Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 4.79 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Antibiotics Market Analysis by Mordor Intelligence

The feed antibiotics market size is projected to grow from USD 3.85 billion in 2025 to USD 3.99 billion in 2026, reaching USD 4.79 billion by 2031, with a CAGR of 3.7% during the 2026-2031 period. Growth reflects a balance between disease management in livestock systems and policy measures limiting non-therapeutic antibiotic use. Regulatory changes in the United States, such as duration-of-use labeling for certain in-feed approvals, influence therapeutic programs and inventory while ensuring access to treatments under veterinary supervision. Tetracyclines remain critical due to efficacy and cost-effectiveness, with 2024 United States sales data identifying this class as holding the largest share of medically important antimicrobials sold for food-producing animals. Rising producer interest in antibiotic-free labeling has heightened the importance of oversight, residue testing, and vaccination. Strategic adjustments in 2026 include portfolio realignments by major suppliers, such as divestments aimed at reallocating resources toward biologics and precision nutrition.

Key Report Takeaways

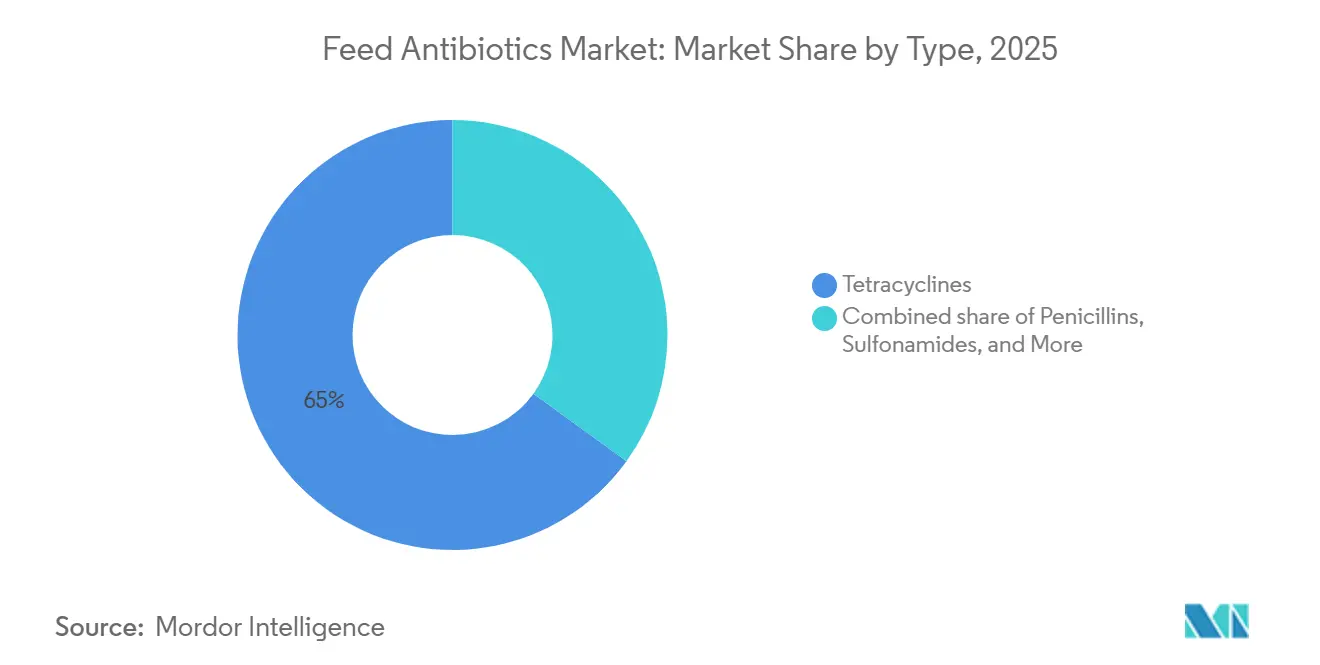

- By type, tetracyclines accounted for the largest 65.0% of the global feed antibiotics market share in 2025. Meanwhile, the market size for macrolides is projected to grow at the fastest CAGR of 3.8% from 2026 to 2031.

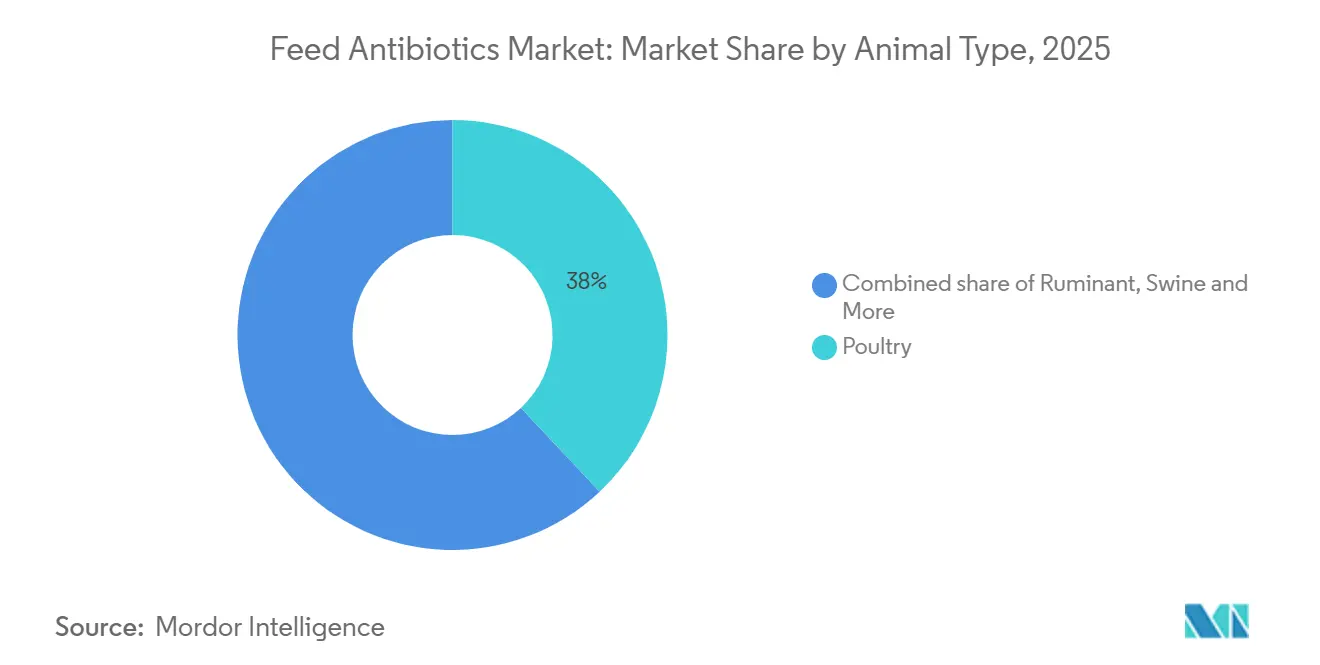

- By animal type, poultry accounted for the largest share of 38.0% in the global feed antibiotics market in 2025, and the poultry market size is projected to achieve the fastest CAGR of 4.0% from 2026 to 2031.

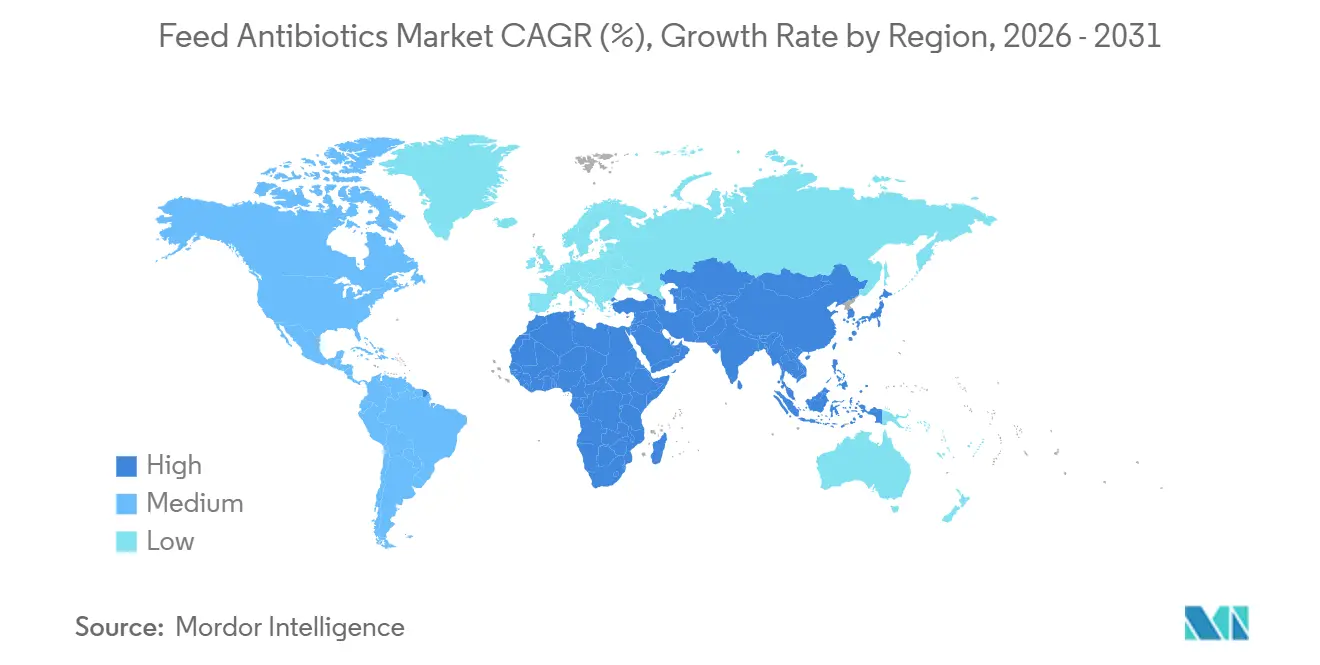

- By geography, Asia-Pacific accounted for the largest 35.0% of the global feed antibiotics market share in 2025, and the Asia-Pacific market size is projected to record the fastest CAGR of 4.2% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Antibiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry and swine production increases medicated feed demand | +1.2% | Global, with acute pressure in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Compound feed growth supports antibiotic volumes | +0.9% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥4 years) |

| Cost-effective tetracyclines remain widely used | +0.7% | Global, particularly cost-sensitive markets in South America and Asia-Pacific | Long term (≥4 years) |

| Veterinary oversight improves compliance | +0.5% | North America and European Union, with gradual adoption in ASEAN and Mercosur | Medium term (2-4 years) |

| Standardized protocols enhance treatment efficiency | +0.3% | North America, European Union, Australia, with pilot programs in Chile and South Africa | Short term (≤ 2 years) |

| Label expansions sustain product use | +0.2% | North America and European Union, expanding to Brazil and China for swine respiratory disease complexes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry and Swine Production Increases Medicated Feed Demand

Disease dynamics in dense production environments necessitate targeted therapeutic use under veterinary supervision, guided by surveillance data and prescribed durations of use [1]Source: United States Food and Drug Administration, “Fact Sheet, Veterinary Feed Directive Final Rule and Next Steps,” U.S. Food and Drug Administration, fda.gov. Positivity rates for porcine reproductive and respiratory syndrome increased in 2025, indicating ongoing respiratory challenges that heighten the need for treatment during swine finishing and nursery phases [2]Source: Swine Health Information Center, “October 2025 SHIC eNewsletter,” Swine Health Information Center, swinehealth.org . In large broiler complexes and integrated pork operations, standardized protocols for diagnosis, dosing, and withdrawal periods are integral to production risk management. Producers are adapting by integrating biosecurity measures, vaccination, and time-limited therapies, monitored through mill-veterinarian systems and audited process controls.

Compound Feed Growth Supports Antibiotic Volumes

The growth of compound feed production in key livestock economies continues to support the use of feed-based antibiotic delivery for approved therapeutic purposes. According to the Alltech Global Feed Survey, global compound feed production exceeded 1.39 billion metric tons in 2024, indicating consistent growth in livestock production systems. In China, compound feed production surpassed 315 million metric tons in 2024, as reported by the China Feed Industry Association. This growth has been driven by government efforts to modernize feed mills and enhance quality control measures, ensuring accurate dosing and improved traceability in medicated feed.

Cost-Effective Tetracyclines Remain Widely Used

Sales and usage data from 2025 identify tetracyclines as the largest class of medically important antimicrobials for food-producing animals in the United States, highlighting their broad-spectrum efficacy and value, which continue to influence purchasing decisions and treatment protocols. Global analyses emphasize their wide availability, pharmacokinetic familiarity, and established withdrawal schedules, maintaining tetracyclines as a preferred first-line option in various therapeutic contexts. Policy updates in Asia have restricted non-therapeutic applications while preserving access for veterinary prescriptions, ensuring therapeutic use in cases where animal health and welfare are at risk.

Veterinary Oversight Improves Compliance

The increasing role of veterinary oversight in livestock production systems is improving compliance with antibiotic usage protocols, ensuring controlled and traceable in-feed applications. As per the United States Food and Drug Administration, medically important antibiotics for food-producing animals in the United States are administered under veterinary authorization in accordance with Veterinary Feed Directive (VFD) regulations. This demonstrates the effective implementation of antibiotic stewardship policies. According to the United States Food and Drug Administration, antimicrobial sales for livestock in the United States declined by approximately 2% between 2022 and 2023, indicating enhanced compliance and a reduction in non-therapeutic usage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phase-Out of Growth Promoters Limits Usage | -1.8% | European Union, North America, China, with progressive adoption in Southeast Asia and Latin America | Long term (≥4 years) |

| Demand for Antibiotic-Free Products Shifts Preferences | -1.1% | North America and European Union core, expanding to Japan, South Korea, and urban Brazil | Medium term (2-4 years) |

| Stricter Residue Rules Increase Costs | -0.7% | European Union, Australia, New Zealand, with phased rollout in ASEAN and Gulf Cooperation Council markets | Medium term (2-4 years) |

| Active Pharmaceutical Ingredient (API) Supply Volatility Affects Availability | -0.5% | Global, with acute exposure in markets reliant on Chinese bulk APIs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Phase-Out of Growth Promoters Limits Usage

Regulatory authorities in key markets have implemented measures to prohibit the non-therapeutic use of antibiotics for growth promotion, while allowing their use for treatment, control, and prevention under specific conditions. In China, the Ministry of Agriculture and Rural Affairs has established policies banning antibiotic growth promoters and mandating veterinary oversight for therapeutic applications. Similarly, in North America, prescription requirements and Veterinary Feed Directive regulations have reclassified antibiotics as a supervised resource rather than a routine input, with clear guidelines on their duration and indications.

Demand for Antibiotic-Free Products Shifts Preferences

The growing demand for antibiotic-free meat and eggs is significantly influencing purchasing patterns, with a shift toward alternative feed solutions driven by regulatory actions and changing consumer preferences. This reflects the ongoing transition to antibiotic-free production systems, as producers seek to meet consumer expectations for healthier and more sustainable products. Additionally, the European Commission reports that European countries have adopted stringent antimicrobial resistance (AMR) reduction targets, further promoting the reduction of routine antibiotic use and encouraging the adoption of innovative feed strategies to maintain livestock health.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tetracyclines Lead on Cost-Efficiency, While Macrolides Capture Therapeutic Value

Tetracyclines accounted for the largest 65.0% of the global feed antibiotics market share in 2025, while the global feed antibiotics market size for macrolides is projected to achieve the fastest segment growth with a 3.8% CAGR from 2026 to 2031, highlighting their distinct roles in managing respiratory and enteric disease complexes. In the United States, tetracyclines held the largest share of medically important antimicrobial sales for food-producing animals in 2024, emphasizing their role in cost-effective therapy with established withdrawal schedules. Pleuromutilins continue to gain traction in swine, driven by established products and ongoing label expansions that enhance their clinical utility for mycoplasma and respiratory pathogens [3]Source: ECO Animal Health Group plc, “Annual Report 2024,” ECO Animal Health Group plc, ecoanimalhealth.com.

Ionophores, which are not classified as medically important for human medicine, remain widely utilized in poultry coccidiosis programs and support feed-conversion control strategies under specific regulatory frameworks. Within the broader therapeutic landscape, aminoglycosides, sulfonamides, and penicillins address specific indications based on pathogen profiles and farm-stage requirements, with veterinarians tailoring treatments to disease pressures and documented susceptibilities. Looking ahead, the feed antibiotics market is projected to see increased use of macrolides in targeted applications, where label convenience and defined durations align with oversight and labor constraints.

By Animal Type: Poultry Market Growth Driven by Broiler Density and Metaphylaxis Practices

Poultry held the largest 38.0% of the global feed antibiotics market share in 2025, and the global feed antibiotics animal market size for poultry is projected to grow fastest at a 4.0% CAGR from 2026 to 2031, driven by disease-management needs in high-capacity broiler systems and the interplay of vaccines and targeted therapeutics. Integrators deploy vaccination and ionophore programs at scale and maintain access to in-feed antibiotics for indicated conditions under veterinary oversight, which balances label-claim aspirations with animal health imperatives. In swine, persistent respiratory disease pressure has kept therapeutic options important, with positivity rates for key viral pathogens reinforcing the need for clearly defined metaphylaxis plans managed by mill and veterinarian teams.

Within the feed antibiotics market, veterinarians tailor class selection and dosing based on species, production stage, and pathogen profile, which leads to distinct usage patterns across poultry, swine, ruminants, and aquaculture. Retail and export programs that stipulate negative-antibiotic claims have increased traceability obligations for integrators, which in turn shape how mill-veterinarian teams schedule and document therapeutic courses. This environment favors clear labels, sustained-release options, and validated withdrawal periods that can withstand audit in channels with elevated verification expectations.

Geography Analysis

Asia-Pacific accounted for the largest 35.0% of the feed antibiotics market share in 2025, and the feed antibiotics market size for Asia-Pacific is projected to grow at the fastest CAGR of 4.2% from 2026 to 2031. This growth reflects the region's significant poultry and swine production, ongoing modernization of feed mills, and veterinary oversight for therapeutic applications. According to the United States Department of Agriculture, poultry production is projected to reach approximately 15.8 million metric tons in 2026, with growth driven by white-broiler production. White-broiler systems account for nearly 70% of total output, supported by vertically integrated operations that dominate industrial poultry production.

North America is driven by formal oversight frameworks and disease management needs, particularly in cattle and swine. The 2026 duration-of-use initiative enhances label clarity for selected in-feed approvals, reducing historical ambiguity around continuous use and aiding planning for feedlots and large integrators. In 2024, United States sales data indicated a significant share held by tetracyclines among medically important antibiotics, reflecting their widespread utility and cost-effectiveness for respiratory and enteric conditions. Swine health surveillance in 2025 recorded elevated numbers of cases of porcine reproductive and respiratory syndrome, underscoring the ongoing demand for supervised therapy at finishing and nursery sites.

Europe is shaped by the region's long-standing prohibition on antibiotic growth promoters and its emphasis on veterinary oversight for therapeutic use. National regulators collaborate with international standards bodies to enhance medicine governance, promoting improved stewardship and residue control in feed-based therapies. Producers in Europe continue to invest in vaccination, enzymes, and phytogenics while maintaining access to in-feed antibiotics for labeled indications under veterinary supervision. As supply chains expand antibiotic-free offerings, processors and retailers demand more rigorous compliance evidence, increasing documentation requirements for feed mills and farms.

Competitive Landscape

The feed antibiotics market is moderately concentrated by the top five players, including Zoetis Inc., Elanco Animal Health Incorporated, Phibro Animal Health Corporation, Huvepharma EOOD, and ECO Animal Health Group plc in 2025. Leading global players integrate feed antibiotics with vaccines, parasiticides, and diagnostics to offer comprehensive solutions to integrators and large-scale farms. Their strategies for 2026 emphasize compliance with labeling regulations, clarity on duration-of-use guidelines, and risk management for residue testing in premium markets. Competitive priorities include ensuring supply chain reliability for key active ingredients, enhancing feed mill service models, and providing documentation that meets buyer audit requirements.

Elanco Animal Health Incorporated introduced new initiatives in anti-infectives, including pleuromutilin derivatives targeting swine respiratory disease and integrated diagnostics partnerships aimed at reducing the time required for treatment decisions. Merck & Co., Inc. progressed with companion-animal product approvals, highlighting ongoing investment in medically significant drug classes. The 2025 approvals indicate regulatory progress that strengthens broader veterinary portfolios. These developments illustrate a strategic balance between maintaining core antibiotic offerings and expanding into new categories to support customers in meeting antibiotic-free commitments.

Specialist companies are strengthening their market positions through species-specific focus and targeted innovation. ECO Animal Health Group plc. has reported consistent growth in pleuromutilins and continues to expand its vaccine portfolio for poultry and swine. Emerging modalities, such as bacteriophage and enzyme-based products, are gaining traction as complementary solutions to vaccination and biosecurity measures in markets with stricter antibiotic usage constraints. Partnerships introducing endolysin tools to poultry and livestock producers in North America exemplify this trend.

Feed Antibiotics Industry Leaders

Zoetis Inc.

Elanco Animal Health Incorporated

Phibro Animal Health Corporation

Huvepharma EOOD

ECO Animal Health Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ECO Animal Health Group plc, a global animal health company with a portfolio of veterinary products and a developing proprietary R&D pipeline, has provided an update on its commercial launch strategy for ECOVAXXIN MS, its poultry vaccine targeting Mycoplasma synoviae, within the European Union (EU).

- May 2025: Merck & Co., Inc., referred to as MSD Animal Health outside the United States and Canada, has received approval from the United States Food and Drug Administration for MOMETAMAX SINGL, a single-dose otic suspension developed for the treatment of otitis externa in dogs.

- October 2024: Phibro Animal Health Corporation has completed the acquisition of Zoetis Inc. The acquisition encompasses manufacturing facilities located in the United States, Italy, and China. This development enhances Phibro Animal Health Corporation's global presence in the feed antibiotics market.

Global Feed Antibiotics Market Report Scope

Feed antibiotics are antimicrobial compounds added to livestock feed to prevent bacterial infections, improve animal health, and enhance feed efficiency. Their use is increasingly regulated due to concerns about antimicrobial resistance and food safety. The feed antibiotics market report is segmented by type (tetracyclines, penicillin, sulfonamides, macrolides, aminoglycosides, cephalosporins, and other types), by animal type (ruminant, poultry, swine, aquaculture, and other animal types), and by geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). The market size and growth forecasts are provided in terms of value (USD).

By Type

| Tetracyclines |

| Penicillins |

| Sulfonamides |

| Macrolides |

| Aminoglycosides |

| Cephalosporins |

| Other types |

By Animal Type

| Ruminant |

| Poultry |

| Swine |

| Aquaculture |

| Other animal types |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Spain |

| United Kingdom | |

| Germany | |

| France | |

| Russia | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Thailand | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Tetracyclines | |

| Penicillins | ||

| Sulfonamides | ||

| Macrolides | ||

| Aminoglycosides | ||

| Cephalosporins | ||

| Other types | ||

| By Animal Type | Ruminant | |

| Poultry | ||

| Swine | ||

| Aquaculture | ||

| Other animal types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Spain | |

| United Kingdom | ||

| Germany | ||

| France | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Thailand | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the feed antibiotics market size in 2026 and the projected value by 2031?

The feed antibiotics market size is USD 3.99 billion in 2026 and is projected to reach USD 4.79 billion by 2031 at a 3.7% CAGR over 2026-2031.

Which segment holds the largest share of the feed antibiotics market in 2025?

Tetracyclines hold the largest share in 2025 at 65%, driven by broad-spectrum efficacy and cost efficiency.

Which animal type is expanding fastest in the feed antibiotics market to 2031?

Poultry is the fastest, with a 4.0% CAGR through 2031, as integrators balance vaccination, ionophore programs, and targeted therapeutic use.

Which region leads the feed antibiotics market and which grows fastest to 2031?

Asia-Pacific leads with 35% share in 2025 and is also the fastest-growing region with a 4.2% CAGR from 2026-2031..

How are regulations shaping demand in the feed antibiotics market in 2026?

Duration-of-use labeling and formal veterinary oversight are tightening, which reduces non-therapeutic use and focuses demand on time-bound, label-compliant therapies.

What product trends are most influential in the feed antibiotics market now?

Macrolide and pleuromutilin label updates that enable convenient dosing, alongside continued reliance on tetracyclines for cost-effective therapy, are most influential.

Page last updated on: