Market Overview

| Study Period | 2019 - 2030 |

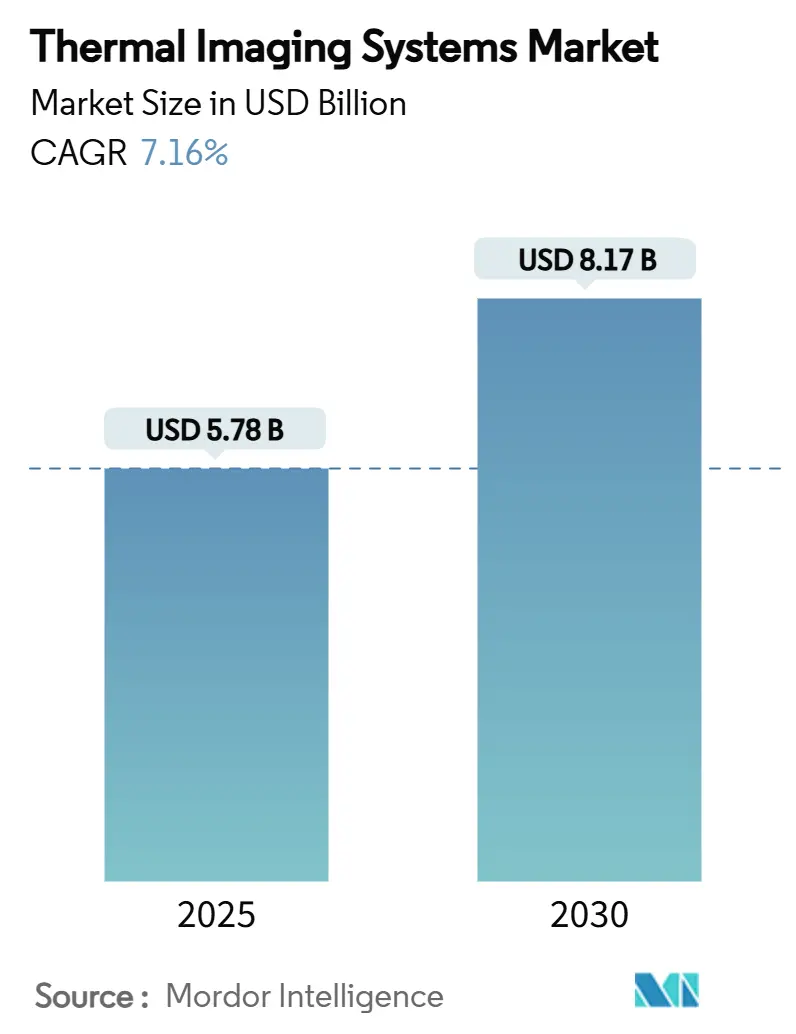

| Market Size (2025) | USD 5.78 Billion |

| Market Size (2030) | USD 8.17 Billion |

| Growth Rate (2025 - 2030) | 7.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thermal Imaging Systems Market Analysis by Mordor Intelligence

The thermal imaging systems market size is valued at USD 5.78 billion in 2025 and is forecast to reach USD 8.17 billion by 2030, expanding at a 7.16% CAGR. Accelerating defense modernization, expanding industrial automation, and mandated automotive safety features are converging to keep demand elevated. Standardization around NFPA-70B thermography is stimulating steady procurement cycles in manufacturing and utilities, while uncooled long-wave infrared (LWIR) price declines are widening accessibility. In parallel, vehicle makers are integrating night-vision cameras into Advanced Driver-Assistance Systems (ADAS) to comply with pending pedestrian-protection rules. The momentum is reinforced by Indo-Pacific ISR budgets, with military programs in the United States and Australia placing multi-year orders for next-generation FLIR sensors.

Key Report Takeaways

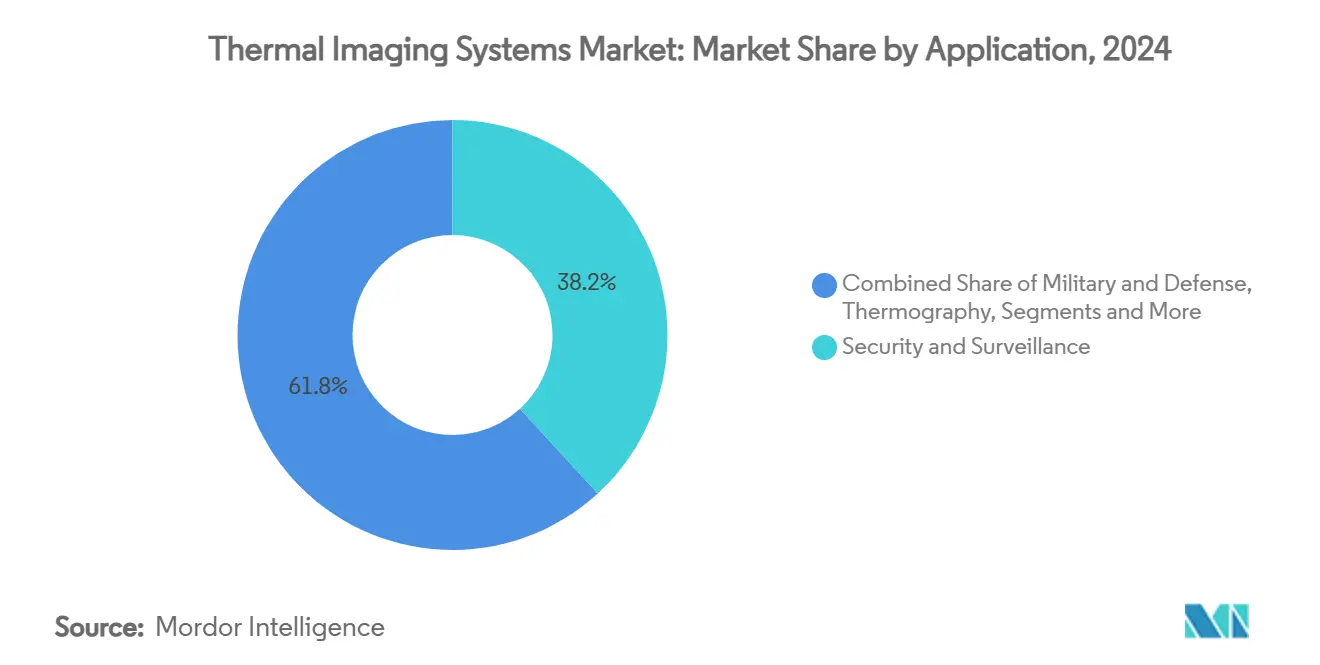

- By application, security and surveillance commanded 38.2% of 2024 thermal imaging systems market share, while automotive ADAS is forecast to post a 7.8% CAGR to 2030.

- By form factor, hand-held units led with 46.4% revenue share in 2024; integrated OEM modules are projected to register a 7.2% CAGR through 2030.

- By technology, uncooled LWIR retained 72.5% of 2024 thermal imaging systems market size; short-wave infrared (SWIR) is expected to be the fastest-growing segment at 7.5% CAGR.

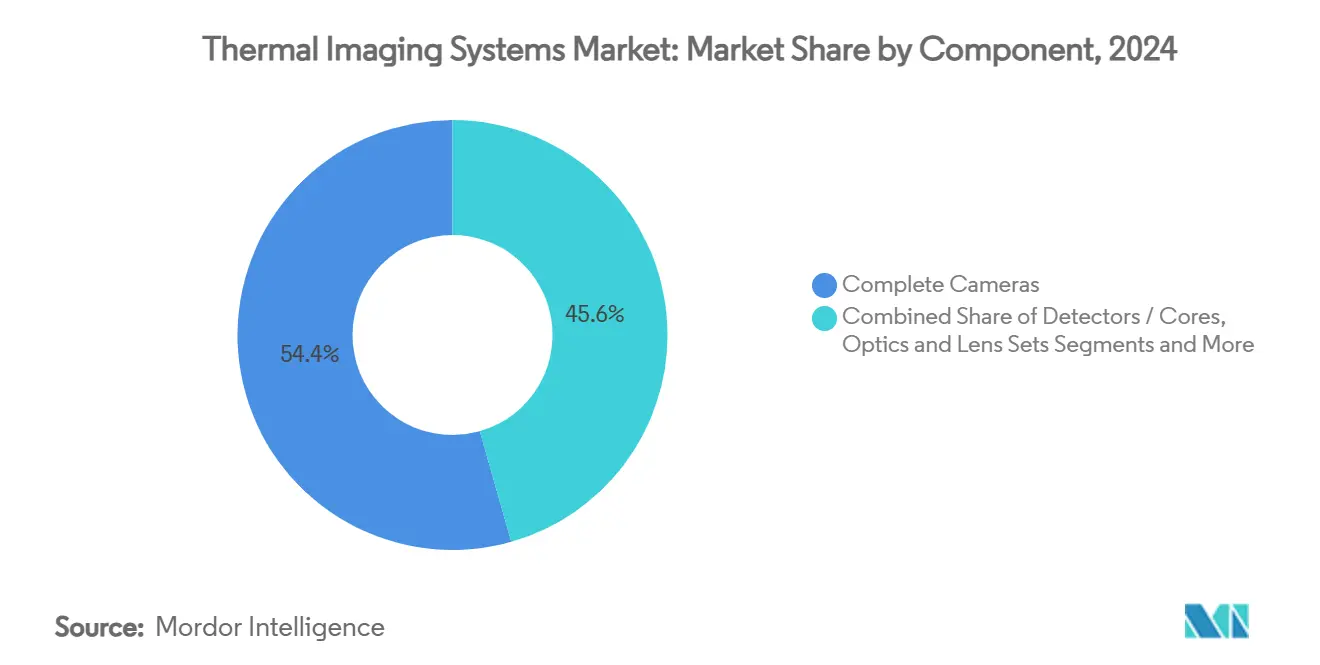

- By component, complete cameras generated 54.4% of 2024 sales, yet software analytics is positioned for the highest 8.9% CAGR by 2030.

- By end-user, defense accounted for 35.6% of 2024 revenue, though automotive is forecast to expand at an 8.0% CAGR during 2025-2030.

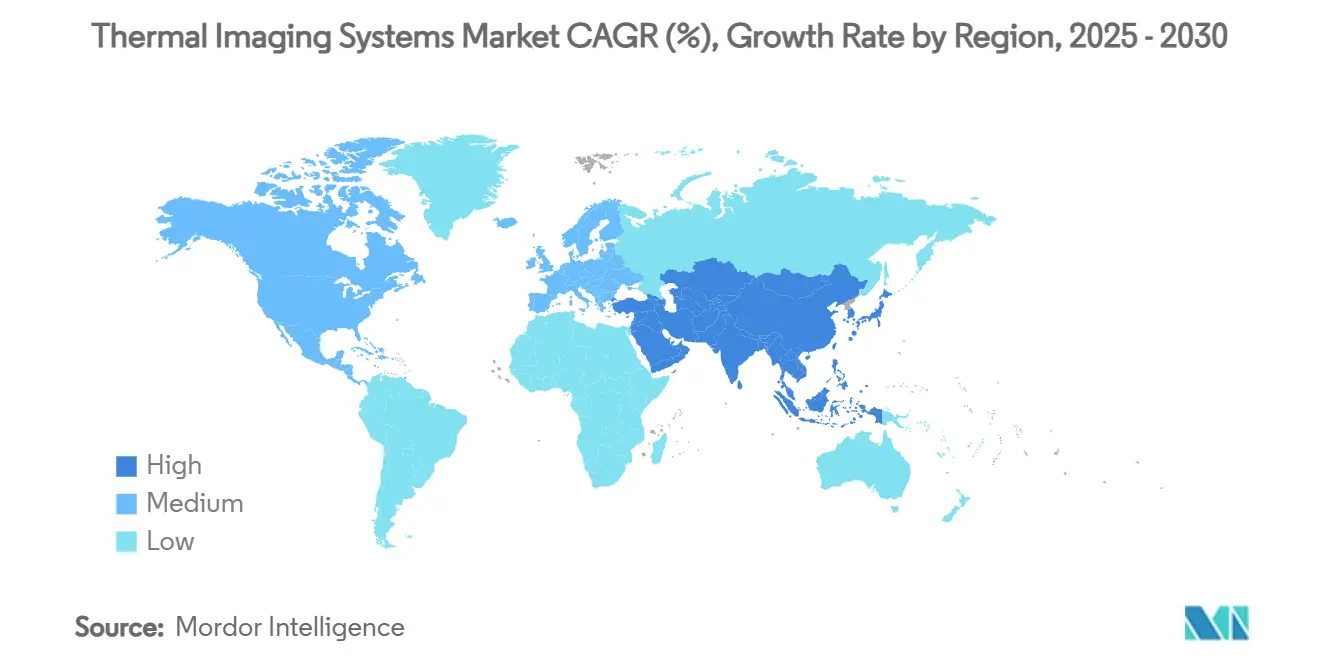

By geography, North America held 41.5% of 2024 revenue; Asia-Pacific is projected for the quickest 8.3% CAGR.

Global Thermal Imaging Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling price of uncooled micro-bolometers | +1.2% | Global, strongest in APAC & emerging markets | Medium term (2-4 years) |

| Growing defense ISR budgets in Indo-Pacific | +1.8% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Mandatory NFPA-70B thermography | +0.9% | North America & EU, adoption in industrial hubs | Short term (≤ 2 years) |

| Vehicle OEM push for cost-effective ADAS night-vision | +1.4% | Global manufacturing centers, led by EU & APAC | Medium term (2-4 years) |

| AI-enabled predictive maintenance in smart factories | +0.8% | Germany, Japan, South Korea, China | Medium term (2-4 years) |

| Climate-driven wildfire monitoring demand | +0.5% | North America West Coast, Australia, Mediterranean | Long term (≥ 4 years) |

Source: Mordor Intelligence

Falling Price of Uncooled Micro-Bolometers

Cost curves for uncooled detectors continue to decline, enlarging addressable opportunities beyond defense and heavy industry. Scale economies, simplified fabrication, and alternative chalcogenide optics from firms such as LightPath are mitigating historic germanium bottlenecks. Smartphone OEMs are piloting thermal add-ons, and fleet operators are specifying thermographic inspections under corporate ESG programs. The broader commercial reach strengthens pricing power for analytics software that converts raw images into actionable insights.

Growing Defense ISR Budgets in Indo-Pacific

Regional security competition is stimulating long-range surveillance procurements. The United States’ Pacific Deterrence Initiative allocates USD 9.9 billion for advanced sensors, while Australia’s AUD 50 billion (USD 34.7 billion) defense roadmap earmarks funds for multispectral imaging platforms. [1]Department of Defense, "Pacific Deterrence Initiative FY 2025," comptroller.defense.govCombined with SBIR grants supporting dual-band FLIR arrays, the pipeline sustains multi-year volume visibility for detector foundries and optics suppliers.

Mandatory NFPA-70B Thermography for Electrical Safety

The 2024 edition of NFPA-70B moves thermography from a recommended to a required practice in preventive maintenance, compelling factories, data centers, and utilities to equip electrical technicians with calibrated imagers.[2]Mike Amundsen, “What are the Reporting Requirements for Thermography According to NFPA 70B 2023,” IRInfo, irinfo.orgInspection frequency clauses promote recurring hardware refresh cycles and subscription analytics, fortifying mid-single-digit replacement demand even in mature markets.

Vehicle OEM Push for Cost-Effective ADAS Night-Vision

Upcoming pedestrian automatic emergency-braking mandates are accelerating the inclusion of thermal sensors alongside radar and LiDAR in Level 2-plus platforms. Lens suppliers such as Ophir Optics have scaled automotive-grade infrared glass to meet stringent reliability standards. Tier-1s are selecting narrow-field modules with on-chip AI to minimize central ECU loads, a move that supports incremental detector ASP uplift within the cost-constrained passenger-car value chain.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control regimes (ITAR & EAR) | -0.7% | Global, strongest on US exporters | Long term (≥ 4 years) |

| High cap-ex for cooled MWIR cameras | -0.4% | Defense & aerospace globally | Medium term (2-4 years) |

| Supply-chain choke points in germanium optics | -0.6% | Precision optics worldwide | Short term (≤ 2 years) |

| Cyber-security risks in networked cameras | -0.3% | Connected infrastructure globally | Medium term (2-4 years) |

Source: Mordor Intelligence

Export-Control Regimes (ITAR & EAR)

Evolving US export rules mandate licenses for many dual-use focal-plane arrays and optics kits, elongating sales cycles and limiting addressable international revenue.[3]U.S. Department of Commerce, “15 CFR § 743.3 – Thermal imaging camera reporting,” Cornell Law School, law.cornell.edu Recent proposals would pull previously uncontrolled commercial imagers into license categories, prompting OEMs to accelerate non-US supply-chain localization. The policy uncertainty introduces compliance costs that particularly burden small-volume niche innovators.

High Cap-Ex for Cooled MWIR Cameras

Cooled mid-wave solutions deliver superior sensitivity and long-range detection yet require integrated cryocoolers, driving unit prices beyond the budgets of many civilian buyers. Capital intensity continues to confine adoption to defense, aerospace, and select petrochemical sites where performance justifies cost.

Segment Analysis

By Application: Security Dominance Amid ADAS Acceleration

Security and surveillance held 38.2% of 2024 revenue, reinforcing the foundational role of perimeter protection in the thermal imaging systems market. Increasing border-control spending and critical infrastructure hardening sustain procurement of fixed and pan-tilt-zoom cameras, while AI-driven analytics cut operator workload. Automotive ADAS, the fastest-growing application at a 7.8% CAGR, capitalizes on regulatory nudges for pedestrian safety and automated emergency braking. OEM design cycles that once specified infrared as optional are now embedding compact modules into higher-volume trims, broadening annual shipment baselines.

Demand diversification is evident in thermography services as factories comply with NFPA-70B, creating annuity-style inspection revenue. Firefighting agencies are equipping frontline responders with thermal monoculars, leveraging satellite-driven hotspot alerts for rapid deployment. Emerging mobile apps pairing smartphones with clip-on micro-bolometers signal the consumerization phase of the thermal imaging systems market.

Note: Segment shares of all individual segments available upon report purchase

By Form Factor: Handheld Leadership Challenged by OEM Integration

Hand-held imagers captured 46.4% of 2024 revenue, favored for versatility across preventive maintenance, law enforcement, and first-responder scenarios. The convenience of battery-operated units sustains significant replacement demand, especially as detector resolution improves. Integrated OEM modules, however, are set to outpace at a 7.2% CAGR, underpinning the expansion of the thermal imaging systems market size inside vehicles, drones, and smart appliances. Fixed-mount solutions remain indispensable in perimeter security and process monitoring where 24/7 coverage is mandatory.

Military procurement emphasizes Size, Weight, Power, and Cost (SWaP-C) gains, driving proprietary shutterless calibration and edge AI to compress payload footprints. Flexible infrared sensors in development promise future wearables, although commercialization is still several design iterations away.

By Technology: Uncooled LWIR Dominance Faces SWIR Challenge

Uncooled LWIR retained 72.5% of 2024 thermal imaging systems market share thanks to favorable economics and broad spectral suitability. SWIR’s projected 7.5% CAGR rests on its ability to pierce smoke, haze, and glass, positioning it for airborne surveillance, industrial analytics, and mining. Cooled MWIR stays essential for missile tracking and border surveillance where extreme sensitivity is non-negotiable despite higher lifecycle cost.

Defense R&D investments in dual-band focal-plane arrays are blurring traditional boundaries, enabling combined LWIR-MWIR payloads that shorten target identification times. Commercial interest in multispectral fusion is accelerating as security integrators seek to curb nuisance alarms in critical infrastructure.

By Component: Software Analytics Drive Value Creation

Complete cameras generated 54.4% of 2024 sales, but revenue gravity is shifting toward software platforms that convert imagery into prescriptive maintenance or threat alerts. Analytics subscriptions are forecast for an 8.9% CAGR as plant managers prioritize OPEX over CAPEX. Optics and lens sets must evolve to meet higher pixel densities, while detector manufacturers invest in wafer-level packaging to cut costs.

Edge computing inside cameras minimizes cloud round-trip latency, and post-quantum encryption initiatives are becoming table stakes for critical-infrastructure bids. Camera makers bundling secure firmware, AI toolchains, and continuous updates are capturing premium margins in the thermal imaging systems market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Defense Leadership Amid Automotive Surge

Defense commanded 35.6% of 2024 sales, a role unlikely to weaken given ISR funding trajectories. Still, automotive ADAS, at an 8.0% CAGR, supplies the steepest volume ramp and broadens the customer mix within the thermal imaging systems industry. Industrial verticals use thermography to pre-empt downtime, while commercial real-estate security modernizes with coordinated visible-thermal analytics. Medical fever screening remains niche but steady as hospitals maintain elevated hygiene protocols.

Wildfire management agencies partner with satellite operators to secure sovereign imagery, while insurance firms encourage factory upgrades to lower fire-related payouts. These diverse demand vectors insulate suppliers from single-vertical volatility and underpin healthy top-line visibility.

Geography Analysis

North America led with 41.5% of 2024 spending, reflecting defense allocations such as the US Army’s USD 117.5 million order for third-generation FLIR sensors. NFPA-70B compliance further bolsters industrial uptake, and automotive Tier-1s are piloting night-vision programs for 2027 model years. Cybersecurity directives from CISA drive premium demand for hardened firmware, enabling US-based vendors to maintain pricing discipline.

Asia-Pacific is projected to log the highest 8.3% CAGR as Japan, South Korea, India, and Australia diversify ISR fleets and expand vehicle exports. China’s share shift from 15% to 63% in thermography during 2019-2020 illustrates the manufacturing scale at play. Indigenous sensor ecosystems are maturing, yet export controls restrict access to state-of-the-art US technology, fueling regional R&D investment.

Europe posts steady growth, buoyed by defense optronics orders and automotive safety regulations. HENSOLDT’s 34% revenue surge in its Optronics segment underscores resilient procurement. Middle East and Africa register firm demand for perimeter surveillance, with Teledyne FLIR shipping multi-sensor pods to Saudi Arabia. South America remains emergent, but industrial maintenance and public-safety budgets point to incremental upside.

Competitive Landscape

The thermal imaging systems market features moderate concentration, with diversified conglomerates, focused defense contractors, and specialized optics suppliers contending for share. Teledyne’s USD 770 million 2025 acquisition spree underscores a strategy of technology breadth and vertical integration. Leonardo DRS leveraged record Q1 2025 bookings of USD 1 billion to scale dual-use product lines.

Players differentiate through proprietary detectors, ruggedized optics, and AI-enabled analytics. Partnerships with automotive Tier-1s help capture ADAS pipelines, while OEMs court industrial integrators to embed analytics into factory MES platforms. Material-science innovation, notably alternative chalcogenide lenses, offers a hedge against germanium risks. Start-ups that focus on wildfire monitoring or cloud-native predictive maintenance force incumbents to balance defense backlogs with commercial agility.

Three strategic patterns dominate: 1) acquisition-driven portfolio expansion to address white-space verticals; 2) dual-use technology transfer from defense to commercial sectors; and 3) investment in secure, upgradable software stacks to lock in lifecycle revenue. The result is a competitive field where brand reputation, export-licensing expertise, and R&D velocity remain decisive.

Thermal Imaging Systems Industry Leaders

-

Opgal Optronic Industries Ltd.

-

Fluke Corporation

-

Testo Inc.

-

Seek Thermal Inc.

-

Teledyne FLIR

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Teledyne FLIR Defense secured contract with Middle East Task Company to supply Lightweight Vehicle Surveillance System integrating TacFLIR 380HD to Saudi military, deliveries by end-2025

- February 2025: Canadian Space Agency awarded CAD 72 million contract to Spire Global and OroraTech for WildFireSat constellation with advanced thermal payloads, targeting 2029 launch.

- January 2025: Teledyne Technologies completed acquisition of Excelitas’ aerospace and defense electronics businesses, deploying USD 770 million to deepen sensor portfolio.

- July 2024: US Army placed USD 117.5 million low-rate production order with Raytheon for third-generation FLIR sensors featuring dual-band arrays.

Global Thermal Imaging Systems Market Report Scope

The scope of the study includes both imagers and thermal cameras. Thermal Detectors with main functionality to sense & detect thermal radiation as opposed to imagers, whose main function is to take an image of thermal radiation.

The Thermal Imaging Systems market is segmented by Application (Thermography, Military, Surveillance, Personal Vision Systems, Fire Fighting, Smartphones (Ruggedized)), Form Factor (Handheld Imaging Devices and Systems, Fixed Mounted Systems), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Application | Security and Surveillance | |||

| Military and Defense | ||||

| Thermography / Inspection | ||||

| Firefighting | ||||

| Personal Vision Systems | ||||

| Smartphones and Tablets | ||||

| Automotive ADAS | ||||

| Maritime and Aerospace | ||||

| By Form Factor | Hand-held Imaging Devices | |||

| Fixed-mount (Rotary / Non-rotary) | ||||

| Integrated OEM Modules | ||||

| By Technology | Uncooled LWIR | |||

| Cooled MWIR | ||||

| SWIR and Multispectral | ||||

| By Component | Detectors / Cores | |||

| Complete Cameras | ||||

| Optics and Lens Sets | ||||

| Software and Analytics | ||||

| By End-user Industry | Defense and Homeland Security | |||

| Industrial | ||||

| Commercial | ||||

| Medical | ||||

| Public Safety | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia Pacific | China | |||

| Japan | ||||

| South Korea | ||||

| India | ||||

| Australia and NZ | ||||

| ASEAN (Break-up) | ||||

| Rest of Asia Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| UAE | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

By Application

| Security and Surveillance |

| Military and Defense |

| Thermography / Inspection |

| Firefighting |

| Personal Vision Systems |

| Smartphones and Tablets |

| Automotive ADAS |

| Maritime and Aerospace |

By Form Factor

| Hand-held Imaging Devices |

| Fixed-mount (Rotary / Non-rotary) |

| Integrated OEM Modules |

By Technology

| Uncooled LWIR |

| Cooled MWIR |

| SWIR and Multispectral |

By Component

| Detectors / Cores |

| Complete Cameras |

| Optics and Lens Sets |

| Software and Analytics |

By End-user Industry

| Defense and Homeland Security |

| Industrial |

| Commercial |

| Medical |

| Public Safety |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and NZ | |||

| ASEAN (Break-up) | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the thermal imaging systems market?

The market is valued at USD 5.78 billion in 2025 and is projected to reach USD 8.17 billion by 2030, growing at a 7.16% CAGR.

Which application segment is expanding fastest?

Automotive ADAS is forecast to post the highest 7.8% CAGR through 2030 as vehicle makers add night-vision capabilities.

Why is NFPA-70B significant for thermal imaging adoption?

The 2024 revision makes thermography mandatory for electrical preventive maintenance, triggering recurring demand for calibrated cameras and analytics software.

Which technology holds the largest share?

Uncooled LWIR accounts for 72.5% of 2024 revenue due to cost advantages and broad suitability across applications.

What regions are growing quickest?

Asia-Pacific is projected for an 8.3% CAGR through 2030, driven by defense modernization and expanding automotive production.

How are vendors addressing supply-chain risk in germanium optics?

Suppliers are investing in chalcogenide glass and wafer-level packaging to reduce reliance on germanium and stabilize lead times.

Page last updated on: July 11, 2025