Market Overview

| Study Period | 2020 - 2030 |

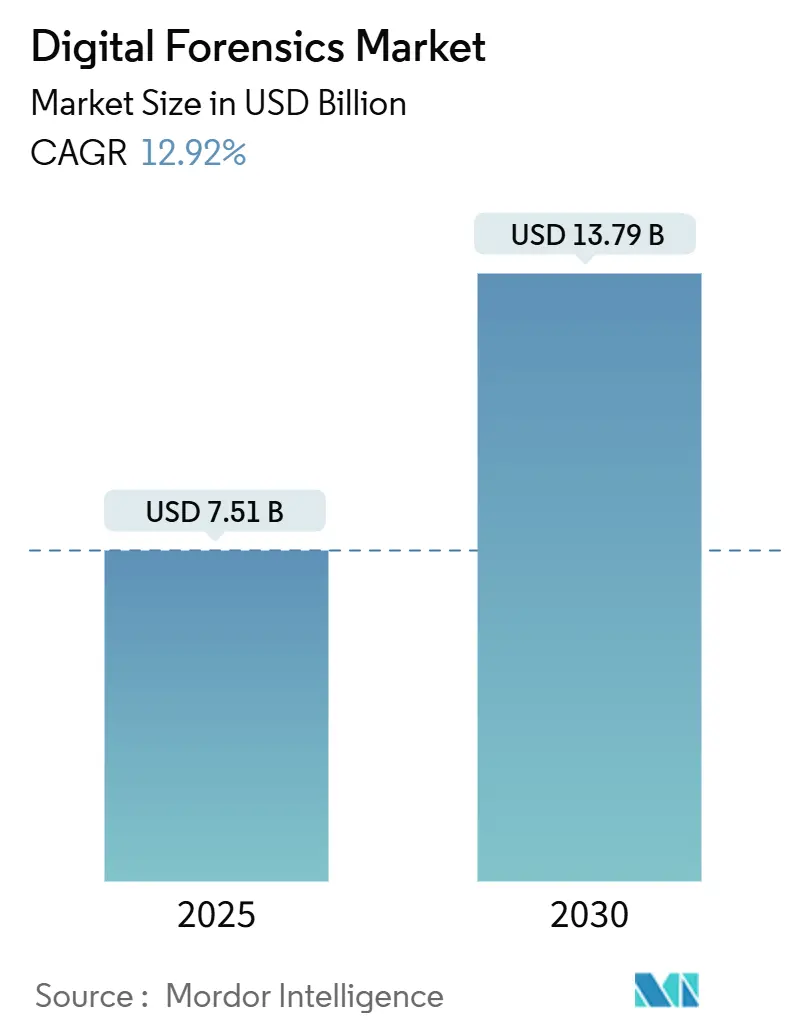

| Market Size (2025) | USD 7.51 Billion |

| Market Size (2030) | USD 13.79 Billion |

| Growth Rate (2025 - 2030) | 12.92% CAGR |

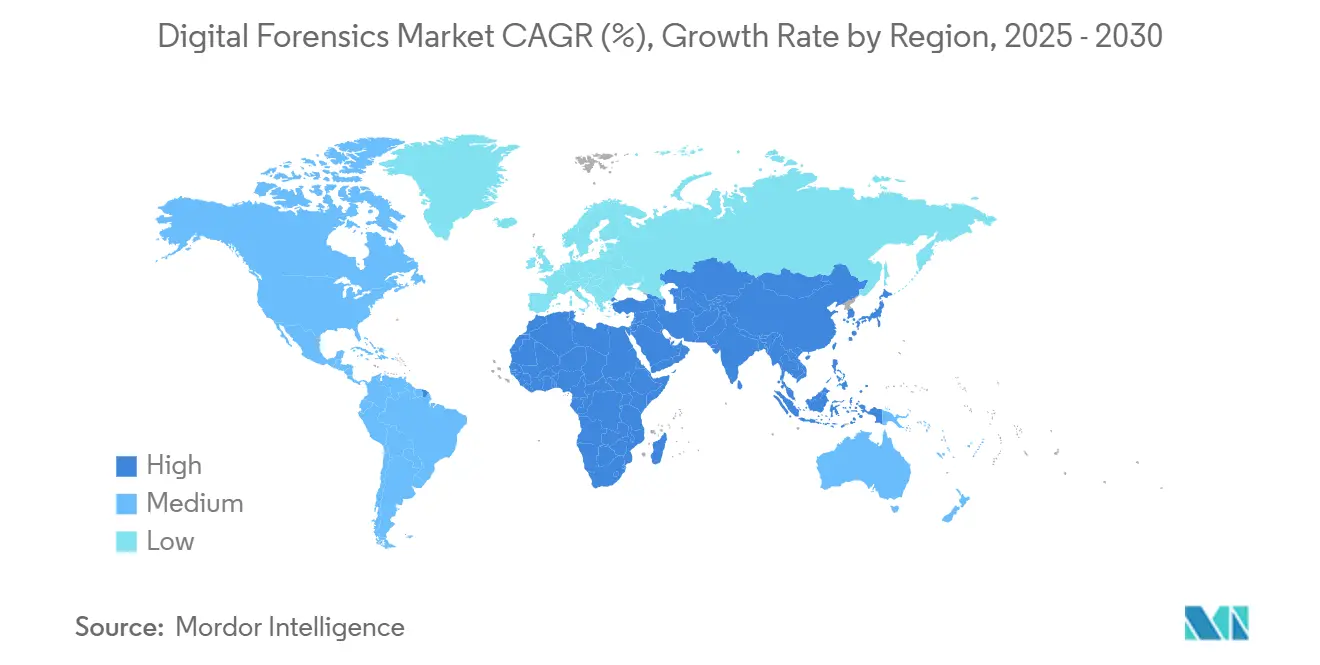

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digital Forensics Market Analysis by Mordor Intelligence

The digital forensics market size generated USD 7.51 billion in 2025 and is projected to reach USD 13.79 billion by 2030, reflecting a 12.92% CAGR. Growth pivots on cloud-native Software-as-a-Service investigations, deepfake countermeasures, and the integration of digital forensics within Extended Detection and Response platforms. Legislated mobile device extraction mandates and steady public-sector investments further underpin demand. Conversely, encryption-by-default and examiner shortages introduce operational friction yet also spur innovation in automated, cloud-based evidence preservation. Competitive dynamics remain moderately fragmented as established vendors embed artificial intelligence and blockchain-enabled chain-of-custody features to secure differentiation.

Key Report Takeaways

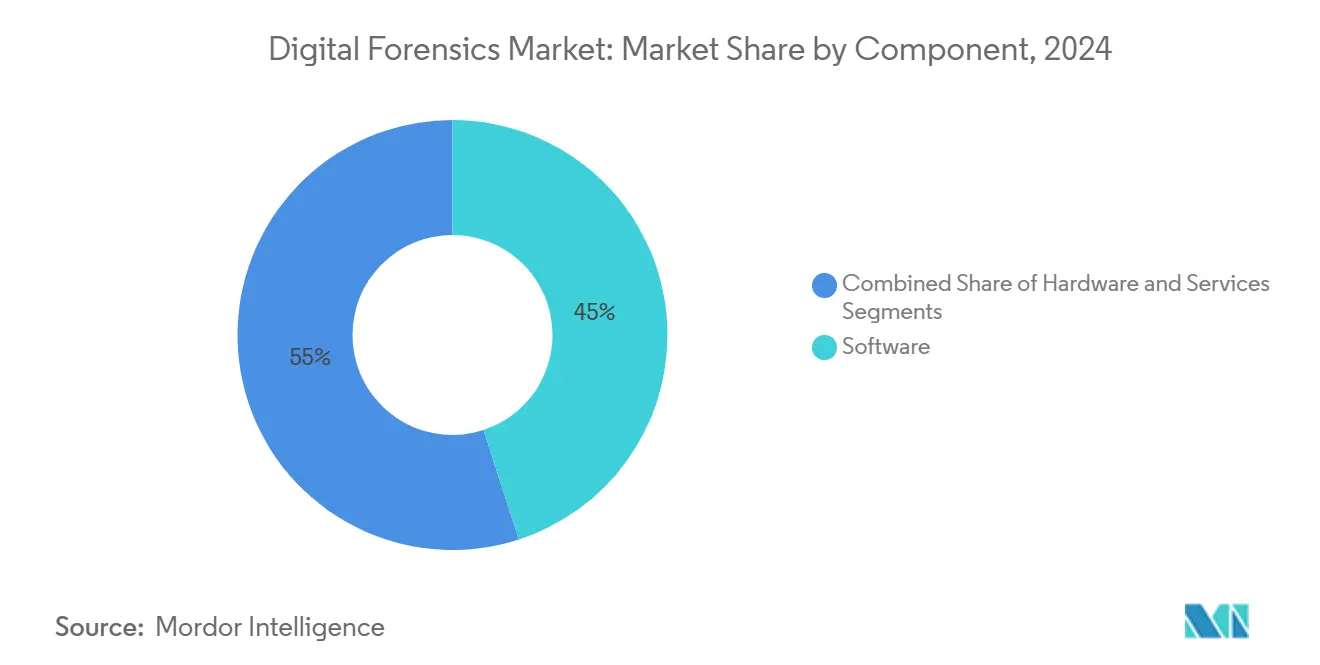

- By component, software solutions led with 45% revenue share in 2024; services are expanding at a 14.7% CAGR through 2030.

- By forensic type, computer forensics held 37% of the digital forensics market share in 2024, while cloud forensics is advancing at a 13.1% CAGR to 2030.

- By tool category, data acquisition commanded 30% of the digital forensics market size in 2024; decryption tools are projected to grow at 14.3% CAGR.

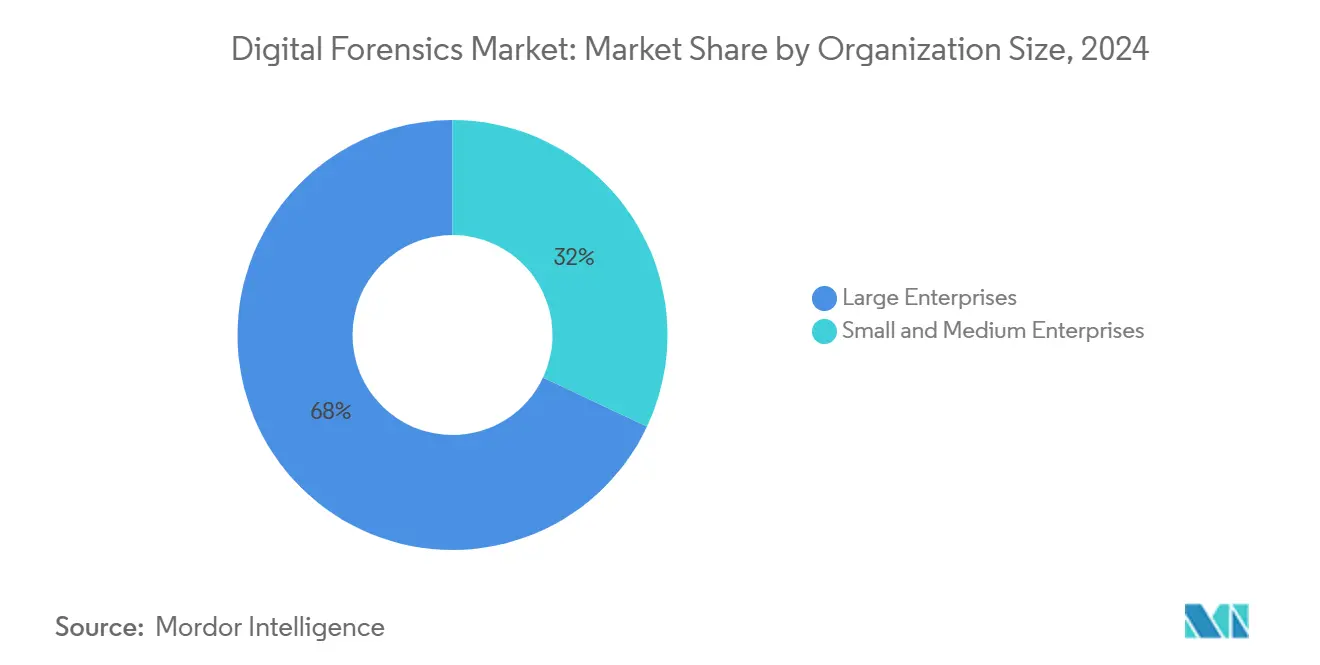

- By organization size, large enterprises accounted for 68% of demand in 2024, whereas small and medium enterprises are set to grow at 13.8% CAGR.

- By end-user vertical, government and law-enforcement bodies captured 38% revenue share in 2024; the BFSI sector is progressing at a 14.0% CAGR.

- By geography, North America led with 35% share in 2024; Asia Pacific is outpacing at 13.4% CAGR through 2030.

Global Digital Forensics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics | +2.80% | Global, with concentration in North America and EU | Medium term (2-4 years) | |

| Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs | +2.10% | Global, particularly APAC and North America | Short term (≤ 2 years) | |

| Extended Detection and Response (XDR) Adoption Necessitating Integrated DFIR Platforms | +1.90% | North America and EU, expanding to APAC | Medium term (2-4 years) | |

| Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement | +1.40% | North America and EU | Long term (≥ 4 years) | |

| Blockchain-Based Evidence Chain-of-Custody Pilots Boosting Forensic Software Upgrades | +0.80% | Global, early adoption in developed markets | Long term (≥ 4 years) | |

| Federal Cybersecurity Investments and Regulatory Compliance Requirements Expanding Forensic Deployments | +0.70% | North America | Medium term (2-4 years) |

Source: Mordor Intelligence

Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics

Cloud migrations displace traditional disk imaging, prompting deployment of forensic platforms that capture volatile data across distributed, multi-tenant environments while meeting ISO/IEC 27035-4:2024 admissibility standards[1]International Organization for Standardization, “ISO/IEC 27035-4:2024,” ISO, iso.org. Evidence isolation requirements and automated chain-of-custody tracking elevate demand for solutions pre-integrated with hyperscaler security services. As a result, vendors offering cloud-native acquisition APIs see accelerated enterprise adoption, particularly among multinational corporations navigating jurisdictional boundaries.

Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs

Machine-generated audio and video fraud now penetrates live interactions, forcing laboratories to replace legacy authentication with neural detection algorithms that achieve 91.82% accuracy on low-resolution content. BFSI institutions integrate blockchain provenance schemes to secure high-value transactions, while law-enforcement agencies invest in real-time screening tools to preserve evidentiary integrity during investigative interviews.

Extended Detection and Response Adoption Necessitating Integrated DFIR Platforms

XDR aggregates telemetry across endpoints, networks, and clouds, raising expectations that forensic workflows ingest orchestration data without disrupting incident response. CrowdStrike’s Falcon ecosystem illustrates market traction, reporting USD 3.86 billion in Annual Recurring Revenue during 2024[2]CrowdStrike Holdings, “Form 8-K,” CrowdStrike, ir.crowdstrike.com. Demand therefore concentrates on solutions that automate evidence capture, maintain legal granularity, and align with security-operations runbooks.

Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement

Recent rulings such as United States v. Brown elevate the need for tools that bypass biometric locks while preserving constitutional compliance. Vendors embed configurable legal modules to adapt extraction procedures by jurisdiction, and professional-services providers expand examiner certification programs to align with differentiated evidentiary thresholds.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost | -1.80% | Global, particularly impacting law enforcement | Short term (≤ 2 years) |

| Shortage of Court-Certified Examiners Outside Tier-1 Cities | -1.20% | Global, acute in developing regions | Medium term (2-4 years) |

| Fragmented Tool Inter-Operability Increasing Total Cost of Ownership for SMEs | -0.90% | Global, concentrated in SME segments | Medium term (2-4 years) |

| Data-Residency Rules Limiting Cross-Border Evidence Transfers (e.g., China CSL) | -0.70% | APAC, MEA, with spillover to global investigations | Long term (≥ 4 years) |

Source: Mordor Intelligence

Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost

Hardware-backed encryption reduces extraction success to below 40% on recent devices, forcing reliance on premium decryption utilities and cloud-based evidence substitutes. Small agencies face budgetary barriers, widening investigative disparity and prompting policy debate on lawful access collaboration.

Shortage of Court-Certified Examiners Outside Tier-1 Cities

Lack of standard credentialing yields uneven evidentiary quality and delays, with ISACA documenting regulatory gaps across most U.S. states. Training costs such as the USD 3,000 CDFE course limit rural uptake, spurring growth for managed forensic services while accentuating concerns over remote chain-of-custody controls.

Segment Analysis

By Component: Software Dominance Amid Service Acceleration

Software retained 45% of the digital forensics market share in 2024, underpinned by advanced analytics for encrypted and cloud evidence. Hardware usage remains niche for physical acquisitions, yet decryption accelerators support investigative throughput. Managed offerings capture enterprises seeking turnkey scalability, while professional services climb 14.7% CAGR as talent shortages persist.

Service providers capitalize on forensic-as-a-service adoption among SMEs, bundling incident response and expert testimony. Vendors integrate blockchain lineage and AI triage to compress analysis cycles, reinforcing software primacy. The strategic interplay between platform licensing and recurring services broadens revenue predictability, positioning vendors for cross-sell of adjacent security capabilities.

Note: Segment shares of all individual segments available upon report purchase

By Type: Computer Forensics Leadership Challenged by Cloud Evolution

Computer forensics controlled 37% of 2024 revenue; however, cloud forensics now logs the fastest 13.1% CAGR amid multi-cloud enterprise workloads. Mobile forensics sustains growth despite encryption headwinds, supported by evolving bypass toolkits. Network, database, and IoT investigations expand as zero-trust architectures and connected devices generate diversified evidence streams.

Regulatory audits in BFSI amplify demand for continuous cloud evidence readiness, widening opportunities for specialized cloud-native vendors. Digital forensics market size for cloud investigations is poised to narrow the gap with computer forensics by 2030 as SaaS reliance deepens. Tool vendors therefore prioritize API-based collection, volatility preservation, and jurisdictional segmentation to boost adoption.

By Tool: Data Acquisition Leads While Decryption Accelerates

Data acquisition frameworks held 30% of 2024 revenue, forming foundational layers for subsequent analytics. The segment benefits from hardware-agnostic agents that compress imaging time and auto-document chain-of-custody. Decryption utilities, projected at 14.3% CAGR, address ubiquitous encryption in consumer and enterprise assets, aligning with judicial expectations for comprehensive evidence recovery.

AI-enabled analysis suites embed machine learning to streamline anomaly recognition, and reporting modules translate forensic artifacts into courtroom-ready narratives. Emerging blockchain repositories demand specialized parsers to interrogate distributed ledger entries, further diversifying tool portfolios. Vendors pursuing consolidated platforms promote lower total cost of ownership relative to piecemeal point solutions.

By Organization Size: Enterprise Dominance with SME Acceleration

Enterprises generated 68% of 2024 demand due to stringent compliance and complex threat surfaces. Digital forensics market size growth among SMEs, forecast at 13.8% CAGR, stems from subscription-based offerings that lower capital thresholds.

Enterprises seek integrations with Security Orchestration Automated Response systems, favoring extensible APIs and federated analytics. SMEs prioritize rapid deployment and intuitive dashboards, catalyzing vendor investment in guided workflows. Marketplace optimism lies in packaging tiers that scale forensic depth with organizational maturity, enabling up-sell of advanced modules as SME cyber resilience strategies mature.

By End-user Vertical: Government Leadership with BFSI Acceleration

Government and law-enforcement agencies comprised 38% of 2024 revenue, anchored by national security funding and mobile extraction mandates. BFSI demand grows 14.0% CAGR, fueled by fraud proliferation and stringent audit expectations.

IT-telecom, healthcare, and retail maintain consistent uptake as zero-trust policies and patient-data protections intensify. Manufacturing and energy operators represent latent potential as operational technology forensics gains strategic importance for critical infrastructure defense. Vendors crafting vertical-specific solution bundles—such as transaction-oriented analytics for BFSI—secure competitive positioning.

Geography Analysis

North America held 35% of 2024 revenue, aided by Executive Order 14144 and robust federal budgets that accelerate AI-driven investigative adoption. Public-sector platform procurements, exemplified by Palantir’s USD 1.20 billion government revenue, cascade into broader ecosystem modernization.

Asia Pacific leads in growth at 13.4% CAGR, reflecting e-commerce expansion and rising cybercrime costs forecast at USD 3.3 trillion by 2025. Regulatory refinements, such as China’s eased cross-border transfer exemptions, gradually reduce investigative friction for multinational forensics providers.

Europe sustains balanced expansion through the EU AI Act and data-privacy mandates driving privacy-preserving forensic tool demand. Middle East and Africa allocate cybersecurity budgets to defend energy and financial corridors, while Latin America shows incremental progress constrained by skill shortages yet supported by regional digitalization policies.

Competitive Landscape

Market concentration remains middle-tier as incumbents fortify suites with AI triage, blockchain custody, and XDR connectors. Acquisition activity, such as Quorum Cyber’s purchase of Kivu Consulting, illustrates strategic scale-out of service depth and geographic reach. Platform convergence shapes buyer preference, rewarding vendors that deliver unified evidence pipelines from collection to courtroom reporting.

Patent output—over 6,000 digital-identity filings—signals sustained R&D, with technology majors commercializing authentication innovations that influence forensic workflows [3]EURASIP Journal Editors, “Mining Digital Identity Insights,” SpringerOpen, doi.org. Challenger firms differentiate via cloud-first architectures and elastic license models that appeal to SMEs. Integration with public-cloud telemetry and zero-knowledge encryption support remain critical gatekeepers for enterprise contracts.

Regulatory alignment capabilities become decisive as cross-border evidence rules tighten. Vendors invest in compliance engines that auto-map procedures to local statutes, thereby lowering user risk and accelerating procurement cycles. Competitive pressure also compels expansion of professional-services benches to address examiner shortages and augment recurring revenue.

Digital Forensics Industry Leaders

-

OpenText Corporation

-

Cellebrite DI Ltd.

-

Exterro Inc.

-

Magnet Forensics Inc.

-

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Ipsidy secured USD 9 million capital and signed a Fortune 500 biometric verification pilot, signaling a strategy to embed blockchain privacy controls in identity assurance stacks.

- February 2025: Palantir forecast FY 2025 revenue up to USD 3.757 billion, underscoring sustained government investment in AI-enabled forensic analytics.

- January 2025: Quorum Cyber acquired Kivu Consulting to bolster global incident-response and digital forensics reach across regulated sectors.

- January 2025: Executive Order 14144 instituted secure-software and identity-verification mandates, elevating compliance thresholds for federal forensic suppliers.

Global Digital Forensics Market Report Scope

Digital forensics is identifying, preserving, analyzing, and presenting digital evidence. Digital forensics enables the extraction of evidence by examining and evaluating data from digital devices. It is used to recover and inspect the data while maintaining its originality. The scope of the study covers the market based on various digital forensics types, such as mobile forensics, computer forensics, and network forensics, and their uses in different end-user industries worldwide.

The Digital Forensics Market is segmented by component (hardware, software, service), type (mobile forensics, computer forensics, network forensics), end-user vertical (government and law enforcement agencies, BFSI, IT and telecom), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Component | Hardware | Forensic Systems, Devices and Write Blockers | ||

| Imaging and Duplication Devices | ||||

| Other Hardware | ||||

| Software | Forensic Data Analysis and Visualization | |||

| Review and Reporting | ||||

| Forensic Decryption | ||||

| Other Software Modules | ||||

| Services | Professional Services | Incident Response and Breach Analysis | ||

| Consulting and Training | ||||

| Managed Forensic Services | ||||

| By Type | Computer Forensics | |||

| Mobile Device Forensics | ||||

| Network Forensics | ||||

| Cloud Forensics | ||||

| Database Forensics | ||||

| IoT and Embedded Device Forensics | ||||

| By Tool | Data Acquisition and Preservation | |||

| Data Recovery and Reconstruction | ||||

| Forensic Data Analysis | ||||

| Review and Reporting | ||||

| Forensic Decryption and Password Cracking | ||||

| By Organization Size | Large Enterprises | |||

| Small and Medium Enterprises | ||||

| By End-user Vertical | Government and Law Enforcement Agencies | |||

| BFSI | ||||

| IT and Telecom | ||||

| Healthcare | ||||

| Retail and E-commerce | ||||

| Energy and Utilities | ||||

| Manufacturing | ||||

| Transportation and Logistics | ||||

| Defense and Aerospace | ||||

| Education | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Nordics | ||||

| Rest of Europe | ||||

| Asia Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Singapore | ||||

| Indonesia | ||||

| Australia | ||||

| New Zealand | ||||

| Rest of Asia Pacific | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Israel | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Kenya | ||||

| Rest of Africa | ||||

By Component

| Hardware | Forensic Systems, Devices and Write Blockers | ||

| Imaging and Duplication Devices | |||

| Other Hardware | |||

| Software | Forensic Data Analysis and Visualization | ||

| Review and Reporting | |||

| Forensic Decryption | |||

| Other Software Modules | |||

| Services | Professional Services | Incident Response and Breach Analysis | |

| Consulting and Training | |||

| Managed Forensic Services | |||

By Type

| Computer Forensics |

| Mobile Device Forensics |

| Network Forensics |

| Cloud Forensics |

| Database Forensics |

| IoT and Embedded Device Forensics |

By Tool

| Data Acquisition and Preservation |

| Data Recovery and Reconstruction |

| Forensic Data Analysis |

| Review and Reporting |

| Forensic Decryption and Password Cracking |

By Organization Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-user Vertical

| Government and Law Enforcement Agencies |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Transportation and Logistics |

| Defense and Aerospace |

| Education |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Singapore | |||

| Indonesia | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the digital forensics market?

The market generated USD 7.51 billion in 2025 and is forecast to reach USD 13.79 billion by 2030 at a 12.92% CAGR.

Which component segment is growing fastest?

Services are expanding at a 14.7% CAGR as organizations outsource complex investigations to managed providers.

Why is cloud forensics gaining momentum?

Enterprise migration to multi-cloud environments necessitates specialized evidence preservation, driving a 13.1% CAGR for cloud forensics tools.

Which region leads market share and which grows fastest?

North America holds 35% share, while Asia Pacific registers the highest 13.4% CAGR through 2030.

Page last updated on: July 7, 2025