Size and Share of Lithium-ion Battery Separator Market for Electric Vehicle Application

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 10.74 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

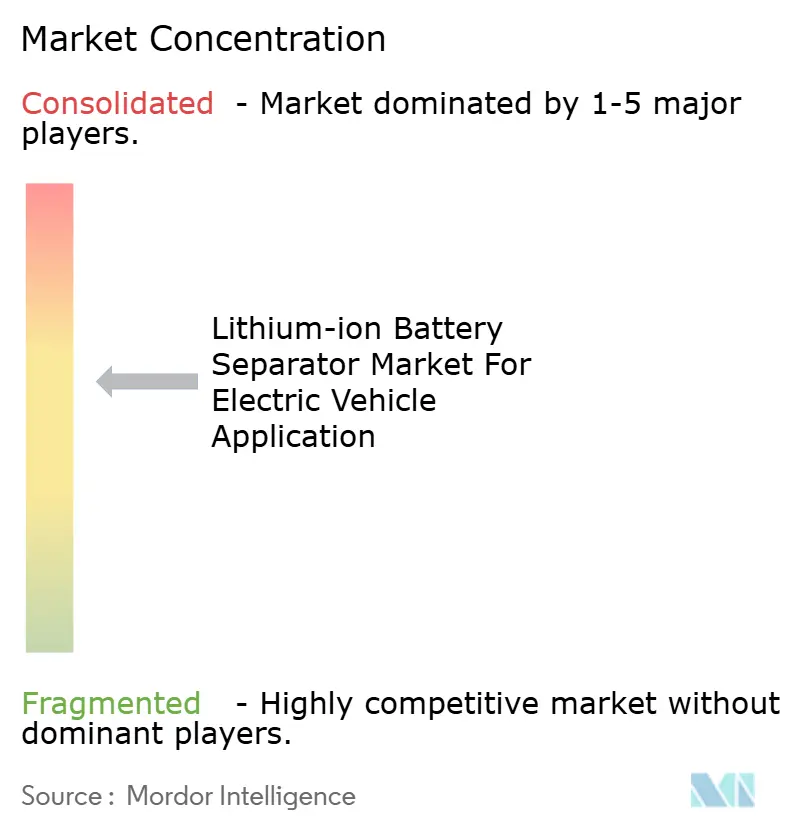

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of Lithium-ion Battery Separator Market for Electric Vehicle Application by Mordor Intelligence

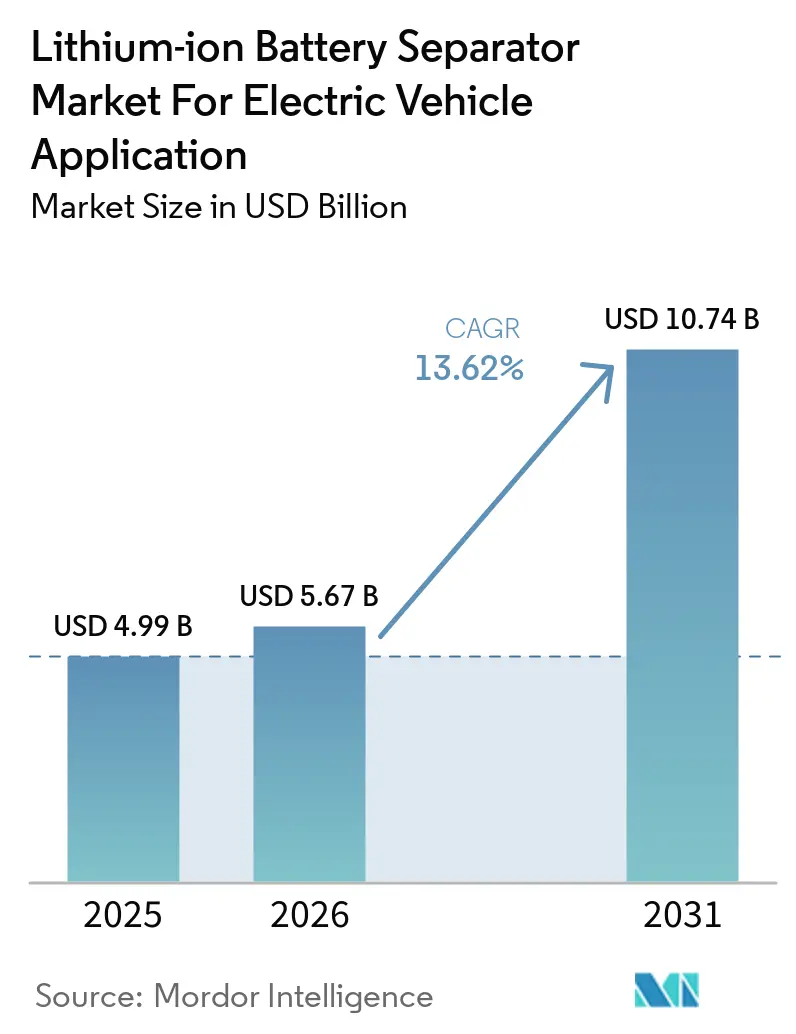

The Lithium-ion Battery Separator Market size For Electric Vehicle Application Industry market size in 2026 is estimated at USD 5.67 billion, growing from 2025 value of USD 4.99 billion with 2031 projections showing USD 10.74 billion, growing at 13.62% CAGR over 2026-2031.

This expansion reflects three converging forces: automakers accelerating their switch to battery-electric platforms, governments subsidizing localized cell production, and cell makers shifting to higher-voltage chemistries that need separators with stronger thermal-shutdown characteristics. Wet-process polyolefin films maintained a 56.5% revenue share in 2024, yet ceramic-coated variants are set to rise at 21.5% a year because premium EV programs demand stronger safety margins. Polypropylene captured 43.8% of the material share in 2024, while non-woven substrates, buoyed by electrospinning advances, are growing at 18.8%. Asia-Pacific generated 55.2% of 2024 revenue on the back of China’s integrated supply chains, but North America is growing the fastest as Section 45X tax credits draw new capacity.

Key Report Takeaways

- By separator type, wet-process polyolefin led with 55.90% of the lithium-ion battery separator market share in 2025; ceramic-coated films are projected to expand at a 20.30% CAGR through 2031.

- By material, polypropylene controlled 43.20% of revenue in 2025; non-woven substrates are advancing at an 18.10% CAGR to 2031.

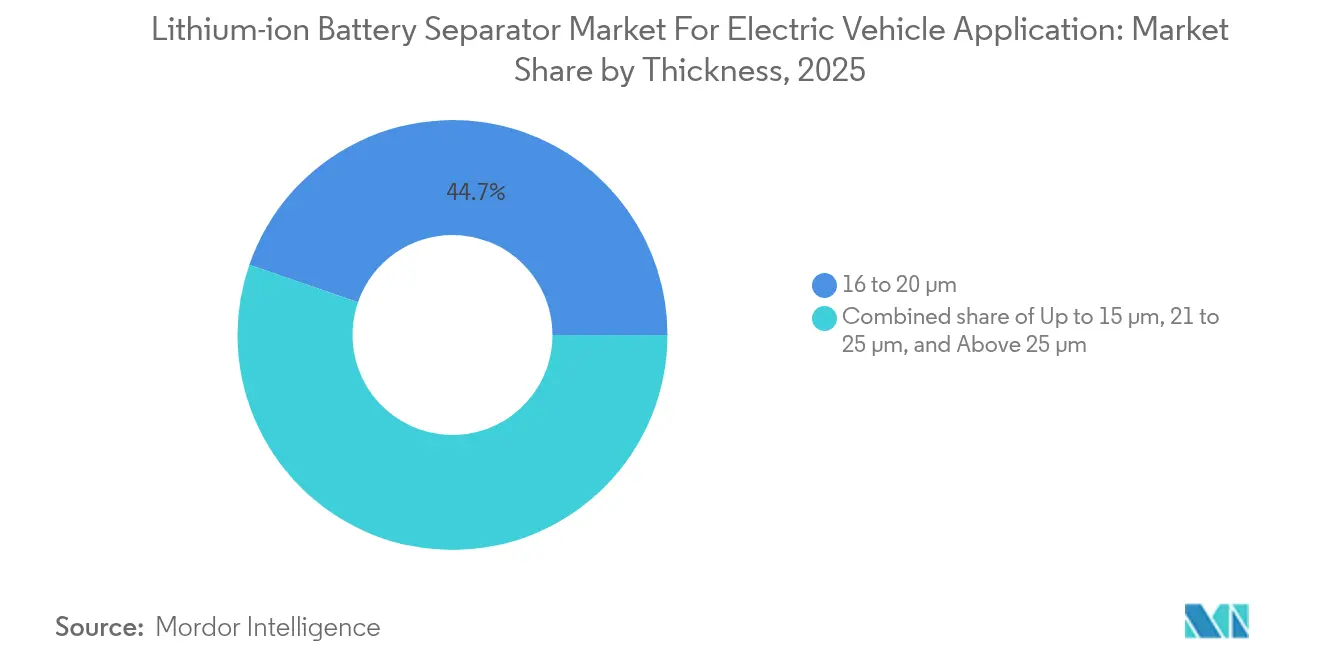

- By thickness, the 16 to 20 micrometer band accounted for 44.70% of the lithium-ion battery separator market size in 2025, while the 21 to 25 micrometer band is set to grow at 17.30% through 2031.

- By battery form factor, pouch cells held 49.00% share in 2025; prismatic cells are expected to record a 18.70% CAGR between 2026 and 2031.

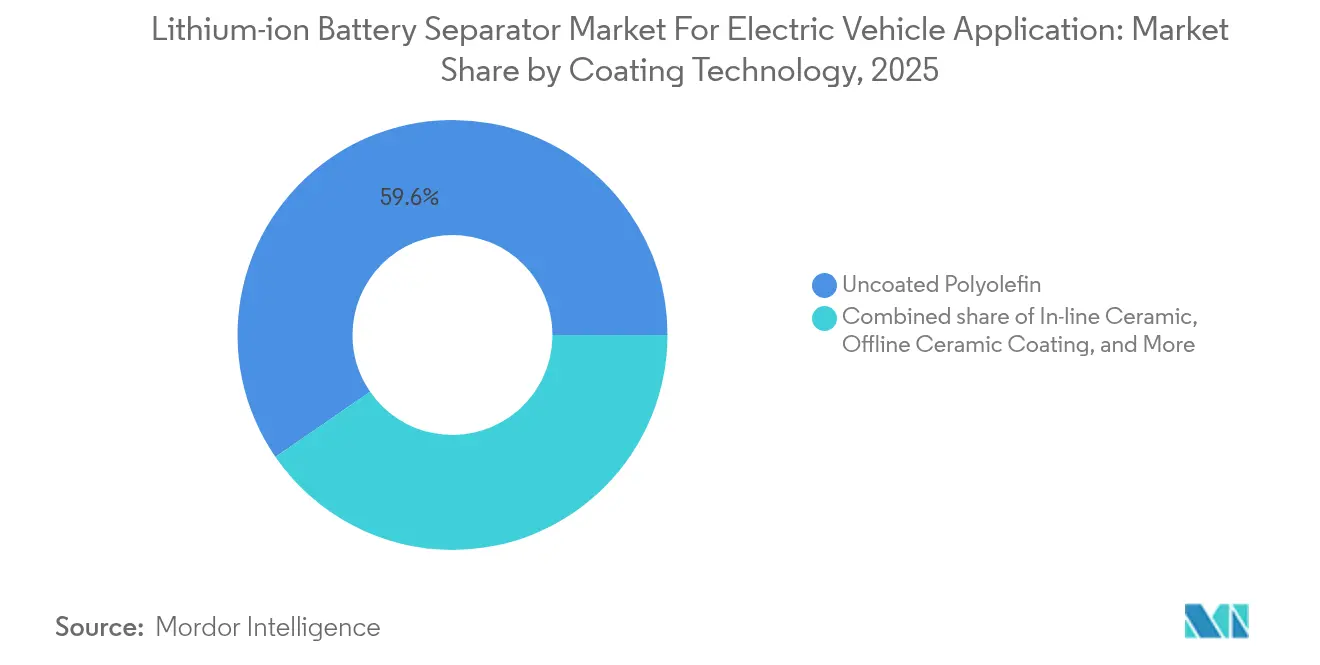

- By coating technology, uncoated polyolefin dominated with a 59.60% share in 2025, but inline ceramic coating is forecast to climb at a 20.60% CAGR.

- By geography, Asia-Pacific captured 54.50% revenue in 2025, yet North America is projected to post the fastest 17.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Lithium-ion Battery Separator Market for Electric Vehicle Application

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring global EV sales and gigafactory build-outs | 4.2% | Global, with concentration in China, North America, Europe | Medium term (2-4 years) |

| Rapid cost decline in wet-process PE/PP separators | 2.8% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Government incentives for domestic battery supply chains | 3.5% | North America (IRA), Europe (EU Battery Regulation), China (subsidy programs) | Medium term (2-4 years) |

| OEM shift to higher-energy 4680 and large-format cells | 2.1% | North America (Tesla), APAC (Panasonic, CATL, BYD) | Long term (≥ 4 years) |

| Adoption of ceramic-coated shutdown layers for thermal safety | 3.3% | Global, led by premium EV segments in Europe and North America | Medium term (2-4 years) |

| Accelerated rollout of high-voltage (>4.4 V) chemistries needing robust separators | 2.6% | Global, with early adoption in premium EV platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Global EV Sales & Gigafactory Build-outs

Global battery-electric vehicle sales crossed 14 million units in 2024, and automakers announced 312 GWh of fresh cell capacity scheduled for 2025–2027. Every gigawatt-hour consumes nearly 2.5 million m² of separator film, tightening supply and prompting multiyear offtake deals that lock volume but raise resin-price exposure.[1]International Energy Agency, “EV Battery Materials Report,” iea.org North America faces a projected 999 GWh separator shortfall by 2029, catalyzing investments such as Asahi Kasei’s 700 million m² plant in Ontario.

Rapid Cost Decline in Wet-Process PE/PP Separators

Automation of phase-separation and stretching steps cut wet-process costs by 30% between 2022 and 2024, tipping competitive balance toward high-throughput Chinese lines. Falling prices free cell makers to allocate savings toward nickel-rich cathodes and silicon anodes that require thicker or coated separators, sustaining wet-process dominance through 2027.

Government Incentives for Domestic Battery Supply Chains

The U.S. Inflation Reduction Act pays USD 0.40 per m² for U.S.-made separators, covering up to 20% of the conversion cost. The EU Battery Regulation mandates carbon-footprint disclosure from 2025 and favors low-carbon supply, steering orders to plants in Poland and Hungary powered by renewables. China continues to fund separator expansions in Jiangsu and Guangdong, cementing cost leadership.

OEM Shift to Higher-Energy 4680 & Large-Format Cells

Tesla’s 4680 cylinder needs separators in the 21–25 µm range with ceramic coatings for thermal integrity. CATL’s cell-to-pack Qilin architecture demands prismatic cells that run thicker films to manage compression. BYD’s Blade battery integrates long prismatic cells into the chassis, relying on polymer-bonded separators for crash resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PP and PE resin supply volatility and price spikes | -1.8% | Global, with acute impact in regions dependent on Middle East naphtha | Short term (≤ 2 years) |

| Stringent battery safety compliance testing costs | -0.9% | North America, Europe (UL, IEC standards) | Medium term (2-4 years) |

| Early-stage solid-state batteries threatening long-term demand | -1.2% | Global, with pilot programs in Japan, North America | Long term (≥ 4 years) |

| Emerging PFAS-related restrictions on fluorinated binder additives | -0.7% | Europe (ECHA restrictions), potential spillover to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PP and PE Resin Supply Volatility and Price Spikes

Polypropylene and polyethylene prices spiked 18% in early 2024 after Middle-East naphtha outages, squeezing margins because resin forms 92% of separator cost. Regional plants without petrochemical integration remain exposed despite long-term supply contracts.

Early-Stage Solid-State Batteries Threatening Long-Term Demand

QuantumScape’s planned 20 GWh ceramic-electrolyte line could trim polyolefin demand in premium segments after 2028, though costs remain USD 400–600 kWh versus USD 156 for conventional packs.[2]QuantumScape, “QSE-5 Technical Brief,” quantumscape.com Separator makers hedge by investing in ceramic-electrolyte coatings to serve both architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Separator Type: Ceramic Coatings Redefine Safety Economics

Wet-process polyolefin retained 55.90% revenue in 2025, underscoring its cost leadership within the lithium-ion battery separator market. Ceramic-coated films are on track for a 20.30% CAGR, helped by inline coating that trims the cost premium to USD 0.12 m². Wet-process separators post higher ionic conductivity, complementing fast-charge 800-V car platforms, while dry-process variants serve cylindrical cells needing tensile strength.

Demand for coated solutions is spreading from premium to mid-tier EVs as UL 1973 and IEC 62619 standards stress thermal-shutdown metrics. Producers with both wet and coated lines can flex output to meet diverging price-and-safety needs, a strategy that helps preserve market balance as coated adoption accelerates after 2027.

By Material: Non-Woven Substrates Challenge Polyolefin Dominance

Polypropylene held a 43.20% share in 2025, thanks to thermal stability up to 165 °C, while polyethylene underpins the shutdown function because it melts at 135 °C. Non-woven substrates, rising at 18.10% a year, post porosity above 70%, enhancing electrolyte uptake and enabling thinner films that raise pack energy density.

Electrospinning throughput lags extrusion, keeping cost high, yet niche demand for 12 µm separators in performance EVs is drawing early orders. Multi-layer PP/PE/PP stacks are mainstream in prismatic cells, combining robustness and thermal fuse action, a format that should keep polyolefin above 60% share through 2031.

By Thickness: Safety Margins Drive Thicker Films

The 16-20 µm range captured 44.70% of the lithium-ion battery separator market size in 2025 as it balanced cost and mechanical integrity. The 21-25 µm band is climbing at 17.30% because thicker gauges accommodate ceramic coatings and mitigate puncture risk in large cells.

Average separator consumption is set to rise from 1.8 m² kWh-¹ in 2024 to 2.0 m² kWh-¹ by 2028, amplifying volume demand beyond EV unit growth. Thinner <15 µm films are receding to consumer electronics, where safety margins are less stringent.

By Battery Form Factor: Prismatic Cells Reshape Specifications

Pouch cells commanded 49.00% share in 2025 on design flexibility, yet prismatic cells are forecasting a brisk 18.70% CAGR because cell-to-pack systems cut inactive mass and lift volumetric density. Cylindrical cells gain renewed attention via Tesla’s 4680, increasing the tensile strength needs for separators.

Regional diversity is emerging: China leans prismatic, Europe and North America still favor pouch, and Tesla’s global cylinder adoption drives hybrid demand. Separator vendors must tailor tensile, compression, and puncture metrics to each form-factor specification to retain qualification.

By Coating Technology: Inline Processes Capture Cost-Conscious Buyers

Uncoated polyolefin represented 59.60% revenue in 2025 as mass-market EVs remain price sensitive. Inline ceramic coating, however, is expanding at 20.60% per year and is predicted to overtake offline coating by 2027. Integrated lines lower capex 25–30% and ensure uniform slurry distribution, helping coated cost converge toward USD 0.11 m².

Offline multi-coat lines persist where dual alumina-zirconia or polymer-ceramic layers are specified. Functional-polymer coatings using PVDF face EU PFAS proposals, accelerating the shift toward fluorine-free polyimide blends.

Geography Analysis

Asia-Pacific generated 54.50% of 2025 revenue, led by China’s 70% share of global separator capacity and South Korea’s ceramic-coating know-how. Growth is moderating as domestic EV uptake plateaus and export markets insert local-content clauses that erode China’s freight advantage. Japan maintains a niche in multilayer coatings but struggles with cost.

North America is projected to post an 17.60% CAGR, the fastest worldwide. Section 45X credits pay USD 0.40 m², effectively neutralizing higher labor and power costs, while gigafactory announcements exceed 450 GWh for 2025–2028. Asahi Kasei’s CAD 1.4 billion Ontario plant, slated for 700 million m², anchors regional build-out and pairs with Honda’s U.S. and Canadian cell lines. Europe is catching up on carbon-footprint compliance. SK IE Technology expanded its Poland and Hungary plants to 3.34 billion m² capacity powered by renewables, meeting the EU’s 2027 emission threshold. Market premiums of 10–15% over Asian film are offset by avoided tariffs and compliance value. South America and the Middle East-Africa remain import-dependent but may attract plants once regional EV production crests 200,000 units by 2027.

Mordor Intelligence provides coverage of the lithium-ion battery separator market for electric vehicle application across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China and France incorporating local coverage and market participation, as required.

Competitive Landscape

The five largest suppliers controlled more than 50% of global capacity in 2024, signaling moderate concentration within the lithium-ion battery separator market. Japanese and South Korean firms defend margins with ceramic-coating patents and inline processes, while Chinese producers leverage resin integration and scale to undercut on price. White-space remains in North America and Europe, where separator output trails cell demand by roughly 4-to-1.

Technology differentiation is moving quickly. SK IE Technology’s inline alumina process trims capex by a quarter and has won orders from three of the top ten cell manufacturers. Asahi Kasei commands a 15% premium in prismatic applications thanks to its PP/PE/PP multilayer IP. New entrants armed with electrospun non-wovens promise higher porosity but must solve throughput limits before challenging incumbents.

Safety standards such as UL 1973 and IEC 62619 tighten puncture and shutdown thresholds, erecting barriers to entry for suppliers without coating tools or multilayer know-how. Incumbents continue licensing and joint-venture deals to secure tax credits, carbon compliance, and proximity to gigafactories.

Leaders of Lithium-ion Battery Separator Market for Electric Vehicle Application

-

Semcorp

-

Asahi Kasei (Celgard/Hipore)

-

SK IE Technology

-

Toray Industries

-

Entek International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Sumitomo Chemical plans to restructure its PERVIO lithium-ion battery separator business by March 2026. The company will halt production at its Ohe Works in Niihama, Ehime Prefecture, Japan. Instead, it will consolidate PERVIO® manufacturing and related functions at its subsidiary, SSLM Co., Ltd. in Daegu, South Korea, which offers greater capacity and productivity.

- September 2025: I Squared Capital has struck a deal to take a majority stake in ENTEK (Entek Technology Holdings) for approximately USD 800 million. This substantial investment aims to bolster ENTEK's expansion efforts, notably funding a massive battery separator gigafactory in Terre Haute, Indiana.

- April 2025: SK ie Technology Co., has kicked off deliveries of separator film for battery cells to LG Energy Solution in North America. The company revealed that the amounts supplied in 2025 and 2026 will be enough to manufacture batteries for around 300,000 electric vehicles.

- April 2024: Asahi Kasei has revealed plans to build an integrated facility in Ontario, Canada. This plant will focus on producing and coating the base film for Hipore™, a wet-process lithium-ion battery (LIB) separator. Asahi Kasei has entered into a foundational agreement with Honda Motor Co., Ltd. (Honda) concerning this facility, and both companies are exploring the possibility of a joint investment.

Scope of Report on Lithium-ion Battery Separator Market for Electric Vehicle Application

A lithium-ion battery separator for electric vehicle (EV) applications is a critical component that significantly influences the performance, safety, and longevity of the battery. This separator is a thin, porous membrane placed between the anode and cathode of the lithium-ion battery, preventing direct contact while allowing lithium ions to pass through during charging and discharging cycles. Typically made from materials such as polyethylene (PE), polypropylene (PP), or a combination of both (PP/PE/PP trilayer), these separators are engineered to withstand high temperatures, mechanical stress, and chemical interactions within the battery.

The global lithium-ion battery separator market for electric vehicle applications is segmented by separator type, material, thickness, form factor, coating technology, and geography. By separator type, the market is segmented into wet-process, dry-process, and ceramic-coated separators. By material, the market is segmented into polypropylene (PP), polyethylene (PE), multilayer, and non-woven materials. By thickness, the market is segmented into up to 15 µm, 16–20 µm, 21–25 µm, and above 25 µm. By form factor, the market is segmented into pouch, cylindrical, and prismatic batteries. By coating technology, the market is segmented into inline coating, offline coating, functional polymer coating, and uncoated separators. The report also covers the market sizes and forecasts for the lithium-ion battery separator market for electric vehicle applications across major countries within each region. For each segment, market sizing and forecasts are provided on the basis of value (USD).

| Wet-Process Polyolefin |

| Dry-Process Polyolefin |

| Ceramic-Coated |

| Polypropylene (PP) |

| Polyethylene (PE) |

| Multilayer PP/PE/PP |

| Non-woven and Others |

| Up to 15 µm |

| 16 to 20 µm |

| 21 to 25 µm |

| Above 25 µm |

| Pouch Cells |

| Cylindrical Cells |

| Prismatic Cells |

| In-line Ceramic Coating |

| Offline Ceramic Coating |

| Functional Polymer Coatings |

| Uncoated Polyolefin |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Separator Type | Wet-Process Polyolefin | |

| Dry-Process Polyolefin | ||

| Ceramic-Coated | ||

| By Material | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Multilayer PP/PE/PP | ||

| Non-woven and Others | ||

| By Thickness | Up to 15 µm | |

| 16 to 20 µm | ||

| 21 to 25 µm | ||

| Above 25 µm | ||

| By Battery Form Factor | Pouch Cells | |

| Cylindrical Cells | ||

| Prismatic Cells | ||

| By Coating Technology | In-line Ceramic Coating | |

| Offline Ceramic Coating | ||

| Functional Polymer Coatings | ||

| Uncoated Polyolefin | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lithium-ion battery separator market for electric vehicles in 2026?

The market stands at USD 5.67 billion in 2026 and is forecast to reach USD 10.74 billion by 2031.

What is driving rapid growth in separator demand?

Rising EV sales, gigafactory build-outs, and the shift to higher-voltage chemistries that need safer separators are key drivers.

Which separator type is growing the fastest?

Ceramic-coated films are expanding at a 20.30% CAGR thanks to superior thermal-shutdown performance.

Why is North America the fastest-growing region?

Section 45X production credits lower cost hurdles for local plants, and over 450 GWh of new cell capacity is slated for 2025–2028.

How do solid-state batteries affect separator demand?

Solid-state technology could erode premium-segment demand after 2028, yet high costs mean polyolefin separators remain mainstream through 2030.

Which companies dominate current separator supply?

Asahi Kasei, SK IE Technology, Semcorp, Toray Industries, and Entek International collectively hold about 60% of capacity.

Page last updated on: