Immunoassays Market Size and Share

Market Overview

| Study Period | 2021 - 2030 |

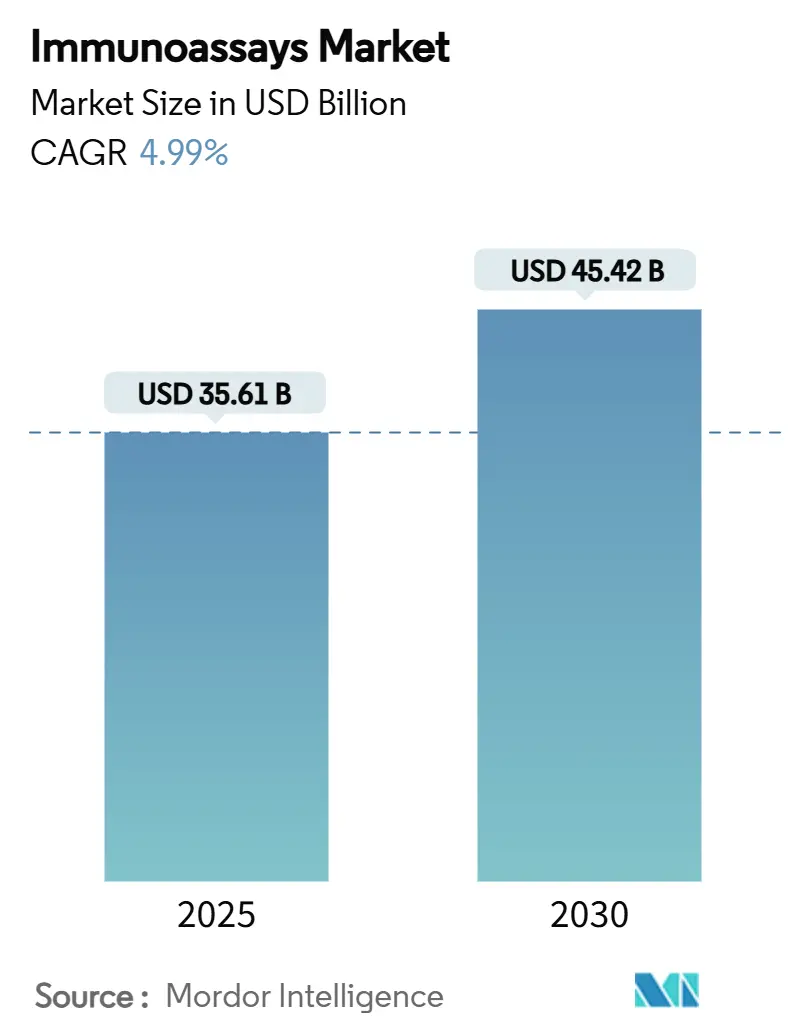

| Market Size (2025) | USD 35.61 Billion |

| Market Size (2030) | USD 45.42 Billion |

| Growth Rate (2025 - 2030) | 4.99% CAGR |

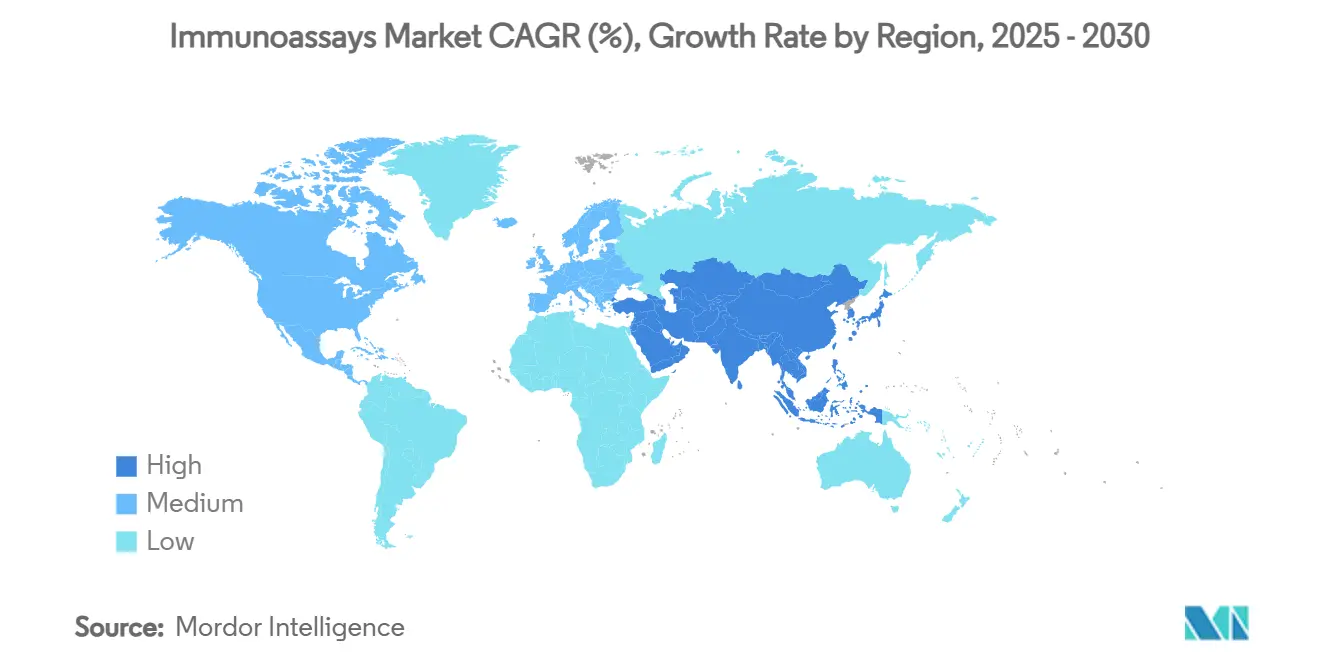

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Immunoassays Market Analysis by Mordor Intelligence

The immunoassays market is valued at USD 35.61 billion in 2025 and is projected to reach USD 45.42 billion by 2030, advancing at a 4.99% CAGR. The forward trajectory reflects a mature yet steadily expanding space, underpinned by accelerating demand for oncology biomarkers, artificial-intelligence-enabled platforms, and real-time bioprocess monitoring. AI-enhanced devices now push immunoassay detection limits down to femtomolar ranges, as seen in Rice University’s flow-cytometry instrument that delivers laboratory-grade accuracy in community clinics. Market growth also benefits from chemiluminescence immunoassay (CLIA) uptake in therapeutic drug monitoring and from heightened infectious-disease surveillance programs across emerging economies. Meanwhile, consolidation among diagnostics majors and venture funding in niche innovators intensify competitive dynamics, even as cross-reactivity issues, high capital costs, and stringent multi-region regulations temper adoption.

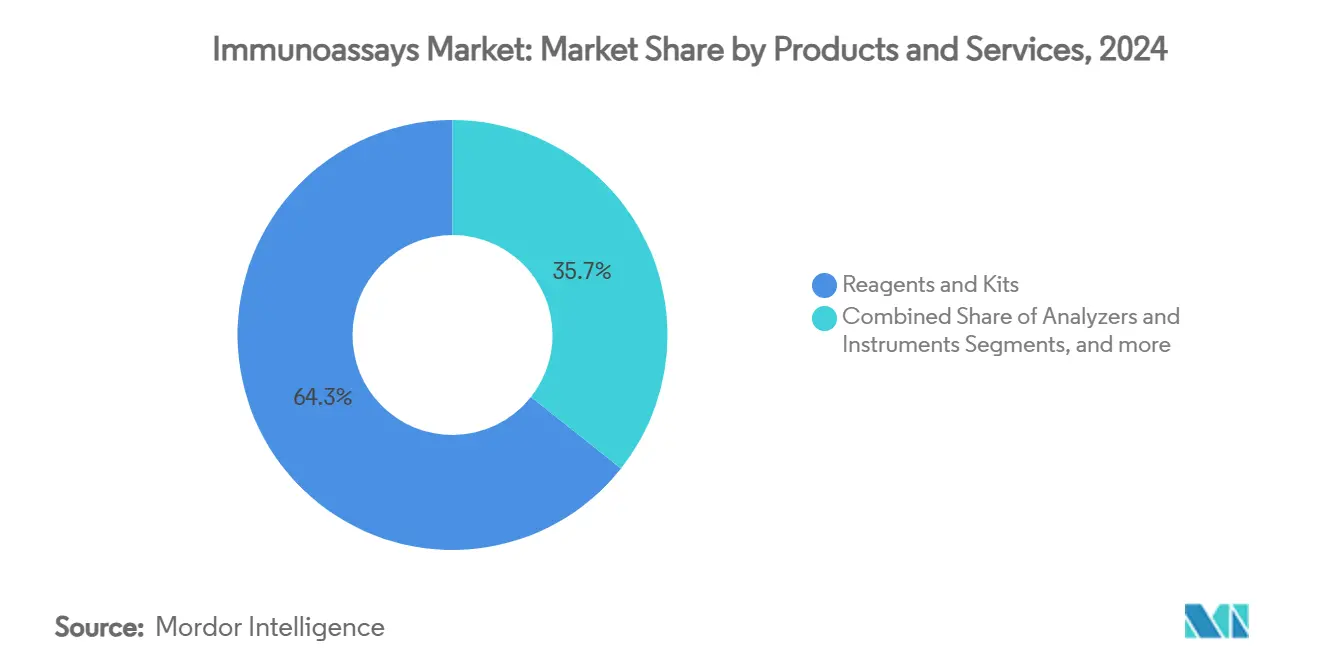

- By products & services, reagents and kits held 64.34% revenue share of the immunoassays market in 2024, while analyzers and instruments are forecast to grow at a 5.34% CAGR through 2030.

- By technology, ELISA accounted for 55.34% of revenue in 2024; CLIA is poised to expand at a 5.41% CAGR to 2030.

- By application, infectious diseases led with 35.45% revenue share in 2024; oncology is the fastest-growing segment at a 5.51% CAGR through 2030.

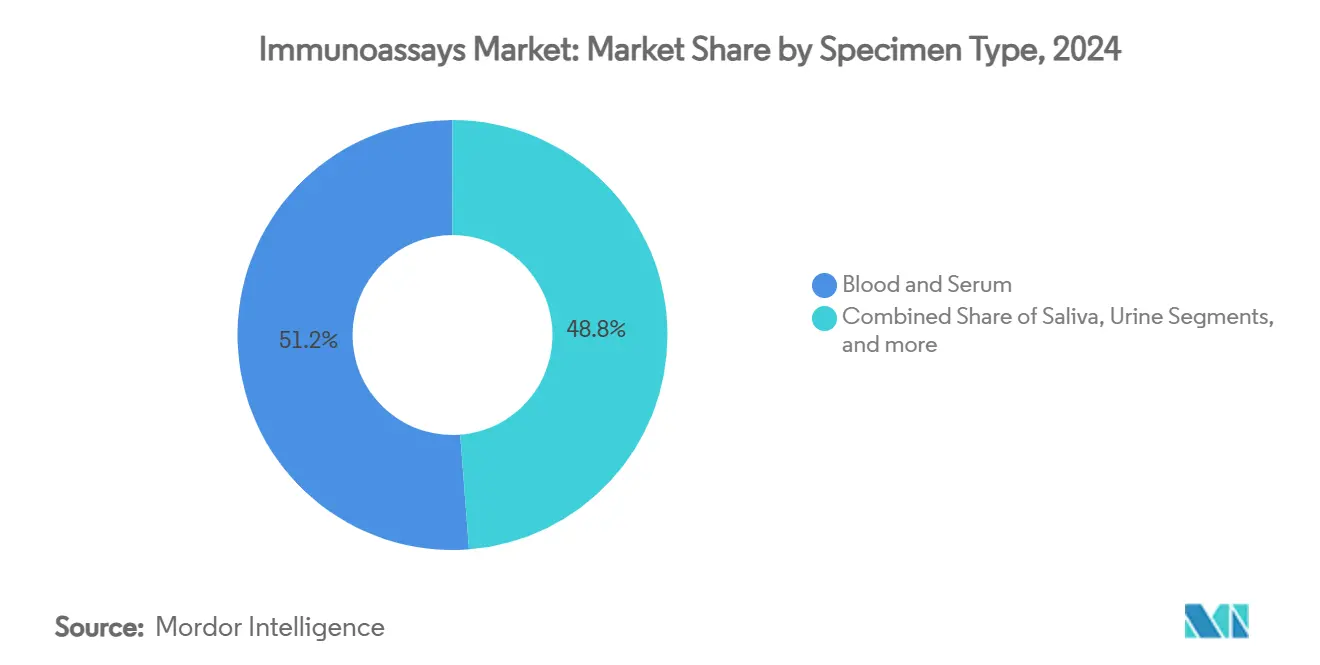

- By specimen type, blood and serum dominated with 51.23% share in 2024; saliva testing will post the strongest growth at a 5.23% CAGR.

- By end user, hospitals captured 36.45% of the immunoassays market size in 2024; point-of-care and home-care settings will grow at a 5.53% CAGR to 2030.

- By geography, North America commanded 41.12% revenue in 2024; Asia-Pacific registers the highest regional CAGR at 5.54% through 2030.

Global Immunoassays Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & infectious diseases | +1.2% | Global; highest impact in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Rapid technological advances in high-throughput analyzers | +0.8% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Expansion of point-of-care/home-based rapid tests | +0.9% | Global; early adoption in North America | Short term (≤ 2 years) |

| Government-funded global surveillance & immunization programs | +0.6% | Global; focus on developing markets | Long term (≥ 4 years) |

| AI/ML-enabled ultra-low-analyte detection platforms | +0.7% | North America & EU; spill-over to APAC | Medium term (2-4 years) |

| PAT immunoassays for real-time bioprocess monitoring | +0.4% | North America & EU; expanding to China | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising Prevalence of Chronic & Infectious Diseases

Escalating cancer, cardiovascular, and infectious-disease burdens continue to redefine testing volumes worldwide. Multi-parameter panels that combine circulating tumor DNA with traditional protein biomarkers are improving early diagnosis and therapy selection, as evidenced by research identifying CA724, ferritin, and β2-microglobulin as thoracic cancer indicators. Cardiometabolic care has embraced advanced lipoprotein(a) assays, with Roche’s Tina-quant test delivering the first molar-based Lp(a) measurement cleared by the FDA. Communicable-disease surveillance, supported by WHO quality-assurance networks, further accelerates reagent consumption and instrument installations.[1]World Health Organization, “Laboratory Network Strengthening for Disease Surveillance,” who.int

Rapid Technological Advances in High-Throughput Analyzers

Automation and machine learning now underpin daily laboratory workflows. The Mayo Clinic’s AI model for kidney-stone spectral analysis cut per-sample review time while preserving accuracy. CLIA platforms from Revvity deliver 60 tests per hour with 48-minute turnaround and monoclonal antibody specificity, a combination essential for precision oncology and endocrinology. Microfluidic biosensors integrate fluid control and optical detection on a single chip, shrinking assay footprints and permitting true walk-away operation.

Expansion of Point-of-Care/Home-Based Rapid Tests

Demand for decentralized diagnostics is reshaping procurement budgets and reimbursement structures. Global POC revenues are slated to eclipse USD 35 billion by 2027, buoyed by diabetes and respiratory-virus screening needs. LOCA-PRAM algorithms now reduce false positives in handheld readers, while optofluidic immunoassays deliver COVID-19 antibody results from 1 µL blood in 40 minutes. Shelf-stable bioluminescence reagents achieve 2.1 pg/mL IL-6 detection, removing cold-chain dependencies for field deployment.

Government-Funded Global Surveillance & Immunization Programs

National and multilateral initiatives continue to build diagnostic capacity. The US CDC’s Global Health Protection division has trained local laboratorians in more than 80 countries. India’s serosurveillance projects guide immunization policy by pinpointing immunity gaps, while Australia’s National Serosurveillance Program has generated 26 peer-reviewed outputs that inform vaccine schedules. WHO’s integrated VPD framework, first deployed in Costa Rica, illustrates how harmonized testing can streamline pathogen tracking.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-jurisdictional regulatory approvals | −0.7% | Global; highest complexity in EU and US | Long term (≥ 4 years) |

| High capital cost of multiplex & automated systems | −0.5% | Global; greater impact in emerging markets | Medium term (2-4 years) |

| Cross-reactivity & matrix interferences in novel assays | −0.3% | Global; focus on complex biological matrices | Short term (≤ 2 years) |

| Supply-chain bottlenecks for high-purity antibodies | −0.4% | Global; concentration in specialized suppliers | Medium term (2-4 years) |

Source: Mordor Intelligence

Stringent Multi-Jurisdictional Regulatory Approvals

Developers face divergent evidence expectations across the FDA, European IVDR, and multiple Asian frameworks, inflating timelines and budgets. Companion diagnostics add layers of inter-agency coordination, while guidance for AI-enabled or multiplex assays remains fragmented. Lack of global harmonization compels parallel validation studies and onsite audits, draining resources from R&D pipelines and product launches.

High Capital Cost of Multiplex & Automated Systems

Instrument price tags, ongoing reagent contracts, and facility retrofits deter smaller labs. Protein A resin and automated analyzers command premium pricing that pushes total cost of ownership beyond many public-sector budgets. Contract manufacturing can offset scale constraints but introduces supply-chain dependencies and potential quality lapses.

Segment Analysis

By Products & Services: Reagents Sustain Market Foundation

Reagents and kits generated USD 22.9 billion in revenue in 2024, translating into the single largest slice of the immunoassays market and providing predictable, recurring income streams for suppliers. Volume growth comes from routine infectious-disease panels, chronic-disease monitoring, and expanding global surveillance programs that require validated, lot-consistent consumables. Reagent interoperability across multiple analyzer platforms is increasingly important, prompting manufacturers to invest in universal chemistries and CE-marked bulk packs that support lean-lab initiatives.

Analyzers and instruments, the fastest-expanding category at a 5.34% CAGR, reflect laboratory moves toward full automation and high-throughput operations. AI-enabled scheduling modules now optimize run order and maintenance cycles, easing technician shortages. Meanwhile, middleware connects immunoassay data with LIS and hospital EHRs, driving integrated clinical decision support. As a result, the immunoassays market size for instruments is projected to rise from USD 7.6 billion in 2025 to USD 9.9 billion in 2030.

Note: Segment shares of all individual segments available upon report purchase

By Technology: ELISA Dominance Faces CLIA Challenge

ELISA occupied 55.34% revenue share in 2024, anchored by standardized protocols, low consumable cost, and decades of accumulated performance evidence. Academic and community laboratories alike continue to rely on ELISA for cytokine panels, endocrine markers, and autoimmune screening, sustaining strong base demand. Yet sensitivity ceilings and relatively long incubation times limit ELISA’s suitability for emerging ultra-low-analyte applications.

Chemiluminescence immunoassays, growing at a 5.41% CAGR, offer higher analytical sensitivity and wider dynamic range, making them the method of choice for therapeutic drug monitoring and tumor-marker quantification. Multiplex microarray platforms add throughput by simultaneously detecting dozens of analytes, a capability now indispensable in translational oncology programs. Consequently, the immunoassays market share commanded by CLIA is forecast to climb toward 30% by decade-end, even as ELISA retains a sizeable installed base.

By Application: Infectious Diseases Lead, Oncology Surges

Infectious-disease testing represented 35.45% of 2024 revenues, supported by surveillance mandates, global vaccine programs, and continuing SARS-CoV-2 variant tracking. WHO-aligned procurement schemes ensure reagent standardization and funding continuity, making this application a durable volume driver. Simultaneously, new multiplex respiratory panels incorporate antigen and antibody targets, extending menu breadth per cartridge and boosting ASPs.

Oncology assays, meanwhile, are projected to register 5.51% CAGR through 2030, the fastest among applications. Liquid-biopsy panels that combine ctDNA and protein markers are gaining reimbursement endorsements, and personalized immunotherapy regimens depend on longitudinal monitoring of checkpoint inhibitor biomarkers. Consequently, the immunoassays market size for oncology is set to rise from USD 6.9 billion in 2025 to USD 9.1 billion by 2030, supported by big-pharma companion-diagnostic partnerships.

By Specimen Type: Blood Dominance, Saliva Innovation

Blood and serum samples comprised 51.23% of 2024 revenues thanks to clinical familiarity, broad analyte coverage, and robust reference ranges. Venipuncture remains the gold standard for high-throughput central-lab workflows, and dried-blood-spot cards now extend cold-chain-free logistics to resource-limited settings.

Saliva testing, advancing at a 5.23% CAGR, benefits from painless collection suited to pediatrics and telehealth. Validation studies have confirmed salivary cortisol, HIV antibodies, and SARS-CoV-2 antigens as reliable targets, with microfluidic devices requiring under 200 µL of sample for multiplex panels. As acceptance grows, the immunoassays market size for saliva-based tests is expected to double between 2025 and 2030, capturing hospital, home, and employer-screening demand.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Lead, POC Transforms Care

Hospitals accounted for 36.45% of revenue in 2024, leveraging integrated LIS systems, reimbursement coverage, and multidisciplinary care pathways that demand rapid diagnostics. Bundle-payment models and clinical-decision-support integration push hospitals toward analyzers that combine immunoassays with chemistry and hematology on a single track, improving throughput and reagent utilization.

Point-of-care and home settings will see 5.53% CAGR through 2030, propelled by patient preference, remote-care policy incentives, and miniaturized analyzer launches. Wearable patches that incorporate microfluidic immunoassay cartridges for cytokine monitoring are entering early clinical trials, signaling future expansion beyond episodic tests. Under these trends, the immunoassays market share of POC users is positioned to exceed 15% by 2030, up from 11% in 2024.

Geography Analysis

North America maintained 41.12% revenue share in 2024, supported by strong reimbursement frameworks, NIH funding, and rapid FDA review pathways for breakthrough diagnostics. Recent clearances such as Roche’s B-cell lymphoma assay illustrate the region’s innovation cadence. Collaboration between Biogen, Beckman Coulter, and Fujirebio on Alzheimer’s markers further demonstrates the value placed on immunoassay-based companion diagnostics[2]Beckman Coulter, “Partnership Advances Alzheimer’s Disease Biomarkers,” beckmancoulter.com. The United States continues to replace aging analyzers with fully automated lines integrating sample prep, while Canada emphasizes universal access and Mexico channels public-sector tenders toward high-sensitivity infectious-disease platforms.

Asia-Pacific is the fastest-growing region at 5.54% CAGR through 2030. China’s Made-in-China 2025 plan accelerates diagnostic self-sufficiency, with Chemclin’s automated systems moving from pilot to national rollout[3]Yicai Global, “Chemclin Diagnostics Unveils Fully Automated Immunodetection System,” yicaiglobal.com. India’s organized diagnostics sector is expanding beyond metropolitan hubs into tier-3 and tier-4 cities, aided by wellness packages and price transparency. Japan incentivizes regenerative-medicine and oncology companion tests via fast-track approval programs, while South Korea supports start-ups through tax credits and hospital test beds. Southeast Asian nations benefit from multilateral funding aimed at tuberculosis and dengue surveillance, creating first-time buyer opportunities for bench-top platforms.

Europe remains a major revenue contributor, although IVDR transition challenges extend launch timelines. Germany and France anchor centralized testing demand, the United Kingdom prioritizes early cancer detection via NHS funding, and Spain expands point-of-care programs in primary-care clinics. Meanwhile, the Middle East and Africa, though smaller today, show double-digit test-volume growth thanks to Gulf state hospital construction and African CDC procurement initiatives. South America leverages Brazil’s unified health-service upgrades to expand neonatal and prenatal screening, while Argentina pushes for local reagent production amid import restrictions.

Competitive Landscape

The immunoassays market is moderately consolidated, with the top five vendors controlling just under 60% of revenue. Abbott, Roche, Siemens Healthineers, bioMérieux, and Thermo Fisher Scientific maintain broad assay menus, global distribution, and aggressive R&D pipelines. Thermo Fisher’s USD 3.1 billion acquisition of Olink fortifies its proteomics depth and underscores a multiyear USD 40-50 billion acquisition budget that targets adjacent technologies. Roche’s USD 295 million LumiraDx purchase and bioMérieux’s EUR 111 million SpinChip deal highlight the scramble for point-of-care capabilities that deliver lab-quality performance in decentralized settings.

Emerging players exploit white spaces in AI-driven detection, microfluidic cartridge design, and PAT sensors. Norwegian start-up SpinChip offers 10-minute whole-blood panels, while US-based pattern-recognition firms supply middleware that harmonizes assay data across brands. Intellectual-property portfolios around antibody engineering and chemiluminescent substrates act as defensive moats, with top vendors filing hundreds of global patents annually. Cross-sector collaborations between pharmaceutical companies and diagnostics firms accelerate companion-diagnostic development, as exclusivity rights tether drug programs to specific test platforms. Regional manufacturers in China and India leverage cost efficiencies and local-government procurement preferences to undercut imports, gradually climbing the value chain toward high-sensitivity assays.

Sustainability and supply security grow in strategic importance. Firms are vertically integrating to secure high-purity monoclonal antibodies and critical chemistries, reducing exposure to pandemic-level disruptions. Digital-service adjacencies—cloud analytics, remote calibration, cybersecurity—differentiate offers in tender evaluations. Market entrants must therefore balance capital intensity, regulatory complexity, and IP barriers against the lucrative recurring-reagents model and expanding application fields.

Immunoassays Industry Leaders

-

Abbott Laboratories Inc.

-

Becton Dickinson and Company

-

Danaher Corporation

-

Hologic Inc.

-

Qiagen NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: bioMérieux completed acquisition of SpinChip Diagnostics for EUR 111 million, adding a 10-minute whole-blood immunoassay platform for acute-care settings.

- January 2025: Roche obtained FDA 510(k) clearance for Tina-quant Lipoprotein(a) Gen.2 Molarity assay, the first US test measuring Lp(a) in molar units.

- January 2025: Beckman Coulter launched RUO blood-based biomarker assays for p-Tau217, GFAP, NfL, and APOE ε4 in Alzheimer’s research.

- July 2024: Thermo Fisher Scientific closed its USD 3.1 billion acquisition of Olink Holding AB, adding Proximity Extension Assay technology covering over 5,300 protein biomarkers.

Global Immunoassays Market Report Scope

As per the scope of this report, an immunoassay is a test that relies on biochemistry to measure the presence and concentration of an analyte. The analyte can be large proteins, antibodies that a person has produced as a result of an infection, or small molecules. Immunoassays are highly sensitive and specific. Their high specificity results from the use of antibodies and purified antigens as reagents. The Immunoassays Market is Segmented by Type (Radioimmunoassay, Enzyme Immunoassays, Fluoroimmnoassay, Chemiluminescence Immunoassay, Others), Application (Disease Diagnosis, Therapeutic Drug Monitoring, Drug Discovery, Clinical Chemistry, Hematology, Others), End-User (Hospitals, Pharma & Biotech Companies, Clinical Laboratories Others) and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Product & Service | Reagents & Kits | ||

| Analyzers & Instruments | |||

| Software & Services | |||

| By Technology | Enzyme-Linked Immunosorbent Assay (ELISA) | ||

| Chemiluminescence Immunoassay (CLIA) | |||

| Fluorescence Immunoassay (FIA) | |||

| Radioimmunoassay (RIA) | |||

| Lateral Flow Immunoassay (LFIA) | |||

| Multiplex & Microarray Immunoassays | |||

| Others (Western Blot, Immuno-PCR) | |||

| By Application | Infectious Diseases | ||

| Oncology | |||

| Cardiology | |||

| Endocrinology | |||

| Autoimmune Disorders | |||

| Therapeutic Drug Monitoring | |||

| Drug Discovery & Development | |||

| Others | |||

| By Specimen Type | Blood & Serum | ||

| Saliva | |||

| Urine | |||

| Other Body Fluids | |||

| By End User | Hospitals | ||

| Clinical Laboratories | |||

| Pharmaceutical & Biotechnology Companies | |||

| Academic & Research Institutes | |||

| Point-of-Care / Home-Care Settings | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Reagents & Kits |

| Analyzers & Instruments |

| Software & Services |

| Enzyme-Linked Immunosorbent Assay (ELISA) |

| Chemiluminescence Immunoassay (CLIA) |

| Fluorescence Immunoassay (FIA) |

| Radioimmunoassay (RIA) |

| Lateral Flow Immunoassay (LFIA) |

| Multiplex & Microarray Immunoassays |

| Others (Western Blot, Immuno-PCR) |

| Infectious Diseases |

| Oncology |

| Cardiology |

| Endocrinology |

| Autoimmune Disorders |

| Therapeutic Drug Monitoring |

| Drug Discovery & Development |

| Others |

| Blood & Serum |

| Saliva |

| Urine |

| Other Body Fluids |

| Hospitals |

| Clinical Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Point-of-Care / Home-Care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and expected growth rate of the immunoassays market?

The immunoassays market stands at USD 35.61 billion in 2025 and is projected to reach USD 45.42 billion by 2030, advancing at a 4.99% CAGR.

Which product category contributes the largest share of revenue?

Reagents and kits account for 64.34% of 2024 revenue, reflecting recurring demand across routine and specialty testing.

Why are chemiluminescence immunoassays attracting more laboratories?

CLIA platforms deliver higher analytical sensitivity and faster turnaround than traditional ELISA, supporting applications such as therapeutic-drug monitoring and oncology biomarker detection.

Which region is expected to register the fastest growth through 2030?

Asia-Pacific will post the highest regional CAGR at 5.54%, driven by healthcare infrastructure upgrades in China, India, and Japan.

What are the main restraints facing market participants today?

Stringent multi-jurisdictional regulatory approvals, high capital costs for automated systems, cross-reactivity challenges, and antibody-supply bottlenecks slow product rollout and adoption.

How will point-of-care testing influence future demand?

Decentralized and home-based rapid tests are projected to grow at a 5.53% CAGR, expanding market reach and fueling demand for compact, AI-enabled analyzers.

Page last updated on: July 4, 2025