, propelled by loyalty ecosystems and bankable brand standards attractive to lenders. The Marriott–Pakuwon agreement for five new hotels totaling 1,300 rooms exemplifies symbiotic tie-ups where local developers gain global demand engines, while chains secure a pipeline without greenfield land risk. New franchising criteria introduced in 2024 could concentrate growth among experienced chains able to certify profitability. Independents counteract by embracing digital distribution and hyper-local design that resonates with Gen-Z domestic travelers. Conversion of unbranded properties into soft-brand collections emerges as a low-capex entry for chains seeking fast market penetration, further professionalizing operations across secondary cities.

Hybrid ownership structures now blend strata-titled condo-hotels with traditional leases, unlocking retail investor pools yet maintaining unified brand control. As the Indonesia hospitality real estate market evolves, independents are expected to maintain leadership in under-indexed towns, while chains dominate tier-1 and high-profile resort destinations where institutional capital demands standardized governance.

By Asset Class: Midscale Anchors Demand, Luxury Outperforms on Yield

Midscale assets held 41.78% of the Indonesia hospitality real estate market size in 2025 due to cost-conscious business travel and family holiday patterns. Their balanced positioning between affordability and service quality sustains a solid 65–70% occupancy across economic cycles. Limited F&B and standardized room prototypes facilitate efficient staffing models that cushion margin compression when ADR softens. Luxury properties, however, record an 11.46% CAGR, buoyed by rising disposable incomes and Indonesia’s pivot to higher-spend tourism. PT Jakarta Setiabudi Internasional booked USD 115.4 million in hotel revenue during 2024, illustrating the luxury’s earnings potency. Premium resorts tap integrated wellness, culinary, and cultural programming to lift ancillary spend, while smart-building tech lowers operating intensity per square foot. Budget stock faces price undercutting from informal rentals, prompting regulators to intensify enforcement, thereby indirectly supporting branded economy chains.

Midscale projects remain favored by domestic banks offering construction loans with shorter tenors, whereas luxury developments increasingly rely on offshore joint ventures and mezzanine slices. Asset managers optimize mixed-use footprints that pair luxury towers with midscale annexes, spreading risk yet preserving top-tier positioning on flagship frontage. This blend aligns with travel demand stratification and elevates the Indonesia hospitality real estate market as a diversified investment landscape.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Jakarta produced 27.14% of the total transaction value in 2025, underpinned by corporate travel, MICE events, and the capital’s status as the key air gateway. Soekarno Hatta recorded a 38.31% rise in international traffic during early 2024, immediately boosting citywide RevPAR. Institutional plays persist, typified by Astra Group’s USD 85 million acquisition of the Mandarin Oriental Jakarta stake. However, gradual government relocation to Nusantara tempers future official travel budgets, prompting hoteliers to cultivate commercial accounts and domestic leisure short breaks. Developers redeploy equity into transit-linked sub-markets such as BSD City, where integrated township plans promise stable weekday demand.

West and East Java clusters offer lower land cost and lighter red tape relative to Jakarta, prompting chain expansion in Surabaya, Bandung, and emerging industrial towns. Strong manufacturing FDI spurs weekday corporate stays, while weekend domestic tourism fills rooms. New four-star projects in Situbondo and Pekalongan illustrate confidence in secondary corridors, supported by toll-road upgrades shortening travel times. Central Java secures pipeline commitments from Swiss-Belhotel and Amaris, signaling brand conviction that secondary cities can sustain standardized service models.

The Rest of Indonesia group registers the highest 11.74% CAGR through 2031, reflecting super-priority destination funding and improved inter-island air links. Bali remains the flagship, with seven five-star openings announced for 2027 and the USD 6.7 billion Kura Kura SEZ steering high-end supply. Eagle Hills’ USD 3.1 billion commitment around Soekarno Hatta Airport shows foreign capital’s readiness to bankroll infrastructure-adjacent hospitality ecosystems. North Sulawesi’s USD 50.0 million hotel inflow and Kalimantan’s brand signings tied to Nusantara broaden spatial diversification. Enhanced digital connectivity permits remote resorts to access online distribution, lowering customer-acquisition costs and spreading the Indonesia hospitality real estate market footprint across 17,000 islands.

Competitive Landscape

Ownership fragmentation keeps competition moderate, encouraging both consolidation and niche specialization. Domestic players leverage local permitting expertise and relationship banking, while global operators contribute distribution heft and standardization. PT Jakarta Setiabudi Internasional’s 2024 hotel revenue concentration of 77% within total group earnings underlines the segment’s profitability for conglomerates that balance property and hospitality arms. State plans to consolidate 103 SOE-owned hotels into a dedicated holding, aim to rationalize operations and enhance scale economics.

Technology adoption proves decisive: operators deploying cloud PMS and AI-driven pricing report up to 30% cost efficiency improvements, freeing capital for refurbishments. OTA penetration democratizes market visibility, but commissions compress net ADR for independents lacking direct-booking infrastructure. Regulatory tightening on illegal accommodations, chiefly in Bali, may favor compliant operators by removing predatory price competition. Partnerships such as Marriott–Pakuwon illustrate the prevalent growth template: local land control plus international brand equity.

Future competition will revolve around ESG alignment and halal-certified offerings, segments where early movers can secure premium rate positioning. The Indonesia hospitality real estate market thus offers a balanced field: incumbents hold local leverage, yet foreign entrants wield brand and capital, producing a dynamic yet orderly competitive setting.

Indonesia Hospitality Real Estate Industry Leaders

Sinar Mas Land

Agung Podomoro Land

Ciputra Group

Duta Anggada Group

Lippo Karawaci

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Santika Indonesia Hotels & Resorts inked an IDR 250 billion (USD 16.0 million) joint venture with Janto Group for portfolio expansion.

- November 2024: Delonix Group confirmed a strategic investment alliance with Indies Hospitality to target secondary-city opportunities.

- September 2024: Marriott International partnered with Pakuwon Group to develop five new hotels with more than 1,300 rooms across Jakarta, Surabaya, and Bali.

- July 2024: UAE-based Eagle Hills signed a USD 3.1 billion memorandum covering hotel assets and tourism infrastructure near Soekarno Hatta International Airport.

Indonesia Hospitality Real Estate Market Report Scope

Hospitality property means the development of real estate, the primary usage of which is as a hotel or motel, with individual rooms principally for short-term rental to tenants occupying the same.

The Indonesian hospitality real estate market is segmented by property type (hotels and accommodations, spas and resorts, and other property types). The report offers market size and forecasts for the Indonesian hospitality real estate market in value (USD) for all the above segments.

By Property Type

| Hotels |

| Resorts & Spas |

| Others (Serviced Apartments, boutique inns, etc) |

By Type

| Chain Hotels |

| Independent Hotels |

By Asset Class

| Affordable/Budget |

| Midscale |

| Luxury |

By Region

| DKI Jakarta |

| West Java (Jawa Barat) |

| East Java (Jawa Timur) |

| Rest of Indonesia |

| By Property Type | Hotels |

| Resorts & Spas | |

| Others (Serviced Apartments, boutique inns, etc) | |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Asset Class | Affordable/Budget |

| Midscale | |

| Luxury | |

| By Region | DKI Jakarta |

| West Java (Jawa Barat) | |

| East Java (Jawa Timur) | |

| Rest of Indonesia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2026 revenue projection for Indonesia’s hospitality property segment?

The Indonesia hospitality real estate market size is valued at USD 2.7 billion in 2026.

How quickly is hospitality real estate expanding across Indonesia?

The sector is forecast to grow at a 10.58% CAGR, reaching USD 4.46 billion by 2031.

Which property type currently dominates Indonesia’s hotel space?

Hotels account for 71.64% of revenue, driven by business travel and urban demand.

Why are chain hotels gaining ground despite independents’ leadership?

Chains deliver brand recognition and financing advantages, enabling an 11.14% CAGR to 2031.