Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.77 Billion |

| Market Size (2031) | USD 9.67 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

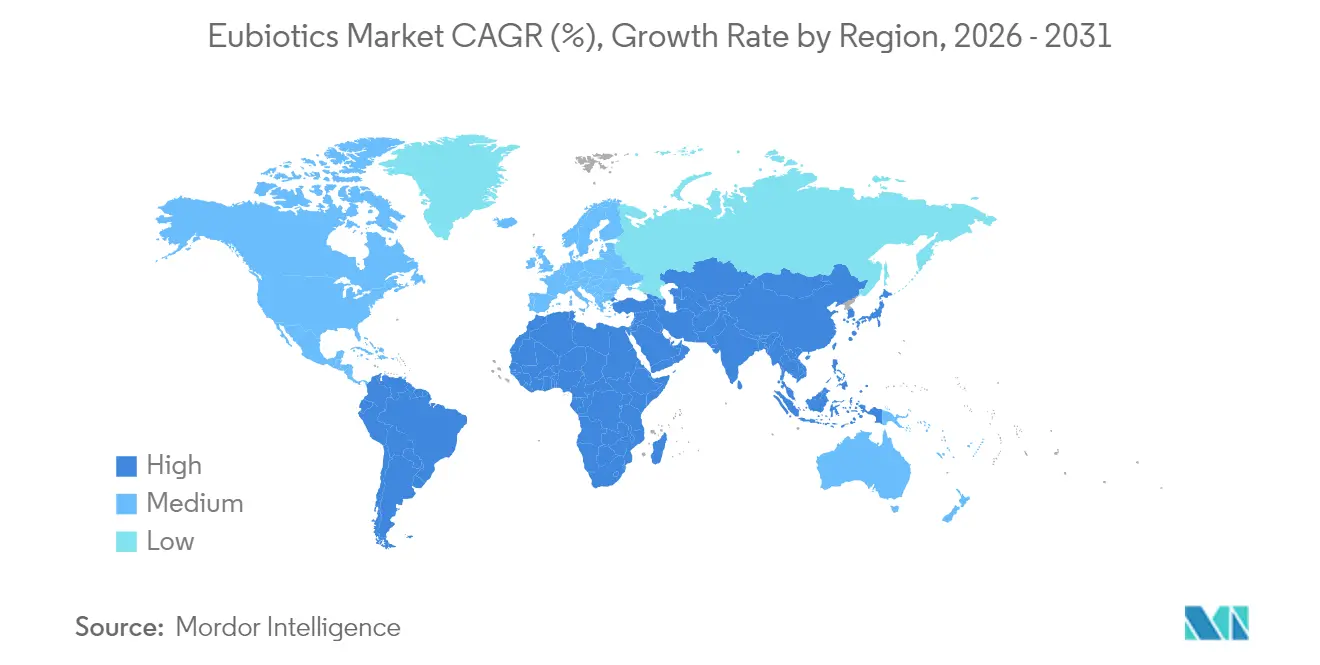

| Fastest Growing Market | Middle East |

| Largest Market | Europe |

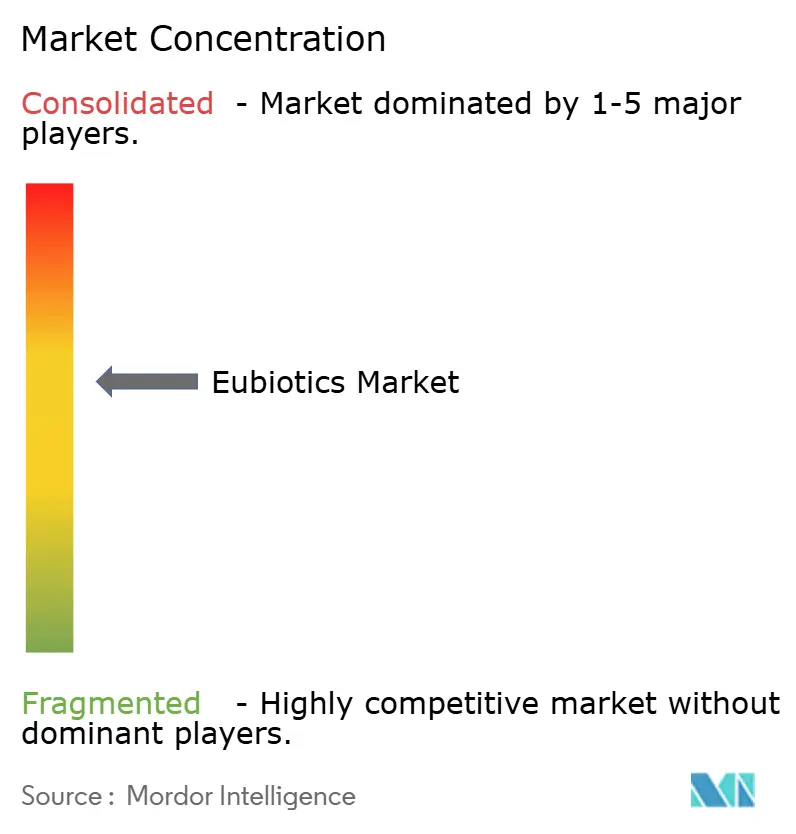

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eubiotics Market Analysis by Mordor Intelligence

The Eubiotics Market size was valued at USD 6.30 billion in 2025 and estimated to grow from USD 6.77 billion in 2026 to reach USD 9.67 billion by 2031, at a CAGR of 7.42% during the forecast period (2026-2031). Rising restrictions on antibiotic growth promoters, steady gains in aquaculture output, and precision nutrition technologies are accelerating the adoption of probiotics, organic acids, prebiotics, and phytogenic additives across all livestock segments. Large retailers that mandate antibiotic-free supply chains reinforce demand momentum, while digital livestock systems show measurable feed-cost savings and lower nitrogen excretion when coupled with targeted eubiotic programs. Supply-chain resilience and circular-economy sourcing strengthen competitive positioning, and regulatory convergence in North America and Asia-Pacific reduces approval complexity for globally harmonized product launches. Moderate market concentration leaves room for regional specialists who can tailor formulations to local raw-material bases and environmental pressures. Across all trends, the eubiotics market continues to pivot from broad-spectrum antibiotics toward sustainable gut-health solutions that deliver quantifiable farm-level returns.

Key Report Takeaways

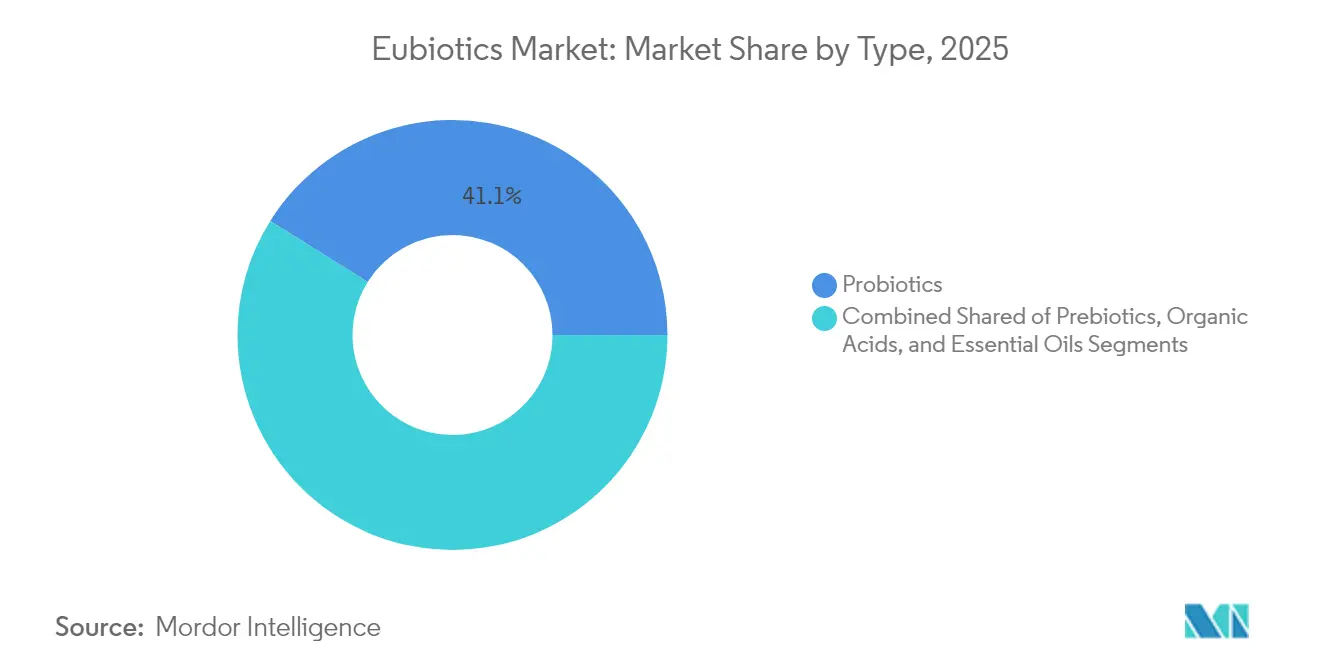

- By type, probiotics led with 41.10% of the eubiotics market share in 2025; essential oils are forecast to expand at a 9.64% CAGR through 2031.

- By animal type, poultry held 34.10% of the eubiotics market share in 2025, while aquaculture is projected to grow at an 8.44% CAGR by 2031.

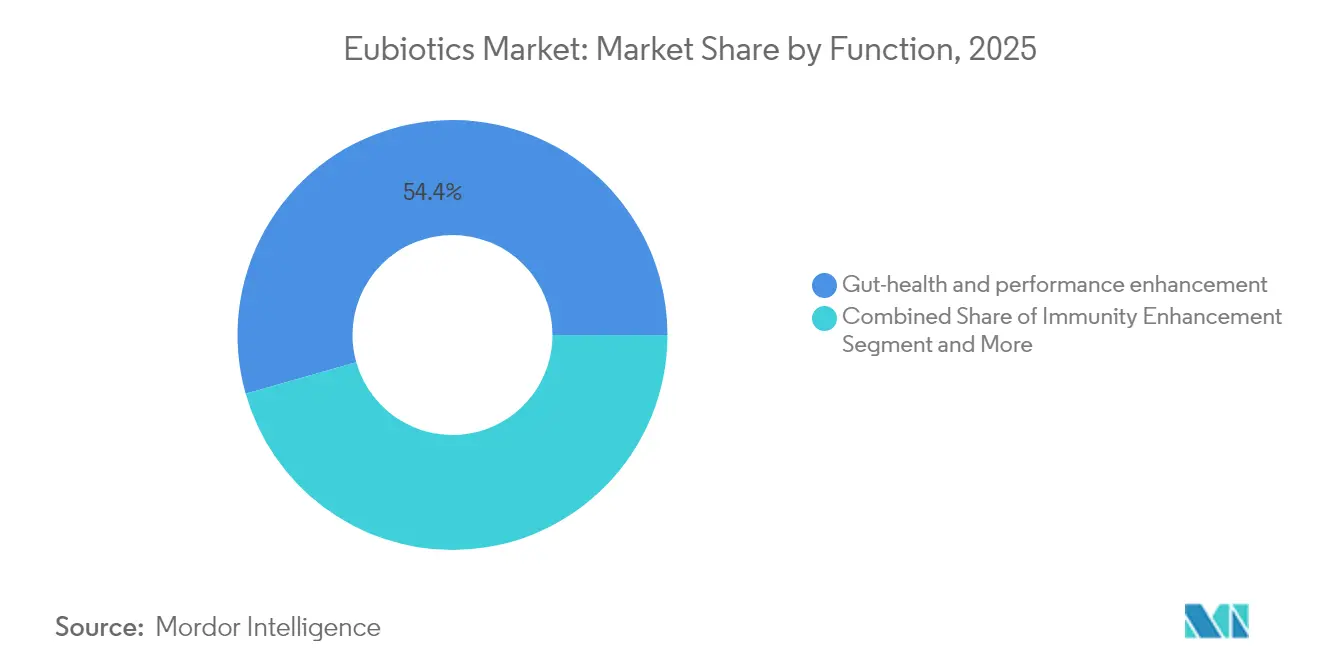

- By function, gut-health and performance applications accounted for 54.40% of 2025 revenue, and feed-efficiency improvement is expected to advance at an 8.33% CAGR through 2031.

- By form, dry powders led with 62.20% of 2025 revenue; liquid formulations register the strongest 8.45% CAGR over the forecast period.

- By geography, Europe accounted for 34.40% of the eubiotics market size in 2025; the Middle East is projected to advance at a 7.78% CAGR over the forecast period.

- The top five suppliers controlled 43.8% of 2024 revenue, with BASF SE leading at 11.5% market share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Eubiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory restrictions on antibiotic growth promoters | +2.1% | Global, led by EU and North America | Medium term (2-4 years) |

| Rising consumer demand for antibiotic-free animal products | +1.8% | North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Expansion of aquaculture production globally | +1.4% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Technological advances in precision nutrition and delivery systems | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Growing awareness of gut-health importance in animal performance | +0.9% | Global, faster adoption in intensive farming regions | Medium term (2-4 years) |

| Increasing focus on sustainable and circular-economy practices | +0.7% | Europe, North America, progressive Asian markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory restrictions on antibiotic growth promoters

The formal phase-out of antibiotic growth promoters across major livestock regions has set an irreversible shift toward eubiotics. Regulation (EC) No 1831/2003 created a rigorous safety dossier process that many other jurisdictions now mirror, resulting in a clearer, more standardized approval path that rewards suppliers with robust clinical data packages.[1]European Food Safety Authority, “Guidance on the Assessment of the Safety of Feed Additives,” efsa.europa.eu As the U.S. FDA’s Innovative FEED Act introduces similar streamlining, multinational producers can coordinate dossier submissions, shorten time-to-market, and deploy harmonized formulations that meet common safety thresholds.

Rising consumer demand for antibiotic-free animal products

Demand for antibiotic-free meat and dairy has moved from niche to mainstream. Large grocery chains impose supplier policies that eliminate antibiotic use, pushing producers toward eubiotics despite higher additive costs. Premium shelf prices offset these costs and create a compelling economic case, particularly in urban Europe, North America, and advanced Asian economies where consumers link antibiotic stewardship to health and food safety.[2]U.S. Food and Drug Administration, “Innovative FEED Act Summary,” fda.gov

Expansion of aquaculture production globally

The rapid expansion of aquaculture is a major driver of eubiotic adoption, as fish and shrimp farms increasingly seek sustainable alternatives to antibiotics for disease prevention and gut health management. Global aquaculture capacity is rising sharply, with Gulf projects such as the Cargill-NEOM venture targeting 600,000 metric-ton output by 2030. Water-stable probiotic and phytogenic formulations reduce pathogen load and improve feed conversion in recirculating aquaculture systems, aligning with environmental discharge regulations and investor sustainability mandates.

Technological advances in precision nutrition and delivery systems

Sensors embedded in feeders adjust eubiotic dosage in real-time, aligning probiotic and phytogenic inclusion rates with daily animal growth curves for higher feed-conversion efficiency. Precision micro-encapsulation protects heat-sensitive essential oils and probiotic spores, ensuring greater than or equal to 90% survival through pelleting temperatures and gastric transit. On-farm trials report 25% lower crude protein intake and 40% less nitrogen excretion when precision nutrition platforms deliver targeted eubiotic blends, supporting stricter environmental-compliance limits. Species-specific algorithms in recirculating aquaculture systems dose water-stable probiotics that cut Vibrio counts by 30% in shrimp grow-out ponds, improving survival rates and reducing antibiotic use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs and complex regulatory approval processes | -1.5% | Global, particularly stringent in EU and North America | Medium term (2-4 years) |

| Supply-chain volatility and raw-material sourcing challenges | -1.1% | Global, acute in developing markets | Short term (≤ 2 years) |

| Limited awareness and technical expertise in developing markets | -0.8% | Africa, parts of Asia-Pacific, South America | Medium term (2-4 years) |

| Inconsistent efficacy results and lack of standardization | -0.6% | Global, more pronounced in emerging applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High costs and complex regulatory approval processes

High costs and complex regulatory approval processes slow product launches and raise entry barriers for smaller suppliers. Submitting a full EFSA safety dossier can cost several million EUR and extend timelines to 3–4 years, tying up capital that could otherwise fund Research and Development. Diverging post-Brexit rules mean companies must now prepare separate submissions for the EU and the UK, duplicating documentation and laboratory studies. These burdens tilt competitive advantage toward multinationals with dedicated regulatory teams and can discourage investment in novel mechanisms of action that lack a clear pathway to fast approval.

Supply-chain volatility and raw-material sourcing challenges

Supply-chain volatility and raw-material sourcing challenges create unpredictable input costs that erode producer margins. Climate-driven swings in Peru’s anchovy fishery, a key omega-3 source, triggered a 35% price spike after the 2023 El Nino shutdown and exposed the fragility of marine-based ingredient supply lines. Logistical disruptions—ranging from container shortages to Red Sea routing detours—add further uncertainty and delay the arrival of critical botanical oils and organic-acid intermediates. Producers increasingly hedge risk through vertical integration, local cultivation of herb crops, and partnerships with single-cell protein ventures that decouple formulations from volatile commodity streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Probiotics Lead While Essential Oils Accelerate

Probiotics held a 41.10% 2025 revenue share, underpinning the largest slice of the eubiotics market. Their dominance stems from extensive clinical validation, reliable performance across climates, and accommodating regulatory precedents that expedite approvals. The segment’s Bacillus spores tolerate pelleting temperatures, ensuring delivery past the proventriculus and into the ileum, where competitive exclusion exerts its effect. Synbiotic formulations that blend probiotics with fructooligosaccharide prebiotics show feed-conversion improvements of 3-4%, validating complementary mechanisms.

Essential oils record the fastest 9.64% CAGR to 2031. Consumer preference for plant-based antimicrobials and the compounds’ multilayered actions on gut microbes drive uptake. Micro-encapsulation of thymol, carvacrol, and cinnamaldehyde stabilizes volatile compounds, and inclusion rates as low as 100 ppm deliver measurable pathogen suppression. Organic acids and prebiotics retain niche roles in acidification and substrate provisioning, while multi-modal blends aim to capture synergistic benefits. Collective progress in formulation science cements the eubiotics market as the central platform for gut-health innovation.

By Animal Type: Poultry Dominance Challenged by Aquaculture Growth

Poultry contributed 34.10% of 2025 revenue, reflecting decades of antibiotic-alternative programs in broilers and layers. Inclusion rates average 500 g per metric ton of feed, and cumulative lifetime feed-conversion gains deliver strong cost-benefit ratios. Aquaculture’s 8.44% forecast CAGR shifts relative growth toward marine and freshwater species. Shrimp, tilapia, and hybrid grouper trials indicate pathogen load reductions exceeding 30% when precise water-stable probiotics are dosed through automated feeders.

Swine operations integrate multi-strain probiotics post-weaning to curb enterotoxigenic Escherichia coli. Ruminant adoption lags due to complex rumen dynamics, yet propionibacterium blends that modulate volatile fatty acid ratios gain traction as methane-reduction tools. Companion-animal formulations segment adds a premium layer where pet-food marketers leverage the humanization trend to justify higher price points. Collectively, animal-specific optimization widens the eubiotics market size while allowing specialty suppliers to capture margin through proprietary strains.

By Function: Performance Applications Drive Market Evolution

Gut-health and performance applications represented 54.40% of 2025 revenue, underscoring the central role of digestive integrity in animal productivity. These products enhance villi height, improve nutrient absorption, and modulate inflammatory responses, delivering consistent weight-gain benefits under a range of farm conditions. Disease-prevention functions, while smaller in revenue share, hold regulatory importance in regions that cap antibiotic residue levels in meat exports. Feed-efficiency improvement posts an 8.33% CAGR, making it the fastest functional driver within the eubiotics market. Producers quantify feed-conversion improvements through daily-gain metrics, enabling direct cost-benefit validation for premium inclusions.

Immune-system enhancement gains prominence as veterinary teams recognize the gut–immune axis; specific yeast-cell-wall derivatives elevate immunoglobulin A levels in broilers. Stress-mitigation functions target stocking density and thermal stress challenges, particularly in tropical poultry houses where heat waves compromise gut barrier integrity. Integration of precision-feeding algorithms introduces dynamic dosing, ensuring functional additives support performance exactly when animals experience metabolic peaks. Collectively, these function-level trends reinforce the eubiotics market’s pivot from basic health insurance to production-economics optimization.

By Form: Liquid Applications Challenge Powder Dominance

Dry powders maintained 62.20% revenue in 2025, driven by long shelf life, low logistics cost, and compatibility with existing feed-mill augers. The eubiotics market nonetheless sees liquid formulations rising at an 8.45% CAGR, supported by stabilization chemistries that prevent microbial spoilage and sedimentation. Liquids are dosed accurately through automated spraying systems, reducing inclusion variability that can erode efficacy. Their water-soluble nature benefits nursery swine and calf milk replacers, where uniform dispersion is critical.

Encapsulated granules occupy a premium niche because lipid coatings trigger controlled release only after the gastric barrier, ensuring active ingredients reach the ileum or cecum. Paste and gel formulations cater to aquaculture and companion-animal segments that require water stability or palatability. Microencapsulation now blends dry-form stability with liquid-form bioavailability, offering hybrid solutions that straddle both benefits. Ultimately, form-factor innovation continues to differentiate suppliers and expands the eubiotics market by addressing specific operational constraints across livestock systems.

Geography Analysis

Europe’s 34.40% revenue share in 2025 stems from stringent feed-additive rules, high producer awareness, and established distribution infrastructure. Product developers benefit from proximity to fermentation inputs, veterinary universities, and contract research labs that speed proprietary-strain screening. The EU Organic Action Plan triggers incremental demand for certified eubiotics that complement organic livestock diets while addressing vitamin and amino-acid gaps. Regulatory divergence following Brexit introduces dual-registration costs but also niche opportunities for fast-track approvals under UK guidelines.

The Middle East delivers the fastest 7.78% CAGR, anchored by aquaculture megaprojects under Saudi Vision 2030. Gulf Cooperation Council countries invest in desert-climate aquafeed facilities that marry single-cell protein and eubiotics to close domestic protein gaps. Government feed-subsidy schemes reward local producers that integrate sustainable gut health solutions to minimize antibiotic residues and align with halal and green-label standards.

Asia-Pacific shows heterogeneous patterns. Advanced markets like Japan and South Korea emphasize value-added formulations and traceability, while China and India focus on cost-effective blends due to scale. Regulatory clearance remains slower in China, yet local production clusters in Shandong and Fujian provinces shorten supply chains. South American producers leverage abundant botanical raw materials to develop essential oil blends domestically, providing cost advantages in export-oriented beef and poultry sectors.

Competitive Landscape

The top five players command 43.8% of 2024 revenue, signifying moderate concentration that still allows regional innovators space to operate. BASF SE holds an 11.5% share through its broad BalanGut and monoglyceride lines that address gut-barrier integrity, while dsm-firmenich’s 10.3% stake faces restructuring as the company divests its Animal Nutrition and Health unit in 2025. This divestiture could catalyze share redistribution, particularly if private equity buyers integrate the asset into existing feed platforms.

Strategic differentiation centers on proprietary strain libraries, encapsulation patents, and digital integration services that model feed-converter responses in real-time. Evonik’s joint venture with Shandong Vland Biotech illustrates the importance of local manufacturing that lowers logistics costs and meets domestic content rules in China. Lesaffre’s acquisition of Biorigin boosts yeast-derived prebiotic capacity, ensuring a secure supply of mannan-oligosaccharides amid rising Brazilian demand.

Supply-chain resilience underpins competitive success. Companies vertically integrate fermentation input streams or partner with single-cell-protein ventures to hedge fishmeal shortages. Those investments not only protect margins but also resonate with sustainability commitments that retailers and investors track through scope-3 emissions dashboards. The outcome is a dynamic eubiotics market in which scale players must constantly innovate while agile entrants leverage focus and speed to capture niche growth.

Eubiotics Industry Leaders

BASF SE

dsm-firmenich

Novonesis

Cargill, Incorporated

ADM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Evonik has introduced Ecobiol, a Bacillus subtilis-based probiotic aimed at enhancing poultry gut health and feed efficiency in mainland China. The expansion aligns with the growing demand for sustainable, functional feed additives in livestock production.

- January 2025: Novus International and Resilient Biotics formed a partnership to develop a microbial feed solution that improves immune health and reduces respiratory issues in swine. The collaboration focuses on using microbiome-based approaches to enhance gut and respiratory health, supporting the production of antibiotic-free livestock.

- October 2024: Novus International and Ginkgo Bioworks established a partnership to develop feed additives that aim to enhance livestock health and productivity. The companies initially focused on developing enzymes with improved efficacy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the eubiotics market as the sale of feed-grade prebiotics, probiotics, organic acids, and essential oils purposely blended into compound feed or premixes to enhance gut microflora, immunity, and feed efficiency across poultry, swine, ruminant, aquaculture, and companion animal sectors. Products intended for direct-fed microbial supplements outside feed manufacturing or for human nutraceuticals are not included.

Scope exclusion: veterinary pharmaceuticals, antibiotic growth promoters, and single-acidifier additives sold outside balanced eubiotic blends are outside this study.

Segmentation Overview

- By Type

- Probiotics

- Lactobacilli

- Bifidobacteria

- Other Probiotics (Bacillus subtilis, Saccharomyces boulardii, etc.)

- Prebiotics

- Inulin

- Fructo-oligosaccharides

- Galacto-oligosaccharides

- Other Prebiotics (Mannan-oligosaccharides, beta-Glucans, etc.)

- Organic Acids

- Essential Oils (Phytogenics)

- Probiotics

- By Animal Type

- Ruminant

- Poultry

- Swine

- Aquaculture

- Other Animal Types (Companion Animals, Equines, etc.)

- By Form

- Dry (powder, granule)

- Liquid (solution, suspension, emulsion)

- By Function (Primary Objective)

- Gut-health and performance enhancement

- Immunity enhancement

- Pathogen control / disease mitigation

- Feed-efficiency improvement

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with nutritionists at feed mills, veterinary consultants, and regional distributors across Europe, Asia-Pacific, and Latin America. Discussions validated typical inclusion rates, recent price revisions, and early demand signals after new AGP restrictions, filling gaps left by desk work and sharpening assumptions.

Desk Research

We began with public datasets on livestock inventories and compound-feed output from sources such as FAO-STAT, USDA FAS, Eurostat, and the International Feed Industry Federation, complemented by regulatory notices from EFSA and the US FDA on antibiotic bans. Trade flow statistics from UN Comtrade and customs portals helped us size regional import dependence for key strains. Company filings, investor decks, and respected trade journals enriched price trends, while paid tools like D&B Hoovers and Questel supplied revenue splits and patent activity. This list is illustrative; many other open and subscription sources supported data checks and context building.

Market-Sizing & Forecasting

A top-down model converts official compound-feed tonnage by species into potential eubiotic demand using consensus penetration and dose benchmarks, which are then cross-checked with selective bottom-up supplier revenue roll-ups and channel checks. Key variables include: 1) national feed output, 2) average inclusion rate by eubiotic type, 3) antibiotic-ban enforcement timelines, 4) average selling price per kilogram, and 5) regional poultry and swine slaughter data that indicate adoption intensity. Forecasts apply multivariate regression blended with scenario analysis to project how feed volume growth, price pass-through, and regulatory pacing alter demand through 2030. Where supplier data fell short, gap regions were interpolated from adjacent markets with similar feed practices and adjusted after expert review.

Data Validation & Update Cycle

Model outputs pass a three-layer review: peer analyst, senior domain lead, and research quality cell before sign-off. Variances above preset thresholds trigger re-checks with sources or fresh expert calls. The report refreshes every twelve months, with interim updates when major events, for example, sudden ASF outbreaks, materially shift baseline assumptions.

Why Mordor's Eubiotics Baseline Commands Reliability

Published figures differ because analysts choose distinct product baskets, base years, and refresh cadences.

By anchoring our numbers to verified feed tonnage, real-world inclusion rates, and annual price audits, Mordor reduces estimation drift that can arise from straight CAGR roll-forwards or partial geographic coverage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.30 B (2025) | Mordor Intelligence | - |

| USD 5.85 B (2024) | Regional Consultancy A | Leaves out essential oils and organic acids; relies on uniform global CAGR without in-year updates |

| USD 4.92 B (2022) | Trade Journal B | Uses older base year and restricts scope to Europe and North America, omitting Asia-Pacific growth surge |

| USD 6.80 B (2024) | Global Consultancy C | Counts poultry probiotics only partially and extrapolates pricing from broad feed-additive averages |

The comparison shows that estimates swing when product scope narrows or data vintages lag. By blending timely field intelligence with transparent, repeatable calculations, Mordor Intelligence delivers a balanced baseline executives can trust for planning and investment decisions.

Key Questions Answered in the Report

What is the Eubiotics market size in 2026 and how fast is it growing?

The market stands at USD 6.77 billion in 2026 and is projected to expand at a 7.42% CAGR to reach USD 9.67 billion by 2031.

Which Eubiotic type commands the largest revenue share?

Probiotics lead the landscape with 41.10% of 2025 revenue, supported by extensive clinical validation and favorable regulatory precedents.

What are the fastest-growing product and animal segments?

Essential oils record the quickest 9.64% CAGR through 2031, while the aquaculture segment posts an 8.44% CAGR as global fish and shrimp production scales up.

What key factors fuel demand for eubiotics?

Regulatory bans on antibiotic growth promoters, consumer preference for clean-label meat and dairy, rapid aquaculture expansion, and precision-nutrition technologies collectively accelerate adoption.

Page last updated on: