Green HVAC Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

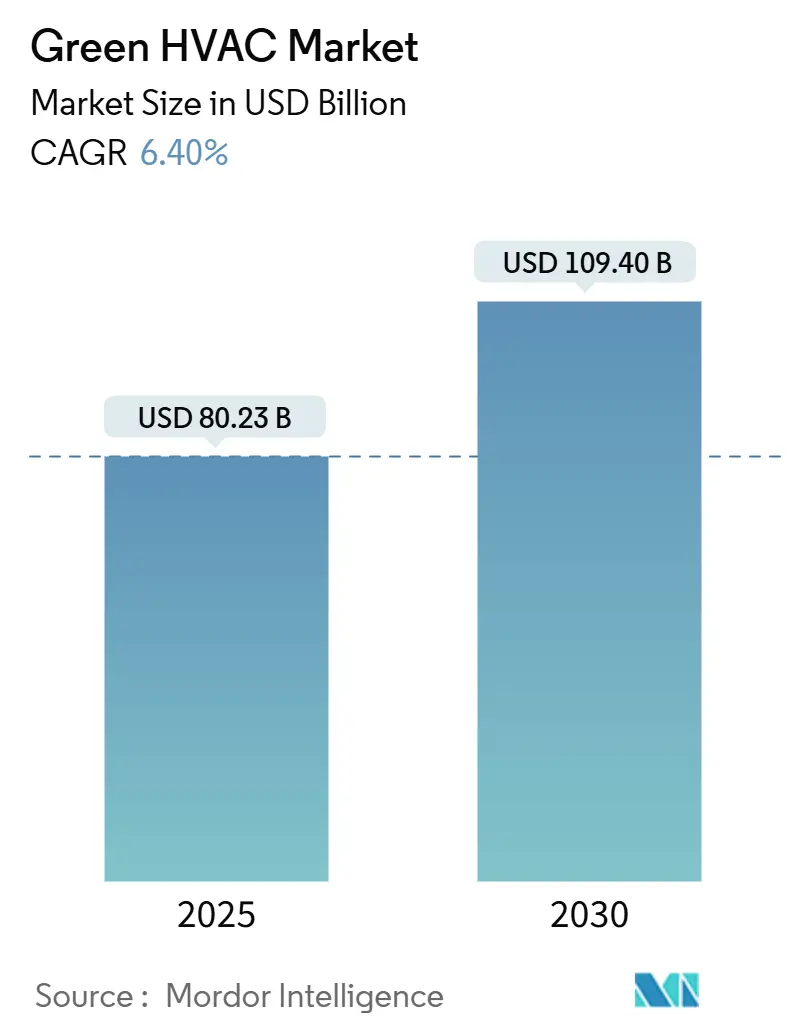

| Market Size (2025) | USD 80.23 Billion |

| Market Size (2030) | USD 109.40 Billion |

| Growth Rate (2025 - 2030) | 6.40% CAGR |

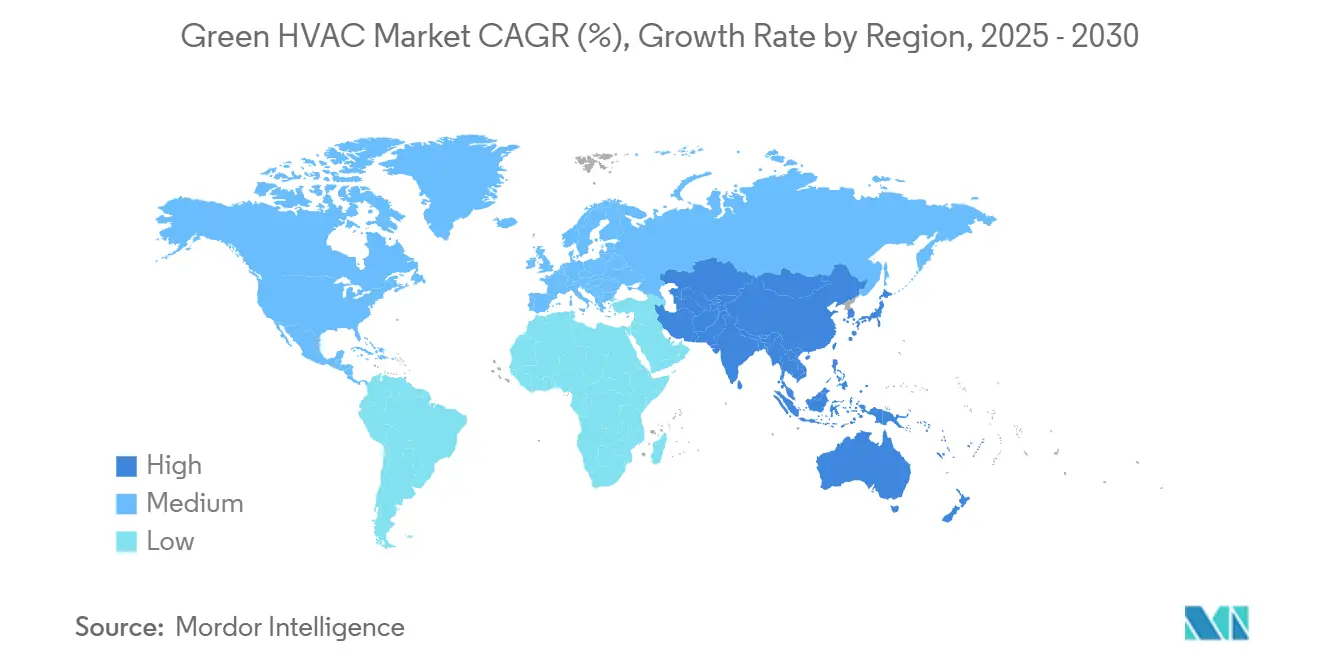

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

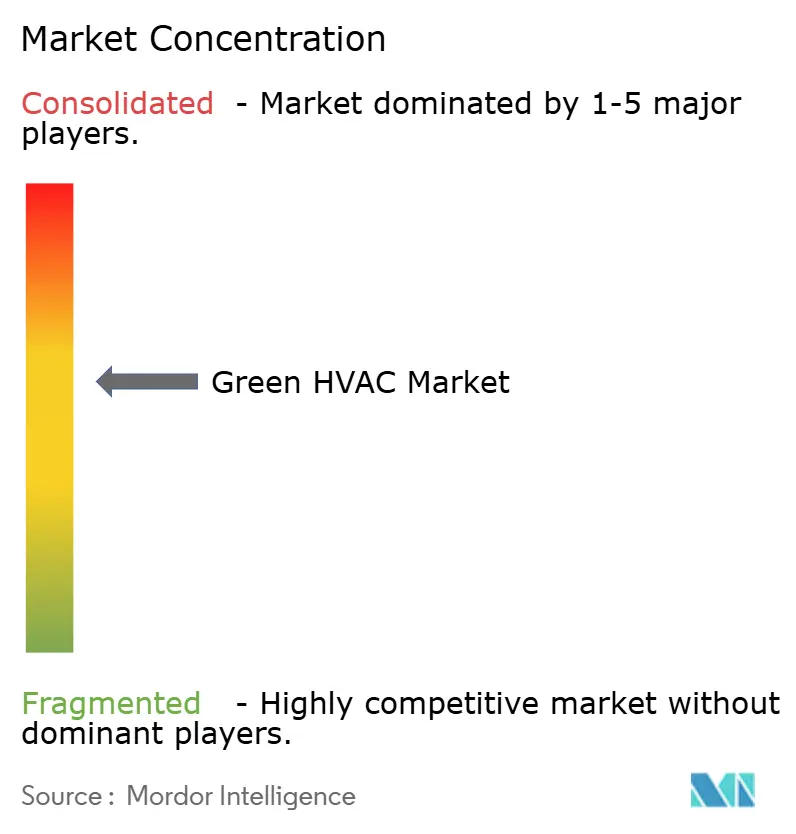

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Green HVAC Market Analysis by Mordor Intelligence

The Green HVAC market size is estimated at USD 80.23 billion in 2025 and is projected to reach USD 109.40 billion by 2030, representing a 6.4% CAGR. This acceleration reflects tightening global efficiency mandates, generous electrification incentives, and rapid cost declines in inverter-driven compressors that together tilt procurement toward low-carbon equipment. Regulatory tailwinds, such as the United States Inflation Reduction Act’s USD 14 billion in heat-pump rebates and the European Union’s F-Gas phase-down, are steering buyers away from fossil-fuel systems toward electric, low-GWP alternatives. Alongside direct subsidies, digital-twin analytics now cut lifetime HVAC operating costs 15-25%, strengthening the business case for connected equipment. The Asia-Pacific region leads current demand with a 44.9% revenue share, driven by China’s heat-pump subsidies and India’s surging cooling intensity. However, Europe is setting de facto technology standards through low-GWP rules that global manufacturers must meet to stay competitive. Supply-chain tightness, especially a shortage of 70,000 trained heat-pump technicians in Europe, continues to influence product design, favoring factory-charged, installer-friendly platforms.

Key Report Takeaways

- By technology, heat pumps accounted for 38.9% of the Green HVAC market share in 2024, while smart HVAC controls are projected to grow at a 7.9% CAGR through 2030.

- By component, heating equipment led with 48.1% share of the Green HVAC market in 2024; controls and services are forecast to expand at a 7.7% CAGR through 2030.

- By end-user, the commercial segment held a 42.6% share of the Green HVAC market in 2024; industrial and data-center applications are projected to advance at a 7.2% CAGR through 2030.

- By application, new construction captured a 56.7% share of the Green HVAC market in 2024; retrofit and replacement projects are set to rise at a 7.1% CAGR through 2030.

- By geography, the Asia-Pacific region dominated with a 44.9% share of the Green HVAC market in 2024 and is expected to post the fastest CAGR of 6.9% to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification incentives and IRA tax credits | +1.2% | North America, spillover to EU and APAC | Medium term (2–4 years) |

| EU F-Gas phase-down, low-GWP mandates | +0.9% | Europe core, global regulatory influence | Long term (≥ 4 years) |

| Inverter-compressor cost fall (< USD 100/kW) | +1.1% | Global, manufacturing centered in APAC | Short term (≤ 2 years) |

| Digital twins cut lifetime OPEX 15-25% | +0.8% | North America and EU leading, APAC adoption rising | Medium term (2–4 years) |

| HVAC-as-a-Service performance contracts | +0.7% | Global commercial sector, strongest in developed markets | Long term (≥ 4 years) |

| Embodied-carbon scoring in green tenders | +0.5% | EU, North America, emerging APAC cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Incentives Drive Market Transformation

Generous tax credits and rebates are tipping procurement decisions toward electric heat pumps. The U.S. Inflation Reduction Act allocates USD 14 billion for rebates, and individual households can claim up to USD 8,000 for qualifying installations.[1]U.S. Department of Energy, “Biden-Harris Administration Launches $9 Billion Home Energy Rebate Programs to Lower Energy Costs,” energy.gov State initiatives such as California’s TECH Clean California add additional grants, amplifying federal dollars. Commercial owners are increasingly treating electrification as a hedge against carbon-pricing risk, locking in predictable operating costs while boosting their ESG scores. Taken together, these programs increase total addressable demand across residential and light-commercial segments, injecting momentum into the Green HVAC market.

EU F-Gas Regulations Accelerate Low-GWP Transition

The EU’s rule to cut hydrofluorocarbon use by 79% by 2030 forces manufacturers to redesign systems for natural refrigerants, such as CO₂ and propane.[2]European Commission, “EU Legislation to Control F-gases,” climate.ec.europa.eu Compliance deadlines starting in 2025 cover commercial refrigeration first, then room air conditioners. Multinationals are pre-emptively rolling out EU-compliant platforms globally, effectively transforming the Green HVAC market into a low-GWP default. Carrier, for example, earmarked USD 85 million for European R&D specific to natural-refrigerant systems, signaling a strategic pivot toward globally harmonized design.

Inverter Technology Cost Reduction Enables Mass Adoption

Vertical integration among leading APAC manufacturers has driven inverter-compressor costs below USD 100 per kilowatt, a threshold that makes variable-speed heat pumps cost-competitive with gas furnaces even without subsidies. Scale economies in semiconductor fabrication and motor production have slashed BOM costs by 30-40%. As a result, formerly premium features, such as cold-climate variable-speed operation, are entering mainstream price tiers, accelerating adoption across the Green HVAC market.

Digital Twin Integration Transforms Operational Economics

Cloud-based digital twins overlay physics models on live building data, enabling 15-25% energy savings and extending equipment life by 20%.[3]Johnson Controls, “Digital Twins Transforming Building Operations,” johnsoncontrols.com Early adopters leverage these tools to secure higher lease rates and lower insurance premiums by proving risk mitigation. Vendors that combine equipment, software, and services into an integrated offer gain a durable advantage as building owners shift toward outcome-based contracts that value lifecycle savings more than upfront discounts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital for heat-pump retrofits | −0.8% | Global, acute in cost-sensitive residential markets | Medium term (2–4 years) |

| Electricity-to-gas price ratio > 3:1 | −0.6% | Europe, varies by country | Short term (≤ 2 years) |

| Installer shortage (≈ 70,000 EU techs) | −0.7% | Europe, North America, nascent APAC issue | Long term (≥ 4 years) |

| Semiconductor/compressor supply volatility | −0.5% | Global manufacturing, concentrated APAC hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs Constrain Residential Adoption

Typical residential heat-pump retrofits cost USD 15,000–25,000, which includes panel upgrades and ductwork modifications.[4]Rocky Mountain Institute, “Heat Pumps for All,” rmi.org Older housing stock often requires insulation fixes, adding another USD 5,000–10,000, lengthening payback periods. Financing tools such as on-bill repayment help, but cash-flow sensitivity continues to slow replacement cycles in the Green HVAC market. Manufacturers now prioritize plug-and-play designs that reduce labor hours, while utilities trial tariff structures that reward electrified homes.

European Energy Price Disparities Limit Heat-Pump Economics

In Germany and Italy, industrial electricity costs EUR 0.15 kWh, compared to a natural-gas parity of EUR 0.05 kWh, resulting in paybacks of seven years even with subsidies. Unless ongoing grid-balancing reforms reduce retail power costs, heat pump adoption will skew toward markets with abundant renewable supply or stronger incentive stacks, thereby mitigating potential growth in the Green HVAC market size in selected EU nations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Heat Pumps Anchor Portfolio Diversification

Heat pumps contributed 38.9% of the 2024 Green HVAC market size and remain the technology benchmark for decarbonizing space conditioning. Their dual heating-cooling role, allied with falling component costs, cements their position in both residential and light-commercial upgrades. Smart controls, although having a smaller base today, are expected to record the fastest 7.9% CAGR, thanks to predictive maintenance and grid-interactive functionality.

Manufacturers are increasingly marketing integrated packages that pair heat pumps with IoT sensors, VRF modules, and cloud analytics to sell “comfort-as-a-service.” Daikin’s VRV platform now bundles occupancy sensors that cut service calls by 30%, illustrating how software-heavy offerings accelerate customer. This convergence sharpens competitive differentiation within the Green HVAC market as buyers prefer holistic solutions over stand-alone units.

By Component: Controls and Services Monetize Lifecycle Value

Heating equipment accounted for 48.1% of revenue in 2024, but growth is tilting toward controls and services, which are expanding at a 7.7% CAGR as facility teams pursue lifecycle savings. Digital controllers integrate ventilation, cooling, and indoor air quality modules, forming the nerve center of smart buildings.

Schneider Electric’s EcoStruxure demonstrates how software subscriptions drive recurring revenue while reducing customer energy bills by 20–30%. Given the tightening of talent pools, outsourced monitoring services are becoming central to building managers, a trend that reallocates value capture across the Green HVAC market.

By End-User: Data Centers Propel Industrial Momentum

Commercial facilities retained a 42.6% share in 2024, but data-center and broader industrial applications show the fastest 7.2% CAGR as digitization elevates cooling density. Hyperscale operators invest in liquid cooling and precision temperature control, turning thermal management into a mission-critical service.

Manufacturing reshoring drives additional industrial load, particularly for low-temperature process heat that is compatible with renewable electricity. Vendors that can customize heavy-duty heat pumps and integrate them with plant energy-management systems seize high-margin niches within the Green HVAC market.

By Application: Retrofits Gain Budget Priority

While new construction generated 56.7% of 2024 revenues, retrofit demand grows at a 7.1% CAGR as cities impose emission caps on existing stock. Local laws such as New York City’s LL97 push building owners toward accelerated equipment replacement, creating a USD 15 billion annual North American retrofit pipeline.

Retrofit complexity rewards suppliers offering turnkey engineering, financing, and performance guarantees. Trane’s optimization service, which pairs equipment upgrades with continuous commissioning, underscores how value migrates from hardware to outcome-oriented contracts. This model reinforces recurring revenue potential across the Green HVAC market.

Geography Analysis

Asia-Pacific generated 44.9% of 2024 revenue for the Green HVAC market and is poised for a 6.9% CAGR through 2030. China’s rural electrification roadmap targets 10 million household heat-pump conversions, while India’s commercial construction boom fuels VRF and chiller demand. Regional manufacturers enjoy local scale that shortens lead times and aligns products with subsidy criteria set by governments intent on domestic industrial growth.

Europe balances strong policy pushes with uneven economics. Nordic nations pair abundant renewable electricity with carbon taxation to achieve leading residential penetration, whereas Germany and Italy wrestle with unfavorable power-to-gas ratios that slow paybacks. Technician shortages compound the challenge, prompting initiatives to re-skill workforces at unprecedented scale. EU-wide low-GWP mandates, however, ensure technology innovation remains centered in the region, influencing design choices globally within the Green HVAC market.

North America benefits from unified federal incentives layered on top of strong state programs. California’s Title 24 codes require heat-pump readiness, accelerating demand in both new builds and retrofits. Canada’s rebate framework supports cold-climate models rated for −15 °F operation, opening northern markets previously dominated by gas furnaces. Meanwhile, Mexico’s manufacturing corridors expand commercial HVAC opportunities tied to nearshoring supply chains. Collectively these dynamics keep the continent a strategic revenue pillar for global suppliers competing in the Green HVAC market.

Competitive Landscape

First-tier manufacturers, such as Daikin, Carrier, and Johnson Controls, maintain scale leadership through broad portfolios and global service networks; however, software-native entrants now challenge incumbents with AI-based optimization layers. Patent activity in variable-speed compressors and refrigerant algorithms increased by 15% per year between 2022 and 2024, underscoring a rapid pace of innovation.

Strategic differentiation revolves around three capabilities. First, cost leadership achieved through component integration and regionalized manufacturing enables price points to be defended in the budget segment of the Green HVAC market. Second, proprietary software platforms amplify equipment efficiency and lock in service fees. Third, outcome-oriented contracts, such as HVAC-as-a-Service, shift the customer's focus to guaranteed savings rather than capital expenditures.

Recent consolidations echo these priorities: Johnson Controls acquired Silent-Aire to expand its data-center cooling reach, and Mitsubishi Electric invested USD 120 million in European low-GWP R&D to preempt regulatory shifts. Mid-sized regional players are seeking alliances with sensor firms and cloud providers to maintain their relevance. Market entrants that combine digital expertise with specialization in low-GWP or cold-climate systems hold disproportionate disruption potential across the Green HVAC market.

Green HVAC Industry Leaders

-

Daikin Industries, Ltd.

-

Carrier Global Corporation

-

Johnson Controls International plc

-

Trane Technologies plc

-

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Daikin Industries committed USD 150 million to expand Texas heat-pump capacity to 500,000 units per year.

- December 2024: Johnson Controls bought Silent-Aire’s data-center cooling division for USD 85 million.

- November 2024: Carrier Global introduced the OptiClean UV-C–enabled air-purification system.

- October 2024: Trane Technologies partnered with Microsoft to deploy AI-based building optimization across 1,000 sites.

Global Green HVAC Market Report Scope

| Heat Pumps |

| Variable Refrigerant-Flow (VRF) Systems |

| Smart HVAC Controls |

| Inverter Air-Conditioners |

| Heating Equipment |

| Cooling Equipment |

| Ventilation and IAQ Equipment |

| Controls and Services |

| Residential |

| Commercial |

| Industrial and Data-Centre |

| Public and Institutional |

| New Construction |

| Retrofit / Replacement |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Technology | Heat Pumps | |

| Variable Refrigerant-Flow (VRF) Systems | ||

| Smart HVAC Controls | ||

| Inverter Air-Conditioners | ||

| By Component | Heating Equipment | |

| Cooling Equipment | ||

| Ventilation and IAQ Equipment | ||

| Controls and Services | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial and Data-Centre | ||

| Public and Institutional | ||

| By Application | New Construction | |

| Retrofit / Replacement | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Green HVAC market?

The Green HVAC market size is USD 80.23 billion in 2025 and is projected to reach USD 109.40 billion by 2030.

Which region leads demand?

Asia-Pacific holds 44.9% of 2024 revenue and is forecast as the fastest-growing at 6.9% CAGR through 2030.

Which technology dominates sales?

Heat pumps contribute 38.9% of 2024 revenue, making them the largest technology segment.

What segment shows the highest growth?

Smart HVAC controls register the fastest 7.9% CAGR owing to predictive-maintenance and energy-optimization features.

What restrains residential adoption?

High retrofit costs of USD 15,00025,000 and installer shortages slow replacement cycles despite incentives.

How are suppliers differentiating?

Vendors integrate software analytics and offer service contracts that guarantee lifecycle savings, moving beyond stand-alone equipment sales.

Page last updated on: