Commercial Aircraft Maintenance, Repair, And Overhaul (MRO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

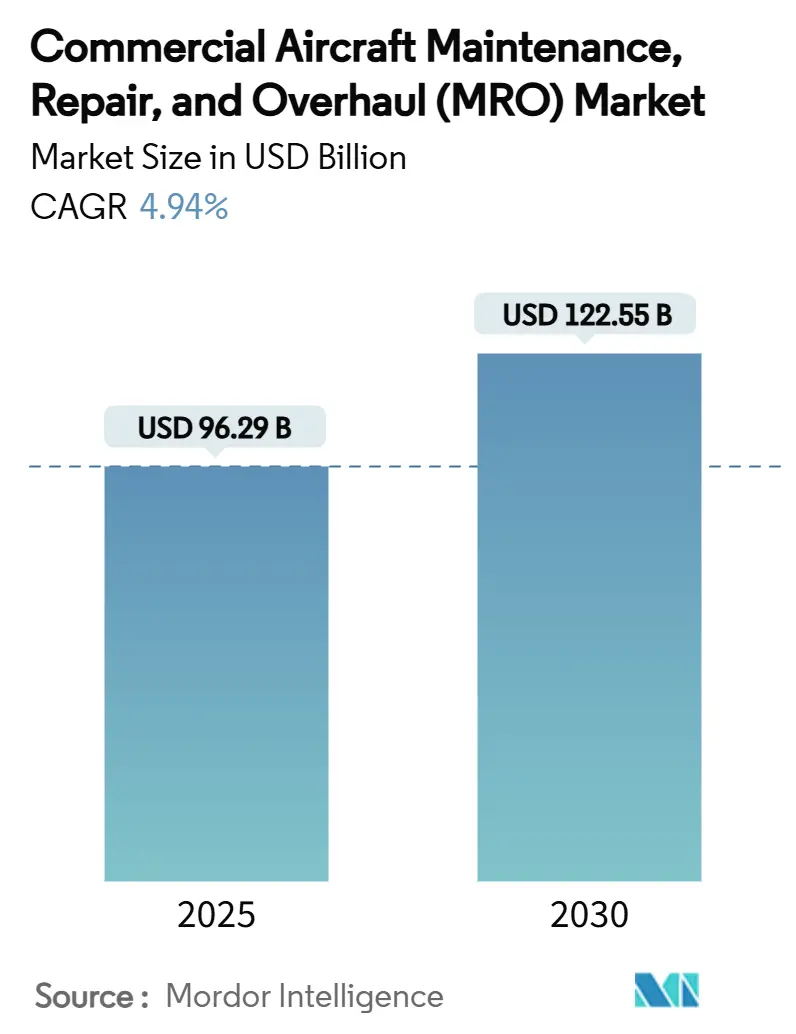

| Market Size (2025) | USD 96.29 Billion |

| Market Size (2030) | USD 122.55 Billion |

| Growth Rate (2025 - 2030) | 4.94% CAGR |

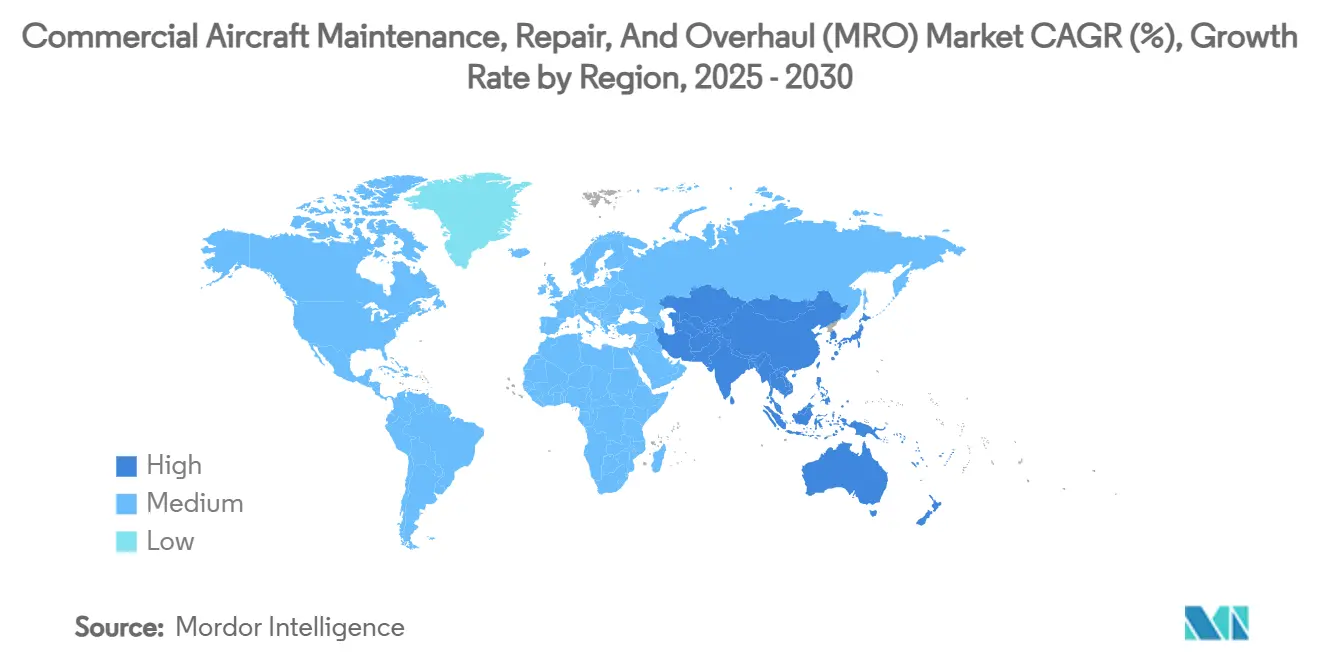

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Aircraft Maintenance, Repair, And Overhaul (MRO) Market Analysis by Mordor Intelligence

The commercial aircraft MRO market stood at USD 96.29 billion in 2025 and is forecasted to reach a market size of USD 122.55 billion by 2030, advancing at a 4.94% CAGR. Fleet operators continued to extend asset lives, so heavy checks and engine shop visits remained the dominant spending categories. Growing investment by original equipment manufacturers (OEMs) in global service networks and airlines’ focus on rapid aircraft-turn capability added structural demand for digital line-maintenance solutions. Consolidation among independent providers accelerated because scale is essential for supply-chain resilience and data-driven services. At the same time, technician shortages and engine-shop bottlenecks limited near-term capacity expansion despite solid traffic recovery.

Key Report Takeaways

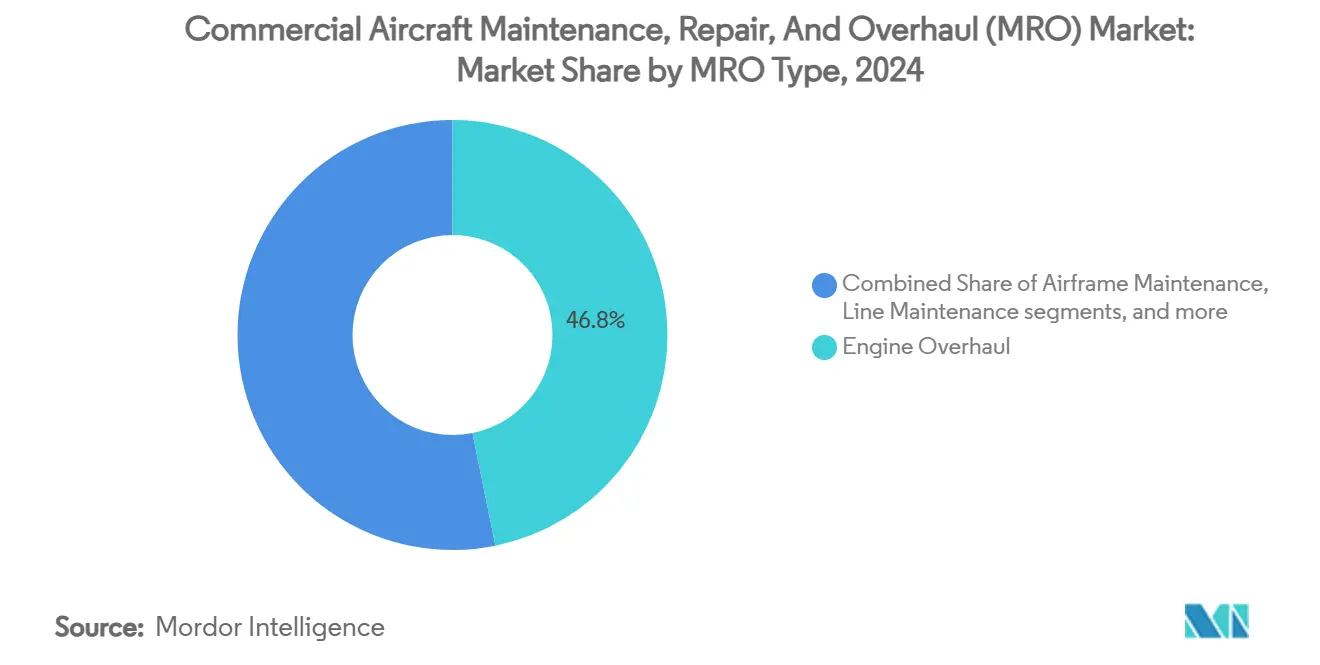

- By MRO type, engine overhaul led with 46.80% of the commercial aircraft MRO market share in 2024, while line maintenance is projected to grow at a 5.71% CAGR to 2030.

- By aircraft type, fixed-wing platforms accounted for 95.45% of the commercial aircraft MRO market in 2024; rotary-wing MRO is expected to expand at a faster 4.78% CAGR through 2030.

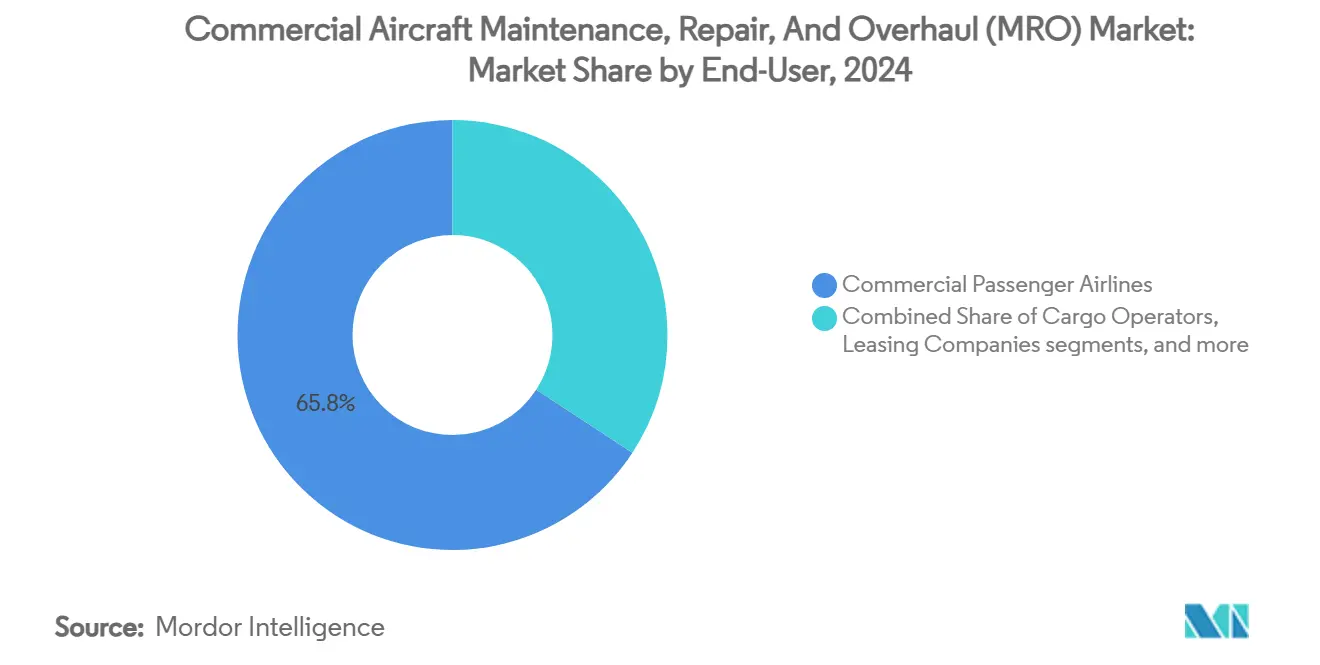

- By end user, commercial passenger airlines held 78.85% revenue share in 2024, whereas charter operators show the highest forecast CAGR at 5.37% to 2030.

- By service-provider type, independent third-party MROs commanded 49.32% of revenue in 2024, yet OEM-affiliated facilities are pacing ahead at a 5.30% CAGR.

- By region, North America captured 38.98% of 2024 revenue, while Asia-Pacific is the fastest-growing geography at a 5.12% CAGR, supported by pro-MRO policy incentives.

Global Commercial Aircraft Maintenance, Repair, And Overhaul (MRO) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging global fleet necessitating heavy checks | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| OEM aftermarket strategy expansion | +0.8% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Surging narrowbody utilization post-COVID | +0.9% | Global, strongest in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Regional government incentives for indigenous MRO | +0.6% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| AI-driven predictive maintenance adoption | +0.5% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Used-serviceable-material (USM) supply chain formalization | +0.4% | Global, with early gains in North America | Medium term (2-4 years) |

Source: Mordor Intelligence

Aging Global Fleet Necessitating Heavy Checks

Average fleet age climbed as carriers deferred retirements because new-delivery slots stayed scarce. Older jets require deeper structural inspections, corrosion control, and component replacements, which lift heavy-maintenance labour hours per airframe. Independent hangars in North America and Europe continued to book multi-year heavy-check contracts, securing stable revenue visibility for the aircraft MRO market.

OEM Aftermarket Strategy Expansion

OEMs invested more than USD 2 billion in service-network additions spanning the United States, Europe, and Asia. GE Aerospace alone committed USD 1 billion to enlarge its overhaul footprint, while Safran earmarked EUR 1 billion (USD 1.18 billion) to lift annual LEAP-engine shop-visit capacity to 1,200 units.[1]Source: Safran, “Safran Invests Over EUR 1 Billion to Develop a Global MRO Network for its LEAP Engine,” safran-group.com These moves tightened OEM control of proprietary repair data and attracted airline power-by-the-hour contracts that enlarge the aircraft MRO market.

Surging Narrow-Body Utilization Post-COVID

Single-aisle daily cycles surpassed 2019 levels as airlines prioritised short-haul frequencies. Higher utilisation raised unscheduled component removals and accelerated line-maintenance demand around hub airports. Providers that invested in mobile inspection rigs and digital slot-planning tools captured an incremental share of the aircraft MRO market, especially in Asia’s fast-turn environments.

Regional Government Incentives for Indigenous MRO

India removed goods-and-services-tax barriers and allowed 100% foreign direct investment in maintenance facilities, stimulating projects such as Air India’s 35-acre Bengaluru complex.[2]Source: Safran, “Safran Invests Over EUR 1 Billion to Develop a Global MRO Network for its LEAP Engine,” safran-group.com Source: Air India, “Air India Commences Construction of Mega MRO Facility in Bengaluru,” airindia.com Singapore’s Aviation Development Fund offered matched-investment grants, while Indonesia expanded free-trade zones around Batam. These policy measures drew fresh capital, diversified the supply base, and bolstered Asia-Pacific’s contribution to the aircraft MRO market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of licensed A&P technicians | -0.9% | Global, most severe in North America | Short term (≤ 2 years) |

| Persistent engine shop visit capacity crunch | -0.7% | Global, concentrated in major MRO hubs | Medium term (2-4 years) |

| Tier-2 component supply chain volatility | -0.5% | Global, with regional variations | Medium term (2-4 years) |

| OEM price escalation on spare parts | -0.4% | Global, affecting all market segments | Long term (≥ 4 years) |

Source: Mordor Intelligence

Acute Shortage of Licensed A&P Technicians

Retirement-driven attrition outpaced new entrants, especially in the United States, where training enrolments trended flat. Airlines offered premium overtime rates and accelerated apprenticeship programs, but labour scarcity still stretched turnaround times and limited incremental hangar capacity, holding back aircraft MRO market growth.

Persistent Engine Shop-Visit Capacity Crunch

Unexpected durability findings on next-generation turbofans pushed up shop-visit rates. Simultaneously, parts shortages lengthened work scopes, so several global engine centres ran near full utilisation. Carriers booked slots more than a year ahead, and some leased spare engines to safeguard schedules, which raised direct maintenance costs within the aircraft MRO market.

Segment Analysis

By MRO Type: Engine Work Commands Investment

Engine overhaul generated 46.80% of 2024 revenue, underscoring the capital-intensive nature of powerplant maintenance within the aircraft MRO market. OEM-certified centres expanded tooling lines for LEAP and GTF variants, while independents specialised in mature engine families to retain competitiveness. The commercial aircraft MRO market size linked to engine work is expected to advance as shop-visit intervals settle into post-pandemic patterns.

Line maintenance showed the highest 5.71% CAGR outlook because quick-turn services maximise operator revenue days. Tablet-based inspection apps and wearable head-up displays shortened routine checks, improving gate-time discipline. As airline schedules densified, providers with on-airport teams captured incremental share and reinforced the broader commercial aircraft MRO market growth trajectory.

Note: Segment shares of all individual segments available upon report purchase

By Aircraft Type: Fixed-Wing Dominates, Rotary Niche Grows

Fixed-wing fleets held 95.45% revenue share in 2024 and continue to anchor demand owing to the scale of commercial jet operations. Narrowbody aircraft drive a sizable portion of the commercial aircraft MRO market size, with utilisation patterns increasing task card frequency on airframe and component lines. Widebody heavy checks remained steady because long-haul traffic recovery continued at a measured pace.

The demand for rotary-wing aircraft is smaller yet resilient because defence modernisation and offshore energy programs need helicopters with high availability. Specialised rotor-blade overhaul capability, strict airworthiness requirements, and government budget visibility produce stable margins. Providers that secured military contracts added a predictable revenue stream that buffers cyclicality in the fixed-wing dominated commercial aircraft MRO market.

By End User: Airline Scale Meets Charter Agility

Commercial passenger carriers comprised 78.85% of spending in 2024. Fleet-spanning maintenance programs and power-by-the-hour agreements allowed airlines to pool volume discounts and reduce unit costs, reinforcing their leadership in the commercial aircraft MRO market.

Charter operators, while smaller, are slated to grow at 5.37% CAGR. Business clients prize rapid return-to-service times and tailored cabin refurbishment, which bring higher labour yields per aircraft. Providers offering dedicated bays for mid-size jets attracted premium work scopes, diversifying overall commercial aircraft MRO market revenue streams.

By Service Provider Type: Independents Hold Scale, OEMs Gain Ground

Independent third-party shops retained 49.32% revenue in 2024 because flexible labour models and competitive pricing attracted cost-sensitive airlines. Several independents pursued consolidation; AAR’s USD 845 million acquisition of Triumph Group’s product support business broadened US and Asia component-repair capacity.[3]Source: AAR Corp, “AAR Completes Acquisition of Triumph Product Support,” aarcorp.com

OEM-affiliated facilities are outpacing market growth and are supported by proprietary tooling, technical data, and long-term service contracts. GE Aerospace’s USD 267 million XEOS plant in Poland exemplified capacity build-out aligned with LEAP engines. This integration recaptured high-value work from independents and tilted competitive dynamics across the commercial aircraft MRO market.

Geography Analysis

North America generated 38.98% of 2024 revenue from the region’s large active fleets and mature maintenance ecosystems. Major Atlanta, Dallas, and Miami hubs offered comprehensive engine, component, and heavy-check capability and efficient logistics. Recent investments, such as Pratt & Whitney’s agreement with Delta TechOps to lift GTF throughput by 30%, reinforced capacity. Strong certification standards and digital adoption sustained productivity growth, keeping the commercial aircraft MRO market competitive despite higher labour rates.

Asia-Pacific delivered the fastest 5.12% CAGR outlook as carriers expanded fleets and governments incentivised domestic maintenance. Singapore Aero Engine Services announced USD 242 million in new facilities, while Air India started work on a 35-acre Bengaluru campus, which is expected to create 1,200 jobs. These expansions help retain regional spend that previously moved to Europe or the Middle East and raise Asia’s contribution to the commercial aircraft MRO market.

Europe remained a technology leader but faced cost pressure. Lufthansa Technik approved a multi-billion euro investment program that included a new heavy-maintenance site in Portugal to secure future wide-body workload. Eastern European countries offered competitive labour costs, attracting engine-overhaul facilities such as XEOS in Poland. The Middle East used geographic connectivity to attract transit-related checks. South America developed niche component-repair clusters to support cargo fleets, ensuring balanced commercial aircraft MRO market development worldwide.

Competitive Landscape

Competition stayed moderate but trended toward consolidation as scale became vital for digital investments and supply-chain leverage. Boeing’s USD 8.3 billion agreement to purchase Spirit AeroSystems aimed to control quality and synchronize production lines, indicating airframe OEM interest in tighter vertical integration. Independent leader AAR finalised several purchases that expanded component-repair capacity and broadened geographical reach.

Digital capability emerged as a key differentiator. Lufthansa Technik introduced its Digital Tech Ops Ecosystem with Avianca to roll out predictive maintenance analytics across mixed fleets. Safran boosted engine-health-monitoring tools alongside its global network expansion, while IFS’s acquisition of EmpowerMX strengthened cloud-based maintenance execution software.

Labour deficits and supply-chain risk encouraged joint ventures that combine capital, technology, and location advantages. GE Aerospace partnered with Lufthansa Technik for the XEOS venture, tapping German engineering expertise and Polish cost competitiveness. West Star Aviation’s sale to Greenbriar Equity highlighted private-equity interest in specialised business-aviation MRO niches. Providers able to deliver integrated, tech-enabled services positioned themselves to win longer-term contracts and grow share in the commercial aircraft MRO market.

Commercial Aircraft Maintenance, Repair, And Overhaul (MRO) Industry Leaders

-

Lufthansa Technik AG

-

AAR CORP.

-

Delta Air Lines, Inc.

-

Hong Kong Aircraft Engineering Company Limited (HAECO)

-

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Aerospace and Lufthansa Technik opened Poland's USD 267 million XEOS LEAP engine centre, targeting 250 annual overhauls.

- October 2024: GE Aerospace announced its plans to invest over USD 130 million in its Maintenance, Repair, and Overhaul (MRO) and component repair facilities in Europe by the end of 2026 as part of its global USD 1 billion MRO spending initiative. The initiative aims to enhance capacity, reduce turnaround times, and expand repair capabilities with advanced technologies.

Global Commercial Aircraft Maintenance, Repair, And Overhaul (MRO) Market Report Scope

Aircraft MRO refers to overhaul, inspection, repair, or modification of an aircraft or its components.

The aircraft maintenance, repair, and overhaul (MRO) market is segmented by MRO type and geography. The market is segmented by MRO type into airframe, engine, component, and line maintenance. The cabin interior modifications and repairs have been considered with the component segment. The scope of the study is limited to MRO services in commercial aircraft, and it does not encompass military and general aviation aircraft. The report also covers the market sizes and forecasts for the aircraft MRO market in major countries across different regions. The market size is provided for each segment in terms of value (USD).

| By MRO Type | Airframe Maintenance | |||

| Engine Overhaul | ||||

| Component Repair and Overhaul | ||||

| Line Maintenance | ||||

| By Aircraft Type | Fixed-Wing | Narrowbody Aircraft | ||

| Widebody Aircraft | ||||

| Regional Transport Aircraft | ||||

| Rotary Wing | ||||

| By End User | Commercial Passenger Airlines | |||

| Cargo Operators | ||||

| Leasing Companies | ||||

| Charter Operators | ||||

| By Service Provider Type | Airline-Affiliated MROs | |||

| Independent Third-Party MROs | ||||

| OEM-Affiliated MROs | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Airframe Maintenance |

| Engine Overhaul |

| Component Repair and Overhaul |

| Line Maintenance |

| Fixed-Wing | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Transport Aircraft | |

| Rotary Wing |

| Commercial Passenger Airlines |

| Cargo Operators |

| Leasing Companies |

| Charter Operators |

| Airline-Affiliated MROs |

| Independent Third-Party MROs |

| OEM-Affiliated MROs |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the aircraft MRO market?

The aircraft MRO market was valued at USD 96.29 billion in 2025 and is projected to reach USD 122.55 billion by 2030, advancing at a 4.94% CAGR.

Which MRO segment generates the most revenue?

Engine overhaul leads, capturing 46.80% of 2024 revenue, largely due to the complexity and cost of modern powerplants.

Which region is growing fastest in aircraft maintenance?

Asia-Pacific shows the highest forecast CAGR of 5.12% through 2030, supported by government incentives and rising fleet counts.

How are OEMs changing the competitive landscape?

OEMs are investing billions to expand branded service networks, leveraging proprietary data and tooling to win long-term maintenance contracts.

What is the biggest challenge facing MRO providers today?

A shortage of licensed technicians and limited engine shop capacity are the most immediate constraints, prolonging turnaround times and pushing costs higher.

Why is line maintenance expected to grow quickly?

Airlines need rapid aircraft-turn capability to maximise daily utilization, so demand for on-airport, technology-enabled line maintenance is rising faster than other categories.

Page last updated on: July 3, 2025